|

|

市場調査レポート

商品コード

1372561

東南アジアの再分配層材料市場規模・予測、地域シェア、動向、成長機会分析レポート収録範囲:タイプ別、用途別Southeast Asia Redistribution Layer Material Market Size and Forecasts, Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Type and Application |

||||||

|

|

|||||||

|

|||||||

| 東南アジアの再分配層材料市場規模・予測、地域シェア、動向、成長機会分析レポート収録範囲:タイプ別、用途別 |

|

出版日: 2023年10月09日

発行: The Insight Partners

ページ情報: 英文 117 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

東南アジアの再分配層材料市場は、2022年の5,451万米ドルから2030年には1億5,011万米ドルに成長すると予測され、2022年から2030年までのCAGRは13.5%と予測されています。

再分配層(RDL)は、集積回路(IC)または半導体デバイス内の電気信号の経路と再分配に使用される導電性材料の薄膜または層です。この層は、IC内のトランジスター、コンデンサー、抵抗器などの部品を接続し、それらの間で信号が効率的に流れるようにするために不可欠です。東南アジアは、この需要の恩恵を受ける戦略的な位置にあります。この地域は、マレーシア、ベトナム、タイといった国々が重要な施設を擁しており、半導体製造・組立のハブとして台頭しています。これらの生産拠点が主要産業に近いということは、再分配層材料の調達が効率的でコスト効率に優れていることを意味します。さらに、自動車と通信セクターの経済成長は、サプライチェーン全体に波及効果をもたらしています。研究開発、技術、インフラへの投資が増加し、再配線層材料の分野における革新と開発を助長する環境が醸成されています。この動向の特徴は、生産量の増加、先進パッケージング技術、小型化要求、この地域の戦略的サプライチェーン上の位置、エコシステム全体へのプラスの経済効果です。これらの要因が総合的に、東南アジアの再分配層材料市場の成長を後押ししています。

コスト削減の追求において、半導体産業は常に革新的なソリューションの開発に取り組んできました。現在、大手半導体メーカーが検討しているアプローチのひとつが、ウエハーやストリップサイズからIC組立専用の大型パネルへの移行です。効率と規模の経済は、この道の付加価値です。ファンアウトパッケージの製造をウエハーから大型パネルに移行するFOWLP(Fan-Out Wafer Level Packaging)からFOPLP(Fan-Out Panel Level Packaging)は、より広く採用されるための解決策となりうる。民生用電子機器、車載システム、産業用機器の小型化・複雑化に伴い、先進的な半導体パッケージング技術へのニーズが高まっています。再分配層はこのプロセスに不可欠であり、より小さなフォームファクターの折り畳みを可能にし、機能性を高め、性能を向上させる。東南アジアのメーカーは、必要な材料を生産・供給することで、この動向を活用できる立場にあります。パッケージング業界の先進化、特に2.5Dと3Dパッケージング技術の採用は、東南アジアの再配線層材料市場成長の重要な促進要因になると見られています。2.5Dおよび3Dパッケージング技術は、チップ密度と機能性を大幅に向上させる。複数の半導体ダイを互いに、あるいは横に積み重ねることで、これらの技術はより堅牢でコンパクトな電子デバイスを可能にします。再配線層は、これらの積層または隣接するダイ間の相互接続を形成し、効率的なデータ転送と電気的接続を確保するために不可欠です。東南アジアは、半導体製造の専門知識を活用して、こうした先進パッケージング技術に必要な重要な再配線層材料を供給することができます。

これらのパッケージング技術は、性能とエネルギー効率の向上という点で特筆すべき利点を提供します。2.5Dおよび3Dパッケージングでは、相互接続長が短くなり、信号経路が短縮されるため、データ処理の高速化と消費電力の低減に貢献します。その結果、シグナルインテグリティと熱管理を維持できる再分配層材料の需要がさらに重要になります。東南アジアは、世界の産業界の需要に応えるため、こうした先端材料を供給する上で極めて重要な役割を果たすことができます。さらに、自動車業界は、ADAS(先進運転支援システム)や自律走行技術の統合を可能にするため、2.5Dおよび3Dパッケージングを採用しつつあります。これらのアプリケーションは、信頼性の高い再配線層材料を必要とする、緊密に統合された高性能半導体パッケージに依存しています。東南アジアは、自動車エレクトロニクス製造における存在感が強く、東南アジアの再配線層材料市場成長の主要な貢献国となっています。

