|

|

市場調査レポート

商品コード

1452639

アジア太平洋のガラス繊維パイプ市場の2028年までの予測-地域別分析:樹脂タイプ別、最終用途別Asia Pacific Fiberglass Pipes Market Forecast to 2028 - Regional Analysis - by Resin Type (Polyester, Epoxy, Phenolic, and Others) and End-Use (Oil and Gas, Sewage, Chemicals, Agriculture, and Others) |

||||||

|

|

|||||||

| アジア太平洋のガラス繊維パイプ市場の2028年までの予測-地域別分析:樹脂タイプ別、最終用途別 |

|

出版日: 2024年01月16日

発行: The Insight Partners

ページ情報: 英文 137 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

アジア太平洋のガラス繊維パイプ市場は、2022年の14億5,717万米ドルから2028年には20億683万米ドルに成長すると予測されています。2022年から2028年までのCAGRは5.5%と推定されます。

従来型パイプよりも複合パイプを好むエンドユーザーの増加がアジア太平洋のガラス繊維パイプ市場を後押し

金属、コンクリート、スチール、プラスチック、複合材料は、石油・ガス輸送、廃水処理から化学パイプラインまで、さまざまな用途のパイプ製造に使用されています。最終用途産業がパイプを選択する際に考慮する主要要因は、材料の種類とサイズです。耐腐食性、無毒性、耐衝撃性、耐候性、水力効率、長寿命、軽量、低熱伝導性などの特性により、ガラス繊維パイプは従来のコンクリート、金属、プラスチックパイプよりも好まれています。

ガラス繊維パイプのメーカーやサプライヤーは、腐食性のある危険な用途向けに幅広い製品を提供しています。エンデューロ・コンポジット社は、プラント仕様と業界標準を満たすガラス繊維パイプを提供しています。このポートフォリオには、ダウンタイムの低減、高強度、耐久性、1,000種類の化学薬品への耐性、-40°Fから300°Fまでの温度耐性などの特性を備えたガラス繊維パイプが含まれています。鋼管やコンクリート管は腐食の影響を受けやすく、管の構造的完全性に悪影響を及ぼします。Burgess Well Company Inc.は、非導電性、耐トルク性、耐高圧性のガラス繊維パイプを提供しています。メーカーが提供するグラスファイバー・パイプの幅広い品揃えと、複合パイプへの嗜好の高まりにより、原油輸送や化学・水セグメントなど、いくつかの用途で従来のパイプに取って代わることが期待されています。

アジア太平洋のガラス繊維パイプ市場概要

アジア太平洋のガラス繊維パイプ市場は、オーストラリア、中国、インド、日本、韓国、その他のアジア太平洋に区分されます。この地域は、化学・石油・ガスセクターの成長、都市化の進展による下水システム需要の増加により、ガラス繊維パイプの有力な市場となっています。さらに、メイク・イン・インドなどの政府の取り組みや政策により、インドではさまざまな製造工場の設立が奨励されています。外国直接投資の増加も地域の経済成長につながり、地域の工業化をさらに後押ししています。化学製造業は、中国、韓国、インド、日本を含むいくつかのアジア諸国にとって、製造輸出の重要な部分を占めています。国際化学工業協会協議会(ICCA)によると、アジア太平洋の化学産業は、同地域のGDPと雇用に最も貢献しており、産業全体の年間経済価値の45%、支援される全雇用の69%を生み出しています。

さらに、アジア太平洋では石油・ガスの需要が増加しています。国際エネルギー機関(IEA)によると、世界の石油需要は2021年に回復し、2025年にはアジアが石油需要の77%を占めると予想されています。アジアの石油輸入需要は、2025年までに日量3,100万バレルを超えると予想されています。アジアの主要国はすべて、中東・アフリカからの石油輸入に大きく依存しています。この地域のさまざまな国々が、石油・ガス需要の増加に対応するためのプロジェクトを開始しています。例えば、2023年4月、インド・アッサム州のジョルハットとマジュリを結ぶブラマプトラ川の地下に、アジア最大の水中炭素パイプラインがIndradhanush Gas Grid Limited (IGGL)によって完成しました。このように、このようなプロジェクトに対する投資の増加は、予測期間中にガラス繊維パイプ市場を強化すると予想されます。

