|

|

市場調査レポート

商品コード

1360056

北米の外科用ステープル留め器具市場の2028年までの予測-地域別分析:製品タイプ、用途、エンドユーザー別North America Surgical Stapling Devices Market Forecast to 2028 -Regional Analysis - by Product, Type, Application, and End User |

||||||

|

|||||||

| 北米の外科用ステープル留め器具市場の2028年までの予測-地域別分析:製品タイプ、用途、エンドユーザー別 |

|

出版日: 2023年07月27日

発行: The Insight Partners

ページ情報: 英文 114 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

北米の外科用ステープリング装置市場は、2022年に19億6,294万米ドルと評価され、2028年には32億808万米ドルに達すると予測されています。2022年から2028年までのCAGRは8.5%で成長すると推定されています。

新製品の発売と戦略的提携が北米の外科用ステープル留め器具市場の成長を促進

病院で実施される外科手術の件数が大幅に増加しているため、医療機器メーカーは新製品の開発・発売と規制当局の承認取得を余儀なくされています。外科用ステープリング装置市場の主要企業は、新製品を開発するための研究開発活動に多大なリソースを割いています。例えば、2022年10月、Teleflex Incorporatedは、肥満手術のための革新的な動力ステープリング技術を商品化しているStandard Bariatrics, Inc.の買収を完了しました。テレフレックスは、買収完了時に1億7,000万米ドルでスタンダード・ベアトリクス社を買収し、特定の商業的マイルストーン達成時に最大1億3,000万米ドルの追加対価を支払う。同様に、2022年6月、ジョンソン・エンド・ジョンソンMedTech傘下のEthicon社は、米国でECHELON 3000ステープラーを発売しました。ECHELON 3000 Staplerは、外科医が患者固有のニーズに対応できるよう、片手で簡単に操作できるデジタル機器です。ECHELON 3000は、顎の開口部が39%大きく、関節スパンが27%大きく設計されており、外科医は、狭いスペースや困難な組織であっても、各切断部へのアクセスやコントロールを向上させることができます。リアルタイムの触覚および音声による装置フィードバックを提供するソフトウェアと組み合わせることで、これらの機能は、外科医が手技中に重要な調整を行うことを可能にします。このような革新的な製品の市場開拓や発売の増加、企業買収や提携が、北米の外科用ステープリング装置市場の成長を後押ししています。

北米の外科用ステープリング装置市場概要

北米の外科用ステープリング装置市場は、米国、カナダ、メキシコに区分されます。米国は、この地域の市場に対する最大の貢献者になると予想されています。北米の市場成長は、高齢者人口の増加、有利なヘルスケア改革、毎年大量に行われる外科手術に起因しています。Journal of Thoracic Disease誌によると、米国では年間530,000件の一般胸部手術が4,000人の心臓胸部外科医によって行われています。米国関節置換術レジストリ(AJRR)によると、2030年までに348万人が膝関節置換術を必要とすると推定されています。この推計は、米国で団塊の世代が高齢になることを考慮して算出されたものです。人工関節全置換術(TJR)は、米国で最も多く行われている選択的手術の一つです。米国整形外科学会(AAOS)の2018年年次総会で発表された新しい研究によると、一次人工股関節全置換術(THR)の件数は2030年までに171%増加し、一次人工膝関節全置換術(TKR)の件数は~189%増加し、それぞれ63万5000件と128万件に達すると予測されています。さまざまな種類の手術において、漏れを防ぐ生体適合性の高いステープルなど、先進的な手術方法や道具に対する需要が急増していることが、米国の外科用ステープル留め器具市場の成長を後押ししています。

北米の外科用ステープル留め器具市場の収益と2028年までの予測(金額)

北米の外科用ステープリングデバイス市場のセグメンテーション

北米の外科用ステープリングデバイス市場は、製品、タイプ、用途、エンドユーザー、国別に区分されます。製品に基づいて、市場は動力式外科用ステープラーと手動式外科用ステープラーに区分されます。2022年には、動力式外科用ステープラ部門がより大きな市場シェアを占めました。

タイプ別では、北米の外科用ステープリングデバイス市場は使い捨て外科用ステープラーと再利用可能外科用ステープラーに区分されます。2022年には、使い捨て外科用ステープルがより大きな市場シェアを占めています。

用途別では、北米の外科用ステープリングデバイス市場は整形外科、内視鏡外科、心臓・胸部外科、腹部・骨盤外科、その他に区分されます。整形外科セグメントは2022年に最大の市場シェアを記録しました。

エンドユーザー別では、北米の外科用ステープル留め器具市場は病院と外来手術センターに区分されます。病院セグメントが2022年に大きな市場シェアを占めました。

国別では、北米の外科用ステープリング装置市場は米国、カナダ、メキシコに区分されます。米国が2022年のこの地域の市場を独占しています。

3M Co、B. Braun SE、Conmed Corp、Ethicon USA LLC、Intuitive Surgical Inc、Medtronic Plcが北米外科用ステープリング装置市場で事業を展開する大手企業です。