世界中のメーカーが新しいパッケージング技術を開発しています。例えば、2021年5月、サムスン電子は、高性能コンピューティング(HPC)からAI、5G、クラウド、大規模データセンター、高速通信、ヘテロジニアス集積によるロジック&メモリー間の電力効率の改善などを実現するI-Cube4を発表しました。また、2023年9月には、ASIC設計サービス、IPプロバイダーであるファラデーテクノロジー株式会社が、2.5D/3D先進パッケージサービスの開始を発表しました。2.5Dパッケージ技術は、AIアクセラレータ、グラフ・プロセッシング・ユニット、ネットワーキング・プロセッサなどのHPCをターゲットに、最高性能を達成するために使用されます。このようなパッケージング技術の先進化は、東南アジアの再分配層材料市場の成長を後押しすると期待されています。

東南アジアの再分配層材料市場に参入している主な企業は、Advanced Semiconductor Engineering, Inc、Amkor Technology、Fujifilm Corporation、DuPont、Infineon Technologies AG、NXP Semiconductors、Samsung Electronics Co.Ltd、信越化学工業、SK Hynix Inc、Jiangsu Changjiang Electronics Technology Co.Ltdなどです。東南アジアの再分配層材料市場で事業を展開する企業は、顧客の要求を満たすため、高品質で革新的な製品の開発に注力しています。

東南アジアの再分配層材料市場全体の規模は、一次情報と二次情報の両方を用いて導き出されたものです。東南アジアの再分配層材料市場に関連する質的・量的情報を入手するため、社内外の情報源を用いて徹底的な二次調査を実施しました。また、データを検証し、トピックに関するより詳細な分析的洞察を得るために、業界関係者に複数の一次インタビューを実施しました。このプロセスの参入企業には、副社長、市場開拓マネージャー、マーケットインテリジェンスマネージャー、国内営業マネージャーなどの業界専門家と、東南アジアの再分配層材料市場を専門とする評価専門家、調査アナリスト、キーオピニオンリーダーなどの外部コンサルタントが含まれます。

