|

|

市場調査レポート

商品コード

1408669

米国の診療管理システム市場:規模と予測、世界・地域別シェア、動向、成長機会分析 - 製品別、コンポーネント別、提供形態別、用途別、エンドユーザー別、国別US Practice Management Systems Market Size and Forecasts, Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Product, Component, Delivery Mode, Application, and End User and Country |

||||||

|

|

|||||||

|

|||||||

| 米国の診療管理システム市場:規模と予測、世界・地域別シェア、動向、成長機会分析 - 製品別、コンポーネント別、提供形態別、用途別、エンドユーザー別、国別 |

|

出版日: 2023年11月17日

発行: The Insight Partners

ページ情報: 英文 116 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

米国の診療管理システム市場規模は、2022年の69億3,600万米ドルから2030年には132億6,700万米ドルに成長すると予測され、2022年から2030年までのCAGRは8.4%と推定されます。

スマートフォンの急速な普及が米国の診療管理システム市場の成長機会をもたらす

ヘルスケア専門家や患者の間でスマートフォンの利用が急増しており、診療管理システム市場に大きなビジネスチャンスがもたらされると期待されています。スマートフォンは、通信やリアルタイムの位置追跡において最もダイナミックでユビキタスな動向の1つです。これらのデバイスはまた、ヘルスケア情報や健康データの収集、患者へのサービス提供のプロセスを簡素化することで、ヘルスケアの実践をより利用しやすく、管理しやすくすることにも貢献しています。スマートフォンの普及に伴い、ヘルスケアプロバイダーは診療管理プロセスを合理化し、患者エンゲージメントを向上させる方法を模索しています。モバイルフレンドリーで、スマートフォンのアプリを通じて予約スケジューリングや請求、患者とのコミュニケーションなどの機能を提供する診療管理システムは、高い需要が見込まれます。さらに、スマートフォンを利用することで、ヘルスケアプロバイダーは患者の記録にアクセスしたり、診療を遠隔で管理したりすることも可能になり、効率性と柔軟性の向上につながります。その結果、診療管理システム市場は今後数年間で大幅な成長が見込まれます。スマートフォンは、電子メールやインターネット閲覧といった定評のある用途に加え、患者やスタッフ、医療機器を追跡・監視するリアルタイムロケーションシステム(RTLS)ソリューションにも利用されています。多種多様なスマートフォンアプリケーション(アプリ)に簡単にアクセスできるため、人々はモバイルヘルスアプリを利用して慢性症状を管理し、健康に関する行動を変えることができます。

製品に基づく洞察

米国の診療管理システム市場は、製品別に統合型診療管理システムとスタンドアロン型診療管理システムに二分されます。2022年の市場シェアは、スタンドアロン型診療管理システム分野が大きいです。2022年から2030年にかけて、より高いCAGRが見込まれます。スタンドアロン型システムは1つのモジュールで構成され、ヘルスケア現場の特定のニーズに対応するように設計されています。このシステムは1つのプロセスのみを扱うため、設置コストやメンテナンスコストは統合システムよりも低いです。さらに、新興国における特定のニーズやコストへの懸念を考慮し、スタンドアロンシステムで提供される医師設定オプションの範囲が拡大していることも、スタンドアロン診療管理システムの採用を後押ししています。

コンポーネンに基づく洞察

コンポーネントに基づき、米国の診療管理システム市場はソフトウェアとサービスに区分されます。2022年の市場シェアは、ソフトウェア分野が大きいです。サービス分野は、2022年から2030年にかけてより高いCAGRを記録すると予測されています。診療管理ソフトウェアは、予約スケジューリング、個人管理、患者管理、コーディングと請求、カルテ管理などの臨床業務の実行に使用されます。現在、ヘルスケア部門は、価値ベースのケアと充実したサービスを患者に提供することに注力しています。その結果、ヘルスケアプロバイダーは、患者の不満、医療費請求のエラー、追加人件費を避けるために、効果的な診療管理のためにリソースを割り当てており、これが米国での診療管理ソフトウェアの採用を後押ししています。また、インテリジェントなアルゴリズムを使用することで、医師は情報に基づいた意思決定を行うことができます。市場で入手可能な診療管理ソフトウェア・ソリューションの中には、患者データ、待ち時間、患者の来院状況、支払先の分析などをリアルタイムで分析できるものもあります。さらに、手作業の削減と人的資源の最適化に重点を置くことで、診療管理ソフトウェア市場の成長は続くと思われます。

