|

|

市場調査レポート

商品コード

1494564

アジア太平洋地域のグリーンセメント・コンクリート市場:2030年までの予測- 地域別分析- 製品タイプ別、エンドユーザー別Asia Pacific Green Cement and Concrete Market Forecast to 2030 - Regional Analysis - by Product Type (Fly Ash Based, Geopolymer, Slag Based, and Others) and End user (Commercial and Public Infrastructure, Industrial, and Residential) |

||||||

|

|||||||

|

|||||||

| アジア太平洋地域のグリーンセメント・コンクリート市場:2030年までの予測- 地域別分析- 製品タイプ別、エンドユーザー別 |

|

出版日: 2024年04月05日

発行: The Insight Partners

ページ情報: 英文 86 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋地域のグリーンセメント・コンクリート市場は、2022年の180億6,493万米ドルから2030年には226億4,123万米ドルに成長すると予想されています。2022年から2030年までのCAGRは2.9%と推定されます。

機能的性能と能力の向上がアジア太平洋地域のグリーンセメント・コンクリート市場を後押し

グリーンセメントは、フライアッシュや産業廃棄物から生成されるケイ酸アルミニウムから製造されます。アルカリ活性セメントと呼ばれ、従来のポルトランドセメントに比べてCO2発生量が40~45%少ないです。オキシ塩化マグネシウムセメントは、マグネシウム鉱山の製品別である濃縮塩化マグネシウム溶液と酸化マグネシウム粉末から製造されます。このカーボンマイナスで環境に優しいセメントは、従来のセメントよりも圧縮強度に優れ、凝結時間が短いです。さらに、フェロクリート・セメントは、鉄鋼とガラス産業の製品別、主に鉄とシリカから製造されます。これらの材料の組み合わせは、CO2の存在下で製造されるため、カーボンニュートラルなセメント材料が実現します。グリーンセメントの製造に必要な天然資源は少なく、製造過程で環境に排出される二酸化炭素はごくわずかです。また、有毒廃棄物を投棄して環境を汚染することもないです。

標準的なセメントの製造工程では、加熱のために大量の天然ガスを必要とします。グリーンセメントは、産業製品別から製造されるため、製造工程がよりエネルギー効率に優れています。グリーンセメントは、他の標準的なセメントよりも耐火性が高く、固まるまでの時間が短いです。グリーンセメントを使用した建物は寿命が長いです。グリーンセメントの製造工程は、炭素排出を減らし、汚染を最小限に抑えることができるハイエンドの技術に従っています。

グリーンセメントの製造には、高炉スラグ、フライアッシュシリカ、鉄などの製品別を利用する必要があり、これらはコスト効率が良いです。グリーンセメントは、0.5~0.6%の二酸化鉄を含み、セメントの固さと色に強度を与えます。このセメントは乾燥が早く、収縮率が小さいです。耐久性が長く、環境にとってより持続可能な代替材料となります。また、グリーンセメントは断熱性に優れ、耐火性も高いです。グリーンセメントは、橋、道路、空港などの交通量の多い場所でも、重い荷重に耐えることができるため、より現実的な選択肢となります。さらに、グリーンセメントは、粘土や石灰岩のような天然資源を保護することができます。このように、グリーンセメントは耐久性、強度、耐性の面でより高い性能と能力を持ち、市場を牽引しています。

アジア太平洋地域のグリーンセメント・コンクリート市場概要

グリーンセメント産業はアジア太平洋地域で力強い成長を遂げているが、これは同地域の建設セクターの活況と環境問題への関心の高まりを反映しています。主要なセメント生産国である中国やインドなどは、より持続可能なセメント生産方法への転換の必要性を認識しています。この移行は、フライアッシュやスラグの使用、よりクリーンでエネルギー効率の高い製造工程の導入など、グリーンセメント技術の研究開発への投資増加につながっています。例えば、JSWは、鉄鋼業の製品別である高炉スラグから製造されるグリーンセメントやセメント系材料を開発・販売することで、セメント・コンクリート業界に変革をもたらそうとしています。グリーンセメントへのシフトは、持続可能な開発と排出削減の試みに対するこの地域のコミットメントと一致しています。

