|

|

市場調査レポート

商品コード

1533086

北米の自動車テレマティクス市場予測(~2030年):地域別分析 - 提供別、接続制別、車両タイプ別、用途別North America Automotive Telematics Market Forecast to 2030 - Regional Analysis - by Offering, Connectivity, Vehicle Type, and Application (Infotainment, Remote Diagnosis, Navigation, Safety and Security, and Others) |

||||||

|

|||||||

|

|||||||

| 北米の自動車テレマティクス市場予測(~2030年):地域別分析 - 提供別、接続制別、車両タイプ別、用途別 |

|

出版日: 2024年06月04日

発行: The Insight Partners

ページ情報: 英文 117 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

北米の自動車テレマティクスの市場規模は、2022年に110億6,390万米ドルと評価され、2030年には385億8,385万米ドルに達すると予測され、2022年~2030年のCAGRは16.9%と推定されます。

自動車販売台数と生産台数の増加が北米の自動車テレマティクス市場を牽引

自動車テレマティクスは、GPSシステム、車載車両診断、ワイヤレス・テレマティック・デバイス、記録や車両データの伝送に使用されるその他のソリューションなど、複数のハードウェアおよびソフトウェア・ソリューションの組み合わせです。テレマティック・デバイスは、位置、速度、メンテナンス要件、サービスなど、いくつかのパラメータを制御します。自動車テレマティクスは、GPS技術の助けを借りて、自動車、自動車機器、トラック、その他の資産などの車両を監視するシステムです。世界中で高度なテレマティクス・システムを組み込んだ自動車の販売と生産が増加していることが、市場の成長を促進しています。

自動車メーカーは、コネクテッド・ビークルを構築するために、自動車テレマティクス・ソリューションやソフトウェアなどの接続オプションを使用しています。自動車メーカーは、GPSデバイス、加速度計、ジャイロスコープ、コネクテッド・ソリューションを組み合わせて使用し、自動車の顧客要件を満たしています。自動車テレマティクスで使用される主要コンポーネントには、入出力インターフェース、GPSレシーバー、加速度計、ブザー、SIMカード、エンジンインターフェースなどがあります。

米国自動車協会によると、自動車製造業は2022年には米国のGDPの11%を占めました。米国の自動車製造業は世界で8番目に大きな分野であり、米国経済に毎年1兆米ドルをもたらしています。アライアンス・フォー・オート・イノベーション・レポートによると、自動車部品と自動車の製造部門は、2022年の米国GDPの3%を占めました。米国の自動車・自動車製造部門は、2023年には1,041億米ドルと評価されました。2021年の米国自動車生産台数は約920万台で、2020年比で4.5%増加しました。

北米の自動車テレマティクス市場概要

北米では、米国が自動車産業に大きく貢献しています。2021年のAlliance for Automotive Innovation Reportによると、自動車部品メーカーから完成車メーカーに至る自動車産業のエコシステムは、米国経済に年間1兆米ドル以上を生み出しています。米国の自動車産業はGDP全体の4.9%を占め、自動車とその部品の製造は同国の製造業全体の6%を占めています。ギア、座席システム、ドア、トランスミッションシステムを含む自動車とその部品は、米国から多く輸出されています。自動車とその部品は、2021年には第2位の輸出品目となり、その輸出額は1,050億米ドルに達しました。

世界中の自動車メーカーによる自動車部品への需要の高まりは、自動車ギア市場に十分な機会をもたらすと予想されます。自動車メーカーは、高度な機能を備えた自動車を製造するために自動車テレマティクスを広く利用しています。米国を拠点とする港湾では、自動車と部品の貿易額が4,000億米ドルを超えています。米国では、自動車メーカーとそのサプライヤーが製造業の大部分を占めており、同国のGDPの3%を占めています。米国自動車政策協議会によれば、ここ数年、自動車メーカーは6,920億米ドル相当の自動車を輸出しています。FCAグループ、フォード、ゼネラルモーターズは、米国における自動車の主要生産者です。これらの大手企業は、先進的なテレマティクス・ソリューションを自動車に搭載しています。また、これらの企業は、顧客の要求を満たすために、上位車両タイプに高度な機能を搭載しています。過去数年間で、これらの企業は米国での組み立て、テレマティクス・ソリューション、組立工場、およびそれらを接続しサポートするその他のインフラに350億米ドル以上を投資してきました。フォード、FCAグループ、ゼネラルモーターズ(GM)は、電気自動車の生産工場の設立と拡張に230億米ドルを投資しました。これらの企業は、プレミアムモデルに自動車テレマティクス・システムを組み込んで提供しています。例えば、2022年10月、ドイツの自動車部品メーカーであるコンチネンタルAGは、メキシコの工場拡張のために約2億948万米ドルを投資しました。