提供形態に基づく洞察

米国の診療管理システム市場は、提供形態によって、ウェブベースの診療管理システム、クラウドベースの診療管理システム、オンプレミスの診療管理システムに分類されます。2022年の市場シェアは、オンプレミス型診療管理システム分野が大きいです。病院やその他の医療機関は、ポイントオブケアシステムを導入しながら、患者のデータを記録・保存するためにオンプレミス型診療管理システムを使用しています。これらのソリューションは、施設内のコンピュータにインストールされ運用されます。オンプレミスの提供形態は、あらゆるタイプのヘルスケア診療所にとって、(長期的には)コスト効率が高く、持ち運び可能なソリューションを提供します。さらに、企業病院チェーンのネットワーク拡大により、オンプレミス型診療管理システムの需要が高まっています。

用途に基づく洞察

米国の診療管理システム市場は、用途別に患者記録追跡、管理業務、保険請求処理、コーディング&請求、その他に分類されます。2022年には、管理業務分野が最大の市場シェアを占めました。管理業務は日常業務の効率化に役立つため、ヘルスケア分野では極めて重要です。これらの業務には、予約スケジューリング、患者登録、保険確認、請求書発行、電子カルテ管理などが含まれます。診療管理システムを導入することで、ヘルスケアプロバイダーはこれらの管理業務を自動化し、ヒューマンエラーの可能性を減らし、全体的な効率を向上させることができます。これにより、スタッフは事務処理に追われることなく、患者ケアに集中できるようになり、最終的には医療現場における健康状態の改善と生産性の向上につながります。さらに、診療管理システムは、貴重なデータ分析とレポート機能を提供することができます。

エンドユーザーに基づく洞察

米国の診療管理システム市場は、エンドユーザー別に病院・診療所、医院・研究所、保険会社、その他に分類されます。2022年の収益シェアでは、病院・診療所セグメントが市場を独占しています。このセグメントの市場は、2022年から2030年にかけて最も高いCAGRで成長すると予測されています。病院・診療所特有のニーズに合わせた診療管理システムは、予約スケジューリング、患者登録、リソース割り当てから請求・クレーム処理に至るまで、幅広い管理業務を効率化する上で極めて重要な役割を果たします。診療管理システムの導入により、これらの施設では、診療科や専門分野にまたがる患者ケアのシームレスな調整が可能になります。これらのシステムは、スケジューリング、リソース管理、患者データへのアクセスの一元化を支援し、効率的な患者の流れ、待ち時間の短縮、ケアコーディネーションの改善を可能にします。さらに、統合された請求およびクレーム管理機能は、正確な償還プロセス、収益サイクル管理、および規制コンプライアンスをサポートし、病院や診療所が質の高いケアを提供しながら財務パフォーマンスを最適化できるようにします。管理ワークフローを合理化することで、これらのシステムは臨床医が患者ケアにより集中できるようにします。

米国の診療管理システム市場に関する報告書を作成する際に参照した主な一次情報および二次情報には、米国疾病管理予防センター、国際糖尿病連合、変形性関節症(OA)行動同盟などがあります。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 診療管理システム市場 - 主要産業力学

- 主な市場促進要因

- 医療機関に対するコスト削減と質の高いサービス提供への圧力の高まり

- 慢性疾患の増加

- 主な市場抑制要因

- データプライバシーに関する懸念

- 主な市場機会

- スマートフォンの急速な普及

- 主な将来動向

- 遠隔モニタリングによる定期的な病院訪問の不要化

- インパクト分析

第5章 診療管理システム市場:市場分析

- 診療管理システム市場の収益(2022年~2030年)

