|

|

市場調査レポート

商品コード

1567826

北米のデータコンバータ:2030年市場予測-地域別分析:タイプ、解像度、コンバータ率、エンドユーザー別North America Data Converter Market Forecast to 2030 - Regional Analysis - by Type, Resolution, Rate of Converter, and End user |

||||||

|

|||||||

|

|||||||

| 北米のデータコンバータ:2030年市場予測-地域別分析:タイプ、解像度、コンバータ率、エンドユーザー別 |

|

出版日: 2024年08月07日

発行: The Insight Partners

ページ情報: 英文 147 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

北米のデータコンバータ市場は、2022年に18億2,109万米ドルと評価され、2030年には31億7,320万米ドルに達すると予測され、2022年から2030年までのCAGRは7.2%と推定されます。

先進5Gインフラ開拓におけるデータコンバータ利用の拡大が北米のデータコンバータ市場を牽引

5Gは、旧世代と比較してより高い周波数と広い帯域幅で動作します。基地局からユーザー機器に至るまで、5Gインフラが世界中で拡大するにつれ、効率的な信号処理のために高速データ・コンバータの必要性がさまざまな分野で高まる。複数の機器から大量のデータが生成され、スマートフォン別データ消費量が増加するため、ルーター、中継器、無線アンテナ、アクセスポイントなど、無線ネットワークで使用される広帯域機器では、今後数年間、データネットワークの混雑が発生します。5G技術の展開は、高速通信ネットワークとネットワークの輻輳制御の需要を押し上げると予想されます。5G技術により、現在の4Gや3Gネットワークよりも高速なデータ転送速度が可能になると予想されます。5Gインフラの成長により、モバイル加入者数は大幅に増加し、ユーザーのデータ要求に対応できるインフラが必要となります。

各国政府は、5Gインフラの増強に向けた取り組みを進めています。2023年9月、米国国立科学財団(NSF)の技術・イノベーション・パートナーシップ局(TIP)は、5つのコンバージェンス・チームをNSFコンバージェンスのフェーズ1からフェーズ2に進めるために2,500万米ドルを投資し、5G通信インフラと運用の課題に取り組むと発表しました。NSFは、トラックGのフェーズ1に16チームを選定しました。今後2年間、フェーズ2のチームは、技術開発、知的財産、財務管理と計画、持続可能性計画、コミュニケーションとアウトリーチを含むイノベーションと起業家カリキュラムに参加します。2023年4月、米国のジーナ・M・ライモンド商務長官は、オープンで相互運用可能なネットワークの開発に15億米ドルを投資することを目的とした「パブリック・ワイヤレス・サプライチェーン・イノベーション・ファンド」の立ち上げを発表しました。2022年CHIPS・科学法(CHIPS and Science Act of 2022)により資金提供されたこの投資は、バイデン=ハリス政権の「アメリカへの投資(Investing in America)」アジェンダの一環であり、無線技術革新の推進、競争の促進、サプライチェーンの強靭性強化を目的としています。このように、5Gインフラの開発におけるデータ・コンバータの利用拡大や政府のイニシアティブの高まりは、今後数年間、北米データ・コンバータ市場に大きなビジネスチャンスをもたらすと期待されています。