米国の自動車部門は、資本の利用可能性と輸出の増加により急成長しています。同国の大手自動車メーカーは、EVとAVへの複数の投資を発表しました。GMは2025年までに自動車産業に350億米ドルを投資すると発表しました。国内での電気自動車の増加に伴い、自動車牽引バーの需要も増加しています。乗用車と商用車の生産台数の増加も、この地域における自動車用テレマティクスの需要を促進すると予想されます。

北米の自動車テレマティクス市場:収益と2030年までの予測(金額)

北米の自動車テレマティクス市場セグメンテーション

北米の自動車テレマティクス市場は、提供、接続性、車両タイプ、用途、国に分類されます。

提供別では、北米の自動車テレマティクス市場はハードウェアとソフトウェア・サービスに区分されます。2022年の市場シェアで大きかったのは、ハードウェアセグメントです。

接続性別では、北米の自動車テレマティクス市場は統合型、テザリング型、組み込み型に分類されます。2022年には、組み込み型セグメントが最大の市場シェアを占めました。

車両タイプ別では、北米の自動車テレマティクス市場は乗用車と商用車に二分されます。2022年には乗用車セグメントがより大きな市場シェアを占めました。

用途別では、北米の自動車テレマティクス市場は、インフォテインメント、遠隔診断、ナビゲーション(GPS)、安全・セキュリティ、その他に区分されます。2022年の市場シェアはインフォテインメントセグメントが最大でした。

国別では、北米の自動車テレマティクス市場は米国、カナダ、メキシコに区分されます。2022年の北米の自動車テレマティクス市場シェアは米国が独占しました。

Verizon Communications Inc、Geotab Inc、Omnitracs LLC、Samsara Inc、Motive Technologies Inc、Lytx Inc、Zonar Systems Inc、ORBCOMM Inc、Trimble Inc、SkyBitz Inc、Valeo SE、TomTom NV、Denso Corp、Luxoft Switzerland AG、Harman International Industries Incなどが北米の自動車テレマティクス市場で事業を展開する大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米の自動車テレマティクス市場情勢

- エコシステム分析

- 自動車テレマティクスサプライヤー一覧

- 自動車テレマティクス企業・加入者リスト

第5章 北米の自動車テレマティクス市場:主要産業力学

- 北米の自動車テレマティクス市場- 主要産業力学

- 市場促進要因

- 世界の自動車販売台数と生産台数の増加

- 自動車OEMによるテレマティクスデバイス設置の増加

- 自動車レンタルサービスの需要拡大

- 輸送・物流部門によるフリート管理ソリューションの採用増加

- 市場抑制要因

- データのプライバシーとセキュリティに関する懸念

- 初期コストの高さと手頃さへの懸念

- 市場機会

- インテリジェントなテレマティック・ソリューションの採用増加

- 今後の動向

- コネクテッドカーの普及拡大

- フリート管理におけるIoTとAIの採用拡大

- 促進要因と抑制要因の影響

第6章 自動車テレマティクス市場:北米市場分析

- 北米の自動車テレマティクス市場の収益(2022年~2030年)

- 北米の自動車テレマティクス市場の予測と分析

第7章 北米の自動車テレマティクス市場分析:提供

- 北米の自動車テレマティクス市場:提供別(2022年・2030年)

- ハードウェア

- ハードウェア市場:収益と2030年までの予測

- テレマティクスコントロールユニット

- ナビゲーションシステム

- 車載インフォテインメント・システム

- その他

- ソフトウェア・サービス

- ソフトウェア・サービス市場:収益と2030年までの予測

第8章 北米の自動車テレマティクス市場分析:接続性

- 北米の自動車テレマティクス市場:接続性別(2022年・2030年)

