|

|

市場調査レポート

商品コード

1533101

欧州の5G基地局市場予測(~2030年):地域別分析 - コンポーネント別、周波数帯域別、セルタイプ別、エンドユーザー別Europe 5G Base Station Market Forecast to 2030 - Regional Analysis - by Component, Frequency Band, Cell Type, and End User |

||||||

|

|||||||

|

|||||||

| 欧州の5G基地局市場予測(~2030年):地域別分析 - コンポーネント別、周波数帯域別、セルタイプ別、エンドユーザー別 |

|

出版日: 2024年06月04日

発行: The Insight Partners

ページ情報: 英文 110 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州の5G基地局の市場規模は、2022年に58億5,474万米ドルとなり、2030年には188億9,044万米ドルに達すると予測され、2022年~2030年のCAGRは15.8%と推定されます。

IoTとインダストリー4.0導入の急増が欧州の5G基地局市場を牽引

インダストリー4.0は、通信、相互接続性、リアルタイムデータ、機械学習を非常に重視する産業革命の新しいフェーズと考えられています。モバイルネットワークのインダストリー4.0利用は、製造業者やサプライチェーン企業にとって関心が高まっているテーマであり、企業が業務におけるインダストリー4.0の適応性を高めようとする中で、5Gモバイル技術を利用することで大きなメリットが得られます。Wi-Fiネットワークは、特にラップトップ、タブレット、スマートフォンを使用するフレキシブルなワークスペースにおいて、あらゆる企業ITネットワークの重要な部分です。しかし、Wi-Fiネットワークには技術的・拡張的な課題が数多くあり、特にデバイスの台数を増やした場合、より広範な製造・サプライチェーンの業務アプリケーションに対するWi-Fiネットワークの有用性が制限されます。そのため、製造業やサプライチェーン企業は、適応可能な生産環境のために5Gモバイル接続を導入することが推奨されています。モバイル・ネットワークは、生産ラインの迅速な再構成、自動搬送車や自律移動ロボット、部品や供給品の信頼性の高い連続追跡、あるいは先に分析したその他の使用事例をサポートする幅広い機能を提供します。その結果、企業はインダストリー4.0投資の完全な利益を達成することができます。

ネットワークスライシング、新しい認証フレームワーク、キー交換と暗号化、エッジコンピューティング、広帯域幅、オープンネットワーキングイニシアチブを含む5Gで導入された実質的な機能は、信頼性の高い低遅延を提供し、インダストリー4.0に最大の柔軟性をもたらします。さらに、タイムセンシティブ・ネットワーキング・サポートなどの5G開発は、有線ネットワークから無線への移行をサポートする追加機能を提供することができます。

さらに、インダストリー4.0は、高度な分析、自動化システム、資産追跡をサポートするビッグデータに大きく依存しています。IoTセンサーは、そのデータをエッジ・デバイスに伝送・収集し、処理するための物理的媒体を提供します。IoTセンサーは膨大なデータポイントを収集し、それを人工知能や機械学習プラットフォームが分析・消費します。センサーは、Bluetooth、Wi-Fi、LTE/5G、LoRaなど、さまざまな無線媒体で通信できます。インダストリー4.0は、プライベートワイヤレスネットワークの形でキャリアグレードの4Gから始まり、ビジネスニーズの出現とともに5Gへと移行するモバイルネットワークによって支えられています。したがって、IoTとインダストリー4.0の導入の急増が5G基地局市場の成長を後押ししています。