アジア太平洋のガラス繊維パイプ市場の収益と2028年までの予測(金額)

アジア太平洋のガラス繊維パイプ市場のセグメンテーション

アジア太平洋のガラス繊維パイプ市場は、樹脂タイプ、最終用途、国別に区分されます。

樹脂タイプ別に見ると、アジア太平洋のガラス繊維パイプ市場は、ポリエステル、エポキシ、フェノール、その他に区分されます。2022年のアジア太平洋ガラス繊維パイプ市場シェアはポリエステルセグメントが最大。

最終用途別では、アジア太平洋ガラス繊維パイプ市場は石油・ガス、下水、化学、農業、その他に区分されます。石油・ガスセグメントが2022年のアジア太平洋ガラス繊維パイプ市場シェアで最大を占めました。

国別に見ると、アジア太平洋のグラスファイバー管市場は、オーストラリア、中国、インド、日本、韓国、その他のアジア太平洋に分類されます。2022年のアジア太平洋ガラス繊維パイプ市場は中国が独占。

Amiblu Holding GmbH、Chemical Process Piping Pvt Ltd、EPP Composites Pvt Ltd、Fibrex FRP Piping Systems、Future Pipe Industries LLC、Gruppo Sarplast Srl、Lianyungang Zhongfu Lianzhong Composites Group Co Ltd、NOV Inc、Plasticon Germany GmbH、Poly Plast Chemi Plants(I)Pvt Ltd、Saudi Arabian Amiantit Co、Sunrise Industries(インド)Ltdは、アジア太平洋ガラス繊維パイプ市場で事業を展開している大手企業です。

目次

第1章 イントロダクション

第2章 要点

第3章 調査手法

- 調査範囲

- 調査手法

- データ収集

- 一次インタビュー

- 仮説の策定

- マクロ経済要因分析

- 基礎数値の作成

- データの三角測量

- 国レベルのデータ

第4章 アジア太平洋のガラス繊維パイプ市場情勢

- アジア太平洋のガラス繊維パイプ市場概要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 競争企業間の敵対関係

- 代替品の脅威

- エコシステム分析

- 原材料サプライヤー

- メーカー

- ディストリビューター/サプライヤー

- 最終用途産業

- 専門家の見解

第5章 アジア太平洋のガラス繊維パイプ市場:主要市場力学

- 市場促進要因

- 石油・ガスパイプライン敷設の増加

- 化学産業におけるガラス繊維パイプ需要の増加

- 市場抑制要因

- 原材料価格の変動

- 市場機会

- 廃水システムにおけるガラス繊維パイプの採用

- 今後の動向

- エンドユーザーによる従来型パイプより複合パイプへの好みの高まり

- 影響分析

第6章 ガラス繊維パイプ:アジア太平洋市場分析

- アジア太平洋のガラス繊維パイプ市場:2028年までの数量予測(1,000メートル)

- アジア太平洋のガラス繊維パイプ市場:収益と2028年までの予測

第7章 アジア太平洋のガラス繊維パイプ市場分析:樹脂タイプ別

- イントロダクション

- アジア太平洋のガラス繊維パイプ市場:樹脂タイプ別(2021年、2028年)

- ポリエステル

- エポキシ

- フェノール樹脂

- その他

第8章 アジア太平洋のガラス繊維パイプ市場分析:最終用途別

- イントロダクション

- アジア太平洋のガラス繊維パイプ市場:最終用途別(2021年、2028年)

- 石油・ガス

- 下水

- 化学

- 農業

- その他

第9章 アジア太平洋のガラス繊維パイプ市場:国別分析

- アジア太平洋

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

第10章 企業プロファイル

- Amiblu Holding GmbH

- Chemical Process Piping Pvt Ltd

- EPP Composites Pvt Ltd

- Fibrex FRP Piping Systems

- Future Pipe Industries LLC

- Gruppo Sarplast Srl

- Lianyungang Zhongfu Lianzhong Composites Group Co Ltd

- NOV Inc

- Saudi Arabian Amiantit Co

- Sunrise Industries(インド)Ltd

- Poly Plast Chemi Plants(I)Pvt Ltd

- Plasticon Germany GmbH

第11章 付録

List Of Tables

- Table 1. Asia Pacific Fiberglass Pipes Market -Volume and Forecast to 2028 (Thousand Meters)

