|

|

市場調査レポート

商品コード

1402490

北米の免疫診断市場の2030年までの予測:地域別分析- 製品別、適応症別、エンドユーザー別North America Immunodiagnostics Market Forecast to 2030 - Regional Analysis - by Product (Enzyme-Linked Immunosorbent Assays, Chemiluminescence Immunoassays, Radioimmunoassays, and Others), By Clinical Indication, and End User |

||||||

|

|

|||||||

|

|||||||

| 北米の免疫診断市場の2030年までの予測:地域別分析- 製品別、適応症別、エンドユーザー別 |

|

出版日: 2023年10月27日

発行: The Insight Partners

ページ情報: 英文 200 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

北米の免疫診断市場は、2023年の104億6,348万米ドルから2030年には173億9,910万米ドルに成長すると予測されています。2023年から2030年までのCAGRは7.5%と推定されます。

ポイントオブケア免疫診断の利用拡大が北米産業用ロボット市場を牽引

ポイントオブケア検査(POCT)は、正確で迅速な治療法を決定するために迅速な診断結果が必要とされるため、患者中心のヘルスケアに不可欠となっています。集中型のポイント・オブ・ケア検査から分散型の検査へのシフトにより、これらの診断へのアクセスが容易になっています。免疫測定検査は、慢性疾患のモニタリングや、細菌やウイルスなどの病原体の検出に役立ちます。先進的なポイントオブケア機器は、1つのサンプルから最大3成分の迅速なスクリーニングを可能にします。また、モバイルヘルスケア(mH)スマートデバイスに傾倒するPOCD(ポイント・オブ・ケア診断)は、個別化されたヘルスケアのモニタリングと管理に革命をもたらし、次世代POCTへの道を開く可能性があります。感染症の管理は、特にタイムリーな医療へのアクセスが困難で、ヘルスケア・インフラが時代遅れでまばらな発展途上国において、POCTによって大幅に改善される可能性があります。さらに、技術的に開発された診断キットは、手作業によるミスを減らすことにつながり、免疫診断市場を促進します。複数の市場プレーヤーが革新的な免疫診断製品を開発しています。例えば、サーモフィッシャーサイエンティフィックは、酵素結合免疫測定法(ELISA)試薬や緩衝液、抗体や検出プローブ、連結機構、ブロッキング緩衝液や洗浄剤、検出基質、捕捉表面などの免疫診断学製品や、バイオコンジュゲーションや検出などのサービスを開発しています。さらに、2020年9月、ロシュはSARS-CoV-2 Rapid Antigen Testを発売しました。この検査はPOC設定で使用され、ヘルスケア専門家がウイルス保有の疑いがある人の感染を15分以内に特定するのに役立ちます。

2021年4月、DiaSorin社は新しい免疫診断POCリーダーであるLIAISON IQと、Lumos Diagnostics社と共同開発したCEマーク取得国向けのLIAISON QuickDetect COVID TrimericS Abテストを発表しました。LIAISON IQ用のこの検査は、ヒト毛細血管のフィンガースティックを用いて、SARS-CoV-2スパイク蛋白に対する特異的IgG抗体を10分で同定します。

2021年4月、Chembio Diagnostics, Inc.は、FDA緊急時使用認可を取得し、従来の検査環境および分散型検査環境で使用できるライセンシングされた迅速ポイントオブケアCOVID-19/Flu A&B検査を発売しました。この迅速イムノアッセイ検査は機器を必要とせず、15分で結果が得られます。

WHOは、COVID-19の危機の中で、検査キット開発者が革新的な取り組みを行い、大衆の要求に応えたことを称賛しました。米国臨床病理学会によると、2020年3月、Cepheid Xpert Xpress SARS-CoV-2検査は、米国食品医薬品局(FDA)から緊急使用許可(EUA)を受けた最初のPOC COVID-19検出アッセイとなった。