目次

第1章 イントロダクション12

- 洞察・パートナーズ調査報告書のガイダンス12

- 市場セグメンテーション13

第2章 エグゼクティブサマリー14

- 主要な洞察14

- 市場の魅力15

第3章 調査手法16

- 調査対象範囲17

- 2次調査。18

- 1次調査。18

第4章 東南アジアの再配線層材料市場情勢19

- 概要19

- ポーターのファイブフォース分析20

- 供給企業の交渉力。20

- 買い手の交渉力。21

- 新規参入業者の脅威。21

- 競争企業間の敵対関係。21

- 代替品の脅威。22

- エコシステム分析。23

- 原材料サプライヤー。23

- 製造業者。23

- 最終用途24

- バリューチェーンのベンダー一覧25

第5章 東南アジアの再配線層材料市場:主要市場力学 27

- 市場促進要因27

- AIベースの機器とツールへの注目の高まり。27

- 自動車産業と通信産業からの需要増加。28

- 市場抑制要因。29

- 原材料価格の変動。29

- 市場機会。30

- 業界別IoTとコネクテッドデバイスの普及。30

- 今後の動向。30

- パッケージング技術の先進化。30

- 影響分析。32

第6章 再配布層材料市場-東南アジア市場分析33

- 東南アジアの再配送層材料市場の売上高33

- 東南アジアの再配線層材料市場数量34

- 東南アジアの再配線層材料市場の予測と分析35

第7章 東南アジアの再配線層材料市場分析-タイプ 36

- ポリイミド(PI) 38

- 概要38

- ポリイミド(PI)の市場規模推移と2030年までの予測39

- ポリベンゾオキサゾール(PBO) 39

- 概要39

- ポリベンゾオキサゾール(PBO)の市場規模推移と2030年までの予測40

- ベンゾシロブテン(BCB) 41

- 概要41

- ベンゾシロブテン(BCB)の市場量と2030年までの予測42

- その他42

- 概要42

- その他の市場規模推移と2030年までの予測44

第8章 東南アジアの再配線層材料市場分析-用途 45

- ファンアウトウエハーレベルパッケージング(FOWLP) 46

- 概要46

- ファンアウトウェーハレベルパッケージング(FOWLP)市場の収益と2030年までの予測47

- 2.5D/3D ICパッケージング48

- 概要。48

- 2.5D/3D ICパッケージ市場の収益と2030年までの予測48

第9章 東南アジアの再配線層材料市場:地域別分析49

- 東南アジアの再配線層材料市場49

- 概要49

- 東南アジアの再配線層材料市場:国別内訳4950

- 再配線層材料の国別市場内訳.50

- インドネシアの再配線層材料の市場規模推移と2030年までの予測51

- シンガポールの再配線層材料の市場規模推移と2030年までの予測54

- マレーシアの再配線層材料の市場規模推移と2030年までの予測57

- 台湾の再配線層材料の市場規模推移と2030年までの予測60

- タイの再配送層材料の市場規模推移と2030年までの予測63

- ベトナムの再配線層材料の市場規模推移と2030年までの予測66

- その他の東南アジアの再配線層材料の市場規模推移と2030年までの予測69

第10章 COVID-19パンデミックの東南アジア再配布層材市場への影響72

- COVID-19前後の影響72

第11章 競合情勢73

- 主要企業別ヒートマップ分析73

- 企業のポジショニングと集中度73

第12章 業界情勢74

- 概要74

- 市場イニシアティブ74

- 新製品開発75

- 合併と買収75

第13章 企業プロファイル

- SK Hynix Inc. 76

- Samsung Electronics Co Ltd. 80

- Infineon Technologies AG. 84

- DuPont de Nemours Inc. 88

- FUJIFILM Holdings Corp. 92

- Amkor Technology Inc. 96

- ASE Technology Holding Co Ltd. 100

- NXP Semiconductors NV. 104

- JCET Group Co Ltd. 108

- Shin-Etsu Chemical Co Ltd. 112

第14章 付録116

List Of Tables

- Table 1. Southeast Asia Redistribution Layer Material Market Segmentation. 13

- Table 2. List of Raw Material Suppliers in Value Chain. 25

- Table 3. List of Manufacturers in Value Chain. 26

- Table 4. Southeast Asia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 35

- Table 5. Southeast Asia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 35

- Table 6. Southeast Asia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 36

- Table 7. Southeast Asia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 37

- Table 8. Southeast Asia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 45

- Table 9. Indonesia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 52

- Table 10. Indonesia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 52

- Table 11. Indonesia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 53

- Table 12. Singapore Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 55

- Table 13. Singapore Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 55

- Table 14. Singapore Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 56

- Table 15. Malaysia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 58

- Table 16. Malaysia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 58

- Table 17. Malaysia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 59

- Table 18. Taiwan Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 61

- Table 19. Taiwan Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 61

- Table 20. Taiwan Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 62

- Table 21. Thailand Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 64

- Table 22. Thailand Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 64

- Table 23. Thailand Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 65

- Table 24. Vietnam Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 67

- Table 25. Vietnam Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 67

- Table 26. Vietnam Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 68

- Table 27. Rest of Southeast Asia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Type. 70

- Table 28. Rest of Southeast Asia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) - Type. 70

- Table 29. Rest of Southeast Asia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) - Application. 71

- Table 30. Company Positioning & Concentration. 73

List Of Figures

- Figure 1. Southeast Asia Redistribution Layer Material Market Segmentation, By Country. 13

- Figure 2. Southeast Asia Redistribution Layer Material Market - Porter's Analysis. 20

