|

|

市場調査レポート

商品コード

1481966

抗体薬物複合体のアジア太平洋市場:地域別分析 - 技術別、用途別、流通チャネル別、予測(~2030年)Asia Pacific Antibody Drug Conjugates Market Forecast to 2030 - Regional Analysis - By Technology, Application, and Distribution Channel |

||||||

|

|||||||

|

|||||||

| 抗体薬物複合体のアジア太平洋市場:地域別分析 - 技術別、用途別、流通チャネル別、予測(~2030年) |

|

出版日: 2024年03月04日

発行: The Insight Partners

ページ情報: 英文 101 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋の抗体薬物複合体の市場規模は、2022年に15億3,283万米ドルに達し、2022~2030年にかけてCAGR 20.8%で成長し、2030年には69億7,103万米ドルに達すると予測されています。

同意管理におけるAIニーズの高まりがアジア太平洋の抗体薬物複合体市場を後押し

がん罹患率の増加は、主に革新的ながん治療に対する需要の増加につながっています。2020年に発表されたGlobal Cancer Observatory(GLOBOCAN)の推計によると、世界中で1,930万人のがん患者が発生しています。中国とインドががん患者数の上位を占めています。GLOBOCANはまた、インドのがん患者は2040年までに208万人になり、2020年から57.5%増加すると推定しています。同様に、2022年2月に発表された世界保健機関(WHO)のデータでは、~1,000万人ががんで死亡しています。最もよく見られるがんの種類は、肺がん、乳がん、結腸・直腸がん、前立腺がん、乳房がんです。がんの増加により、世界中で懸念が高まっています。以下は、2020年に世界で報告された一般的ながん症例のリストです。

- 表1. 世界で新たに発生するがん、2020年

がん種 罹患数(100万人)

1 Stomach 1.09

2 Skin (non-melanoma) 1.2

3 Prostate 1.41

4 Colon and Rectum 1.93

5 Lung 2.21

6 Breast 2.26

がんは現在、不健康な食習慣を持ち、運動不足の人によく見られる生活習慣病です。また、アルコールやタバコの摂取も、がん発症のリスクを高める。中低所得国における慢性感染症は、がんの危険因子をさらに悪化させる。2022年2月に発表されたWHOのデータによると、ヒトパピローマウイルス(HPV)、ヘリコバクターピロリ菌、B型肝炎ウイルス、C型肝炎ウイルス、エプスタインバーウイルスなどの慢性感染症は、2018年に診断された患者の18%近くを占めています。また、ADCの有望な結果は、効果的ながん治療としての需要を加速し、市場成長を促進すると予想されます。

アジア太平洋の抗体薬物複合体市場の概要

アジア太平洋の抗体薬物複合体(ADC)市場は、中国、日本、インド、韓国、オーストラリア、その他のアジア太平洋に区分されます。ADC市場の成長は、企業提携、がん罹患率の増加、臨床試験の増加によって大きく牽引されています。

ADCの開発に携わるアジア太平洋諸国の主要企業は、臨床試験を完了した後に市場に投入するパイプライン製品を持っています。2023年6月、RemeGen Co., Ltd.はInnovent Biologics, Inc.と臨床試験を開始し、新規メソセリン(MSLN)標的抗体薬物複合体(ADC)であるRC88との併用療法TYVYT(シンチリマブ注射剤)、または新規c-Met標的ADCであるRC108との併用療法TYVYTを供給する契約を締結しました。これらは固形がんを治療する新規治療薬であると主張しています。本契約に基づき、RemeGenはTYVYTの抗腫瘍活性と安全性を評価するため、第1/2a相臨床試験を実施します。同社はまた、Distamab vedotin(RC48)とPD1の併用療法をパイプラインに有しています。この併用療法は、異なるがん適応症に対して2つのフェーズで評価されており、最初の併用療法は尿路上皮がんを対象とした第III相試験、2つ目は筋層浸潤性膀胱がんおよび胃がんを対象とした第II相試験です。

さらに、日本企業は画期的な製品を投入しており、ADC市場を席巻することが予想されます。2021年6月、Daiichi Sankyo CompanyとAstraZeneca plcは、HER2低値乳がん患者を治療するために開発された新規クラスのADCであるEnhertuを発売しました。Daiichi Sankyo Companyは、米国と欧州の売上高を合算した2023年第1四半期の売上高が前年同期比156.6%増となったことを報告しました。このような同社の売上高の大幅な伸びは、同国のADC市場規模に大きく寄与しており、今後数年間で飛躍的に成長すると推定されます。