- 統合型

- 統合型市場:収益と2030年までの予測

- テザリング型

- テザリング型市場:収益と2030年までの予測

- 組み込み型

- 組み込み型市場:収益と2030年までの予測

第9章 北米の自動車テレマティクス市場分析:車両タイプ別

- 北米の自動車テレマティクス市場:車両タイプ別(2022年・2030年)

- 乗用車

- 乗用車市場:収益と2030年までの予測

- 商用車

- 商用車市場:収益と2030年までの予測

第10章 北米の自動車テレマティクス市場分析:用途別

- 北米の自動車テレマティクス市場:用途別(2022年・2030年)

- インフォテインメント

- インフォテインメント市場:収益と2030年までの予測

- 遠隔診断

- 遠隔診断市場:収益と2030年までの予測

- ナビゲーション(GPS)

- ナビゲーション(GPS)市場:収益と2030年までの予測

- 安全とセキュリティ

- 安全・セキュリティ市場:収益と2030年までの予測

- その他

- その他市場:収益と2030年までの予測

第11章 北米の自動車テレマティクス市場:国別分析

- 米国

- カナダ

- メキシコ

第12章 競合情勢

- 主要企業によるヒートマップ分析

- 企業のポジショニングと集中度

第13章 業界情勢

- 市場イニシアティブ

- 製品開発

第14章 企業プロファイル

- Verizon Communications Inc

- Geotab Inc.

- Omnitracs LLC

- Samsara Inc

- Motive Technologies Inc

- Lytx Inc

- Zonar Systems Inc

- ORBCOMM Inc

- Trimble Inc

- SkyBitz Inc

- Valeo SE

- TomTom NV

- Denso Corp

- Luxoft Switzerland AG

- Harman International Industries Inc

第15章 付録

List Of Tables

- Table 1. List of Suppliers in the Value Chain

- Table 2. North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Million)

- Table 3. North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Million) - Offering

- Table 4. North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Million) - Connectivity

- Table 5. North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Million) - Vehicle Type

- Table 6. North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Million) - Application

- Table 7. US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Offering

- Table 8. US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Hardware

- Table 9. US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Connectivity

- Table 10. US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Vehicle Type

- Table 11. US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Application

- Table 12. Canada: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Offering

- Table 13. Canada: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Hardware

- Table 14. Canada: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Connectivity

- Table 15. Canada: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Vehicle Type

- Table 16. Canada: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Application

- Table 17. Mexico: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Offering

- Table 18. Mexico: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Hardware

- Table 19. Mexico: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Connectivity

- Table 20. Mexico: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Vehicle Type

- Table 21. Mexico: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn) - Application

- Table 22. Heat Map Analysis by Key Players

- Table 23. List of Abbreviation

List Of Figures

- Figure 1. North America Automotive Telematics Market Segmentation, By Country

- Figure 2. Ecosystem: North America Automotive Telematics Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. North America Automotive Telematics Market Revenue (US$ Million), 2022 - 2030

- Figure 5. North America Automotive Telematics Market Share (%) - Offering, 2022 and 2030

- Figure 6. Hardware Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 7. Software and Services Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 8. North America Automotive Telematics Market Share (%) - Connectivity, 2022 and 2030

- Figure 9. Integrated Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 10. Tethered Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 11. Embedded Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 12. North America Automotive Telematics Market Share (%) - Vehicle Type, 2022 and 2030

- Figure 13. Passenger Cars Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 14. Commercial Vehicles Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 15. North America Automotive Telematics Market Share (%) - Application, 2022 and 2030

- Figure 16. Infotainment Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 17. Remote Diagnosis Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 18. Navigation (GPS) Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 19. Safety and Security Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 20. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 21. North America Automotive Telematics Market Breakdown by Key Country - Revenue (2022) (US$ Million)

- Figure 22. North America Automotive Telematics Market Breakdown by Key Country, 2022 and 2030 (%)

- Figure 23. US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 24. Canada: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 25. Mexico: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 26. Company Positioning & Concentration

The North America automotive telematics market was valued at US$ 11,063.90 million in 2022 and is expected to reach US$ 38,583.85 million by 2030; it is estimated to register a CAGR of 16.9% from 2022 to 2030.