欧州の5G基地局市場概要

欧州各国の政府は5G技術の戦略的重要性を認識し、その展開を促進するためのイニシアティブを打ち出しています。こうした取り組みには、インフラや周波数割り当てへの投資が含まれることが多いです。欧州委員会は2013年に5Gの機会を特定し、5G技術の研究とイノベーションを加速するために5Gに関する官民パートナーシップ(5G-PPP)を設立しました。欧州委員会は、この活動を支援するため、Horizon Programme 2020を通じて7億9,802万米ドルを超える公的資金を拠出しました。これらの活動には、5Gに関する世界の合意形成を確実にするための国際的な計画が付随していました。2013年のEUによる5Gへの投資と研究は、2025年までに予想されるトラフィック量を支えるために不可欠です。EUの投資はまた、IoTやM2M(Machine-to-Machine)通信などの新興分野におけるネットワークとインターネットアーキテクチャを後押ししました。同様に、2021年には、欧州投資基金(European Investment Fund)が実施した人工知能(AI)およびブロックチェーンのパイロット・プログラムなど、対象となるファンド・オブ・ファンズの設定において、1億1,400万米ドルが投入され、対象となる企業への7億9,802万米ドルを超える投資全体が促進されました。さらに、欧州の通信事業者は、加入者を獲得し市場競争力を維持するために、5Gネットワークの導入を競っています。例えば、2023年8月、PPFグループはブルガリア、ハンガリー、セルビア、スロバキアの通信事業部門の支配権を当初23億1,333万米ドルで売却することに合意しました。また、主要企業間の市場競争の激化が5Gインフラの拡大を促進しています。したがって、5G基地局の需要も欧州で増加しており、市場成長を後押ししています。

欧州の5G基地局市場の収益と2030年までの予測(金額)

欧州の5G基地局市場セグメンテーション

欧州の5G基地局市場は、コンポーネント、周波数帯域、セルタイプ、エンドユーザー、国に分類されます。

コンポーネント別では、欧州の5G基地局市場はハードウェアとサービスに二分されます。2022年の市場シェアで大きかったのはハードウェアセグメントです。

周波数帯域では、欧州の5G基地局市場は2.5GHz未満、2.5~8GHz、8~25GHz、25GHz超に区分されます。2022年の市場シェアは2.5~8GHzが最も大きくなりました。

セルタイプ別に見ると、欧州の5G基地局市場はマクロセルとスモールセルに二分されます。2022年の市場シェアで大きかったのはスモールセルセグメントです。さらに、スモールセルセグメントはマイクロセル、ピコセル、フェムトセルに細分化されます。

エンドユーザー別では、欧州の5G基地局市場は産業、商業、住宅に区分されます。2022年には、商業セグメントが最大の市場シェアを占めています。

国別では、欧州の5G基地局市場はドイツ、フランス、イタリア、英国、ロシア、その他欧州に区分されます。2022年の欧州の5G基地局市場シェアはドイツが独占しました。

Airspan Networks Holdings Inc、CommScope Holding Co Inc、Huawei Technologies Co Ltd、NEC Corp、Nokia Corp、Samsung Electronics Co Ltd、Telefonaktiebolaget LM Ericsson、ZTE Corpは、欧州の5G基地局市場で事業を展開する大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 欧州の5G基地局市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 欧州の5G基地局市場:主要市場力学

- 欧州の5G基地局市場:主要市場力学

- 市場促進要因

- 低遅延・高速データへの需要の高まり

- IoTとインダストリー4.0導入の急増

- 市場抑制要因

- 5Gインフラ導入コストの高さ

- ネットワーク放射線に関する政府規制

- 市場機会

- スマートインフラとスマートシティの発展

- 今後の動向

- エッジコンピューティングの利用増加

- 促進要因と抑制要因の影響

第6章 5G基地局市場:欧州市場分析

- 欧州の5G基地局市場の収益(2020年~2030年)