第6章 診療管理システム市場:収益と2030年までの予測 - 製品タイプ別

- 収益シェア(2022年・2030年)- 製品タイプ別

- 統合型診療管理システム

- スタンドアロン型診療管理システム

第7章 診療管理システム市場:2030年までの収益と予測 - コンポーネント別

- 収益シェア(2022年・2030年)- 製品タイプ別

- ソフトウェア

- サービス

第8章 診療管理システム市場:収益と2030年までの予測 - 提供形態別

- 収益シェア(2022年・2030年)- 提供形態別

- ウェブベース

- クラウドベース

- オンプレミス

第9章 診療管理システム市場:収益と2030年までの予測 - 用途別

- 収益シェア(2022年・2030年)- 用途別

- 患者記録の追跡

- 管理業務

- 保険請求処理

- コーディングと請求

- その他

第10章 診療管理システム市場:収益と2030年までの予測 - エンドユーザー別

- 収益シェア(2022年・2030年)- エンドユーザー別

- 病院および診療所

- 医院および研究所

- 保険会社

- その他

第11章 診療管理システム市場:業界情勢

- 診療管理システム市場における成長戦略

- 無機的成長戦略

- 有機的成長戦略

第12章 企業プロファイル

- WRS Health

- PracticeEHR

- AdvancedMD Inc

- Azalea Health Innovations Inc

- DrChrono Inc

- PracticeSuite Inc

- Meditab Software Inc

- Microwize Technology Inc

- MedicalMine Inc

- Henry Schein Medical Systems Inc

- MEDENT

第13章 付録

List Of Tables

- Table 1. Practice Management Systems Market Segmentation

- Table 2. Recent Inorganic Growth Strategies in the Practice Management Systems Market

- Table 3. Recent Organic Growth Strategies in the Practice Management Systems Market

- Table 4. Glossary of Terms, US Practice Management Systems Market

List Of Figures

- Figure 1. Practice Management Systems Market Segmentation, By Geography

- Figure 2. Practice Management Systems Market - Key Industry Dynamics

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Practice Management Systems Market Revenue (US$ Mn), 2022 - 2030

- Figure 5. Practice Management Systems Market Revenue, Geography (US$ Mn), 2022 - 2030

- Figure 6. Practice Management Systems Market Revenue Share, by Product, 2022 & 2030 (%)

- Figure 7. Integrated Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Standalone Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Practice Management Systems Market Revenue Share, by Component 2022 & 2030 (%)

- Figure 10. Software: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Services: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Practice Management Systems Market Revenue Share, by Delivery Mode, 2022 & 2030 (%)

- Figure 13. Web-Based Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Cloud-Based Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. On-Premise Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 16. Practice Management Systems Market Revenue Share, by Application, 2022 & 2030 (%)

- Figure 17. Patient Record Tracking: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 18. Administrative Tasks: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 19. Processing Insurance Claims: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 20. Coding & Billing: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 21. Others: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 22. Practice Management Systems Market Revenue Share, by End Users, 2022 & 2030 (%)

- Figure 23. Hospitals and Clinics: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 24. Physicians Office and Labs: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 25. Insurance Companies: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 26. Others: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- Figure 27. Growth Strategies in the Practice Management Systems Market

The US practice management systems market size is expected to grow from US$ 6.936 billion in 2022 to US$ 13.267 billion by 2030; it is estimated to register a CAGR of 8.4% from 2022 to 2030.

Burgeoning Use of Smartphones Will Provide Opportunity for Growth of US Practice Management System Market

The burgeoning use of smartphones among healthcare professionals and patients is expected to provide significant opportunities for the practice management systems market. A smartphone is one of the most dynamic and ubiquitous trends in communications and real-time location tracking. These devices also contribute to making healthcare practices more accessible and manageable by simplifying the process of collecting healthcare information or health data and offering services to patients. With the increasing adoption of smartphones, healthcare providers are looking for ways to streamline their practice management processes and improve patient engagement. Practice management systems that are mobile-friendly and offer features such as appointment scheduling, billing, and patient communication through smartphone apps are likely to be in high demand. Additionally, the use of smartphones can also enable healthcare providers to access patient records and manage their practice remotely, leading to greater efficiency and flexibility. As a result, the practice management systems market is expected to experience substantial growth in the coming years. In addition to their well-established applications such as e-mail and Internet browsing, smartphones are used in real-time location system (RTLS) solutions for tracking and monitoring patients, staff, and medical equipment. With easy access to a wide variety of smartphone applications (apps), people can use mobile health apps to manage chronic conditions and change health-related behaviors.

Product-Based Insights

Based on the product, the US practice management systems market is bifurcated into integrated practice management systems and standalone practice management systems. The standalone practice management systems segment held a larger market share in 2022. A higher CAGR is anticipated to register from 2022 to 2030. Standalone systems comprise only one module and are designed to address specific needs of healthcare settings. As the system deals with only one process, its installation and maintenance costs are lower than those of integrated systems. Additionally, an expanding range of physician setting options provided in standalone systems, considering specific needs and cost concerns in emerging nations, propel the adoption of standalone practice management systems.