Rising Automotive Sales and Production Fuel North America Automotive Telematics Market

Automotive telematics is the combination of several hardware and software solutions, including GPS systems, onboard vehicle diagnostics, wireless telematic devices, and other solutions used to transmit the record and vehicle's data. Telematic devices control several parameters, such as location, speed, maintenance requirements, and services. Automotive telematics is a system of monitoring vehicles such as cars, automotive equipment, trucks, and other assets with the help of GPS technologies. Increasing automotive sales and production with built-in advanced telematics systems across the globe is driving market growth.

Automotive manufacturers use connectivity options, including automotive telematic solutions and software, to create a connected vehicle. Carmakers use a combination of GPS devices, accelerometers, gyroscopes, and connected solutions to meet customer requirements for the vehicles. There are several major components used in automotive telematics, which are:

Input and output interface GPS receiver Accelerometer Buzzers SIM card Engine interface Others According to the American Automotive Association, the automobile manufacturing sector accounted for 11% of the US GDP in 2022. The automotive manufacturing industry of the US is the eighth largest sector globally, which generates US$ 1 trillion annually to the US economy. The manufacturing sector of motor parts and vehicles represents 3% of the US GDP, according to the Alliance for Auto Innovation Report in 2022. The US car and automobile manufacturing sector was valued at US$ 104.1 billion in 2023. In 2021, nearly 9.2 million US vehicles were produced, an increase of 4.5% compared to 2020.

North America Automotive Telematics Market Overview

In North America, the US significantly contributes to the automobile industry. According to the Alliance for Automotive Innovation Report in 2021, the automotive industry's ecosystem, from automotive component manufacturers to the original vehicle manufacturers, generates over US$ 1 trillion annually for the US economy. The automotive sector in the US contributed 4.9% of its overall GDP, with manufacturing of vehicles and their parts representing 6% of the overall manufacturing in the country. Motor vehicles and parts, including gears, seating systems, doors, and transmission systems, are heavily exported from the US. Automotive vehicles and their components were the second-largest exporting goods in 2021, valued at ~US$ 105 billion.

The rising demand for automotive components by the original vehicle manufacturers worldwide is anticipated to create ample opportunity for the automotive gears market. The original vehicle manufacturers widely use automotive telematics to produce advanced features-based vehicles. The US-based ports have executed over US$ 400 billion in trade volume in vehicles and components. In the US, automakers and their suppliers are the largest part of the manufacturing sector, responsible for 3% of the country's GDP. As per the American Automotive Policy Council, in the last few years, automakers have exported vehicles worth ~US$ 692 billion. FCA Group, Ford, and General Motors are the major producers of vehicles in the US. These major players are providing advanced telematics solutions in their vehicles. Also, these companies are providing advanced features in their top vehicle models in order to meet their customers' demands. Over the past few years, these companies have invested ~US$ 35 billion in their US assembly, telematics solutions, assembly plants, and other infrastructure that connects and supports them. The country is also highly engaged in designing electric vehicles; Ford, FCA Group, and General Motors (GM) invested ~US$ 23 billion for the establishment and expansion of the production plants of the vehicles. These companies are offering in built automotive telematics systems on their premium models. For instance, in October 2022, Continental AG Germany based auto parts manufacturer invested around US$ 209.48 million for the expansion of its plant in Mexico.

The automotive sector in the US is growing rapidly due to capital availability and an increase in exports. Major automakers in the country announced several investments in EVs and AVs. GM announced an investment of US$ 35 billion in the automotive industry by 2025. Owing to the growing number of electric vehicles in the country, the demand for automotive tow bars is also increasing. The growing production of passenger cars and commercial vehicles is also anticipated to propel the demand for automotive telematics in this region.

North America Automotive Telematics Market Revenue and Forecast to 2030 (US$ Million)

North America Automotive Telematics Market Segmentation

The North America automotive telematics market is categorized into offering, connectivity, vehicle type, application, and country.