目次

第1章 イントロダクション

第2章 北米の外科用ステープル留め器具市場-要点

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米の外科用ステープル留め器具市場-市場情勢

- 北米PEST分析

- 専門家の見解

第5章 北米の外科用ステープル留め器具市場-主要市場力学

- 市場促進要因

- 創傷と外科手術の増加

- 新製品の発売と企業間の戦略的提携

- 市場抑制要因

- 製品リコールとデバイスコストの高騰

- 市場機会

- 美容外科の人気急上昇と新興諸国における医療ツーリズムの成長

- 今後の動向

- 技術の進歩

- 影響分析

第6章 外科用ステープル留め器具市場:北米分析

- 北米の外科用ステープリングデバイス市場収益と予測分析

第7章 北米の外科用ステープル留め器具市場-2028年までの収益と予測:製品別

- 北米の外科用ステープリングデバイス市場:2021年・2028年製品別売上高シェア(%)

- 電動式外科用ステープラー

- 手動式外科用ステープラー

第8章 北米の外科用ステープリングデバイス市場-2028年に至る収益と予測-タイプ別

- 北米の外科用ステープリングデバイス市場2021年・2028年タイプ別売上高シェア(%)

- 使い捨て外科用ステープラー

- 再利用可能外科用ステープラー

第9章 北米の外科用ステープリングデバイス市場分析と2028年までの予測-用途別

- 北米の外科用ステープリングデバイス市場:用途別2021年・2028年(%)

- 整形外科

- 内視鏡外科

- 心臓外科および胸部外科

- 腹部および骨盤外科

- その他

第10章 北米外科用ステープル留め器具市場:エンドユーザー別収益と2028年までの予測

- 北米の外科用ステープル留め器具市場:2021年・2028年エンドユーザー別売上高シェア(%)

- 病院

- 外来手術センター

第11章 北米の外科用ステープル留め器具市場:2028年までの収益と予測:国別分析

- 北米

- 米国

- カナダ

- メキシコ

第12章 北米の外科用ステープル留め器具市場-業界情勢

- 有機的成長戦略

第13章 企業プロファイル

- Intuitive Surgical Inc

- Medtronic Plc

- Ethicon USA LLC

- B. Braun SE

- Conmed Corp

- 3M Co

第14章 付録

List Of Tables

- Table 1. North America Surgical Stapling Devices Market, Revenue and Forecast, 2019-2028 (US$ Mn)

- Table 2. United States Surgical Stapling Devices Market, by Product - Revenue and forecast to 2028 (USD Million)

- Table 3. United States Surgical Stapling Devices Market, by Type - Revenue and forecast to 2028 (USD Million)

- Table 4. United States Surgical Stapling Devices Market, by Application - Revenue and forecast to 2028 (USD Million)

- Table 5. United States Surgical Stapling Devices Market, by End User - Revenue and forecast to 2028 (USD Million)

- Table 6. Canada Surgical Stapling Devices Market, by Product- Revenue and forecast to 2028 (USD Million)

- Table 7. Canada: Surgical Stapling Devices Market, by Type- Revenue and forecast to 2028 (USD Million)

- Table 8. Canada Surgical Stapling Devices Market, by Application - Revenue and forecast to 2028 (USD Million)

- Table 9. Canada Surgical Stapling Devices Market, by End User - Revenue and forecast to 2028 (USD Million)

- Table 10. Mexico Surgical Stapling Devices Market, by Product- Revenue and forecast to 2028 (USD Million)

- Table 11. Mexico: Surgical Stapling Devices Market, by Type- Revenue and forecast to 2028 (USD Million)

- Table 12. Mexico Surgical Stapling Devices Market, by Application - Revenue and forecast to 2028 (USD Million)

- Table 13. Mexico Surgical Stapling Devices Market, by End User- Revenue and forecast to 2028 (USD Million)

- Table 14. Recent Organic Growth Strategies in the Surgical Stapling Devices Market

- Table 15. Glossary of Terms

List Of Figures

- Figure 1. North America Surgical Stapling Devices Market Segmentation

- Figure 2. North America Surgical Stapling Devices Market, by Country

- Figure 3. North America Surgical Stapling Devices Market Overview

- Figure 4. North America Surgical Stapling Devices Market, by Product

- Figure 5. North America Surgical Stapling Devices Market, by Country

- Figure 6. North America: PEST Analysis

- Figure 7. Experts\' Opinion

- Figure 8. North America Surgical Stapling Devices Market: Impact Analysis of Drivers and Restraints