確立された経済と技術の進歩が、アジア太平洋地域の多様な産業と市場の成長を支えています。APACには多くの人口が存在するため、住宅だけでなく商業建築の需要も増加しています。同地域には、インドやその他多くの東南アジア諸国を含む新興経済諸国があり、インフラ・プロジェクトに対する需要が高まっています。さらに、各国政府はインフラ開発プロジェクトへの民間投資を誘致するため、さまざまな対策を講じています。住宅や商業施設建設プロジェクトへの投資の増加は、APAC諸国におけるグリーンセメントやコンクリートソリューションを含む先端建築材料の需要を押し上げています。

さらに2023年には、アダニ・セメントの子会社であるACCセメントが、新製品であるグリーンコンクリート製品「ACC ECOMaxX」を発売しました。ACC ECOMaxXは、業界で最も包括的なグリーン・コンクリート・ソリューションであり、OPCを使用して施工された基準コンクリートと比較して、体積炭素含有量が30~100%低いです。同製品は、CO2排出量を最大100%削減することでグリーン効果を最大化する独自のグリーン・レディーミックス・テクノロジーを用いて製造されます。

さらに2023年、アンブジャ・セメントはクリンカ生産能力を800万トン拡張する発注を発表しました。この能力拡張プロジェクトは、1,400万トンのグリーンセメント生産をサポートする見込みです。さらに、中国の建設業界は、2022年の経済成長を刺激するためにインフラ支出を増やし、拡大しました。同国のインフラと固定資産投資のバロメーターである最新の掘削機指数は、2022年の建設活動の増加を示しています。業界で認知されたグリーンセメント・コンクリート市場のプレーヤー数社がAPACに進出しているため、建設業界のプレーヤーは型枠ソリューションを容易に入手できます。型枠ソリューションの円滑なサプライチェーンが市場の成長を大きく支えています。同地域における生産能力の増強や新製品開拓のためのこうした政府の取り組みや主要企業の投資が、グリーンセメント・コンクリート市場を牽引しています。

アジア太平洋地域のグリーンセメント・コンクリート市場の収益と2030年までの予測(金額)

アジア太平洋地域のグリーンセメント・コンクリート市場のセグメンテーション

アジア太平洋地域のグリーンセメント・コンクリート市場は、製品タイプ、エンドユーザー、国別に区分されます。

製品タイプ別に見ると、アジア太平洋地域のグリーンセメント・コンクリート市場は、フライアッシュベース、ジオポリマーベース、スラグベース、その他に区分されます。2022年のアジア太平洋地域のグリーンセメント・コンクリート市場では、フライアッシュベースのセグメントが最大のシェアを占めています。

エンドユーザー別では、アジア太平洋地域のグリーンセメント・コンクリート市場は、商業・公共インフラ、産業、住宅に区分されます。2022年のアジア太平洋地域のグリーンセメント・コンクリート市場では、商業・公共インフラ分野が最大のシェアを占めています。

国別に見ると、アジア太平洋地域のグリーンセメント・コンクリート市場は、オーストラリア、中国、インド、日本、韓国、その他アジア太平洋地域に区分されます。2022年のアジア太平洋地域のグリーンセメント・コンクリート市場は中国が独占。

ACC Ltd、UltraTech Cement Ltd、China National Building Material Co Ltd、Anhui Conch Cement Co Ltd、Holcim Ltd、JSW Cement Ltd、Navrattan Green Cement Industries Pvt Ltd、Cemex SAB de CV、HeidelbergCement AGは、アジア太平洋地域のグリーンセメント・コンクリート市場で事業を展開している大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋地域のグリーンセメント・コンクリート市場情勢