Based on offering, the North America automotive telematics market is segmented into hardware and software & services. The hardware segment held a larger market share in 2022.

In terms of connectivity, the North America automotive telematics market is categorized into integrated, tethered, and embedded. The embedded segment held the largest market share in 2022.

By vehicle type, the North America automotive telematics market is bifurcated into passenger cars and commercial cars. The passenger cars segment held a larger market share in 2022.

By application, the North America automotive telematics market is segmented into infotainment, remote diagnosis, navigation (GPS), safety and security, and others. The infotainment segment held the largest market share in 2022.

By country, the North America automotive telematics market is segmented into the US, Canada, and Mexico. The US dominated the North America automotive telematics market share in 2022.

Verizon Communications Inc, Geotab Inc., Omnitracs LLC, Samsara Inc, Motive Technologies Inc, Lytx Inc, Zonar Systems Inc, ORBCOMM Inc, Trimble Inc, SkyBitz Inc, Valeo SE, TomTom NV, Denso Corp, Luxoft Switzerland AG, and Harman International Industries Inc are among the leading companies operating in the North America automotive telematics market.

Table Of Contents

1. Introduction

- 1.1 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Automotive Telematics Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Automotive Telematic Suppliers

- 4.3 List of Automotive Telematics companies and subscribers

5. North America Automotive Telematics Market - Key Industry Dynamics

- 5.1 North America Automotive Telematics Market - Key Industry Dynamics

- 5.2 Market Drivers

- 5.2.1 Rising Automotive Sales and Production Globally

- 5.2.2 Increasing Installation of Telematic Devices by Automotive OEMs

- 5.2.3 Growing Demand for Vehicle Rental Services

- 5.2.4 The Rising Adoption of Fleet Management Solutions by the Transport and Logistics Sector

- 5.3 Market Restraints

- 5.3.1 Data Privacy and Security Concerns

- 5.3.2 High Initial Costs and Affordability Concerns

- 5.4 Market Opportunities

- 5.4.1 Increasing Adoption of Intelligent Telematic Solutions

- 5.5 Future Trends

- 5.5.1 Rising Adoption of Connected Cars

- 5.5.2 Mounting Adoption of IoT and AI in Fleet Management

- 5.6 Impact of Drivers and Restraints:

6. Automotive Telematics Market - North America Market Analysis

- 6.1 North America Automotive Telematics Market Revenue (US$ Million), 2022 - 2030

- 6.2 North America Automotive Telematics Market Forecast and Analysis

7. North America Automotive Telematics Market Analysis - Offering

- 7.1 North America Automotive Telematics Market, By Offering (2022 and 2030)

- 7.2 Hardware

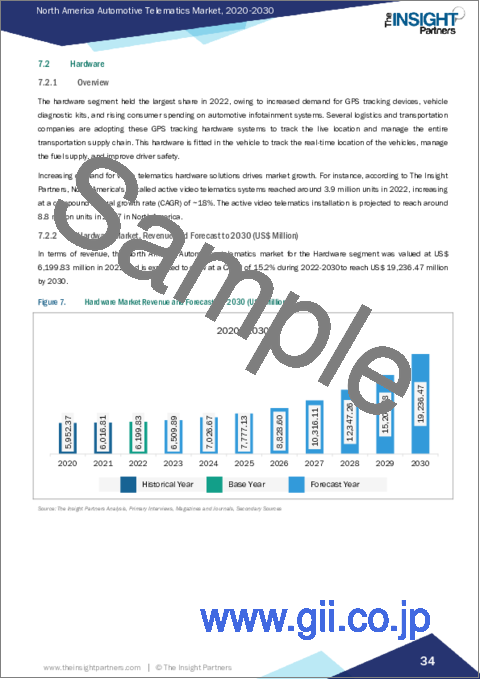

- 7.2.1 Overview

- 7.2.2 Hardware Market, Revenue and Forecast to 2030 (US$ Million)

- 7.2.3 Telematics Control Units

- 7.2.3.1 Overview

- 7.2.4 Navigation System

- 7.2.4.1 Overview

- 7.2.5 In-Vehicle Infotainment Systems

- 7.2.5.1 Overview

- 7.2.6 Others

- 7.2.6.1 Overview

- 7.3 Software and Services

- 7.3.1 Overview

- 7.3.2 Software and Services Market, Revenue and Forecast to 2030 (US$ Million)