- Figure 3. Ecosystem: Southeast Asia Redistribution Layer Material Market 23

- Figure 4. Market Dynamics: Southeast Asia Redistribution Layer Material Market 27

- Figure 5. Southeast Asia Redistribution Layer Material Market Impact Analysis of Drivers and Restraints. 32

- Figure 6. Southeast Asia Redistribution Layer Material Market Revenue (US$ Million), 2020 - 2030. 33

- Figure 7. Southeast Asia Redistribution Layer Material Market Volume (Tons), 2020 - 2030. 34

- Figure 8. Southeast Asia Redistribution Layer Material Market Share (%) - Type, 2022 and 2030. 36

- Figure 9. Polyimide (PI) Market Revenue and Forecasts To 2030 (US$ Million) 38

- Figure 10. Polyimide (PI) Market Volume and Forecasts To 2030 (Tons) 39

- Figure 11. Polybenzoxazole (PBO) Market Revenue and Forecasts To 2030 (US$ Million) 40

- Figure 12. Polybenzoxazole (PBO) Market Volume and Forecasts To 2030 (Tons) 40

- Figure 13. Benzocylobutene (BCB) Market Revenue and Forecasts To 2030 (US$ Million) 41

- Figure 14. Benzocylobutene (BCB) Market Volume and Forecasts To 2030 (Tons) 42

- Figure 15. Others Market Revenue and Forecasts To 2030 (US$ Million) 43

- Figure 16. Others Market Volume and Forecasts To 2030 (Tons) 44

- Figure 17. Southeast Asia Redistribution Layer Material Market Share (%) -Application, 2022 and 2030. 45

- Figure 18. Fan-Out Wafer Level Packaging (FOWLP) Market Revenue and Forecasts To 2030 (US$ Million) 47

- Figure 19. 2.5D/3D IC Packaging Market Revenue and Forecasts To 2030 (US$ Million) 48

- Figure 20. Southeast Asia Redistribution Layer Material Market Breakdown By Key Countries, 2022 And 2030 (%) 50

- Figure 21. Indonesia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 50

- Figure 22. Indonesia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 51

- Figure 23. Singapore Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 54

- Figure 24. Singapore Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 54

- Figure 25. Malaysia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 57

- Figure 26. Malaysia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 57

- Figure 27. Taiwan Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 60

- Figure 28. Taiwan Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 60

- Figure 29. Thailand Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 63

- Figure 30. Thailand Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 63

- Figure 31. Vietnam Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 66

- Figure 32. Vietnam Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 66

- Figure 33. Rest of Southeast Asia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 69

- Figure 34. Rest of Southeast Asia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 69

- Figure 35. Heat Map Analysis By Key Players. 73

The Southeast Asia redistribution layer material market is expected to grow from US$ 54.51 million in 2022 to US$ 150.11 million by 2030; it is expected to grow at a CAGR of 13.5% from 2022 to 2030.

The redistribution layer (RDL) is the thin film or layer of conductive material used to route and redistribute electrical signals within an integrated circuit (IC) or semiconductor device. This layer is essential for connecting components, such as transistors, capacitors, and resistors, within the IC and ensuring that signals can flow efficiently between them. Southeast Asia is strategically positioned to benefit from this demand. The region has emerged as a semiconductor manufacturing and assembly hub, with countries such as Malaysia, Vietnam, and Thailand hosting significant facilities. The proximity of these production centers to the key industries means that sourcing redistribution layer materials is efficient and cost-effective. Additionally, the economic growth of the automotive and telecommunications sectors has a ripple effect on the entire supply chain. Investments in research and development, technology, and infrastructure are increasing, fostering an environment conducive to innovation and development in the field of redistribution layer materials. This trend is characterized by increased production, advanced packaging technologies, miniaturization requirements, the region's strategic supply chain position, and a positive economic impact on the entire ecosystem. These factors collectively propel the Southeast Asia redistribution layer material market growth.