- 欧州の5G基地局市場の予測と分析

第7章 欧州の5G基地局市場分析:コンポーネント

- ハードウェア

- ハードウェア市場:収益と2030年までの予測

- サービス

- サービス市場:収益と2030年までの予測

第8章 欧州の5G基地局市場分析:周波数帯域

- 2.5GHz未満

- 2.5GHz未満市場:収益と2030年までの予測

- 2.5~8GHz

- 2.5~8GHz市場:収益と2030年までの予測

- 8~25GHz

- 8~25GHz市場:収益と2030年までの予測

- 25GHz超

- 25GHz超市場:収益と2030年までの予測

第9章 欧州の5G基地局市場分析:セルタイプ

- マクロセル

- マクロセル市場:収益と2030年までの予測

- スモールセル

- スモールセル市場:収益と2030年までの予測

- マイクロセル

- ピコセル

- フェムトセル

第10章 欧州の5G基地局市場分析:エンドユーザー

- 産業

- 産業市場:収益と2030年までの予測

- 商業

- 商業市場:収益と2030年までの予測

- 住宅

- 住宅市場:収益と2030年までの予測

第11章 欧州の5G基地局市場:国別分析

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- その他欧州

第12章 業界情勢

- 市場イニシアティブ

- 製品開発

- 合併と買収

第13章 企業プロファイル

- ZTE Corp

- CommScope Holding Co Inc

- Huawei Technologies Co Ltd

- NEC Corp

- Samsung Electronics Co Ltd

- Telefonaktiebolaget LM Ericsson

- Nokia Corp

- Airspan Networks Holdings Inc

第14章 付録

List Of Tables

- Table 1. Europe 5G Base Station Market Segmentation

- Table 2. Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Million)

- Table 3. Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Million) - Component

- Table 4. Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Million) - Frequency Band

- Table 5. Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Million) - Cell Type

- Table 6. Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Million) - Small Cell

- Table 7. Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Million) - End User

- Table 8. Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Country

- Table 9. Germany 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 10. Germany 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Frequency Band

- Table 11. Germany 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Cell Type

- Table 12. Germany 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Small Cell

- Table 13. Germany 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 14. France 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 15. France 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Frequency Band

- Table 16. France 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Cell Type

- Table 17. France 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Small Cell

- Table 18. France 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 19. Italy 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 20. Italy 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Frequency Band

- Table 21. Italy 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Cell Type

- Table 22. Italy 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Small Cell

- Table 23. Italy 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 24. UK 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 25. UK 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Frequency Band

- Table 26. UK 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Cell Type

- Table 27. UK 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Small Cell

- Table 28. UK 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 29. Russia 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 30. Russia 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Frequency Band

- Table 31. Russia 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Cell Type

- Table 32. Russia 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Small Cell

- Table 33. Russia 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 34. Rest of Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 35. Rest of Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Frequency Band

- Table 36. Rest of Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Cell Type

- Table 37. Rest of Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By Small Cell

- Table 38. Rest of Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 39. List of Abbreviation

List Of Figures

- Figure 1. Europe 5G Base Station Market Segmentation, By Country

- Figure 2. Ecosystem: 5G Base Station Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Europe 5G Base Station Market Revenue (US$ Million), 2020 - 2030

- Figure 5. Europe 5G Base Station Market Share (%) - Component, 2022 and 2030

- Figure 6. Hardware Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 7. Service Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 8. Europe 5G Base Station Market Share (%) - Frequency Band, 2022 and 2030

- Figure 9. Less Than 2.5 GHz Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 10. 2.5 - 8 GHz Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 11. 8 - 25 GHz Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 12. More Than 25 GHz Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 13. Europe 5G Base Station Market Share (%) - Cell Type, 2022 and 2030

- Figure 14. Macrocell Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 15. Small Cell Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 16. Microcell Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 17. Picocell Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 18. Femtocell Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 19. Europe 5G Base Station Market Share (%) - End User, 2022 and 2030

- Figure 20. Industrial Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 21. Commercial Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 22. Residential Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 23. Europe 5G Base Station Market, by Key Country - Revenue (2022) (US$ Million)

- Figure 24. 5G Base Station Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 25. Germany 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 26. France 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 27. Italy 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 28. UK 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 29. Russia 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 30. Rest of Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

The Europe 5G base station market was valued at US$ 5,854.74 million in 2022 and is expected to reach US$ 18,890.44 million by 2030; it is estimated to register a CAGR of 15.8% from 2022 to 2030.