アジア太平洋の抗体薬物複合体市場の収益と2030年までの予測(金額)

アジア太平洋の抗体薬物複合体市場のセグメンテーション

アジア太平洋の抗体薬物複合体市場は、技術、用途、流通チャネル、国によって区分されます。

技術別に見ると、アジア太平洋の抗体薬物複合体市場は開裂性リンカーと非開裂性リンカーに二分されます。2022年には開裂性リンカーセグメントがより大きなシェアを占めています。

用途別では、アジア太平洋の抗体薬物複合体市場は血液がん、乳がん、卵巣がん、尿路上皮がん、その他に区分されます。2022年には乳がん分野が最大のシェアを占めています。

流通チャネル別に見ると、アジア太平洋の抗体薬物複合体市場は病院薬局、小売薬局、オンライン薬局に区分されます。2022年には病院薬局セグメントが最大のシェアを占める。

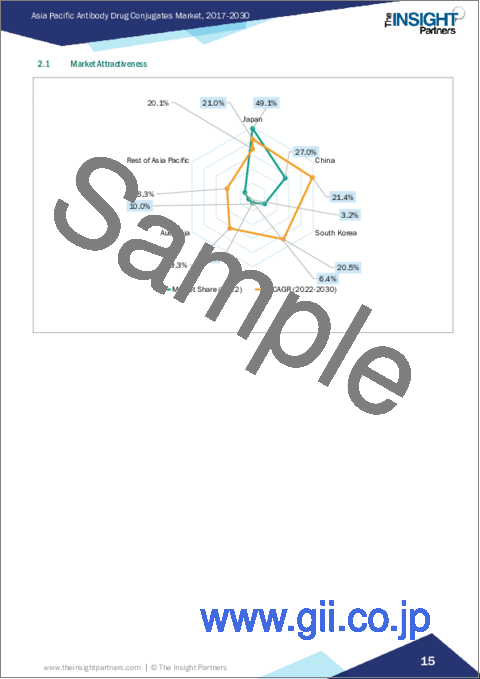

国別に見ると、アジア太平洋の抗体医薬結合体市場はオーストラリア、中国、インド、日本、韓国、その他アジア太平洋に分類されます。2022年のアジア太平洋抗体薬物複合体市場は日本が支配的でした。

Pfizer Inc、Hoffmann-La Roche Ltd、GSK Plc、Gilead Sciences Inc、AstraZeneca Plc、Astellas Pharma Inc、RemeGen Co Ltd、武田薬品工業は、アジア太平洋の抗体薬物複合体市場で事業を展開している大手企業の一部です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋の抗体薬物複合体市場 - 主要産業力学

- 主な市場促進要因

- 抗体薬物複合体開発のための戦略的パートナーシップの拡大

- がん患者の増加

- ADCに対するFDA承認の増加

- 市場抑制要因

- ADCの開発と商業化にかかる高コスト

- 市場機会

- ADC開発への投資の増加

- 市場動向

- ADCのパイプラインの増加

- 影響分析

第5章 抗体薬物複合体市場:アジア太平洋市場分析

- アジア太平洋の抗体薬物複合体の市場収益(2017~2030年)

第6章 アジア太平洋の抗体薬物複合体市場:収益・予測(~2030年):技術別

- アジア太平洋の抗体薬物複合体市場の収益シェア、技術別、2022年・2030年(%)

- 開裂性リンカー

- 非開裂性リンカー

第7章 アジア太平洋の抗体薬物複合体市場:収益・予測(~2030年):用途別

- アジア太平洋の抗体薬物複合体市場の収益シェア、用途別、2022年・2030年(%)

- 血液がん

- 乳がん

- 卵巣がん

- 尿路上皮がん

- その他

第8章 アジア太平洋の抗体薬物複合体市場:収益・予測(~2030年):流通チャネル別

- アジア太平洋の抗体薬物複合体市場の収益シェア、流通チャネル別、2022年・2030年(%)