In the quest for cost reduction, the semiconductor industry has always been involved in developing innovative solutions. One approach currently considered by the leading semiconductor players is the migration from wafer and strip size to large-size panels dedicated to IC assembly. Efficiency and economies of scale are the added value of this path. Moving fan-out package manufacturing from a wafer, Fan-Out Wafer Level Packaging (FOWLP) to a large-scale panel, Fan-Out Panel Level Packaging (FOPLP), could be the solution for a wider adoption. As consumer electronics, automotive systems, and industrial devices become more compact and complex, there is a growing need for advanced semiconductor packaging technologies. Redistribution layers are integral to this process, it enables the creasing of smaller form factors, increases functionality and improves performance. Manufacturers in Southeast Asia are positioned to capitalize on this trend by producing and supplying the necessary materials. Advancements in the packaging industries, specifically the adoption of 2.5D and 3D packaging technologies, are poised to be significant drivers of the Southeast Asia redistribution layer material market growth. 2.5D and 3D packaging technologies significantly increase chip density and functionality. By stacking multiple semiconductors die on each other or side by side, these technologies allow for more robust and compact electronic devices. Redistribution layers are essential for creating interconnections between these stacked or adjacent dies, ensuring efficient data transfer and electrical connectivity. Southeast Asia can leverage semiconductor manufacturing expertise to supply the critical redistribution layer materials required for these advanced packaging techniques.

These packaging technologies offer notable advantages in terms of improved performance and energy efficiency. With 2.5D and 3D packaging, shorter interconnect lengths and reduced signal paths contribute to faster data processing and lower power consumption. As a result, demand for redistribution layer materials capable of maintaining signal integrity and thermal management becomes even more crucial. Southeast Asia can play a pivotal role in delivering these advanced materials to meet global industry demands. Furthermore, the automotive industry is embracing 2.5D and 3D packaging to enable the integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies. These applications rely on tightly integrated, high-performance semiconductor packages that demand reliable redistribution layer materials. Southeast Asia's strong presence in automotive electronics manufacturing positions it as a key contributor to the Southeast Asia redistribution layer material market growth.

Manufacturers across the globe are developing new packaging technologies. For instance, in May 2021, Samsung Electronics launched I-Cube4, for High-Performance Computing (HPC) to AI, 5G, cloud, and large data center, fast communication, and improving power efficiency between logic & memory through heterogeneous integration. In addition, in September 2023, Faraday Technology Corporation, an ASIC design service, and IP provider, announced the launch of its 2.5D/3D advanced package service. The 2.5D package technology is used for achieving the highest performance, targeting HPC such as AI accelerator, graph processing unit, and networking processor. Such advancements in packaging technology are expected to bolster the Southeast Asia redistribution layer material market growth.

A few key players operating in the Southeast Asia redistribution layer material market are Advanced Semiconductor Engineering, Inc; Amkor Technology; Fujifilm Corporation; DuPont; Infineon Technologies AG; NXP Semiconductors; Samsung Electronics Co., Ltd; Shin-Etsu Chemical Co., Ltd; SK Hynix Inc; and Jiangsu Changjiang Electronics Technology Co., Ltd. Players operating in the Southeast Asia redistribution layer material market are highly focused on developing high-quality and innovative product offerings to fulfill customers' requirements.

The overall Southeast Asia redistribution layer material market size has been derived using both primary and secondary sources. Exhaustive secondary research has been conducted using internal and external sources to obtain qualitative and quantitative information related to the Southeast Asia redistribution layer material market. Also, multiple primary interviews have been conducted with industry participants to validate the data and gain more analytical insights into the topic. The participants of this process include industry experts, such as VPs, business development managers, market intelligence managers, and national sales managers-along with external consultants, such as valuation experts, research analysts, and key opinion leaders-specializing in the Southeast Asia redistribution layer material market.

Reasons to Buy:

- Progressive industry trends in the Southeast Asia redistribution layer material market to help players develop effective long-term strategies

- Business growth strategies adopted by developed and developing markets

- Quantitative analysis of the Southeast Asia redistribution layer material market from 2020 to 2030

- Estimation of the demand for redistribution layer material across various industries

- Porter’s five forces analysis provide a 360-degree view of the Southeast Asia redistribution layer material market

- Recent developments to understand the competitive market scenario and the demand for redistribution layer material in the Southeast Asia scenario.