同様に、がん治療における免疫診断の使用も増加しています。オンコロジーにおいて、免疫診断学検査は、既知の腫瘍関連抗原または抗体を検出することにより、固形腫瘍の存在を確認することができます。このような利点と適応症が免疫診断市場を牽引しています。

北米の免疫診断市場の概要

北米ではがんの罹患率が急速に増加しており、がん診断の需要が高まっています。米国がん協会(ASC)の2023年がん統計推計によると、米国では190万人近くのがん患者が新たに登録されました。さらに、2023年には609,360人ががんで死亡すると予測されており、これは1日あたり1,670人の死亡に相当します。しかし、診断技術の向上により、がんに関連した死亡者数は減少しています。ASCによると、過去28年間で、男女のがんによる死亡率は1991年のピークから2019年まで32%減少しました。死亡率の低下は、早期かつ高度ながん診断のためであることが判明しました。診断技術の進歩に対する人々の意識が高まった。そのため、米国におけるイムノアッセイ市場は大きく成長しています。同様に、米国では老年人口に糖尿病が高い割合で蔓延しています。多くの企業が糖尿病用のイムノアッセイキットを提供しています。例えば、Bio-Rad Laboratories, Inc.はBio-Plex Proヒト糖尿病イムノアッセイを提供しており、ヒトの糖尿病や肥満マーカーの研究に信頼性が高く便利です。これらは糖尿病患者の糖尿病の管理と治療に役立ちます。米国市民の糖尿病有病率の上昇により、同市場は大きな成長が見込まれています。米国疾病予防管理センター(CDC)が2023年全国糖尿病統計報告書で発表したデータによると、米国では3,730万人が糖尿病を患っており、これは米国総人口の11.3%を占める。また、18歳以上の9,600万人が糖尿病予備軍であり、米国人口の38%を占めるとしています。このように、同国における糖尿病の有病率を考慮すると、免疫診断に対する需要の増加が予想され、市場の成長につながります。近年、革新的で改良された医療技術がかつてない成長を遂げています。その結果、先進的な診断法やヘルスケア産業全体が発展しています。さらに米国では、ポイントオブケア診断のための最先端製品を開発するさまざまな企業が存在し、免疫診断市場の成長に道を開いています。2020年4月、Bio-Rad Laboratories社はSARS-CoV-2に対する抗体を同定する血液ベースの免疫測定キットを発売しました。

北米の免疫診断市場の収益と2030年までの予測(金額)

北米の免疫診断市場のセグメンテーション

北米の免疫診断市場は、製品、臨床適応症、エンドユーザー、国に区分されます。

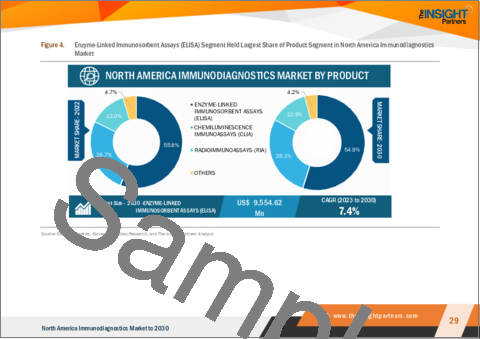

製品別に見ると、北米の免疫診断市場は酵素結合免疫吸着測定法(ELISA)、化学発光免疫測定法(CLIA)、ラジオイムノアッセイ(RIA)、その他に区分されます。2023年には、酵素結合免疫吸着測定法(ELISA)セグメントが北米の免疫診断市場で最大のシェアを記録しました。化学発光免疫測定法(CLIA)セグメントはさらに、ビタミンDアッセイ市場、HIV検出市場、HIV ag/abコンボアッセイ市場、その他の検査に区分されます。

臨床適応に基づき、北米の免疫診断市場は感染症、肝炎+HIV、内分泌、消化器、代謝、その他に区分されます。2023年、感染症セグメントは北米の免疫診断市場で最大のシェアを記録しました。感染症セグメントはさらに、COVID-19、結核、ライム、感染管理、ジカ熱、トレポネーマ、トーチ、麻疹・おたふくかぜ、VZV、EBVに区分されます。内分泌分野はさらに、高血圧、成長、糖尿病、甲状腺、生殖内分泌に区分されます。