- Table 2. Asia Pacific Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- Table 3. Asia Pacific Fiberglass Pipes Market, by Resin Type - Volume and Forecast to 2028 (Thousand Meters)

- Table 4. Asia Pacific Fiberglass Pipes Market, by Resin Type - Revenue and Forecast to 2028 (US$ Million)

- Table 5. Asia Pacific Fiberglass Pipes Market, by End Use - Revenue and Forecast to 2028 (US$ Million)

- Table 6. Australia Fiberglass Pipes Market, by Resin Type- Volume and Forecast to 2028 (Thousand Meters)

- Table 7. Australia Fiberglass Pipes Market, by Resin Type- Revenue and Forecast to 2028 (US$ Million)

- Table 8. Australia Fiberglass Pipes Market, by End Use - Revenue and Forecast to 2028 (US$ Million)

- Table 9. China Fiberglass Pipes Market, by Resin Type - Volume and Forecast to 2028 (Thousand Meters)

- Table 10. China Fiberglass Pipes Market, by Resin Type - Revenue and Forecast to 2028 (US$ Million)

- Table 11. China Fiberglass Pipes Market, by End Use - Revenue and Forecast to 2028 (US$ Million)

- Table 12. India Fiberglass Pipes Market, by Resin Type - Volume and Forecast to 2028 (Thousand Meters)

- Table 13. India Fiberglass Pipes Market, by Resin Type - Revenue and Forecast to 2028 (US$ Million)

- Table 14. India Fiberglass Pipes Market, by End Use - Revenue and Forecast to 2028 (US$ Million)

- Table 15. Japan Fiberglass Pipes Market, by Resin Type - Volume and Forecast to 2028 (Thousand Meters)

- Table 16. Japan Fiberglass Pipes Market, by Resin Type - Revenue and Forecast to 2028 (US$ Million)

- Table 17. Japan Fiberglass Pipes Market, by End Use - Revenue and Forecast to 2028 (US$ Million)

- Table 18. South Korea Fiberglass Pipes Market, by Resin Type - Volume and Forecast to 2028 (Thousand Meters)

- Table 19. South Korea Fiberglass Pipes Market, by Resin Type - Revenue and Forecast to 2028 (US$ Million)

- Table 20. South Korea Fiberglass Pipes Market, by End Use - Revenue and Forecast to 2028 (US$ Million)

- Table 21. Rest of Asia Pacific Fiberglass Pipes Market, by Resin Type - Volume and Forecast to 2028 (Thousand Meters)

- Table 22. Rest of Asia Pacific Fiberglass Pipes Market, by Resin Type - Revenue and Forecast to 2028 (US$ Million)

- Table 23. Rest of Asia Pacific Fiberglass Pipes Market, by End Use - Revenue and Forecast to 2028 (US$ Million)

- Table 24. Glossary of Terms, Asia Pacific Fiberglass Pipes Market

List Of Figures

- Figure 1. Asia Pacific Fiberglass Pipes Market Segmentation

- Figure 2. Asia Pacific Fiberglass Pipes Market Segmentation - By Country

- Figure 3. Asia Pacific Fiberglass Pipes Market Overview

- Figure 4. Asia Pacific Fiberglass Pipes Market, By End-Use

- Figure 5. Asia Pacific Fiberglass Pipes Market, by Country

- Figure 6. Porter's Five Forces Analysis of Asia Pacific Fiberglass Pipes Market

- Figure 7. Asia Pacific Fiberglass Pipes Market, Ecosystem

- Figure 8. Asia Pacific Expert Opinion

- Figure 10. Asia Pacific Fiberglass Pipes Market Impact Analysis of Drivers and Restraints

- Figure 11. Asia Pacific Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- Figure 12. Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 13. Asia Pacific Fiberglass Pipes Market Revenue Share, By Resin Type (2021 and 2028)