北米のデータコンバータ市場の概要

北米のデータコンバータ市場は米国、カナダ、メキシコに区分されます。この地域の市場成長は、ヘルスケアアプリケーションにおける高解像度画像に対する需要の高まりに起因しています。画質の向上により、あらゆる疾患の迅速な診断と治療が可能になり、医師の生産性が向上します。技術的に進んだデータ収集システムでデータ・コンバータの採用が増加していることが、北米市場の成長をさらに後押ししています。エレクトロニクス業界は、柔軟なソフトウェアとモジュール式ハードウェアを組み合わせた動向にシフトしています。複数の市場プレーヤーが、データ収集システムに使用されるデータ・コンバータを導入しています。例えば、テキサス・インスツルメンツ(TXN)は2023年11月、スペース・ハイグレード・プラスチック(SHP)と呼ばれるデバイス・スクリーニング仕様と、SHP互換のアナログ・デジタル・コンバータ(ADC)、すなわちADC12DJ5200-SPとADC12QJ1600-SPを発表しました。TXNはまた、パルス幅変調(PWM)コントローラの新ファミリであるTPS7H5005-SEPにより、耐放射線性スペース・エンハンスト・プラスチック(スペースEP)ポートフォリオを強化しました。同様に2021年12月、テキサス・インスツルメンツ・インコーポレイテッドは最小24ビット広帯域アナログ・デジタル・コンバータ(ADC)を発表しました。このコンバータは、より広い帯域幅で業界をリードする信号測定精度を実現するのに役立ちます。ADS127L11は、50%小型化されたパッケージで超高精度データ収集を実現し、幅広い産業用システムの消費電力、測定帯域幅、分解能を大幅に最適化します。このように、これらすべての要因が、予測期間中の北米におけるデータ・コンバータの需要を押し上げています。Balanceが発表した記事によると、2022年、自動車産業は米国経済に毎年1兆米ドル以上の貢献をしています。自動車産業では、データ・コンバータは、他の車両や固定ネットワークと通信するためのワイヤレス・トランシーバなど、さまざまな用途に使用されています。また、車載レーダー、LiDAR、カメラなどのアナログ・センサにはADCインターフェースが必要です。このように、自動車産業におけるデータ・コンバータの用途拡大が、データ・コンバータ市場を後押ししています。

Texas Instruments Incorporated社、Analog Devices社、Omni Design Technologies社、Synopsys社、Microchip Technology社が北米で事業を展開する主要データ・コンバータ・メーカーです。したがって、上記のパラメータが北米のデータコンバータ市場の成長を促進しています。

北米のデータコンバータ市場の収益と2030年までの予測(金額)

北米のデータコンバータ市場セグメンテーション

北米のデータコンバータ市場は、タイプ、解像度、コンバータ率、エンドユーザー、国に分類されます。

タイプ別では、北米のデータコンバータ市場はADCとDACに二分されます。2022年の市場シェアはADCセグメントが大きいです。

分解能別では、北米のデータコンバータ市場は10ビット、12ビット、14ビット、16ビット、その他に区分されます。2022年には、その他セグメントが最大の市場シェアを占めました。10ビットセグメントはさらに、50Mspsまで、51~100Msps、101~200Msps、201~500Msps、501Msps~1Gsps、1Gsps以上にサブセグメント化されます。12ビットセグメントはさらに、50Mspsまで、51~100Msps、101~200Msps、201~500Msps、501Msps~1Gsps、1Gsps以上にサブセグメント化されます。14ビットセグメントはさらに、50Mspsまで、51~100Msps、101~200Msps、201~500Msps、501Msps~1Gsps、1Gsps以上にサブセグメント化されます。16ビットセグメントはさらに、50Mspsまで、51~100Msps、101~200Msps、201~500Msps、501Msps~1Gsps、1Gsps以上にサブセグメント化されます。その他ビットセグメントは、さらに50Mspsまで、51~100Msps、101~200Msps、201~500Msps、501Msps~1Gsps、1Gsps以上に細分化されます。

コンバータの速度に基づいて、北米のデータコンバータ市場は50Mspsまで、51~100Msps、101~200Msps、201~500Msps、501Msps~1Gsps、1Gsps以上に区分されます。501Msps~1Gspsのセグメントが2022年に最大の市場シェアを占めました。

エンドユーザー別では、北米のデータコンバータ市場は自動車、通信、家電、産業、医療、その他に区分されます。2022年には民生用電子機器セグメントが最大の市場シェアを占めました。

国別では、北米のデータコンバータ市場は米国、カナダ、メキシコに区分されます。2022年の北米のデータコンバータ市場シェアは米国が独占しました。

Analog Devices Inc、Asahi Kasei Microdevices Corp、Cirrus Logic Inc、Microchip Technology Inc、On Semiconductor Corp、Renesas Electronics Corp、ROHM Co Ltd、STMicroelectronics NV、Teledyne Technologies Inc、Texas Instruments Incなどが北米のデータコンバータ市場で事業を展開する主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米のデータコンバータ市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 北米のデータコンバータ市場:主要市場力学