エンドユーザー別に見ると、北米の免疫診断市場は病院、診療所、診断研究所、学術・研究機関、その他に区分されます。2023年、北米の免疫診断市場は病院セグメントが最大シェアを記録しました。

国別では、北米市場セグメンテーションは米国、カナダ、メキシコに区分されます。2023年、米国は北米の免疫診断市場で最大のシェアを記録しました。

Abbott Laboratories;bioMerieux SA;Danaher Corp;DiaSorin SpA;F. Hoffmann-La Roche Ltd;PerkinElmer Inc;Shenzhen Mindray Bio-Medical Electronics Co., Ltd;Siemens Healthcare GmbH;Svar Life Science AB;and Thermo Fisher Scientific Inc.は、北米の免疫診断市場に参入している大手企業です。

目次

第1章 イントロダクション

第2章 北米の免疫診断市場-要点

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米の免疫診断市場:市場情勢

- 北米のPEST分析

- 専門家の見解

第5章 北米の免疫診断市場:主要市場力学

- 市場促進要因

- 感染症罹患率の増加

- ポイントオブケア免疫診断の利用拡大

- 市場抑制要因

- 不十分な償還シナリオ

- 市場機会

- 主要企業による研究開発投資と事業拡大への注目の高まり

- 今後の動向

- 免疫診断における技術の進歩

- 影響分析

第6章 免疫診断市場:北米分析

- 北米の免疫診断市場の収益予測と分析

第7章 北米の免疫診断市場分析:製品別

- 酵素結合免疫吸着測定法(ELISA)

- 化学発光免疫測定法(CLIA)

- ラジオイムノアッセイ(RIA)

- その他

第8章 北米の免疫診断市場分析:臨床適応症別

- 感染症

- COVID-19

- 結核

- ライム

- 感染症管理

- ジカ熱

- トレポネーマ

- トーチ

- 麻疹および流行性耳下腺炎

- VZV

- EBV

- 肝炎+HIV

- 消化器

- 代謝疾患

- 内分泌学

- 高血圧

- 成長

- 糖尿病

- 糖尿病

- 甲状腺

- 内分泌学

- 生殖内分泌学

- 内分泌学

- その他

- その他

第9章 北米の免疫診断市場分析:エンドユーザー別

- 病院

- 病院

- 診療所

- 診断研究所

- 研究機関

- 学術・研究機関

- その他

第10章 北米の免疫診断市場 - 2030年までの収益と予測:国別分析

第11章 北米の免疫診断市場:業界情勢

- 無機的成長戦略

- 有機的成長戦略

第12章 企業プロファイル

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd

- DiaSorin SpA

- Danaher Corp

- Thermo Fisher Scientific Inc

- PerkinElmer Inc

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- bioMerieux SA

- Svar Life Science AB

- Siemens Healthcare GmbH

第13章 付録

List Of Tables

- Table 1. US Immunodiagnostics Market, by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 2. US Immunodiagnostics Market, by Chemiluminescence Immunoassays (CLIA)- Revenue and Forecast to 2030 (US$ Million)

- Table 3. US Immunodiagnostics Market, by Clinical Indication - Revenue and Forecast to 2030 (US$ Million)

- Table 4. US Immunodiagnostics Market, by Infectious Diseases - Revenue and Forecast to 2030 (US$ Million)

- Table 5. US Immunodiagnostics Market, by Endocrinology - Revenue and Forecast to 2030 (US$ Million)

- Table 6. US Immunodiagnostics Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 7. Canada Immunodiagnostics Market, by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 8. Canada Immunodiagnostics Market, by Chemiluminescence Immunoassays (CLIA)- Revenue and Forecast to 2030 (US$ Million)

- Table 9. Canada Immunodiagnostics Market, by Clinical Indication - Revenue and Forecast to 2030 (US$ Million)