- Market trends and outlook coupled with factors driving and restraining the growth of the Southeast Asia redistribution layer material market.

- Decision-making process by understanding strategies that underpin commercial interest concerning the Southeast Asia redistribution layer material market growth

- The Southeast Asia redistribution layer material market size at various nodes of market

- Detailed overview and segmentation of the Southeast Asia redistribution layer material market as well as its dynamics in the industry

- The Southeast Asia redistribution layer material market size in different regions with promising growth opportunities

Table Of Contents

1. Introduction 12

- 1.1 The Insight Partners Research Report Guidance. 12

- 1.2 Market Segmentation. 13

2. Executive Summary 14

- 2.1 Key Insights. 14

- 2.2 Market Attractiveness. 15

3. Research Methodology 16

- 3.1 Coverage. 17

- 3.2 Secondary Research. 18

- 3.3 Primary Research. 18

4. Southeast Asia Redistribution Layer Material Market Landscape 19

- 4.1 Overview. 19

- 4.2 Porter's Five Forces Analysis. 20

- 4.2.1 Bargaining Power of Suppliers. 20

- 4.2.2 Bargaining Power of Buyers. 21

- 4.2.3 Threat of New Entrants. 21

- 4.2.4 Intensity of Competitive Rivalry. 21

- 4.2.5 Threat of Substitutes. 22

- 4.3 Ecosystem Analysis. 23

- 4.3.1 Raw Material Suppliers. 23

- 4.3.2 Manufacturers. 23

- 4.3.3 End Use. 24

- 4.3.4 List of Vendors in the Value Chain: 25

5. Southeast Asia Redistribution Layer Material Market - Key Market Dynamics 27

- 5.1 Market Drivers. 27

- 5.1.1 Growing Focus on AI-based Equipment and Tools. 27

- 5.1.2 Increasing Demand from Automotive and Telecommunication Industries. 28

- 5.2 Market Restraints. 29

- 5.2.1 Fluctuation in Raw Material Prices. 29

- 5.3 Market Opportunities. 30

- 5.3.1 Proliferation of IoT and Connected Devices Across Industry Verticals. 30

- 5.4 Future Trends. 30

- 5.4.1 Advancements in the Packaging Technology. 30

- 5.5 Impact Analysis. 32

6. Redistribution Layer Material Market - Southeast Asia Market Analysis 33

- 6.1 Southeast Asia Redistribution Layer Material Market Revenue (US$ Million) 33

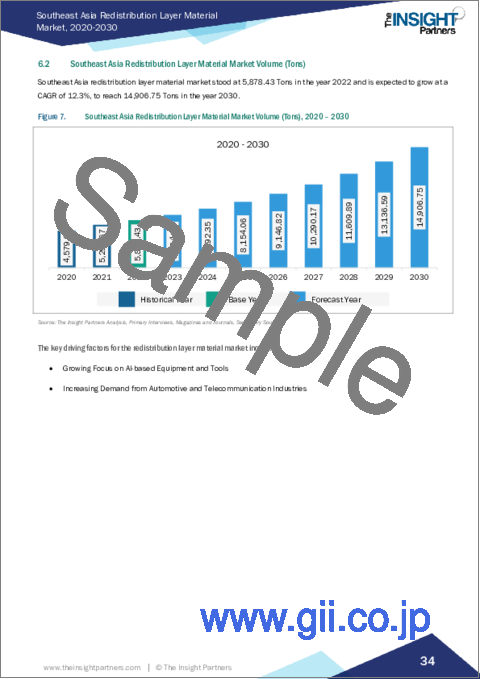

- 6.2 Southeast Asia Redistribution Layer Material Market Volume (Tons) 34

- 6.3 Southeast Asia Redistribution Layer Material Market Forecast and Analysis. 35