- 市場促進要因

- エンドユーザーによる試験・計測需要の増加

- 無線通信におけるデータコンバータの需要増加

- 製品上市の増加

- 市場抑制要因

- ADCの複雑な設計

- 原材料コストの変動

- 市場機会

- IoTデバイスとデータ消費の潜在的用途

- 高度な5Gインフラの開発におけるデータ・コンバータの利用拡大

- 今後の動向

- 高速データコンバータの台頭

- 促進要因と抑制要因の影響

第6章 データコンバータ市場:北米分析

- 北米のデータコンバータ市場収益(2020年~2030年)

- 北米のデータコンバータ市場予測分析

第7章 北米のデータコンバータ市場分析:タイプ別

- ADC

- DAC

第8章 北米のデータコンバータの市場分析:解像度別

- ビット

- 12ビット

- 14ビット

- 16ビット

- その他

第9章 北米のデータコンバータ市場分析-コンバータ率別

- 50Msps以下

- 51~100Msps

- 101~200Msps以下

- 201~500Msps

- 501~1Gps

- 1Gsps以上

第10章 北米のデータコンバータ市場分析-エンドユーザー別

- 自動車

- 通信

- コンシューマー・エレクトロニクス

- 産業用

- 医療

- その他

第11章 北米のデータコンバータ市場:国別分析

- 米国

- カナダ

- メキシコ

第12章 競合情勢

- 主要プレーヤーによるヒートマップ分析

- 企業のポジショニングと集中度

第13章 業界情勢

- 市場イニシアティブ

- 製品開発

第14章 企業プロファイル

- Texas Instruments Inc

- STMicroelectronics NV

- Renesas Electronics Corp

- ROHM Co Ltd

- Analog Devices Inc

- Cirrus Logic Inc

- Asahi Kasei Microdevices Corp

- Microchip Technology Inc

- On Semiconductor Corp

- Teledyne Technologies Inc

第15章 企業概要付録

List Of Tables

- Table 1. North America Data Converter Market Segmentation

- Table 2. List of Vendors

- Table 3. North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Table 4. North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million) - by Type

- Table 5. North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million) - by Resolution

- Table 6. North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million) - by Rate Of Converter

- Table 7. North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million) - by End user

- Table 8. North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Country

- Table 9. United States: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Type

- Table 10. United States: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Resolution

- Table 11. United States: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Rate Of Converter

- Table 12. United States: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by End user

- Table 13. Canada: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Type

- Table 14. Canada: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Resolution

- Table 15. Canada: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Rate Of Converter

- Table 16. Canada: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by End user

- Table 17. Mexico: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Type

- Table 18. Mexico: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Resolution

- Table 19. Mexico: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by Rate Of Converter

- Table 20. Mexico: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million) - by End user

- Table 21. Heat Map Analysis by Key Players

- Table 22. List of Abbreviation

List Of Figures

- Figure 1. North America Data Converter Market Segmentation, by Country

- Figure 2. Ecosystem: North America Data Converter Market

- Figure 3. North America Data Converter Market - Key Market Dynamics

- Figure 4. Impact Analysis of Drivers and Restraints

- Figure 5. North America Data Converter Market Revenue (US$ Million), 2020 - 2030

- Figure 6. North America Data Converter Market Share (%) - by Type (2022 and 2030)

- Figure 7. ADC: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. DAC: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. North America Data Converter Market Share (%) - by Resolution (2022 and 2030)

- Figure 10. 10 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. 12 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. 14 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. 16 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Others: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. North America Data Converter Market Share (%) - by Rate Of Converter (2022 and 2030)

- Figure 16. Upto 50 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. 51 to 100 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. 101 to 200 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. 201 to 500 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 20. 501 Msps to 1 Gsps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Above 1 Gsps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. North America Data Converter Market Share (%) - by End user (2022 and 2030)

- Figure 23. Automotive: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 24. Communications: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 25. Consumer Electronics: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 26. Industrial: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 27. Medical: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 28. Others: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 29. North America Data Converter Market Breakdown, by Key Countries - Revenue (2022) (US$ Million)

- Figure 30. North America Data Converter Market Breakdown, by Key Countries, 2022 and 2030 (%)

- Figure 31. United States: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million)

- Figure 32. Canada: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million)

- Figure 33. Mexico: North America Data Converter Market - Revenue and Forecast to 2030(US$ Million)

- Figure 34. Company Positioning & Concentration

The North America data converter market was valued at US$ 1,821.09 million in 2022 and is expected to reach US$ 3,173.20 million by 2030; it is estimated to register a CAGR of 7.2% from 2022 to 2030 .