- Table 10. Canada: Immunodiagnostics Market, by Infectious Diseases - Revenue and Forecast to 2030 (US$ Million)

- Table 11. Canada Immunodiagnostics Market, by Endocrinology - Revenue and Forecast to 2030 (US$ Million)

- Table 12. Canada Immunodiagnostics Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 13. Mexico Immunodiagnostics Market, by Product - Revenue and Forecast to 2030 (US$ Million)

- Table 14. Mexico Immunodiagnostics Market, by Chemiluminescence Immunoassays (CLIA)- Revenue and Forecast to 2030 (US$ Million)

- Table 15. Mexico Immunodiagnostics Market, by Clinical Indication - Revenue and Forecast to 2030 (US$ Million)

- Table 16. Mexico: Immunodiagnostics Market, by Infectious Diseases - Revenue and Forecast to 2030 (US$ Million)

- Table 17. Mexico Immunodiagnostics Market, by Endocrinology - Revenue and Forecast to 2030 (US$ Million)

- Table 18. Mexico Immunodiagnostics Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 19. Recent Inorganic Growth Strategies in the Immunodiagnostics Market

- Table 20. Recent Organic Growth Strategies in the Immunodiagnostics Market

- Table 21. Glossary of Terms, North America Immunodiagnostics Market

List Of Figures

- Figure 1. North America Immunodiagnostics Market Segmentation

- Figure 2. North America Immunodiagnostics Market, by Country

- Figure 3. North America Immunodiagnostics Market Overview

- Figure 4. Enzyme-Linked Immunosorbent Assays (ELISA) Segment Held Largest Share of Product Segment in North America Immunodiagnostics Market

- Figure 5. Canada Expected to Show Remarkable Growth During Forecast Period

- Figure 6. North America: PEST Analysis

- Figure 7. Experts' Opinion

- Figure 8. North America Immunodiagnostics Market: Impact Analysis of Drivers and Restraints

- Figure 9. North America Immunodiagnostics Market - Revenue Forecast and Analysis - 2021-2030

- Figure 10. North America Immunodiagnostics Market, by Product, 2022 & 2030 (%)

- Figure 11. Enzyme-linked Immunosorbent Assays (ELISA): North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Chemiluminescence Immunoassays (CLIA): North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Vitamin D Assay: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 14. HIV Detection: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 15. HIV Ag/Ab Combo Assay: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Other Tests: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Radioimmunoassays (RIA): North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Others: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 19. North America Immunodiagnostics Market Share by Clinical Indication - 2022 & 2030 (%)

- Figure 20. Infectious Diseases: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 21. COVID-19: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 22. Tuberculosis: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 23. Lyme: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 24. Infection Management: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 25. Zika: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 26. Treponema: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 27. TORCH: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 28. Measles and Mumps: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 29. VZV: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 30. EBV: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 31. Hepatitis+HIV: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 32. Gastrointestinal: North America Immunodiagnostics Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 33. Metabolics: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 34. Endocrinology: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 35. Hypertension: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 36. Growth: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 37. Diabetes: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 38. Thyroid: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 39. Reproductive Endocrinology: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 40. Endocrinology: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- Figure 41. North America Immunodiagnostics Market Share by End User - 2022 & 2030 (%)

- Figure 42. Hospitals: North America Immunodiagnostics Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 43. Clinics: North America Immunodiagnostics Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 44. Diagnostic Laboratories: North America Immunodiagnostics Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 45. Academic and Research Institutes: North America Immunodiagnostics Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 46. Others: North America Immunodiagnostics Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 47. North America: Immunodiagnostics Market, by Key Country - Revenue (2022) (US$ Million)

- Figure 48. North America: Immunodiagnostics Market, by Country, 2022 & 2030 (%)

- Figure 49. US: Immunodiagnostics market - Revenue and Forecast to 2030 (US$ Million)

- Figure 50. Canada: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 51. Mexico: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

The North America immunodiagnostics market is expected to grow from US$ 10,463.48 million in 2023 to US$ 17,399.10 million by 2030. It is estimated to grow at a CAGR of 7.5% from 2023 to 2030.