- エコシステム分析

- 原材料サプライヤー

- グリーンセメントメーカー

- エンドユーザー

- グリーンセメント・コンクリートのサプライヤー一覧

第5章 アジア太平洋地域のグリーンセメント・コンクリート市場:主要産業力学

- グリーンセメント・コンクリート市場:主要産業力学

- 市場促進要因

- 世界の炭素排出削減への関心の高まり

- 機能的性能と能力の向上

- 有利な政府のイニシアティブと政策

- 市場抑制要因

- グリーンセメント・コンクリートの使用に対する認識不足と消極性

- 市場機会

- インフラ整備の拡大

- 今後の動向

- 公共インフラにおける持続可能な材料の利用拡大

- 促進要因と抑制要因の影響

第6章 グリーンセメント・コンクリート市場:アジア太平洋地域市場分析

- アジア太平洋地域のグリーンセメント・コンクリート市場の収益、2022年~2030年

- アジア太平洋地域のグリーンセメント・コンクリート市場の予測と分析

第7章 アジア太平洋地域のグリーンセメント・コンクリート市場分析:製品タイプ別

- フライアッシュベース

- ジオポリマー

- スラグベース

- その他

第8章 アジア太平洋地域のグリーンセメント・コンクリート市場分析:エンドユーザー別

- 商業・公共インフラ

- 産業

- 住宅

第9章 アジア太平洋地域のグリーンセメント・コンクリート市場:国別分析

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

第10章 業界情勢

- 新製品開発

- 市場イニシアティブ

- 合併と買収

第11章 企業プロファイル

- ACC Ltd

- UltraTech Cement Ltd

- China National Building Material Co Ltd

- Anhui Conch Cement Co Ltd

- Holcim Ltd

- JSW Cement Ltd

- Navrattan Green Cement Industries Pvt Ltd

- Cemex SAB de CV

- HeidelbergCement AG

第12章 付録

List Of Tables

- Table 1. Green Cement and Concrete Market Segmentation

- Table 2. List of Vendors in the Value Chain

- Table 3. Asia Pacific Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Million)

- Table 4. Asia Pacific Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Million) - Product Type

- Table 5. Asia Pacific Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Million) - End-user

- Table 6. Asia Pacific Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By Country

- Table 7. Australia Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By Product Type

- Table 8. Australia Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By End-user

- Table 9. China Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By Product Type

- Table 10. China Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By End-user

- Table 11. India Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By Product Type

- Table 12. India Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By End-user

- Table 13. Japan Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By Product Type

- Table 14. Japan Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By End-user

- Table 15. South Korea Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By Product Type

- Table 16. South Korea Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By End-user

- Table 17. Rest of Asia Pacific Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By Product Type

- Table 18. Rest of Asia Pacific Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn) - By End-user

- Table 19. List of Abbreviation

List Of Figures

- Figure 1. Green Cement and Concrete Market Segmentation, By Country

- Figure 2. Ecosystem: Green Cement and Concrete Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Asia Pacific Green Cement and Concrete Market Revenue (US$ Million), 2022 - 2030

- Figure 5. Asia Pacific Green Cement and Concrete Market Share (%) - Product Type, 2022 and 2030

- Figure 6. Fly ash-based Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 7. Asia Pacific Geopolymer Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 8. Asia Pacific Slag Based Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 9. Others: Green Cement and Concrete Market Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Asia Pacific Green Cement and Concrete Market Share (%) - End-user, 2022 and 2030

- Figure 11. Commercial and Public Infrastructure: Green Cement and Concrete Market Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Industrial: Green Cement and Concrete Market Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Residential: Green Cement and Concrete Market Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Asia Pacific Green Cement and Concrete Market, By Key Country - Revenue 2022 (US$ Mn)

- Figure 15. Asia Pacific Green Cement and Concrete Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 16. Australia Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 17. China Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 18. India Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 19. Japan Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 20. South Korea Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn)

- Figure 21. Rest of Asia Pacific Green Cement and Concrete Market Revenue and Forecasts To 2030 (US$ Mn)

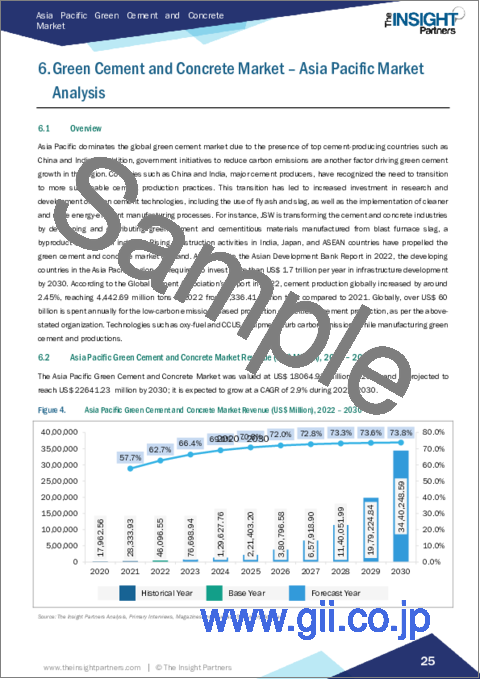

The Asia Pacific green cement and concrete market is expected to grow from US$ 18,064.93 million in 2022 to US$ 22,641.23 million by 2030. It is estimated to record a CAGR of 2.9% from 2022 to 2030.