Growing Use of Data Converters in Developing Advanced 5G Infrastructure Fuel North America Data Converter Market

5G operates at higher frequencies and wider bandwidths compared to previous generations. As 5G infrastructure expands across the world, from base stations to user devices, the need for high-speed data converters will grow across various segments for efficient signal processing. Due to the massive amount of data produced by several devices and increased data consumption by smartphones, high-bandwidth equipment used in wireless networks such as routers, repeaters, wireless antennas, and access points will experience congestion in data networking in the coming years. The deployment of 5G technology is anticipated to boost the demand for high-speed communication networks and network congestion control. The 5G technology is expected to enable aggregate data rates that are faster than those of the current 4G and 3G networks. The growth of 5G infrastructure would significantly increase the number of mobile subscribers, forming a requirement for developed infrastructure that can handle user data requests.

Governments of many countries are taking initiatives to increase their 5G infrastructure. In September 2023, the US National Science Foundation Directorate for Technology, Innovation and Partnerships (TIP) announced that it is tackling 5G communication infrastructure and operational challenges through a US$ 25 million investment to advance five convergent teams from Phase 1 to Phase 2 of NSF Convergence. NSF selected 16 teams for Phase 1 of Track G. Over the next two years, the Phase 2 teams will take part in an innovation and entrepreneurial curriculum that includes technology development, intellectual property, financial management and planning, sustainability planning, and communications and outreach. In April 2023, US Secretary of Commerce Gina M. Raimondo announced the launch of the Public Wireless Supply Chain Innovation Fund, which aimed to invest US$ 1.5 billion in the development of open and interoperable networks. Funded by the CHIPS and Science Act of 2022, this investment is part of the Biden-Harris Administration's Investing in America agenda, aiming to drive wireless innovation, foster competition, and strengthen supply chain resilience. Thus, the growing use of data converters in developing 5G infrastructure and increasing government initiatives are expected to offer significant opportunities for the North America data converter market in the coming years.

North America Data Converter Market Overview

The North America data converter market is segmented into the US, Canada, and Mexico. The market growth in the region is attributed to the rising demand for high-resolution images in healthcare applications. The improved image quality can enable quick diagnosis and treatment of any disease, enhancing physicians' productivity. The rising adoption of data converters in technologically advanced data acquisition systems further drives the growth of the market in North America. The electronics industry is shifting toward a trend that combines flexible software and modular hardware. Several market players are introducing data converters used in data acquisition systems. For instance, in November 2023, Texas Instruments TXN introduced device-screening specifications called space high-grade plastic (SHP) and SHP-compatible analog-to-digital converters (ADCs), namely ADC12DJ5200-SP and ADC12QJ1600-SP. TXN also bolstered its radiation-tolerant Space Enhanced Plastic (Space EP) portfolio with a new family of pulse-width modulation (PWM) controllers, namely TPS7H5005-SEP. Similarly, in December 2021, Texas Instruments Incorporated introduced the minimum 24-bit wideband analog-to-digital converter (ADC). The converter helps deliver industry-leading signal-measurement precision at wider bandwidths. The ADS127L11 can achieve ultra-precise data acquisition in a 50% smaller package, considerably optimizing power consumption, measurement bandwidth, and resolution for a wide range of industrial systems. Thus, all these factors surge the demand for data converters in North America during the forecast period. According to the article published by the Balance, in 2022, the automotive industry contributes more than US$ 1 trillion to the US economy each year. In the automotive industry, data converters are used for various applications, including wireless transceivers, to communicate with other vehicles or with a fixed network. Also, analog sensors such as automotive radar, LiDAR, and cameras require an ADC interface. Thus, the increasing application of data converters in the automotive industry is favoring the data converters market.