- Figure 14. Polyester: Asia Pacific Fiberglass Pipes Market - Volume and Forecast To 2028 (Thousand Meters)

- Figure 15. Polyester: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 16. Epoxy : Asia Pacific Fiberglass Pipes Market - Volume and Forecast To 2028 (Thousand Meters)

- Figure 17. Epoxy : Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 18. Phenolic: Asia Pacific Fiberglass Pipes Market - Volume and Forecast To 2028 (Thousand Meters)

- Figure 19. Phenolic: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 20. Others: Asia Pacific Fiberglass Pipes Market - Volume and Forecast To 2028 (Thousand Meters)

- Figure 21. Others: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 22. Asia Pacific Fiberglass Pipes Market Revenue Share, By End Use (2021 and 2028)

- Figure 23. Oil and Gas: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 24. Sewage: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 25. Chemicals: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 26. Agriculture: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 27. Others: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast To 2028 (US$ Million)

- Figure 28. Asia Pacific: Fiberglass Pipes Market Revenue, by Key Country (2021 and 2028)

- Figure 29. Asia Pacific: Fiberglass Pipes Market Revenue Share, by Key Country (2021 and 2028)

- Figure 30. Australia: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- Figure 31. Australia: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- Figure 32. China: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- Figure 33. China: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- Figure 34. India: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- Figure 35. India: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- Figure 36. Japan: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- Figure 37. Japan: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- Figure 38. South Korea: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- Figure 39. South Korea: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- Figure 40. Rest of Asia Pacific: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- Figure 41. Rest of Asia Pacific: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

The Asia Pacific fiberglass pipes market is expected to grow from US$ 1,457.17 million in 2022 to US$ 2,006.83 million by 2028. It is estimated to grow at a CAGR of 5.5% from 2022 to 2028.

Rising Preference Among the End Users for Composite Pipes Over Conventional Pipes Fuels Asia Pacific Fiberglass Pipes Market

Metal, concrete, steel, plastics, and composites are used to produce pipes for several applications ranging from oil & gas transmission and wastewater treatment to chemical pipelines. Material type and size are major factors considered by the end-use industries while selecting pipe for specific applications. Due to their characteristics such as corrosion resistance, nontoxic nature, strong impact resistance, weathering resistance, hydraulic efficiency, long service life, lightweight, and low thermal & electrical conductivity, fiberglass pipes are preferred over conventional concrete, metal, or plastic pipes.

Fiberglass pipe manufacturers and suppliers offer a wide range of products for several corrosive and hazardous applications. Enduro Composites provide fiberglass pipes that meet plant specifications and industry standards. The portfolio comprises fiberglass pipes with properties such as less downtime, high strength, durability, resistance to 1,000 chemicals, and temperature tolerance from -40°F through 300°F. Steel and concrete pipes are susceptible to corrosion and negatively affect the structural integrity of pipes. Burgess Well Company Inc, provides nonconductive, torque resistant, and high-pressure resistant fiberglass pipes. The wide range of fiberglass pipes offered by manufacturers and the rising preference for composite pipes is expected to replace conventional pipes in several applications such as crude oil transmission, and chemicals and water sectors.

Asia Pacific Fiberglass Pipes Market Overview

The fiberglass pipes market in Asia Pacific is segmented into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. This region is a prominent market for fiberglass pipes owing to growth in the chemical and oil & gas sectors and a rise in urbanization, leading to increased demand for sewage systems. Moreover, government initiatives and policies such as Make-in-India encourage the setup of various manufacturing plants in India. The rise in foreign direct investments also leads to regional economic growth, further bolstering industrialization in the region. The chemical manufacturing industry is an important part of manufactured exports for several Asian nations, including China, South Korea, India, and Japan. According to the International Council of Chemical Associations (ICCA), the Asia Pacific chemical industry is the largest contributor to the region's GDP and employment, generating 45% of the industry's total annual economic value and 69% of all jobs supported.