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 アジア太平洋の抗体薬物複合体市場:国別分析

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他のアジア太平洋

第10章 アジア太平洋の抗体薬物複合体市場:産業情勢

- 有機的成長戦略

- 無機的成長戦略

- 各社の生産能力

第11章 企業プロファイル

- Pfizer Inc

- Hoffmann-La Roche Ltd

- GSK Plc

- Gilead Sciences Inc

- AstraZeneca Plc

- Astellas Pharma Inc

- RemeGen Co Ltd

- Takeda Pharmaceutical Co Ltd

第12章 付録

List Of Tables

- Table 1. Asia Pacific Antibody Drug Conjugates Market Segmentation

- Table 2. New Cancer Cases Worldwide, in 2020

- Table 3. List of FDA-Approved ADCs

- Table 4. China: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Technology

- Table 5. China: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Application

- Table 6. China: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Distribution Channel

- Table 7. Japan: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Technology

- Table 8. Japan: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Application

- Table 9. Japan: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Distribution Channel

- Table 10. India: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Technology

- Table 11. India: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Application

- Table 12. India: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Distribution Channel

- Table 13. South Korea: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Technology

- Table 14. South Korea: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Application

- Table 15. South Korea: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Distribution Channel

- Table 16. Australia: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Technology

- Table 17. Australia: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Application

- Table 18. Australia: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Distribution Channel

- Table 19. Rest of Asia Pacific: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Technology

- Table 20. Rest of Asia Pacific: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Application

- Table 21. Rest of Asia Pacific: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn) - Distribution Channel

- Table 22. Recent Organic Growth Strategies in Antibody Drug Conjugates Market

- Table 23. Recent Inorganic Growth Strategies in the Antibody Drug Conjugates Market

- Table 24. Glossary of Terms, Antibody Drug Conjugates Market

List Of Figures

- Figure 1. Asia Pacific Antibody Drug Conjugates Market Segmentation, By Country

- Figure 2. Key Insights

- Figure 3. Asia Pacific Antibody Drug Conjugates Market - Key Industry Dynamics

- Figure 4. Impact Analysis of Drivers and Restraints

- Figure 5. Asia Pacific Antibody Drug Conjugates Market Revenue (US$ Mn), 2017 - 2030

- Figure 6. Asia Pacific Antibody Drug Conjugates Market Revenue Share, by Technology 2022 & 2030 (%)

- Figure 7. Cleavable Linker: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Non-Cleavable Linker: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Asia Pacific Antibody Drug Conjugates Market Revenue Share, by Application 2022 & 2030 (%)

- Figure 10. Blood Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Breast Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Ovarian Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Urothelial Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Others: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Asia Pacific Antibody Drug Conjugates Market Revenue Share, by Distribution Channel 2022 & 2030 (%)

- Figure 16. Hospital Pharmacies: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Retail Pharmacies: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Online Pharmacies: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. Asia Pacific Antibody Drug Conjugates, by Key Country - Revenue (2022) (US$ Million)

- Figure 20. Asia Pacific: Antibody Drug Conjugates Market, By Key Countries, 2022 And 2030 (%)

- Figure 21. China: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 22. Japan: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 23. India: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 24. South Korea: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 25. Australia: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 26. Rest of Asia Pacific: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

The Asia Pacific antibody drug conjugates market was valued at US$ 1,532.83 million in 2022 and is expected to reach US$ 6,971.03 million by 2030; it is estimated to grow at a CAGR of 20.8% from 2022 to 2030.

Rising Need for AI in Consent Management Fuels the Asia Pacific Antibody Drug Conjugates Market

Rising cancer incidences are primarily leading to the increasing demand for innovative cancer treatments. As per the Global Cancer Observatory (GLOBOCAN) estimates published in 2020, there were 19.3 million cancer cases across the globe. China, and India were among the countries leading in cancer cases. The GLOBOCAN has also estimated that the cancer cases in India will be ~2.08 million by 2040, representing a rise of 57.5% from 2020. Similarly, as per the World Health Organization (WHO) data published in February 2022, ~10 million people have died from cancer. The most commonly seen cancer types were lung, breast, colon and rectum, prostate, and breast. The rising incidences of cancer have raised concerns worldwide. Below is the list of common cancer cases reported worldwide in 2020.