Texas Instruments Incorporated, Analog Devices, Omni Design Technologies, Synopsys, and Microchip Technology are the key data converter manufacturers operating in North America. Therefore, the parameters mentioned above are driving the growth of the North America data converter market.

North America Data Converter Market Revenue and Forecast to 2030 (US$ Million)

North America Data Converter Market Segmentation

The North America data converter market is categorized into type, resolution, rate of converter, end user, and country.

Based on type, the North America data converter market is bifurcated ADC and DAC. The ADC segment held a larger market share in 2022.

By resolution, the North America data converter market is segmented into 10 bit, 12 bit, 14 bit, 16 bit, and others. The others segment held the largest market share in 2022. The 10 bit segment is further sub segmented into Upto 50 Msps, 51 to 100 Msps, 101 to 200 Msps, 201 to 500 Msps, 501 Msps to 1Gsps, and Above 1Gsps. The 12 bit segment is further sub segmented into Upto 50 Msps, 51 to 100 Msps, 101 to 200 Msps, 201 to 500 Msps, 501 Msps to 1Gsps, and Above 1Gsps. The 14 bit segment is further sub segmented into Upto 50 Msps, 51 to 100 Msps, 101 to 200 Msps, 201 to 500 Msps, 501 Msps to 1Gsps, and Above 1Gsps. The 16 bit segment is further sub segmented into Upto 50 Msps, 51 to 100 Msps, 101 to 200 Msps, 201 to 500 Msps, 501 Msps to 1Gsps, and Above 1Gsps. The others bit segment is further sub segmented into Upto 50 Msps, 51 to 100 Msps, 101 to 200 Msps, 201 to 500 Msps, 501 Msps to 1Gsps, and Above 1Gsps.

Based on rate of converter, the North America data converter market is segmented into Upto 50 Msps, 51 to 100 Msps, 101 to 200 Msps, 201 to 500 Msps, 501 Msps to 1 Gsps, and Above 1 Gsps. The 501 Msps to 1 Gsps segment held the largest market share in 2022.

In terms of end user, the North America data converter market is segmented into automotive, communications, consumer electronics, industrial, medical, and others. The consumer electronics segment held the largest market share in 2022.

By country, the North America data converter market is segmented into the US, Canada, and Mexico. The US dominated the North America data converter market share in 2022.

Analog Devices Inc, Asahi Kasei Microdevices Corp, Cirrus Logic Inc, Microchip Technology Inc, On Semiconductor Corp, Renesas Electronics Corp, ROHM Co Ltd, STMicroelectronics NV, Teledyne Technologies Inc, and Texas Instruments Inc are some of the leading companies operating in the North America data converter market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

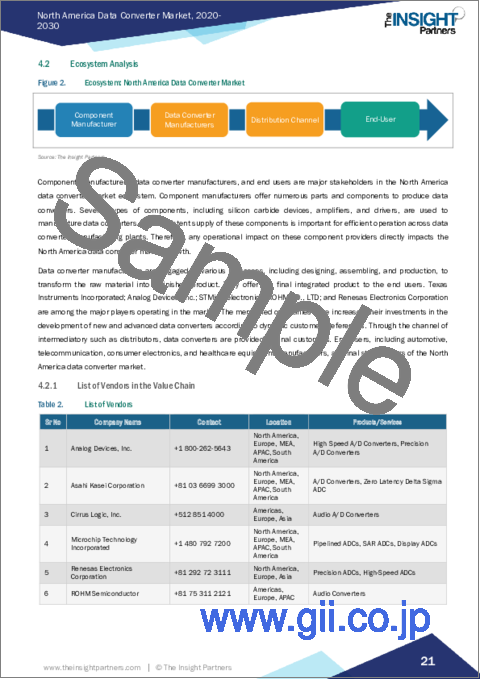

4. North America Data Converter Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Vendors in the Value Chain

5. North America Data Converter Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Testing and Measurement by End Users

- 5.1.2 Rising Demand for Data Converters in Wireless Communications

- 5.1.3 Increasing Product Launches

- 5.2 Market Restraints

- 5.2.1 Complex Design of ADCs

- 5.2.2 Fluctuations in Cost of Raw Materials

- 5.3 Market Opportunities

- 5.3.1 Potential Use of IoT Devices and Data Consumption

- 5.3.2 Growing Use of Data Converters in Developing Advanced 5G Infrastructure

- 5.4 Future Trends

- 5.4.1 Rise of High-Speed Data Converters

- 5.5 Impact of Drivers and Restraints:

6. Data Converter Market - North America Analysis

- 6.1 North America Data Converter Market Revenue (US$ Million), 2020 - 2030

- 6.2 North America Data Converter Market Forecast Analysis

7. North America Data Converter Market Analysis - by Type

- 7.1 ADC

- 7.1.1 Overview

- 7.1.2 ADC: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2 DAC

- 7.2.1 Overview

- 7.2.2 DAC: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

8. North America Data Converter Market Analysis - by Resolution

- 8.1 Bit

- 8.1.1 Overview

- 8.1.2 10 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2 12 Bit

- 8.2.1 Overview

- 8.2.2 12 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3 14 Bit

- 8.3.1 Overview

- 8.3.2 14 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 16 Bit

- 8.4.1 Overview

- 8.4.2 16 Bit: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 Others

- 8.5.1 Overview

- 8.5.2 Others: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

9. North America Data Converter Market Analysis - by Rate of Converter

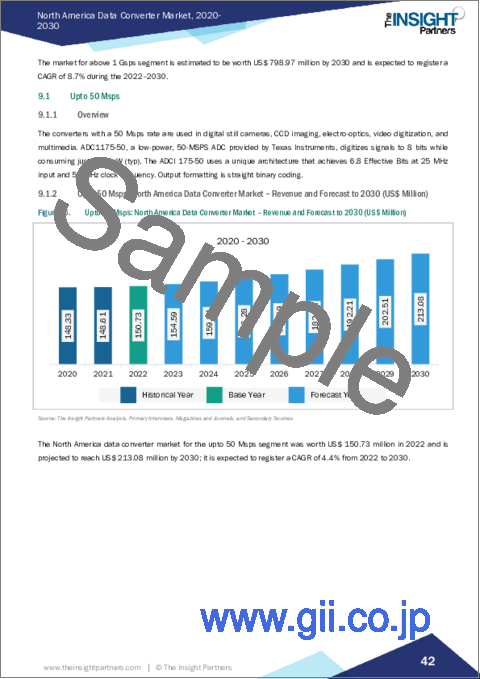

- 9.1 Upto 50 Msps

- 9.1.1 Overview

- 9.1.2 Upto 50 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 9.2 51 to 100 Msps

- 9.2.1 Overview

- 9.2.2 51 to 100 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 9.3 101 to 200 Msps

- 9.3.1 Overview

- 9.3.2 101 to 200 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 9.4 201 to 500 Msps

- 9.4.1 Overview

- 9.4.2 201 to 500 Msps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 9.5 501 Msps to 1 Gsps

- 9.5.1 Overview

- 9.5.2 501 Msps to 1 Gsps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 9.6 Above 1 Gsps

- 9.6.1 Overview

- 9.6.2 Above 1 Gsps: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

10. North America Data Converter Market Analysis - by End user

- 10.1 Automotive

- 10.1.1 Overview

- 10.1.2 Automotive: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 10.2 Communications

- 10.2.1 Overview

- 10.2.2 Communications: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 10.3 Consumer Electronics

- 10.3.1 Overview

- 10.3.2 Consumer Electronics: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 10.4 Industrial

- 10.4.1 Overview

- 10.4.2 Industrial: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 10.5 Medical

- 10.5.1 Overview

- 10.5.2 Medical: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 10.6 Others

- 10.6.1 Overview

- 10.6.2 Others: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

11. North America Data Converter Market - Country Analysis

- 11.1 Overview

- 11.1.1 North America Data Converter Market - Revenue and Forecast Analysis - by Country

- 11.1.1.1 North America Data Converter Market - Revenue and Forecast Analysis - by Country

- 11.1.1.2 United States: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.2.1 United States: North America Data Converter Market Breakdown, by Type

- 11.1.1.2.2 United States: North America Data Converter Market Breakdown, by Resolution