8. North America Automotive Telematics Market Analysis - Connectivity

- 8.1 North America Automotive Telematics Market, By Connectivity (2022 and 2030)

- 8.2 Integrated

- 8.2.1 Overview

- 8.2.2 Integrated Market, Revenue and Forecast to 2030 (US$ Million)

- 8.3 Tethered

- 8.3.1 Overview

- 8.3.2 Tethered Market, Revenue and Forecast to 2030 (US$ Million)

- 8.4 Embedded

- 8.4.1 Overview

- 8.4.2 Embedded Market, Revenue and Forecast to 2030 (US$ Million)

9. North America Automotive Telematics Market Analysis - Vehicle Type

- 9.1 North America Automotive Telematics Market, By Vehicle Type (2022 and 2030)

- 9.2 Passenger Cars

- 9.2.1 Overview

- 9.2.2 Passenger Cars Market, Revenue and Forecast to 2030 (US$ Million)

- 9.3 Commercial Vehicles

- 9.3.1 Overview

- 9.3.2 Commercial Vehicles Market, Revenue and Forecast to 2030 (US$ Million)

10. North America Automotive Telematics Market Analysis - Application

- 10.1 North America Automotive Telematics Market, By Application (2022 and 2030)

- 10.2 Infotainment

- 10.2.1 Overview

- 10.2.2 Infotainment Market, Revenue and Forecast to 2030 (US$ Million)

- 10.3 Remote Diagnosis

- 10.3.1 Overview

- 10.3.2 Remote Diagnosis Market, Revenue and Forecast to 2030 (US$ Million)

- 10.4 Navigation (GPS)

- 10.4.1 Overview

- 10.4.2 Navigation (GPS) Market, Revenue and Forecast to 2030 (US$ Million)

- 10.5 Safety and Security

- 10.5.1 Overview

- 10.5.2 Safety and Security Market, Revenue and Forecast to 2030 (US$ Million)

- 10.6 Others

- 10.6.1 Overview

- 10.6.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

11. North America Automotive Telematics Market - Country Analysis

- 11.1 Overview

- 11.1.1 North America Automotive Telematics Market Revenue and Forecasts and Analysis - By Country

- 11.1.1.1 US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.1.1.1 US: North America Automotive Telematics Market Breakdown by Offering

- 11.1.1.1.1.1 US: North America Automotive Telematics Market Breakdown by Hardware

- 11.1.1.1.2 US: North America Automotive Telematics Market Breakdown by Connectivity

- 11.1.1.1.3 US: North America Automotive Telematics Market Breakdown by Vehicle Type

- 11.1.1.1.4 US: North America Automotive Telematics Market Breakdown by Application

- 11.1.1.2 Canada: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.1.2.1 Canada: North America Automotive Telematics Market Breakdown by Offering

- 11.1.1.2.1.1 Canada: North America Automotive Telematics Market Breakdown by Hardware

- 11.1.1.2.2 Canada: North America Automotive Telematics Market Breakdown by Connectivity

- 11.1.1.2.3 Canada: North America Automotive Telematics Market Breakdown by Vehicle Type

- 11.1.1.2.4 Canada: North America Automotive Telematics Market Breakdown by Application

- 11.1.1.3 Mexico: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.1.3.1 Mexico: North America Automotive Telematics Market Breakdown by Offering

- 11.1.1.3.1.1 Mexico: North America Automotive Telematics Market Breakdown by Hardware

- 11.1.1.3.2 Mexico: North America Automotive Telematics Market Breakdown by Connectivity

- 11.1.1.3.3 Mexico: North America Automotive Telematics Market Breakdown by Vehicle Type

- 11.1.1.3.4 Mexico: North America Automotive Telematics Market Breakdown by Application

- 11.1.1.1 US: North America Automotive Telematics Market Revenue and Forecasts to 2030 (US$ Mn)

- 11.1.1 North America Automotive Telematics Market Revenue and Forecasts and Analysis - By Country

12. Competitive Landscape

- 12.1 Heat Map Analysis by Key Players

- 12.2 Company Positioning & Concentration

13. Industry Landscape

- 13.1 Overview

- 13.2 Market Initiative

- 13.3 Product Development

14. Company Profiles

- 14.1 Verizon Communications Inc

- 14.1.1 Key Facts

- 14.1.2 Business Description

- 14.1.3 Products and Services

- 14.1.4 Financial Overview

- 14.1.5 SWOT Analysis

- 14.1.6 Key Developments

- 14.2 Geotab Inc.