- Table 1. New Cancer Cases Worldwide, in 2020

Sr. No. Cancer Type Number of Cases (Million)

1 Stomach 1.09

2 Skin (non-melanoma) 1.2

3 Prostate 1.41

4 Colon and Rectum 1.93

5 Lung 2.21

6 Breast 2.26

Cancer is now a lifestyle disease commonly seen among people with unhealthy food habits and who are physically inactive. Also, the consumption of alcohol and tobacco adds up to the risk of developing cancer. Chronic infectious diseases in low- and middle-income countries can further aggravate the cancer risk factors. According to the WHO data published in February 2022, chronic infectious diseases such as human papillomavirus (HPV), Helicobacter pylori, hepatitis B virus, hepatitis C virus, and Epstein-Barr virus attributed to nearly 18% of the diagnosed in 2018. Also, promising results of ADCs are anticipated to accelerate their demand as an effective cancer treatment and propel the market growth.

Asia Pacific Antibody Drug Conjugates Market Overview

The Asia Pacific antibody drug conjugates (ADCs) market is segmented into China, Japan, India, South Korea, Australia, and the Rest of Asia Pacific. The growth of the ADCs market is widely driven by company collaborations, growing incidences of cancer, and increasing clinical trials.

The leading companies in Asia Pacific countries that are involved in developing ADCs have pipeline products to be launched in the market after completing the clinical trials. In June 2023, RemeGen Co., Ltd. signed an agreement with Innovent Biologics, Inc. to enter clinical trials and supply combination therapies TYVYT (sintilimab injection) with RC88, a novel mesothelin (MSLN)-targeting antibody-drug conjugate (ADC), or TYVYT with RC108, a novel c-Met-targeting ADC. These are claimed to be novel therapies to treat solid tumors. Under the agreement, RemeGen Co., Ltd will conduct Phase 1/2a clinical studies for TYVYT to evaluate the anti-tumor activity and safety. The company also has Distamab vedotin (RC48) +PD1 combination in the pipeline. The combination is evaluated in two phases for different cancer indications, first combination is in phase III, evaluated to treat urothelial cancer in and second is in phase II, evaluated to treat muscle invasive bladder and gastric cancer.

In addition, Japanese companies are introducing breakthrough products that are expected to dominate the ADCs market. In June 2021, Daiichi Sankyo Company, Limited, and AstraZeneca plc launched Enhertu-a novel class of ADCs developed to treat HER2-low breast cancer patients. Daiichi Sankyo Company, Limited reported a year-on-year sales growth of 156.6% in the first quarter of 2023 by combining the US and European sales. Such a huge growth in the company's sales has significantly contributed to the ADCs market size in the country and is estimated to grow exponentially in the coming years.

Asia Pacific Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Antibody Drug Conjugates Market Segmentation

The Asia Pacific antibody drug conjugates market is segmented based on technology, application, distribution channel, and country.

Based on technology, the Asia Pacific antibody drug conjugates market antibody drug conjugates market is bifurcated into cleavable linker and non-cleavable linker. The cleavable linker segment held a larger share in 2022.

Based on application, the Asia Pacific antibody drug conjugates market antibody drug conjugates market is segmented into blood cancer, breast cancer, ovarian cancer, urothelial cancer, and others. The breast cancer segment held the largest share in 2022.

Based on distribution channel, the Asia Pacific antibody drug conjugates market antibody drug conjugates market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment held the largest share in 2022.

Based on country, the Asia Pacific antibody drug conjugates market is categorized into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. Japan dominated the Asia Pacific antibody drug conjugates market in 2022.

Pfizer Inc, Hoffmann-La Roche Ltd, GSK Plc, Gilead Sciences Inc, AstraZeneca Plc, Astellas Pharma Inc, RemeGen Co Ltd, and Takeda Pharmaceutical Co Ltd are some of the leading companies operating in the Asia Pacific antibody drug conjugates market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Antibody Drug Conjugates Market - Key Industry Dynamics

- 4.1 Key Market Drivers:

- 4.1.1 Growing Strategic Partnerships to Develop Antibody Drug Conjugates

- 4.1.2 Rising Incidences of Cancer Cases

- 4.1.3 Increasing FDA Approvals for ADCs

- 4.2 Market Restraints

- 4.2.1 High Cost of ADCs Development and Commercialization

- 4.3 Market Opportunities

- 4.3.1 Increasing Investments to Develop ADCs

- 4.4 Market Trends

- 4.4.1 Escalating Pipeline of ADCs

- 4.5 Impact Analysis:

5. Antibody Drug Conjugates Market - Asia Pacific Market Analysis

- 5.1 Asia Pacific Antibody Drug Conjugates Market Revenue (US$ Mn), 2017 - 2030

6. Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 - by Technology

- 6.1 Overview

- 6.2 Asia Pacific Antibody Drug Conjugates Market Revenue Share, by Technology 2022 & 2030 (%)

- 6.3 Cleavable Linker

- 6.3.1 Overview

- 6.3.2 Cleavable Linker: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- 6.4 Non-cleavable Linker

- 6.4.1 Overview

- 6.4.2 Non-cleavable Linker: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

7. Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 - by Application

- 7.1 Overview

- 7.2 Asia Pacific Antibody Drug Conjugates Market Revenue Share, by Application 2022 & 2030 (%)

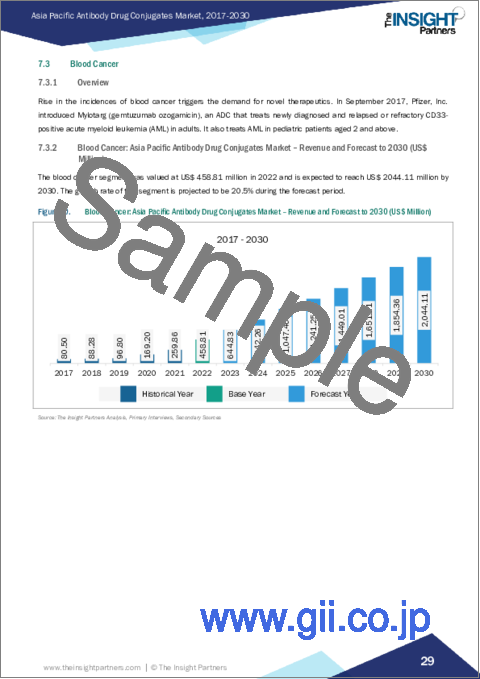

- 7.3 Blood Cancer

- 7.3.1 Overview

- 7.3.2 Blood Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 Breast Cancer

- 7.4.1 Overview

- 7.4.2 Breast Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- 7.5 Ovarian Cancer

- 7.5.1 Overview

- 7.5.2 Ovarian Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- 7.6 Urothelial Cancer

- 7.6.1 Overview

- 7.6.2 Urothelial Cancer: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- 7.7 Others

- 7.7.1 Overview

- 7.7.2 Others: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 - by Distribution Channel

- 8.1 Overview

- 8.2 Asia Pacific Antibody Drug Conjugates Market Revenue Share, by Distribution Channel 2022 & 2030 (%)

- 8.3 Hospital Pharmacies

- 8.3.1 Overview

- 8.3.2 Hospital Pharmacies: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Retail Pharmacies

- 8.4.1 Overview

- 8.4.2 Retail Pharmacies: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 Online Pharmacies

- 8.5.1 Overview

- 8.5.2 Online Pharmacies: Asia Pacific Antibody Drug Conjugates Market - Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Antibody Drug Conjugates Market - Country Analysis

- 9.1 Asia Pacific Antibody Drug Conjugates Market, Revenue and Forecast To 2030

- 9.1.1 Overview

- 9.1.2 Asia Pacific Antibody Drug Conjugates Market Breakdown, by key Country - Revenue (2022) (US$ Million)

- 9.1.3 Asia Pacific: Antibody Drug Conjugates Market, by Country

- 9.1.3.1 China

- 9.1.3.1.1 Overview

- 9.1.3.1.2 China: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- 9.1.3.1.3 China: Antibody Drug Conjugates Market, by Technology

- 9.1.3.1.4 China: Antibody Drug Conjugates Market, by Application

- 9.1.3.1.5 China: Antibody Drug Conjugates Market, by Distribution Channel

- 9.1.3.2 Japan

- 9.1.3.2.1 Overview

- 9.1.3.2.2 Japan: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- 9.1.3.2.3 Japan: Antibody Drug Conjugates Market, by Technology

- 9.1.3.2.4 Japan: Antibody Drug Conjugates Market, by Application

- 9.1.3.2.5 Japan: Antibody Drug Conjugates Market, by Distribution Channel

- 9.1.3.3 India

- 9.1.3.3.1 Overview

- 9.1.3.3.2 India: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- 9.1.3.3.3 India: Antibody Drug Conjugates Market, by Technology