Surge in IoT and Industry 4.0 Adoption Drives Europe 5G Base Station Market

Industry 4.0 is considered a new phase of the industrial revolution, which highly emphasizes telecommunication, interconnectivity, real-time data, and machine learning. Industry 4.0 use of mobile networks is a growing topic of interest to manufacturers and supply chain companies; as enterprises drive to increase Industry 4.0 adaptability in their operations, they achieve significant benefits while using 5G mobile technologies. Wi-Fi networks are a key part of any enterprise IT network, particularly for flexible workspaces that use laptops, tablets, and smartphones. However, there are a number of technical and scalability challenges that limit the usefulness of Wi-Fi networks for wider manufacturing and supply chain operational applications, particularly when device numbers are scaled up. Therefore, manufacturing and supply chain companies are encouraged to introduce 5G mobile connectivity for their adaptable production environments. Mobile networks deliver the breadth of capabilities to support rapid reconfiguration of the production line, automated guided vehicles or autonomous mobile robots, reliable continuous tracking of components or supplies, or any of the other use cases analyzed earlier. As a result, the enterprise is able to achieve the complete benefits of Industry 4.0 investments.

The substantial capabilities introduced with 5G, including network slicing, new authentication framework, key exchange and encryption, edge computing, massive bandwidth, and open networking initiatives-provide ultra-reliable low-latency and deliver the greatest flexibility for Industry 4.0. In addition, 5G developments such as time-sensitive networking support can deliver additional capabilities to support the migration of wired networks to wireless.

Furthermore, Industry 4.0 heavily depends on big data to support advanced analytics, automated systems, and asset tracking. IoT sensors offer the physical medium to transmit and collect that data to edge devices for processing. IoT sensors collect massive data points, which are then analyzed and consumed by artificial intelligence and machine learning platforms. Sensors can communicate across an array of wireless mediums, such as Bluetooth, Wi-Fi, LTE/5G, and LoRa. Industry 4.0 is being powered by mobile networks starting with carrier-grade 4G in the form of private wireless networks and migrating to 5G as business needs emerge. Hence, the surge in IoT and Industry 4.0 adoption fuels the 5G base station market growth.

Europe 5G Base Station Market Overview

Governments of various countries in Europe have recognized the strategic importance of 5G technology and have launched initiatives to promote its deployment. These initiatives often involve investments in infrastructure and spectrum allocation. The European Commission identified 5G opportunities in 2013, establishing a public-private partnership on 5G (5G-PPP) to accelerate research and innovation in 5G technology. The European Commission committed public funding of more than US$ 798.02 million through the Horizon Programme 2020 to support this activity. These activities were accompanied by an international plan to ensure global agreement building on 5G. EU investment in 5G in 2013 and research is vital to support the traffic volume expected by 2025. EU investment also boosted networks and Internet architectures in emerging areas such as the IoT and machine-to-machine (M2M) communication. Similarly, in 2021, in the setup of targeted fund-of-funds envelopes such as the artificial intelligence (AI) and Blockchain pilot program implemented by the European Investment Fund, which deployed US$ 114 million to catalyze an overall investment of more than US$ 798.02 million in eligible companies. Furthermore, telecom operators in Europe compete to deploy 5G networks to attract subscribers and remain competitive in the market. For instance, in August 2023, PPF Group agreed to sell a controlling stake in its telecom's units in Bulgaria, Hungary, Serbia, and Slovakia for an initial amount of US$ 2,313.33 million. Also, the rise in market competition between key players is driving the expansion of 5G infrastructure. Therefore, the demand for 5G base stations is also increasing in Europe, which boosts market growth.