- 14.2.1 Key Facts

- 14.2.2 Business Description

- 14.2.3 Products and Services

- 14.2.4 Financial Overview

- 14.2.5 SWOT Analysis

- 14.2.6 Key Developments

- 14.3 Omnitracs LLC

- 14.3.1 Key Facts

- 14.3.2 Business Description

- 14.3.3 Products and Services

- 14.3.4 Financial Overview

- 14.3.5 SWOT Analysis

- 14.3.6 Key Developments

- 14.4 Samsara Inc

- 14.4.1 Key Facts

- 14.4.2 Business Description

- 14.4.3 Products and Services

- 14.4.4 Financial Overview

- 14.4.5 SWOT Analysis

- 14.4.6 Key Developments

- 14.5 Motive Technologies Inc

- 14.5.1 Key Facts

- 14.5.2 Business Description

- 14.5.3 Products and Services

- 14.5.4 Financial Overview

- 14.5.5 SWOT Analysis

- 14.5.6 Key Developments

- 14.6 Lytx Inc

- 14.6.1 Key Facts

- 14.6.2 Business Description

- 14.6.3 Products and Services

- 14.6.4 Financial Overview

- 14.6.5 SWOT Analysis

- 14.6.6 Key Developments

- 14.7 Zonar Systems Inc

- 14.7.1 Key Facts

- 14.7.2 Business Description

- 14.7.3 Products and Services

- 14.7.4 Financial Overview

- 14.7.5 SWOT Analysis

- 14.7.6 Key Developments

- 14.8 ORBCOMM Inc

- 14.8.1 Key Facts

- 14.8.2 Business Description

- 14.8.3 Products and Services

- 14.8.4 Financial Overview

- 14.8.5 SWOT Analysis

- 14.8.6 Key Developments

- 14.9 Trimble Inc

- 14.9.1 Key Facts

- 14.9.2 Business Description

- 14.9.3 Products and Services

- 14.9.4 Financial Overview

- 14.9.5 SWOT Analysis

- 14.9.6 Key Developments

- 14.10 SkyBitz Inc

- 14.10.1 Key Facts

- 14.10.2 Business Description

- 14.10.3 Products and Services

- 14.10.4 Financial Overview

- 14.10.5 SWOT Analysis

- 14.10.6 Key Developments

- 14.11 Valeo SE

- 14.11.1 Key Facts

- 14.11.2 Business Description

- 14.11.3 Products and Services

- 14.11.4 Financial Overview

- 14.11.5 SWOT Analysis

- 14.11.6 Key Developments

- 14.12 TomTom NV

- 14.12.1 Key Facts

- 14.12.2 Business Description

- 14.12.3 Products and Services

- 14.12.4 Financial Overview

- 14.12.5 SWOT Analysis

- 14.12.6 Key Developments

- 14.13 Denso Corp

- 14.13.1 Key Facts

- 14.13.2 Business Description

- 14.13.3 Products and Services

- 14.13.4 Financial Overview

- 14.13.5 SWOT Analysis

- 14.13.6 Key Developments

- 14.14 Luxoft Switzerland AG

- 14.14.1 Key Facts

- 14.14.2 Business Description

- 14.14.3 Products and Services

- 14.14.4 Financial Overview

- 14.14.5 SWOT Analysis

- 14.14.6 Key Developments

- 14.15 Harman International Industries Inc

- 14.15.1 Key Facts

- 14.15.2 Business Description

- 14.15.3 Products and Services

- 14.15.4 Financial Overview

- 14.15.5 SWOT Analysis

- 14.15.6 Key Developments

15. Appendix

- 15.1 Word Index

- 15.2 About The Insight Partners