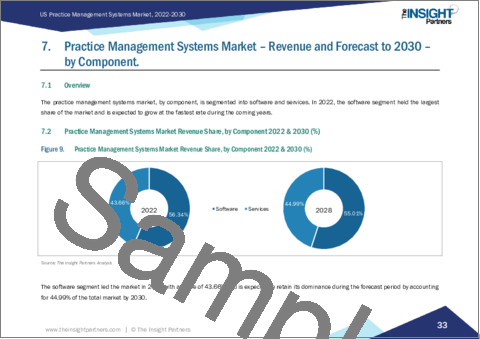

Component-Based Insights

Based on components, the US practice management systems market is segmented into software and services. The software segment held a larger market share in 2022. The services segment is anticipated to register a higher CAGR during 2022-2030. Practice management software is used for performing clinical operations such as appointment scheduling, personal management, patient management, coding and billing, and medical record management. Currently, the healthcare sector is focused on offering value-based care and enhanced services to patients. As a result, healthcare providers allocate their resources for effective practice management to avoid dissatisfaction among patients, errors in medical billing, and additional labor charges, which drives the adoption of medical practice management software in the US. The use of intelligent algorithms also allows physicians to make informed decisions. Some of the practice management software solutions available in the market provide real-time analysis of patient data, waiting time, patient visits, and analysis of payers. Additionally, emphasis on the reduction of manual work and optimization of human resources would continue the growth of the market for practice management software.

Delivery Mode-Based Insights

In terms of Delivery Mode, the US practice management systems market is categorized into web-based practice management systems, cloud-based practice management systems, and on-premise practice management systems. The on-premise practice management systems segment held a larger market share in 2022. Hospitals or other healthcare entities use on-premise practice management systems to record and store the patient's data while implementing a point-of-care system. These solutions are installed and operated on computers within the premises of facilities. An on-premise delivery mode offers a cost-efficient (in the long term) and portable solution for all types of healthcare practices. Additionally, the expanding networks of corporate hospital chains generate a high demand for on-premises practice management systems.

Application-Based Insights

The US practice management systems market, by application, is categorized into patient record tracking, administrative tasks, processing insurance claims, coding & billing, and others. The administrative tasks segment accounted for the largest market share in 2022. Administrative tasks are crucial in the healthcare sector as they help streamline day-to-day operations. These tasks include appointment scheduling, patient registration, insurance verification, billing and invoicing, and managing electronic health records. By implementing a practice management system, healthcare providers can automate these administrative tasks, reducing the likelihood of human error and improving overall efficiency. This allows staff to focus more on patient care and less on paperwork, ultimately leading to better health outcomes and increased productivity within medical practices. Additionally, practice management systems can provide valuable data analytics and reporting capabilities.

End User-Based Insights

Based on end users, the US practice management systems market is categorized into hospitals and clinics, physician's offices and labs, insurance companies, and others. The hospitals and clinics segment dominated the market in terms of revenue share in 2022. The market for this segment is anticipated to grow at the highest CAGR from 2022 to 2030. Practice management systems tailored to the specific needs of hospitals and clinics play a pivotal role in streamlining a wide range of administrative tasks, from appointment scheduling, patient registration, and resource allocation to billing and claims processing. The implementation of practice management systems confers the seamless coordination of patient care across departments and specialties in these facilities. These systems aid in centralized scheduling, resource management, and patient data accessibility, allowing for efficient patient flow, reduced wait times, and improved care coordination. Additionally, integrated billing and claims management functionalities support accurate reimbursement processes, revenue cycle management, and regulatory compliance, empowering hospitals and clinics to optimize financial performance while delivering high-quality care. By streamlining administrative workflows, these systems allow clinicians to focus more on patient care.

A few of the major primary and secondary sources referred to while preparing the report on the US practice management system market are the Centers for Disease Control and Prevention, the International Diabetes Federation, and the Osteoarthritis (OA) Action Alliance.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players and segments in the US practice management system market.

- Highlights key business priorities in order to assist companies to realign their business strategies.

- The key findings and recommendations highlight crucial progressive industry trends in the US practice management system market, thereby allowing players across the value chain to develop effective long-term strategies.

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

- Scrutinize in-depth market trends and outlook coupled with the factors driving the US practice management system market, as well as those hindering it.