7. Southeast Asia Redistribution Layer Material Market Analysis - Type 36

- 7.1 Polyimide (PI) 38

- 7.1.1 Overview. 38

- 7.1.2 Polyimide (PI) Market Revenue and Forecast to 2030 (US$ Million) 38

- 7.1.3 Polyimide (PI) Market Volume and Forecast to 2030 (Tons) 39

- 7.2 Polybenzoxazole (PBO) 39

- 7.2.1 Overview. 39

- 7.2.2 Polybenzoxazole (PBO) Market Revenue and Forecast to 2030 (US$ Million) 40

- 7.2.3 Polybenzoxazole (PBO) Market Volume and Forecast to 2030 (Tons) 40

- 7.3 Benzocylobutene (BCB) 41

- 7.3.1 Overview. 41

- 7.3.2 Benzocylobutene (BCB) Market Revenue and Forecast to 2030 (US$ Million) 41

- 7.3.3 Benzocylobutene (BCB) Market Volume and Forecast to 2030 (Tons) 42

- 7.4 Others. 42

- 7.4.1 Overview. 42

- 7.4.2 Others Market Revenue and Forecast to 2030 (US$ Million) 43

- 7.4.3 Others Market Volume and Forecast to 2030 (Tons) 44

8. Southeast Asia Redistribution Layer Material Market Analysis - Application 45

- 8.1 Fan-Out Wafer Level Packaging (FOWLP) 46

- 8.1.1 Overview. 46

- 8.1.2 Fan-Out Wafer Level Packaging (FOWLP) Market Revenue, and Forecast to 2030 (US$ Million) 47

- 8.2 2.5D/3D IC Packaging. 48

- 8.2.1 Overview. 48

- 8.2.2 2.5D/3D IC Packaging Market Revenue, and Forecast to 2030 (US$ Million) 48

9. Southeast Asia Redistribution Layer Material Market - Geographical Analysis 49

- 9.1 Southeast Asia Redistribution Layer Material Market 49

- 9.1.1 Overview. 49

- 9.1.2 Southeast Asia Redistribution Layer Material Market Breakdown by Country. 50

- 9.1.2.1 Redistribution Layer Material Market Breakdown by Country. 50

- 9.1.2.2 Indonesia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 50

- 9.1.2.3 Indonesia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 51

- 9.1.2.3.1 Indonesia Redistribution Layer Material Market Breakdown by Type. 52

- 9.1.2.3.2 Indonesia Redistribution Layer Material Market Breakdown by Application. 53

- 9.1.2.4 Singapore Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 54

- 9.1.2.5 Singapore Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 54

- 9.1.2.5.1 Singapore Redistribution Layer Material Market Breakdown by Type. 55

- 9.1.2.5.2 Singapore Redistribution Layer Material Market Breakdown by Application. 56

- 9.1.2.6 Malaysia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 57

- 9.1.2.7 Malaysia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 57

- 9.1.2.7.1 Malaysia Redistribution Layer Material Market Breakdown by Type. 58

- 9.1.2.7.2 Malaysia Redistribution Layer Material Market Breakdown by Application. 59

- 9.1.2.8 Taiwan Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 60

- 9.1.2.9 Taiwan Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 60

- 9.1.2.9.1 Taiwan Redistribution Layer Material Market Breakdown by Type. 61

- 9.1.2.9.2 Taiwan Redistribution Layer Material Market Breakdown by Application. 62

- 9.1.2.10 Thailand Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 63

- 9.1.2.11 Thailand Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 63

- 9.1.2.11.1 Thailand Redistribution Layer Material Market Breakdown by Type. 64

- 9.1.2.11.2 Thailand Redistribution Layer Material Market Breakdown by Application. 65

- 9.1.2.12 Vietnam Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 66

- 9.1.2.13 Vietnam Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 66

- 9.1.2.13.1 Vietnam Redistribution Layer Material Market Breakdown by Type. 67

- 9.1.2.13.2 Vietnam Redistribution Layer Material Market Breakdown by Application. 68

- 9.1.2.14 Rest of Southeast Asia Redistribution Layer Material Market Revenue and Forecasts To 2030 (US$ Million) 69