Improved Functional Performance and Capabilities Fuel Asia Pacific Green Cement and Concrete Market

Green cement is fabricated from aluminum silicates generated from fly ash and industrial wastes. It is termed alkali-activated cement and generates 40-45% less CO2 than conventional portland cement. Magnesium oxychloride cement is fabricated from magnesium mining byproducts known as concentrated magnesium chloride solution and magnesium oxide powder. This carbon-negative and environment-friendly cement has superior compressive strength and a quicker setting time than conventional cement. In addition, Ferrocrete cement is produced from byproducts of the steel and glass industry, primarily iron and silica. A combination of these materials is fabricated in the presence of CO2; thus, a carbon-neutral cement material is achieved. Green cement production needs fewer natural resources, owing to which very little carbon dioxide is emitted into the environment during the production process. It also does not pollute the environment by dumping toxic waste.

The production process of fabricating standard cement requires a large quantity of natural gas for heating purposes. The green cement is fabricated from industrial byproduct which makes the production process more energy efficient. Green cement presents more fire resistance and takes less setting time than other standard cement. Constructions built using green cement have a longer life span. The fabrication process of green cement follows high-end techniques that can decrease carbon discharges, causing minimum pollution.

The production of green cement requires the application of byproducts, such as blast furnace slag, fly ash silica, and iron, which are cost-effective. Green cement possesses 0.5-0.6% iron dioxide in its properties, which offers strength to the solidity and color of the cement. This cement dries out quickly and has a minimal rate of shrinkage. It endures longer and makes for a more sustainable alternative for the environment. Green cement also provides superior thermal insulation and high fire resistance. Green cement is a more viable choice for high-traffic areas such as bridges, roads, and airports, as it can endure heavy loads. Additionally, green cement can preserve natural resources, such as clay and limestone, which are limited resources that are becoming rare. Thus, green cement's higher performance level and capabilities in terms of durability, strength, and resistance propel the market.

Asia Pacific Green Cement and Concrete Market Overview

The green cement industry is experiencing robust growth in Asia Pacific, reflecting the region's booming construction sector alongside increasing environmental concerns. Countries such as China and India, major cement producers, have recognized the need to transition to more sustainable cement production practices. This transition has led to increased investment in research and development of green cement technologies, including the use of fly ash and slag, as well as the implementation of cleaner and more energy-efficient manufacturing processes. For instance, JSW is transforming the cement and concrete industries by developing and distributing green cement and cementitious materials manufactured from blast furnace slag, a byproduct of the steel industry. The shift toward green cement aligns with the region's commitment to sustainable development and emission reduction attempts.

Established economies and technological advancements support the growth of diversified industries and markets in Asia Pacific. The presence of a large population in APAC has led to increased demand for residential as well as commercial construction. The region comprises several developing economies, including India and many other Southeast Asian countries, which poses a strong demand for more infrastructure projects. Further, governments of various countries are taking various measures to attract private investments in infrastructure development projects. Increasing investments in residential and commercial construction projects are boosting the demand for advanced building materials, including green cement and concrete solutions, in APAC countries.

In addition, in 2023, ACC Cement, a subsidiary of Adani Cement, launched its new product, ACC ECOMaxX, a green concrete product. ACC ECOMaxX is the industry's most comprehensive green concrete solution, with a lower embodied carbon content of 30 to 100% compared to a reference concrete constructed using OPC. The products are created using a proprietary Green Ready-Mix Technology that maximizes green effect by reducing CO2 emissions by up to 100%.

Moreover, in 2023, Ambuja Cement announced placing orders to expand its clinker capacity by 8 million tons. This capacity expansion project is expected to support the production of green cement of 14 million tons. Further, China's construction industry expanded as the country increased infrastructure expenditure to stimulate economic growth in 2022. The latest excavator index, a barometer of the country's infrastructure and fixed-asset investment, showed increased construction activity in 2022. Several industry-recognized green cement and concrete market players have a presence in APAC, which leads to the easy availability of formwork solutions to the construction industry players. The smooth supply chain of formwork solutions significantly supports the growth of the market. Such government initiatives and key player investment to increase the production capacities and new product development in the region have driven the green cement and concrete market.