Growing Use of Point-of-Care Immunodiagnostics Drive North America Industrial Robotics Market

Point-of-care testing (POCT) has become critical to patient-centric healthcare due to the need for rapid diagnostic results to determine accurate and faster treatments. A shift from centralized point-of-care testing to decentralized testing has resulted in easy access to these diagnostics. Immunoassay testing helps monitor chronic conditions and detect pathogens, such as bacteria and viruses. Advanced point-of-care devices enable rapid screening of up to three components from a single sample. Also, the point-of-care diagnostics (POCD) inclined toward mobile healthcare (mH) smart devices could revolutionize personalized healthcare monitoring and management, paving the way for next-generation POCTs. The management of infectious diseases can be significantly improved by POCTs, particularly in developing countries where access to timely medical care is challenging and healthcare infrastructure is outdated and sparse. Additionally, the technologically developed diagnostic kits leading to fewer manual errors propel the immunodiagnostics market. Several market players are developing innovative immunodiagnostics products. For instance, Thermo Fisher Scientific has developed immunodiagnostics products such as enzyme-linked immunoassay (ELISA) reagents and buffers, antibodies and detection probes, linking mechanisms, blocking buffers and detergents, detection substrates, and capture surfaces, as well as services such as bioconjugation and detection. Further, in September 2020, Roche launched the SARS-CoV-2 Rapid Antigen Test, which is used in POC settings to help healthcare professionals identify the infection within 15 minutes in people suspected of carrying the virus.

In April 2021, DiaSorin introduced the LIAISON IQ, a new immunodiagnostics Point-of-Care (POC) reader, and the LIAISON QuickDetect COVID TrimericS Ab test, developed with Lumos Diagnostics for countries accepting the CE Mark. Using a fingerstick of human capillary blood, this test for the LIAISON IQ identifies specific IgG antibodies against SARS-CoV-2 Spike Protein in 10 minutes.

In April 2021, Chembio Diagnostics, Inc. launched an FDA Emergency Use Authorization-approved, in-licensed rapid point-of-care COVID-19/Flu A&B test for use in traditional and decentralized testing settings. The rapid immunoassay test requires no instrumentation and produces results in 15 minutes.

WHO applauded the test kit developers for efforts taken to innovate and respond to the masses' requirements during the COVID-19 crisis. According to the American Society for Clinical Pathology, in March 2020, the Cepheid Xpert Xpress SARS-CoV-2 test became the first POC COVID-19 detection assay to receive Emergency Use Authorization (EUA) from the US Food and Drug Administration (FDA).

Likewise, the use of immunodiagnostics in cancer treatment is increasing. In oncology, an immunodiagnostics test can confirm the presence of a solid tumor by detecting known tumor-associated antigens or antibodies. These advantages and indications are driving the immunodiagnostics market.

North America Immunodiagnostics Market Overview

The prevalence of cancer is increasing in the country at an alarming rate, leading to the rising demand for cancer diagnoses. According to the American Cancer Society's (ASC) cancer facts & figures estimates for 2023, nearly 1.9 million new cancer cases were registered in the US. It is further projected that in 2023, the country will register 609,360 deaths from cancer, which is ~1,670 deaths a day. However, the increased diagnostics have reduced the number of cancer-linked deaths. As per the ASC, in the past 28 years, the death rate from cancer in men and women has fallen 32% from its peak in 1991 to 2019. The fall in death rates was found to be because of early and advanced cancer diagnoses. The awareness of the advancements in diagnostic technology has grown among people. Therefore, it has resulted in the significant growth of the immunoassay market in the US. Similarly, diabetes is prevailing at a high rate in the geriatric population in the US. Many companies are providing immunoassay kits for diabetes. For instance, Bio-Rad Laboratories, Inc. offers Bio-Plex Pro human diabetes immunoassays, which are reliable and convenient for studying human diabetes and obesity markers. They help in managing and treating diabetes in diabetic patients. The market is expected to witness significant growth due to the rising prevalence of diabetes among US citizens. According to the data published by the Centers for Disease Control and Prevention (CDC) in the 2023 National Diabetes Statistics Report, 37.3 million people have diabetes in the US, which accounts for 11.3% of the total US population. Also, the reports state that 96 million people aged 18 years or above are prediabetic, accounting for 38% of the US population. Thus, considering the prevalence of diabetes in the country, an increased demand for immunodiagnostics is anticipated, leading to market growth. There has been unprecedented growth in innovative and improved medical technologies in recent years. As a result, there have been developments in advanced diagnostics and the overall healthcare industry. Moreover, the US houses various companies developing cutting-edge products for point-of-care diagnosis, paving the way for the growth of the immunodiagnostics market. In April 2020, Bio-Rad Laboratories launched a blood-based immunoassay kit to identify antibodies to the SARS-CoV-2.