- 9.1.2.15 Rest of Southeast Asia Redistribution Layer Material Market Volume and Forecasts To 2030 (Tons) 69

- 9.1.2.15.1 Rest of Southeast Asia Redistribution Layer Material Market Breakdown by Type. 70

- 9.1.2.15.2 Rest of Southeast Asia Redistribution Layer Material Market Breakdown by Application. 71

10. Impact of COVID-19 Pandemic on Southeast Asia Redistribution Layer Material Market 72

- 10.1 Pre & Post Covid-19 Impact 72

11. Competitive Landscape 73

- 11.1 Heat Map Analysis By Key Players. 73

- 11.2 Company Positioning & Concentration. 73

12. Industry Landscape 74

- 12.1 Overview. 74

- 12.2 Market Initiative. 74

- 12.3 New Product Development 75

- 12.4 Merger and Acquisition. 75

13. Company Profiles 76

- 13.1 SK Hynix Inc. 76

- 13.1.1 Key Facts. 76

- 13.1.2 Business Description. 76

- 13.1.3 Products and Services. 77

- 13.1.4 Financial Overview. 77

- 13.1.5 SWOT Analysis. 79

- 13.1.6 Key Developments. 79

- 13.2 Samsung Electronics Co Ltd. 80

- 13.2.1 Key Facts. 80

- 13.2.2 Business Description. 80

- 13.2.3 Products and Services. 81

- 13.2.4 Financial Overview. 81

- 13.2.5 SWOT Analysis. 83

- 13.2.6 Key Developments. 83

- 13.3 Infineon Technologies AG. 84

- 13.3.1 Key Facts. 84

- 13.3.2 Business Description. 84

- 13.3.3 Products and Services. 85

- 13.3.4 Financial Overview. 85

- 13.3.5 SWOT Analysis. 87

- 13.3.6 Key Developments. 87

- 13.4 DuPont de Nemours Inc. 88

- 13.4.1 Key Facts. 88

- 13.4.2 Business Description. 88

- 13.4.3 Products and Services. 89

- 13.4.4 Financial Overview. 89

- 13.4.5 SWOT Analysis. 91

- 13.4.6 Key Developments. 91

- 13.5 FUJIFILM Holdings Corp. 92

- 13.5.1 Key Facts. 92

- 13.5.2 Business Description. 92

- 13.5.3 Products and Services. 93

- 13.5.4 Financial Overview. 93

- 13.5.5 SWOT Analysis. 95

- 13.5.6 Key Developments. 95

- 13.6 Amkor Technology Inc. 96

- 13.6.1 Key Facts. 96

- 13.6.2 Business Description. 96

- 13.6.3 Products and Services. 97

- 13.6.4 Financial Overview. 97

- 13.6.5 SWOT Analysis. 99

- 13.6.6 Key Developments. 99

- 13.7 ASE Technology Holding Co Ltd. 100

- 13.7.1 Key Facts. 100

- 13.7.2 Business Description. 100

- 13.7.3 Products and Services. 101

- 13.7.4 Financial Overview. 101

- 13.7.5 SWOT Analysis. 103

- 13.7.6 Key Developments. 103

- 13.8 NXP Semiconductors NV. 104

- 13.8.1 Key Facts. 104

- 13.8.2 Business Description. 104

- 13.8.3 Products and Services. 105

- 13.8.4 Financial Overview. 105

- 13.8.5 SWOT Analysis. 107

- 13.8.6 Key Developments. 107

- 13.9 JCET Group Co Ltd. 108

- 13.9.1 Key Facts. 108

- 13.9.2 Business Description. 108

- 13.9.3 Products and Services. 108

- 13.9.4 Financial Overview. 109

- 13.9.5 SWOT Analysis. 110

- 13.9.6 Key Developments. 111

- 13.10 Shin-Etsu Chemical Co Ltd. 112

- 13.10.1 Key Facts. 112

- 13.10.2 Business Description. 112

- 13.10.3 Products and Services. 113

- 13.10.4 Financial Overview. 113

- 13.10.5 SWOT Analysis. 114

- 13.10.6 Key Developments. 115