Asia Pacific Green Cement and Concrete Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Green Cement and Concrete Market Segmentation

The Asia Pacific green cement and concrete market is segmented into product type, end user, and country.

Based on product type, the Asia Pacific green cement and concrete market is segmented into fly ash based, geopolymer, slag based, and others. The fly ash-based segment held the largest share of the Asia Pacific green cement and concrete market in 2022.

In terms of end user, the Asia Pacific green cement and concrete market is segmented into commercial and public infrastructure, industrial, and residential. The commercial and public infrastructure segment held the largest share of the Asia Pacific green cement and concrete market in 2022.

Based on country, the Asia Pacific green cement and concrete market is segmented into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific green cement and concrete market in 2022.

ACC Ltd, UltraTech Cement Ltd, China National Building Material Co Ltd, Anhui Conch Cement Co Ltd, Holcim Ltd, JSW Cement Ltd, Navrattan Green Cement Industries Pvt Ltd, Cemex SAB de CV, and HeidelbergCement AG are some of the leading companies operating in the Asia Pacific green cement and concrete market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Green Cement and Concrete Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 Raw Material Suppliers:

- 4.2.2 Green Cement Manufacturers:

- 4.2.3 End Users

- 4.2.4 List of Green Cement and Concrete Suppliers

5. Asia Pacific Green Cement and Concrete Market - Key Industry Dynamics

- 5.1 Green Cement and Concrete Market - Key Industry Dynamics

- 5.2 Market Drivers

- 5.2.1 Increasing Concerns for Mitigating Carbon Emissions Globally

- 5.2.2 Improved Functional Performance and Capabilities

- 5.2.3 Favourable Government Initiatives and Policies

- 5.3 Market Restraints

- 5.3.1 Lack of Awareness and Reluctance to Use Green Cement and Concrete

- 5.4 Market Opportunities

- 5.4.1 Growing Infrastructure Development

- 5.5 Future Trends

- 5.5.1 Growing Utilization of Sustainable Materials in Public Infrastructure

- 5.6 Impact of Drivers and Restraints:

6. Green Cement and Concrete Market - Asia Pacific Market Analysis

- 6.1 Overview

- 6.2 Asia Pacific Green Cement and Concrete Market Revenue (US$ Million), 2022 - 2030

- 6.3 Asia Pacific Green Cement and Concrete Market Forecast and Analysis

7. Asia Pacific Green Cement and Concrete Market Analysis - Product Type

- 7.1 Fly Ash Based

- 7.1.1 Overview

- 7.1.2 Fly Ash-Based Market, Revenue and Forecast to 2030 (US$ Million)

- 7.2 Geopolymer

- 7.2.1 Overview

- 7.2.2 Asia Pacific Geopolymer Market, Revenue and Forecast to 2030 (US$ Million)

- 7.3 Slag Based

- 7.3.1 Overview

- 7.3.2 Slag Based Market, Revenue and Forecast to 2030 (US$ Million)

- 7.4 Others

- 7.4.1 Overview

- 7.4.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Green Cement and Concrete Market Analysis - End-user

- 8.1 Commercial and Public Infrastructure

- 8.1.1 Overview

- 8.1.2 Commercial and Public Infrastructure Market Revenue, and Forecast to 2030 (US$ Million)

- 8.2 Industrial

- 8.2.1 Overview

- 8.2.2 Industrial Market Revenue, and Forecast to 2030 (US$ Million)

- 8.3 Residential

- 8.3.1 Overview

- 8.3.2 Residential Market Revenue, and Forecast to 2030 (US$ Million)

9. Asia Pacific Green Cement and Concrete Market - Country Analysis

- 9.1 Asia Pacific Green Cement and Concrete Market

- 9.1.1 Overview

- 9.1.2 Asia Pacific Green Cement and Concrete Market, By Key Revenue - Revenue 2022 (US$ Mn)

- 9.1.3 Asia Pacific Green Cement and Concrete Market Revenue and Forecasts and Analysis - By Country