- 9.1.3.3.4 India: Antibody Drug Conjugates Market, by Application

- 9.1.3.3.5 India: Antibody Drug Conjugates Market, by Distribution Channel

- 9.1.3.4 South Korea

- 9.1.3.4.1 Overview

- 9.1.3.4.2 South Korea: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- 9.1.3.4.3 South Korea: Antibody Drug Conjugates Market, by Technology

- 9.1.3.4.4 South Korea: Antibody Drug Conjugates Market, by Application

- 9.1.3.4.5 South Korea: Antibody Drug Conjugates Market, by Distribution Channel

- 9.1.3.5 Australia

- 9.1.3.5.1 Overview

- 9.1.3.5.2 Australia: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- 9.1.3.5.3 Australia: Antibody Drug Conjugates Market, by Technology

- 9.1.3.5.4 Australia: Antibody Drug Conjugates Market, by Application

- 9.1.3.5.5 Australia: Antibody Drug Conjugates Market, by Distribution Channel

- 9.1.3.6 Rest of Asia Pacific

- 9.1.3.6.1 Overview

- 9.1.3.6.2 Rest of Asia Pacific: Antibody Drug Conjugates Market Revenue and Forecast to 2030 (US$ Mn)

- 9.1.3.6.3 Rest of Asia Pacific: Antibody Drug Conjugates Market, by Technology

- 9.1.3.6.4 Rest of Asia Pacific: Antibody Drug Conjugates Market, by Application

- 9.1.3.6.5 Rest of Asia Pacific: Antibody Drug Conjugates Market, by Distribution Channel

- 9.1.3.1 China

10. Asia Pacific Antibody Drug Conjugates Market-Industry Landscape

- 10.1 Overview

- 10.2 Organic Growth Strategies

- 10.2.1 Overview

- 10.3 Inorganic Growth Strategies

- 10.3.1 Overview

- 10.4 Companies' Manufacturing Capacities and Capabilities

11. Company Profiles

- 11.1 Pfizer Inc

- 11.1.1 Key Facts

- 11.1.2 Business Description

- 11.1.3 Products and Services

- 11.1.4 Financial Overview

- 11.1.5 SWOT Analysis

- 11.1.6 Key Developments

- 11.2 Hoffmann-La Roche Ltd

- 11.2.1 Key Facts

- 11.2.2 Business Description

- 11.2.3 Products and Services

- 11.2.4 Financial Overview

- 11.2.5 SWOT Analysis

- 11.2.6 Key Developments

- 11.3 GSK Plc

- 11.3.1 Key Facts

- 11.3.2 Business Description

- 11.3.3 Products and Services

- 11.3.4 Financial Overview

- 11.3.5 SWOT Analysis

- 11.3.6 Key Developments

- 11.4 Gilead Sciences Inc

- 11.4.1 Key Facts

- 11.4.2 Business Description

- 11.4.3 Products and Services

- 11.4.4 Financial Overview

- 11.4.5 SWOT Analysis

- 11.4.6 Key Developments

- 11.5 AstraZeneca Plc

- 11.5.1 Key Facts

- 11.5.2 Business Description

- 11.5.3 Products and Services

- 11.5.4 Financial Overview

- 11.5.5 SWOT Analysis

- 11.5.6 Key Developments

- 11.6 Astellas Pharma Inc

- 11.6.1 Key Facts

- 11.6.2 Business Description

- 11.6.3 Products and Services

- 11.6.4 Financial Overview

- 11.6.5 SWOT Analysis

- 11.6.6 Key Developments

- 11.7 RemeGen Co Ltd

- 11.7.1 Key Facts

- 11.7.2 Business Description

- 11.7.3 Products and Services

- 11.7.4 Financial Overview

- 11.7.5 SWOT Analysis

- 11.7.6 Key Developments

- 11.8 Takeda Pharmaceutical Co Ltd

- 11.8.1 Key Facts

- 11.8.2 Business Description

- 11.8.3 Products and Services

- 11.8.4 Financial Overview

- 11.8.5 SWOT Analysis

- 11.8.6 Key Developments

12. Appendix

- 12.1 About Us

- 12.2 Glossary of Terms