North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

North America Immunodiagnostics Market Segmentation

The North America immunodiagnostics market is segmented into product, clinical indication, end user, and country.

Based on product, the North America immunodiagnostics market is segmented into enzyme-linked immunosorbent assays (ELISA), chemiluminescence immunoassays (CLIA), radioimmunoassays (RIA), and others. In 2023, the enzyme-linked immunosorbent assays (ELISA) segment registered the largest share in the North America immunodiagnostics market. The chemiluminescence immunoassays (CLIA) segment is further segmented into vitamin D assay market, HIV detection market, HIV ag/ab combo assay market, and other tests.

Based on clinical indication, the North America immunodiagnostics market is segmented into infectious diseases, hepatitis+HIV, endocrinology, gastrointestinal, metabolics, and others. In 2023, the infectious diseases segment registered the largest share in the North America immunodiagnostics market. The infectious diseases segment is further segmented into COVID-19, tuberculosis, lyme, infection management, zika, treponema, torch, measles and mumps, VZV, and EBV. The endocrinology segment is further segmented into hypertension, growth, diabetes, thyroid, and reproductive endocrinology.

Based on end user, the North America immunodiagnostics market is segmented into hospitals, clinics, diagnostic laboratories, academic & research institutes, and others. In 2023, the hospitals segment registered the largest share in the North America immunodiagnostics market.

Based on country, the North America immunodiagnostics market is segmented into the US, Canada, Mexico. In 2023, the US registered the largest share in the North America immunodiagnostics market.

Abbott Laboratories; bioMerieux SA; Danaher Corp; DiaSorin SpA; F. Hoffmann-La Roche Ltd; PerkinElmer Inc; Shenzhen Mindray Bio-Medical Electronics Co., Ltd.; Siemens Healthcare GmbH; Svar Life Science AB; and Thermo Fisher Scientific Inc are some of the leading companies operating in the North America immunodiagnostics market.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the North America immunodiagnostics market.

- Highlights key business priorities in order to assist companies to realign their business strategies

- The key findings and recommendations highlight crucial progressive industry trends in the North America immunodiagnostics market, thereby allowing players across the value chain to develop effective long-term strategies

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets

- Scrutinize in-depth North America market trends and outlook coupled with the factors driving the immunodiagnostics market, as well as those hindering it

- Enhance the decision-making process by understanding the strategies that underpin commercial interest with respect to client products, segmentation, pricing, and distribution

Table Of Contents

1. Introduction

- 1.1 Scope of the Study

- 1.2 The Insight Partners Research Report Guidance

- 1.3 Market Segmentation

- 1.3.1 North America Immunodiagnostics Market - by Product

- 1.3.2 North America Immunodiagnostics Market - by Clinical Indication

- 1.3.3 North America Immunodiagnostics Market - by End User

- 1.3.4 North America Immunodiagnostics Market - by Country

2. North America Immunodiagnostics Market - Key Takeaways

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Immunodiagnostics Market - Market Landscape

- 4.1 Overview

- 4.2 North America PEST Analysis

- 4.3 Expert's Opinion

5. North America Immunodiagnostics Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increasing Prevalence of Infectious Diseases