- 9.1.3.1 Asia Pacific Green Cement and Concrete Market Revenue and Forecasts and Analysis - By Country

- 9.1.3.2 Australia Green Cement and Concrete Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.3.2.1 Australia Green Cement and Concrete Market Breakdown by Product Type

- 9.1.3.2.2 Australia Green Cement and Concrete Market Breakdown by End-user

- 9.1.3.3 China Green Cement and Concrete Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.3.3.1 China Green Cement and Concrete Market Breakdown by Product Type

- 9.1.3.3.2 China Green Cement and Concrete Market Breakdown by End-user

- 9.1.3.4 India Green Cement and Concrete Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.3.4.1 India Green Cement and Concrete Market Breakdown by Product Type

- 9.1.3.4.2 India Green Cement and Concrete Market Breakdown by End-user

- 9.1.3.5 Japan Green Cement and Concrete Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.3.5.1 Japan Green Cement and Concrete Market Breakdown by Product Type

- 9.1.3.5.2 Japan Green Cement and Concrete Market Breakdown by End-user

- 9.1.3.6 South Korea Green Cement and Concrete Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.3.6.1 South Korea Green Cement and Concrete Market Breakdown by Product Type

- 9.1.3.6.2 South Korea Green Cement and Concrete Market Breakdown by End-user

- 9.1.3.7 Rest of Asia Pacific Green Cement and Concrete Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.3.7.1 Rest of Asia Pacific Green Cement and Concrete Market Breakdown by Product Type

- 9.1.3.7.2 Rest of Asia Pacific Green Cement and Concrete Market Breakdown by End-user

10. Industry Landscape

- 10.1 Overview

- 10.2 New Product Development

- 10.3 Market Initiative

- 10.4 Merger and Acquisition

11. Company Profiles

- 11.1 ACC Ltd

- 11.1.1 Key Facts

- 11.1.2 Business Description

- 11.1.3 Products and Services

- 11.1.4 Financial Overview

- 11.1.5 SWOT Analysis

- 11.1.6 Key Developments

- 11.2 UltraTech Cement Ltd

- 11.2.1 Key Facts

- 11.2.2 Business Description

- 11.2.3 Products and Services

- 11.2.4 Financial Overview

- 11.2.5 SWOT Analysis

- 11.2.6 Key Developments

- 11.3 China National Building Material Co Ltd

- 11.3.1 Key Facts

- 11.3.2 Business Description

- 11.3.3 Products and Services

- 11.3.4 Financial Overview

- 11.3.5 SWOT Analysis

- 11.3.6 Key Developments

- 11.4 Anhui Conch Cement Co Ltd

- 11.4.1 Key Facts

- 11.4.2 Business Description

- 11.4.3 Products and Services

- 11.4.4 Financial Overview

- 11.4.5 SWOT Analysis

- 11.4.6 Key Developments

- 11.5 Holcim Ltd

- 11.5.1 Key Facts

- 11.5.2 Business Description

- 11.5.3 Products and Services

- 11.5.4 Financial Overview

- 11.5.5 SWOT Analysis

- 11.5.6 Key Developments

- 11.6 JSW Cement Ltd

- 11.6.1 Key Facts

- 11.6.2 Business Description

- 11.6.3 Products and Services

- 11.6.4 Financial Overview

- 11.6.5 SWOT Analysis

- 11.6.6 Key Developments

- 11.7 Navrattan Green Cement Industries Pvt Ltd

- 11.7.1 Key Facts

- 11.7.2 Business Description

- 11.7.3 Products and Services

- 11.7.4 Financial Overview

- 11.7.5 SWOT Analysis

- 11.7.6 Key Developments

- 11.8 Cemex SAB de CV

- 11.8.1 Key Facts

- 11.8.2 Business Description

- 11.8.3 Products and Services

- 11.8.4 Financial Overview

- 11.8.5 SWOT Analysis

- 11.8.6 Key Developments

- 11.9 HeidelbergCement AG

- 11.9.1 Key Facts

- 11.9.2 Business Description

- 11.9.3 Products and Services

- 11.9.4 Financial Overview

- 11.9.5 SWOT Analysis

- 11.9.6 Key Developments

12. Appendix

- 12.1 About the Insight Partners

- 12.2 Word Index