Europe 5G Base Station Market Revenue and Forecast to 2030 (US$ Million)

Europe 5G Base Station Market Segmentation

The Europe 5G base station market is categorized into component, frequency band, cell type, end user, and country.

Based on component, the Europe 5G base station market is bifurcated into hardware and service. The hardware segment held a larger market share in 2022.

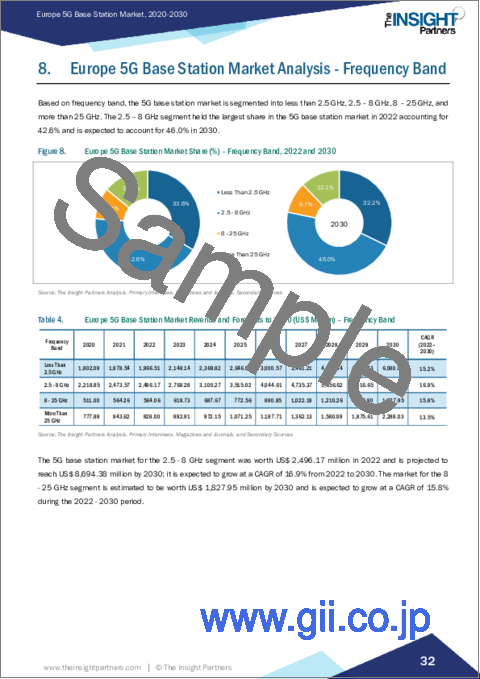

In terms of frequency band, the Europe 5G base station market is segmented into less than 2.5 GHz, 2.5 - 8 GHz, 8 - 25 GHz, and more than 25 GHz. The 2.5 - 8 GHz segment held the largest market share in 2022.

By cell type, the Europe 5G base station market is bifurcated into macrocell and small cell. The small cell segment held a larger market share in 2022. Furthermore, the small cell segment is subsegmented into microcell, picocell, and femtocell.

Based on end user, the Europe 5G base station market is segmented into industrial, commercial, and residential. The commercial segment held the largest market share in 2022.

By country, the Europe 5G base station market is segmented into Germany, France, Italy, the UK, Russia, and the Rest of Europe. Germany dominated the Europe 5G base station market share in 2022.

Airspan Networks Holdings Inc, CommScope Holding Co Inc, Huawei Technologies Co Ltd, NEC Corp, Nokia Corp, Samsung Electronics Co Ltd, Telefonaktiebolaget LM Ericsson, and ZTE Corp are among the leading companies operating in the Europe 5G base station market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Europe 5G Base Station Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Vendors in the Value Chain:

5. Europe 5G Base Station Market - Key Market Dynamics

- 5.1 Europe 5G Base Station Market - Key Market Dynamics

- 5.2 Market Drivers

- 5.2.1 Increased Demand for Low Latency and High-speed Data

- 5.2.2 Surge in IoT and Industry 4.0 Adoption

- 5.3 Market Restraints

- 5.3.1 High Cost of Installing 5G Infrastructure

- 5.3.2 Government Regulations Related to Network Radiation

- 5.4 Market Opportunities

- 5.4.1 Development of Smart Infrastructure and Smart City

- 5.5 Future Trends

- 5.5.1 Rise in Usage of Edge Computing

- 5.6 Impact of Drivers and Restraints:

6. 5G Base Station Market - Europe Market Analysis

- 6.1 Europe 5G Base Station Market Revenue (US$ Million), 2020 - 2030

- 6.2 Europe 5G Base Station Market Forecast and Analysis

7. Europe 5G Base Station Market Analysis - Component

- 7.1 Hardware

- 7.1.1 Overview

- 7.1.2 Hardware Market, Revenue and Forecast to 2030 (US$ Million)

- 7.2 Service

- 7.2.1 Overview

- 7.2.2 Service Market, Revenue and Forecast to 2030 (US$ Million)