- 5.1.2 Growing Use of Point-of-Care Immunodiagnostics

- 5.2 Market Restraints

- 5.2.1 Inadequate Reimbursement Scenario

- 5.3 Market Opportunities

- 5.3.1 Rising Focus on R&D Investment and Expansion by Key Players

- 5.4 Future Trends

- 5.4.1 Technological Advancements in Immunodiagnostics

- 5.5 Impact Analysis

6. Immunodiagnostics Market - North America Analysis

- 6.1 North America Immunodiagnostics Market Revenue Forecast and Analysis

7. North America Immunodiagnostics Market Analysis - by Product

- 7.1 Overview

- 7.2 North America Immunodiagnostics Market, By Product, 2022 & 2030 (%)

- 7.3 Enzyme-linked Immunosorbent Assays (ELISA)

- 7.3.1 Overview

- 7.3.2 Enzyme-linked Immunosorbent Assays (ELISA): North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 7.4 Chemiluminescence Immunoassays (CLIA)

- 7.4.1 Overview

- 7.4.2 Chemiluminescence Immunoassays (CLIA): North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 7.4.3 Vitamin D Assay

- 7.4.3.1 Overview

- 7.4.3.2 Vitamin D Assay: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 7.4.4 HIV Detection

- 7.4.4.1 Overview

- 7.4.4.2 HIV Detection: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 7.4.5 HIV Ag/Ab Combo assay

- 7.4.5.1 Overview

- 7.4.5.2 HIV Ag/Ab Combo Assay: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 7.4.6 Other Tests

- 7.4.6.1 Overview

- 7.4.6.2 Other Tests: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 7.5 Radioimmunoassays (RIA)

- 7.5.1 Overview

- 7.5.2 Radioimmunoassays (RIA): North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

8. North America Immunodiagnostics Market Analysis - Clinical Indication

- 8.1 Overview

- 8.2 North America Immunodiagnostics Market Share by Clinical Indication - 2022 & 2030 (%)

- 8.3 Infectious Diseases:

- 8.3.1 Overview

- 8.3.2 Infectious Diseases: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.1 COVID-19

- 8.3.2.1.1 Overview

- 8.3.2.1.2 COVID-19: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.2 Tuberculosis

- 8.3.2.2.1 Overview

- 8.3.2.2.2 Tuberculosis: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.3 Lyme

- 8.3.2.3.1 Overview

- 8.3.2.3.2 Lyme: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.4 Infection Management

- 8.3.2.4.1 Overview

- 8.3.2.4.2 Infection Management: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.5 Zika

- 8.3.2.5.1 Overview

- 8.3.2.5.2 Zika: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.6 Treponema

- 8.3.2.6.1 Overview

- 8.3.2.6.2 Treponema: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.7 TORCH

- 8.3.2.7.1 Overview

- 8.3.2.7.2 TORCH: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.8 Measles and Mumps

- 8.3.2.8.1 Overview

- 8.3.2.8.2 Measles and Mumps: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.9 VZV

- 8.3.2.9.1 Overview

- 8.3.2.9.2 VZV: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.10 EBV

- 8.3.2.10.1 Overview

- 8.3.2.10.2 EBV: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.1 COVID-19

- 8.4 Hepatitis+HIV:

- 8.4.1 Overview

- 8.4.2 Hepatitis+HIV: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.5 Gastrointestinal

- 8.5.1 Overview

- 8.5.2 Gastrointestinal: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.6 Metabolic Disorders

- 8.6.1 Overview

- 8.6.2 Metabolics: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.7 Endocrinology

- 8.7.1 Overview

- 8.7.2 Endocrinology: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.7.3 Hypertension

- 8.7.3.1 Overview

- 8.7.3.2 Hypertension: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.7.4 Growth

- 8.7.4.1 Overview

- 8.7.4.2 Growth: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.7.5 Diabetes

- 8.7.5.1 Overview

- 8.7.5.2 Diabetes: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.7.6 Thyroid