Further, the demand for oil and gas is increasing in Asia Pacific. According to the International Energy Agency, the global oil demand rebounded in 2021, and Asia is expected to account for 77% of oil demand by 2025. Asian oil import requirements are expected to surpass 31 million barrels per day by 2025. All major Asian economies heavily depend on oil imports from the Middle East & Africa. Various countries in the region have initiated projects to cater to the growing demand for oil and gas. For instance, in April 2023, Asia's largest underwater hydro-carbon pipeline, below the river Brahmaputra connecting Jorhat and Majuli in Assam, India, was completed by the Indradhanush Gas Grid Limited (IGGL). Thus, the growing investments in such projects are expected to bolster the fiberglass pipes market during the forecast period.

Asia Pacific Fiberglass Pipes Market Revenue and Forecast to 2028 (US$ Million)

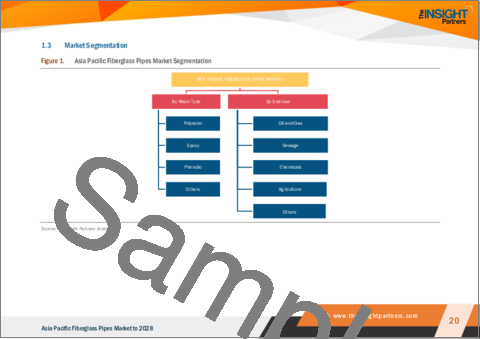

Asia Pacific Fiberglass Pipes Market Segmentation

The Asia Pacific fiberglass pipes market is segmented into resin type, end use, and country.

Based on resin type, the Asia Pacific fiberglass pipes market is segmented into polyester, epoxy, phenolic, and others. The polyester segment held a largest Asia Pacific fiberglass pipes market share in 2022.

Based on end use, the Asia Pacific fiberglass pipes market is segmented into oil and gas, sewage, chemicals, agriculture, and others. The oil and gas segment held the largest Asia Pacific fiberglass pipes market share in 2022.

Based on country, the Asia Pacific fiberglass pipes market has been categorized into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific fiberglass pipes market in 2022.

Amiblu Holding GmbH, Chemical Process Piping Pvt Ltd, EPP Composites Pvt Ltd, Fibrex FRP Piping Systems, Future Pipe Industries LLC, Gruppo Sarplast Srl, Lianyungang Zhongfu Lianzhong Composites Group Co Ltd, NOV Inc, Plasticon Germany GmbH, Poly Plast Chemi Plants (I) Pvt Ltd, Saudi Arabian Amiantit Co, and Sunrise Industries (India) Ltd are some of the leading companies operating in the Asia Pacific fiberglass pipes market.

Table Of Contents

1. Introduction

- 1.1 Study Scope

- 1.2 The Insight Partners Research Report Guidance

- 1.3 Market Segmentation

- 1.3.1 Asia Pacific Fiberglass Pipes Market, by Resin Type

- 1.3.2 Asia Pacific Fiberglass Pipes Market, by End-Use

- 1.3.3 Asia Pacific Fiberglass Pipes Market, by country

2. Key Takeaways

3. Research Methodology

- 3.1 Scope of the Study

- 3.2 Research Methodology

- 3.2.1 Data Collection:

- 3.2.2 Primary Interviews:

- 3.2.3 Hypothesis formulation:

- 3.2.4 Macro-economic factor analysis:

- 3.2.5 Developing base number:

- 3.2.6 Data Triangulation:

- 3.2.7 Country level data:

4. Asia Pacific Fiberglass Pipes Market Landscape

- 4.1 Asia Pacific Fiberglass Pipes Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants:

- 4.2.2 Bargaining Power of Suppliers:

- 4.2.3 Bargaining Power of Buyers:

- 4.2.4 Competitive Rivalry:

- 4.2.5 Threat of Substitutes:

- 4.3 Ecosystem Analysis

- 4.3.1 Overview:

- 4.3.2 Raw Material Suppliers:

- 4.3.3 Manufacturers

- 4.3.4 Distributors/Suppliers

- 4.3.5 End-Use Industries

- 4.4 Expert Opinion

5. Asia Pacific Fiberglass Pipes Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increasing Installation of Oil & Gas Pipelines