8. Europe 5G Base Station Market Analysis - Frequency Band

- 8.1 Less Than 2.5 GHz

- 8.1.1 Overview

- 8.1.2 Less Than 2.5 GHz Market, Revenue and Forecast to 2030 (US$ Million)

- 8.2 2.5 - 8 GHz

- 8.2.1 Overview

- 8.2.2 2.5 - 8 GHz Market, Revenue and Forecast to 2030 (US$ Million)

- 8.3 8 - 25 GHz

- 8.3.1 Overview

- 8.3.2 8 - 25 GHz Market, Revenue and Forecast to 2030 (US$ Million)

- 8.4 More Than 25 GHz

- 8.4.1 Overview

- 8.4.2 More Than 25 GHz Market, Revenue and Forecast to 2030 (US$ Million)

9. Europe 5G Base Station Market Analysis - Cell Type

- 9.1 Macrocell

- 9.1.1 Overview

- 9.1.2 Macrocell Market, Revenue and Forecast to 2030 (US$ Million)

- 9.2 Small Cell

- 9.2.1 Overview

- 9.2.2 Small Cell Market, Revenue and Forecast to 2030 (US$ Million)

- 9.2.3 Microcell

- 9.2.3.1 Overview

- 9.2.3.2 Microcell Market, Revenue and Forecast to 2030 (US$ Million)

- 9.2.4 Picocell

- 9.2.4.1 Overview

- 9.2.4.2 Picocell Market, Revenue and Forecast to 2030 (US$ Million)

- 9.2.5 Femtocell

- 9.2.5.1 Overview

- 9.2.5.2 Femtocell Market, Revenue and Forecast to 2030 (US$ Million)

10. Europe 5G Base Station Market Analysis - End User

- 10.1 Industrial

- 10.1.1 Overview

- 10.1.2 Industrial Market, Revenue and Forecast to 2030 (US$ Million)

- 10.2 Commercial

- 10.2.1 Overview

- 10.2.2 Commercial Market, Revenue and Forecast to 2030 (US$ Million)

- 10.3 Residential

- 10.3.1 Overview

- 10.3.2 Residential Market, Revenue and Forecast to 2030 (US$ Million)

11. Europe 5G Base Station Market - Country Analysis

- 11.1 Europe

- 11.1.1 Europe 5G Base Station Market Overview

- 11.1.2 Europe 5G Base Station Market Revenue and Forecasts and Analysis - By Country

- 11.1.2.1 Europe 5G Base Station Market Revenue and Forecasts and Analysis - By Country

- 11.1.2.2 Germany 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.2.2.1 Germany 5G Base Station Market Breakdown, by Component

- 11.1.2.2.2 Germany 5G Base Station Market Breakdown, by Frequency Band

- 11.1.2.2.3 Germany 5G Base Station Market Breakdown, by Cell Type

- 11.1.2.2.3.1 Germany 5G Base Station Market Breakdown, by Small Cell

- 11.1.2.2.4 Germany 5G Base Station Market Breakdown, by End User

- 11.1.2.3 France 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.2.3.1 France 5G Base Station Market Breakdown, by Component

- 11.1.2.3.2 France 5G Base Station Market Breakdown, by Frequency Band

- 11.1.2.3.3 France 5G Base Station Market Breakdown, by Cell Type

- 11.1.2.3.3.1 France 5G Base Station Market Breakdown, by Small Cell

- 11.1.2.3.4 France 5G Base Station Market Breakdown, by End User

- 11.1.2.4 Italy 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.2.4.1 Italy 5G Base Station Market Breakdown, by Component

- 11.1.2.4.2 Italy 5G Base Station Market Breakdown, by Frequency Band

- 11.1.2.4.3 Italy 5G Base Station Market Breakdown, by Cell Type

- 11.1.2.4.3.1 Italy 5G Base Station Market Breakdown, by Small Cell

- 11.1.2.4.4 Italy 5G Base Station Market Breakdown, by End User

- 11.1.2.5 UK 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.2.5.1 UK 5G Base Station Market Breakdown, by Component