- 11.1.1.2.3 United States: North America Data Converter Market Breakdown, by Rate Of Converter

- 11.1.1.2.4 United States: North America Data Converter Market Breakdown, by End user

- 11.1.1.3 Canada: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.3.1 Canada: North America Data Converter Market Breakdown, by Type

- 11.1.1.3.2 Canada: North America Data Converter Market Breakdown, by Resolution

- 11.1.1.3.3 Canada: North America Data Converter Market Breakdown, by Rate Of Converter

- 11.1.1.3.4 Canada: North America Data Converter Market Breakdown, by End user

- 11.1.1.4 Mexico: North America Data Converter Market - Revenue and Forecast to 2030 (US$ Million)

- 11.1.1.4.1 Mexico: North America Data Converter Market Breakdown, by Type

- 11.1.1.4.2 Mexico: North America Data Converter Market Breakdown, by Resolution

- 11.1.1.4.3 Mexico: North America Data Converter Market Breakdown, by Rate Of Converter

- 11.1.1.4.4 Mexico: North America Data Converter Market Breakdown, by End user

- 11.1.1 North America Data Converter Market - Revenue and Forecast Analysis - by Country

12. Competitive Landscape

- 12.1 Heat Map Analysis by Key Players

- 12.2 Company Positioning & Concentration

13. Industry Landscape

- 13.1 Overview

- 13.2 Market Initiative

- 13.3 Product Development

14. Company Profiles

- 14.1 Texas Instruments Inc

- 14.1.1 Key Facts

- 14.1.2 Business Description

- 14.1.3 Products and Services

- 14.1.4 Financial Overview

- 14.1.5 SWOT Analysis

- 14.1.6 Key Developments

- 14.2 STMicroelectronics NV

- 14.2.1 Key Facts

- 14.2.2 Business Description

- 14.2.3 Products and Services

- 14.2.4 Financial Overview

- 14.2.5 SWOT Analysis

- 14.2.6 Key Developments

- 14.3 Renesas Electronics Corp

- 14.3.1 Key Facts

- 14.3.2 Business Description

- 14.3.3 Products and Services

- 14.3.4 Financial Overview

- 14.3.5 SWOT Analysis

- 14.3.6 Key Developments

- 14.4 ROHM Co Ltd

- 14.4.1 Key Facts

- 14.4.2 Business Description

- 14.4.3 Products and Services

- 14.4.4 Financial Overview

- 14.4.5 SWOT Analysis

- 14.4.6 Key Developments

- 14.5 Analog Devices Inc

- 14.5.1 Key Facts

- 14.5.2 Business Description

- 14.5.3 Products and Services

- 14.5.4 Financial Overview

- 14.5.5 SWOT Analysis

- 14.5.6 Key Developments

- 14.6 Cirrus Logic Inc

- 14.6.1 Key Facts

- 14.6.2 Business Description

- 14.6.3 Products and Services

- 14.6.4 Financial Overview

- 14.6.5 SWOT Analysis

- 14.6.6 Key Developments

- 14.7 Asahi Kasei Microdevices Corp

- 14.7.1 Key Facts

- 14.7.2 Business Description

- 14.7.3 Products and Services

- 14.7.4 Financial Overview

- 14.7.5 SWOT Analysis

- 14.7.6 Key Developments

- 14.8 Microchip Technology Inc

- 14.8.1 Key Facts

- 14.8.2 Business Description

- 14.8.3 Products and Services

- 14.8.4 Financial Overview

- 14.8.5 SWOT Analysis

- 14.8.6 Key Developments

- 14.9 On Semiconductor Corp

- 14.9.1 Key Facts

- 14.9.2 Business Description

- 14.9.3 Products and Services

- 14.9.4 Financial Overview

- 14.9.5 SWOT Analysis

- 14.9.6 Key Developments

- 14.10 Teledyne Technologies Inc

- 14.10.1 Key Facts

- 14.10.2 Business Description

- 14.10.3 Products and Services

- 14.10.4 Financial Overview

- 14.10.5 SWOT Analysis

- 14.10.6 Key Developments

15. Appendix

- 15.1 Word Index

- 15.2 About The Insight Partners