- 5.1.2 Rising Demand for Fiberglass Pipes in Chemical Industry

- 5.2 Market Restraints

- 5.2.1 Fluctuation in Prices of Raw Materials

- 5.3 Market Opportunities

- 5.3.1 Adoption of Fiberglass Pipes in Wastewater Systems

- 5.4 Future Trends

- 5.4.1 Rising Preference among the End Users for Composite Pipes over Conventional Pipes

- 5.5 Impact Analysis

6. Fiberglass Pipes - Asia Pacific Market Analysis

- 6.1 Asia Pacific Fiberglass Pipes Market -Volume and Forecast to 2028 (Thousand Meters)

- 6.2 Asia Pacific Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

7. Asia Pacific Fiberglass Pipes Market Analysis - By Resin Type

- 7.1 Overview

- 7.2 Asia Pacific Fiberglass Pipes Market, By Resin Type (2021 and 2028)

- 7.3 Polyester

- 7.3.1 Overview

- 7.3.2 Polyester: Asia Pacific Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 7.3.3 Polyester: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- 7.4 Epoxy

- 7.4.1 Overview

- 7.4.2 Epoxy: Asia Pacific Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 7.4.3 Epoxy: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- 7.5 Phenolic

- 7.5.1 Overview

- 7.5.2 Phenolic: Asia Pacific Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 7.5.3 Phenolic: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: Asia Pacific Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 7.6.3 Others: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

8. Asia Pacific Fiberglass Pipes Market Analysis - By End Use

- 8.1 Overview

- 8.2 Asia Pacific Fiberglass Pipes Market, By End Use (2021 and 2028)

- 8.3 Oil and Gas

- 8.3.1 Overview

- 8.3.2 Oil and Gas: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- 8.4 Sewage

- 8.4.1 Overview

- 8.4.2 Sewage: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- 8.5 Chemicals

- 8.5.1 Overview

- 8.5.2 Chemicals: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- 8.6 Agriculture

- 8.6.1 Overview

- 8.6.2 Agriculture: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

- 8.7 Others

- 8.7.1 Overview

- 8.7.2 Others: Asia Pacific Fiberglass Pipes Market - Revenue and Forecast to 2028 (US$ Million)

9. Asia Pacific Fiberglass Pipes Market - Country Analysis

- 9.1 Asia Pacific: Fiberglass Pipes Market

- 9.1.1 Asia Pacific: Fiberglass Pipes Market, by Key Country

- 9.1.1.1 Australia: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 9.1.1.2 Australia: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- 9.1.1.2.1 Australia: Fiberglass Pipes Market, by Resin Type

- 9.1.1.2.2 Australia: Fiberglass Pipes Market, by Resin Type

- 9.1.1.2.3 Australia: Fiberglass Pipes Market, by End Use

- 9.1.1.3 China: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 9.1.1.4 China: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- 9.1.1.4.1 China: Fiberglass Pipes Market, by Resin Type

- 9.1.1.4.2 China: Fiberglass Pipes Market, by Resin Type

- 9.1.1.4.3 China: Fiberglass Pipes Market, by End Use

- 9.1.1.5 India: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 9.1.1.6 India: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- 9.1.1.6.1 India: Fiberglass Pipes Market, by Resin Type

- 9.1.1.6.2 India: Fiberglass Pipes Market, by Resin Type

- 9.1.1.6.3 India: Fiberglass Pipes Market, by End Use

- 9.1.1.7 Japan: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 9.1.1.8 Japan: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- 9.1.1.8.1 Japan: Fiberglass Pipes Market, by Resin Type

- 9.1.1.8.2 Japan: Fiberglass Pipes Market, by Resin Type

- 9.1.1.8.3 Japan: Fiberglass Pipes Market, by End Use

- 9.1.1.9 South Korea: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 9.1.1.10 South Korea: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- 9.1.1.10.1 South Korea: Fiberglass Pipes Market, by Resin Type

- 9.1.1.10.2 South Korea: Fiberglass Pipes Market, by Resin Type

- 9.1.1.10.3 South Korea: Fiberglass Pipes Market, by End Use

- 9.1.1.11 Rest of Asia Pacific: Fiberglass Pipes Market - Volume and Forecast to 2028 (Thousand Meters)