- 11.1.2.5.2 UK 5G Base Station Market Breakdown, by Frequency Band

- 11.1.2.5.3 UK 5G Base Station Market Breakdown, by Cell Type

- 11.1.2.5.3.1 UK 5G Base Station Market Breakdown, by Small Cell

- 11.1.2.5.4 UK 5G Base Station Market Breakdown, by End User

- 11.1.2.6 Russia 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.2.6.1 Russia 5G Base Station Market Breakdown, by Component

- 11.1.2.6.2 Russia 5G Base Station Market Breakdown, by Frequency Band

- 11.1.2.6.3 Russia 5G Base Station Market Breakdown, by Cell Type

- 11.1.2.6.3.1 Russia 5G Base Station Market Breakdown, by Small Cell

- 11.1.2.6.4 Russia 5G Base Station Market Breakdown, by End User

- 11.1.2.7 Rest of Europe 5G Base Station Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.2.7.1 Rest of Europe 5G Base Station Market Breakdown, by Component

- 11.1.2.7.2 Rest of Europe 5G Base Station Market Breakdown, by Frequency Band

- 11.1.2.7.3 Rest of Europe 5G Base Station Market Breakdown, by Cell Type

- 11.1.2.7.3.1 Rest of Europe 5G Base Station Market Breakdown, by Small Cell

- 11.1.2.7.4 Rest of Europe 5G Base Station Market Breakdown, by End User

12. Industry Landscape

- 12.1 Overview

- 12.2 Market Initiative

- 12.3 Product Development

- 12.4 Mergers & Acquisitions

13. Company Profiles

- 13.1 ZTE Corp

- 13.1.1 Key Facts

- 13.1.2 Business Description

- 13.1.3 Products and Services

- 13.1.4 Financial Overview

- 13.1.5 SWOT Analysis

- 13.1.6 Key Developments

- 13.2 CommScope Holding Co Inc

- 13.2.1 Key Facts

- 13.2.2 Business Description

- 13.2.3 Products and Services

- 13.2.4 Financial Overview

- 13.2.5 SWOT Analysis

- 13.2.6 Key Developments

- 13.3 Huawei Technologies Co Ltd

- 13.3.1 Key Facts

- 13.3.2 Business Description

- 13.3.3 Products and Services

- 13.3.4 Financial Overview

- 13.3.5 SWOT Analysis

- 13.3.6 Key Developments

- 13.4 NEC Corp

- 13.4.1 Key Facts

- 13.4.2 Business Description

- 13.4.3 Products and Services

- 13.4.4 Financial Overview

- 13.4.5 SWOT Analysis

- 13.4.6 Key Developments

- 13.5 Samsung Electronics Co Ltd

- 13.5.1 Key Facts

- 13.5.2 Business Description

- 13.5.3 Products and Services

- 13.5.4 Financial Overview

- 13.5.5 SWOT Analysis

- 13.5.6 Key Developments

- 13.6 Telefonaktiebolaget LM Ericsson

- 13.6.1 Key Facts

- 13.6.2 Business Description

- 13.6.3 Products and Services

- 13.6.4 Financial Overview

- 13.6.5 SWOT Analysis

- 13.6.6 Key Developments

- 13.7 Nokia Corp

- 13.7.1 Key Facts

- 13.7.2 Business Description

- 13.7.3 Products and Services

- 13.7.4 Financial Overview

- 13.7.5 SWOT Analysis

- 13.7.6 Key Developments

- 13.8 Airspan Networks Holdings Inc

- 13.8.1 Key Facts

- 13.8.2 Business Description

- 13.8.3 Products and Services

- 13.8.4 Financial Overview

- 13.8.5 SWOT Analysis

- 13.8.6 Key Developments

14. Appendix

- 14.1 Word Index