- Enhance the decision-making process by understanding the strategies that underpin security interest with respect to client products, segmentation, pricing and distribution.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Practice Management Systems Market - Key Industry Dynamics

- 4.1 Key Market Drivers

- 4.1.1 Rising Pressure on Healthcare Institutions to Provide High-Quality Services at Reduced Costs

- 4.1.2 Rising Prevalence of Chronic Diseases

- 4.2 Key Market Restraints

- 4.2.1 Concerns Regarding Data Privacy

- 4.3 Key Market Opportunities

- 4.3.1 Burgeoning Use of Smartphones

- 4.4 Key Future Trends

- 4.4.1 Remote Monitoring Eliminating Need for Routine Visits to Hospitals

- 4.5 Impact Analysis:

5. Practice Management Systems Market - Market Analysis

- 5.1 Practice Management Systems Market Revenue (US$ Mn), 2022 - 2030

6. Practice Management Systems Market - Revenue and Forecast to 2030 - by Product Type

- 6.1 Overview

- 6.2 Practice Management Systems Market Revenue Share, by Product, 2022 & 2030 (%)

- 6.3 Integrated Practice Management Systems

- 6.3.1 Overview

- 6.3.2 Integrated Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- 6.4 Standalone Practice Management Systems

- 6.4.1 Overview

- 6.4.2 Standalone Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

7. Practice Management Systems Market - Revenue and Forecast to 2030 - by Component.

- 7.1 Overview

- 7.2 Practice Management Systems Market Revenue Share, by Component 2022 & 2030 (%)

- 7.3 Software

- 7.3.1 Overview

- 7.3.2 Software: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 Services

- 7.4.1 Overview

- 7.4.2 Services: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

8. Practice Management Systems Market - Revenue and Forecast to 2030 - by Delivery Mode

- 8.1 Overview

- 8.2 Practice Management Systems Market Revenue Share, by Delivery Mode, 2022 & 2030 (%)

- 8.3 Web-Based Practice Management Systems

- 8.3.1 Overview

- 8.3.2 Web-Based Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Cloud-Based Practice Management Systems

- 8.4.1 Overview

- 8.4.2 Cloud-Based Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 On-Premise Practice Management Systems

- 8.5.1 Overview

- 8.5.2 On-Premise Practice Management Systems: Practice Management Systems Market - Revenue and Forecast to 2030 (US$ Million)

9. Practice Management Systems Market - Revenue and Forecast to 2030 - by Application

- 9.1 Overview

- 9.2 Practice Management Systems Market Revenue Share, by Application, 2022 & 2030 (%)

- 9.3 Patient Record Tracking

- 9.3.1 Overview

- 9.3.2 Patient Record Tracking: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- 9.4 Administrative Tasks

- 9.4.1 Overview

- 9.4.2 Administrative Tasks: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- 9.5 Processing Insurance Claims

- 9.5.1 Overview

- 9.5.2 Processing Insurance Claims: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- 9.6 Coding & Billing

- 9.6.1 Overview

- 9.6.2 Coding & Billing: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- 9.7 Others

- 9.7.1 Overview

- 9.7.2 Others: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

10. Practice Management Systems Market - Revenue and Forecast to 2030 - by End Users

- 10.1 Overview

- 10.2 Practice Management Systems Market Revenue Share, by End Users, 2022 & 2030 (%)

- 10.3 Hospitals and Clinics

- 10.3.1 Overview

- 10.3.2 Hospitals and Clinics: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- 10.4 Physicians Office and Labs

- 10.4.1 Overview

- 10.4.2 Physicians Office and Labs: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- 10.5 Insurance Companies

- 10.5.1 Overview

- 10.5.2 Insurance Companies: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

- 10.6 Others

- 10.6.1 Overview

- 10.6.2 Others: Practice Management Systems Market - Revenue and Forecast to 2030(US$ Million)

11. Practice Management Systems Market-Industry Landscape

- 11.1 Overview

- 11.2 Growth Strategies in the Practice Management Systems Market

- 11.3 Inorganic Growth Strategies

- 11.3.1 Overview

- 11.4 Organic Growth Strategies

- 11.4.1 Overview

12. Company Profiles

- 12.1 WRS Health

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 PracticeEHR

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 AdvancedMD Inc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Azalea Health Innovations Inc

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 DrChrono Inc

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 PracticeSuite Inc

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Meditab Software Inc

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Microwize Technology Inc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 MedicalMine Inc

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Henry Schein Medical Systems Inc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

- 12.11 MEDENT

- 12.11.1 Key Facts

- 12.11.2 Business Description

- 12.11.3 Products and Services

- 12.11.4 Financial Overview

- 12.11.5 SWOT Analysis

- 12.11.6 Key Developments

13. Appendix

- 13.1 About Us

- 13.2 Glossary of Terms