- 9.1.1.12 Rest of Asia Pacific: Fiberglass Pipes Market -Revenue and Forecast to 2028 (US$ Million)

- 9.1.1.12.1 Rest of Asia Pacific: Fiberglass Pipes Market, by Resin Type

- 9.1.1.12.2 Rest of Asia Pacific: Fiberglass Pipes Market, by Resin Type

- 9.1.1.12.3 Rest of Asia Pacific: Fiberglass Pipes Market, by End Use

- 9.1.1 Asia Pacific: Fiberglass Pipes Market, by Key Country

10. Company Profiles

- 10.1 Amiblu Holding GmbH

- 10.1.1 Key Facts

- 10.1.2 Business Description

- 10.1.3 Products and Services

- 10.1.4 Financial Overview

- 10.1.5 SWOT Analysis

- 10.1.6 Key Developments

- 10.2 Chemical Process Piping Pvt Ltd

- 10.2.1 Key Facts

- 10.2.2 Business Description

- 10.2.3 Products and Services

- 10.2.4 Financial Overview

- 10.2.5 SWOT Analysis

- 10.2.6 Key Developments

- 10.3 EPP Composites Pvt Ltd

- 10.3.1 Key Facts

- 10.3.2 Business Description

- 10.3.3 Products and Services

- 10.3.4 Financial Overview

- 10.3.5 SWOT Analysis

- 10.3.6 Key Developments

- 10.4 Fibrex FRP Piping Systems

- 10.4.1 Key Facts

- 10.4.2 Business Description

- 10.4.3 Products and Services

- 10.4.4 Financial Overview

- 10.4.5 SWOT Analysis

- 10.4.6 Key Developments

- 10.5 Future Pipe Industries LLC

- 10.5.1 Key Facts

- 10.5.2 Business Description

- 10.5.3 Products and Services

- 10.5.4 Financial Overview

- 10.5.5 SWOT Analysis

- 10.5.6 Key Developments

- 10.6 Gruppo Sarplast Srl

- 10.6.1 Key Facts

- 10.6.2 Business Description

- 10.6.3 Products and Services

- 10.6.4 Financial Overview

- 10.6.5 SWOT Analysis

- 10.6.6 Key Developments

- 10.7 Lianyungang Zhongfu Lianzhong Composites Group Co Ltd

- 10.7.1 Key Facts

- 10.7.2 Business Description

- 10.7.3 Products and Services

- 10.7.4 Financial Overview

- 10.7.5 SWOT Analysis

- 10.7.6 Key Developments

- 10.8 NOV Inc

- 10.8.1 Key Facts

- 10.8.2 Business Description

- 10.8.3 Products and Services

- 10.8.4 Financial Overview

- 10.8.5 SWOT Analysis

- 10.8.6 Key Developments

- 10.9 Saudi Arabian Amiantit Co

- 10.9.1 Key Facts

- 10.9.2 Business Description

- 10.9.3 Products and Services

- 10.9.4 Financial Overview

- 10.9.5 SWOT Analysis

- 10.9.6 Key Developments

- 10.10 Sunrise Industries (India) Ltd

- 10.10.1 Key Facts

- 10.10.2 Business Description

- 10.10.3 Products and Services

- 10.10.4 Financial Overview

- 10.10.5 SWOT Analysis

- 10.10.6 Key Developments

- 10.11 Poly Plast Chemi Plants (I) Pvt Ltd

- 10.11.1 Key Facts

- 10.11.2 Business Description

- 10.11.3 Products and Services

- 10.11.4 Financial Overview

- 10.11.5 SWOT Analysis

- 10.11.6 Key Developments

- 10.12 Plasticon Germany GmbH

- 10.12.1 Key Facts

- 10.12.2 Business Description

- 10.12.3 Products and Services

- 10.12.4 Financial Overview

- 10.12.5 SWOT Analysis

- 10.12.6 Key Developments

11. Appendix

- 11.1 About The Insight Partners

- 11.2 Glossary of Terms