- 8.7.6.1 Overview

- 8.7.6.2 Thyroid: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.7.7 Reproductive Endocrinology

- 8.7.7.1 Overview

- 8.7.7.2 Reproductive Endocrinology: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 8.8 Others

- 8.8.1 Overview

- 8.8.2 Others: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

9. North America Immunodiagnostics Market Analysis - End User

- 9.1 Overview

- 9.2 North America Immunodiagnostics Market Share by End User - 2022 & 2030 (%)

- 9.3 Hospitals

- 9.3.1 Overview

- 9.3.2 Hospitals: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 9.4 Clinics

- 9.4.1 Overview

- 9.4.2 Clinics: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 9.5 Diagnostic Laboratories

- 9.5.1 Overview

- 9.5.2 Diagnostic Laboratories: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 9.6 Academic and Research Institutes

- 9.6.1 Overview

- 9.6.2 Academic and Research Institutes: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

- 9.7 Others

- 9.7.1 Overview

- 9.7.2 Others: North America Immunodiagnostics Market Revenue and Forecast to 2030 (US$ Million)

10. North America Immunodiagnostics Market - Revenue and Forecast to 2030 - Country Analysis

- 10.1 Overview

- 10.1.1.1 US: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.1 Overview

- 10.1.1.1.2 US: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.3 US: Immunodiagnostics Market, by Product, 2020-2030 (US$ Million)

- 10.1.1.1.3.1 US: Immunodiagnostics Market, by Chemiluminescence Immunoassays (CLIA)- Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.4 US: Immunodiagnostics Market, by Clinical Indication - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.4.1 US: Immunodiagnostics Market, by Infectious Diseases - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.4.2 US: Immunodiagnostics Market, by Endocrinology - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.1.5 US: Immunodiagnostics Market, by End User, 2020-2030 (US$ Million)

- 10.1.1.2 Canada: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.1 Overview

- 10.1.1.2.2 Canada: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.3 Canada: Immunodiagnostics Market, by Product, 2020-2030 (US$ Million)

- 10.1.1.2.3.1 Canada: Immunodiagnostics Market, by Chemiluminescence Immunoassays (CLIA)- Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.4 Canada: Immunodiagnostics Market, by Clinical Indication - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.4.1 Canada: Immunodiagnostics Market, by Infectious Diseases - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.4.2 Canada: Immunodiagnostics Market, by Endocrinology - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.2.5 Canada: Immunodiagnostics Market, by End User, 2020-2030 (US$ Million)

- 10.1.1.3 Mexico: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.1 Overview

- 10.1.1.3.2 Mexico: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.3 Mexico: Immunodiagnostics Market, by Product, 2020-2030 (US$ Million)

- 10.1.1.3.3.1 Mexico: Immunodiagnostics Market, by Chemiluminescence Immunoassays (CLIA)- Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.4 Mexico: Immunodiagnostics Market, by Clinical Indication - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.4.1 Mexico: Immunodiagnostics Market, by Infectious Diseases - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.4.2 Mexico: Immunodiagnostics Market, by Endocrinology - Revenue and Forecast to 2030 (US$ Million)

- 10.1.1.3.5 Mexico: Immunodiagnostics Market, by End User, 2020-2030 (US$ Million)

- 10.1.1.1 US: Immunodiagnostics Market - Revenue and Forecast to 2030 (US$ Million)

11. North America Immunodiagnostics Market -Industry Landscape

- 11.1 Overview

- 11.2 Inorganic Growth Strategies

- 11.2.1 Overview

- 11.3 Organic Growth Strategies

- 11.3.1 Overview

12. Company Profiles

- 12.1 Abbott Laboratories

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 F. Hoffmann-La Roche Ltd

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 DiaSorin SpA

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Danaher Corp

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Thermo Fisher Scientific Inc

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 PerkinElmer Inc

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 bioMerieux SA

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Svar Life Science AB

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Siemens Healthcare GmbH

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Glossary of Terms