- Figure 9. North America Surgical Stapling Devices Market - Revenue Forecast and Analysis

- Figure 10. North America Surgical Stapling Devices Market Revenue Share, by Product 2021 & 2028 (%)

- Figure 11. Powered Surgical Staplers: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 12. Manual Surgical Staplers: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 13. North America Surgical Stapling Devices Market Revenue Share, by Type 2021 & 2028 (%)

- Figure 14. Disposable Surgical Staplers: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 15. Reusable Surgical Staplers: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 16. North America Surgical Stapling Devices Market, by Application 2021 & 2028 (%)

- Figure 17. Endoscopic Surgery: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 18. Cardio and Thoracic Surgery: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 19. Abdominal and Pelvic Surgery: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 20. Others: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 21. North America Surgical Stapling Devices Market Revenue Share, by End User 2021 & 2028 (%)

- Figure 22. Hospitals: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 23. Ambulatory Surgical Centers: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 24. North America: Global Surgical Stapling Devices Market, by Key Country - Revenue (2021) (USD Million)

- Figure 25. North America: Surgical Stapling Devices Market, by Country, 2021 & 2028 (%)

- Figure 26. United States: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- Figure 27. Canada: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- Figure 28. Mexico: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

The North America surgical stapling devices market was valued at US$ 1,962.94 million in 2022 and is projected to reach US$ 3,208.08 million by 2028. It is estimated to grow at a CAGR of 8.5% from 2022 to 2028.

New Product Launches and Strategic Collaborations Fuel North America Surgical Stapling Devices Market Growth

A significant rise in the number of surgical procedures performed at hospitals has compelled medical device manufacturers to develop and launch new products and obtain regulatory approvals for them. Major companies in the surgical stapling devices market allocate significant resources to research and development activities to come up with new offerings. For instance, In October 2022, Teleflex Incorporated completed the acquisition of Standard Bariatrics, Inc., which has commercialized an innovative powered stapling technology for bariatric surgery. Teleflex acquired Standard Bariatrics for US$ 170 million at closing, with additional consideration of up to US$ 130 million that is payable upon achieving certain commercial milestones. Similarly, in June 2022, Ethicon, a part of Johnson & Johnson MedTech, launched ECHELON 3000 Stapler in the US. It is a digitally enabled device that provides surgeons with simple, one-handed powered articulation to help address the unique needs of their patients. Designed with a 39% greater jaw aperture and a 27% larger articulation span, ECHELON 3000 gives surgeons better access and control over each transection, even in tight spaces and on challenging tissue. Combined with software that provides real-time haptic and audible device feedback, these features enable surgeons to make critical adjustments during procedures. An increase in the number of developments and launches of such innovative products, along with business acquisitions and collaborations, boosts the growth of the North America surgical stapling devices market.

North America Surgical Stapling Devices Market Overview

The North America surgical stapling devices market is segmented into the US, Canada, and Mexico. The US is expected to be the largest contributor to the market in this region. The market growth in North America is ascribed to the growing geriatric population, favorable healthcare reforms, and surgical procedures performed in large numbers every year. According to the Journal of Thoracic Disease, ~530,000 general thoracic surgeries are performed yearly in the US by ~4,000 cardiothoracic surgeons. According to the American Joint Replacement Registry (AJRR), it is estimated that ~3.48 million people would require knee replacement by 2030. The estimates are calculated by considering the baby boomers reaching old age in the US. Total joint replacement (TJR) is one of the most performed elective surgeries in the US. According to a new study presented at the 2018 Annual Meeting of the American Academy of Orthopedic Surgeons (AAOS), the number of primary total hip replacement (THR) procedures is projected to grow by 171% by 2030, while the primary total knee replacement (TKR) procedures would increase by ~189%, reaching the count of 635,000 and 1.28 million procedures, respectively. A surge in demand for advanced surgical methods and tools such as biocompatible staples with better leakage protection in different types of surgeries favors the growth of the surgical stapling devices market in the US.

North America Surgical Stapling Devices Market Revenue and Forecast to 2028 (US$ Million)

North America Surgical Stapling Devices Market Segmentation

The North America surgical stapling devices market is segmented on the basis of product, type, application, end user, and country. Based on product, the market is segmented into powered surgical staplers and manual surgical staplers. The powered surgical staplers segment held a larger market share in 2022.

Based on type, the North America surgical stapling devices market is segmented into disposable surgical staplers and reusable surgical staplers. The disposable surgical staple segment accounted for a larger market share in 2022.

Based on application, the North America surgical stapling devices market is segmented into orthopedic surgery, endoscopic surgery, cardiac and thoracic surgery, abdominal and pelvic surgery, and others. The orthopedic surgery segment registered the largest market share in 2022.

Based on end user, the North America surgical stapling devices market is segmented into hospitals and ambulatory surgical centers. The hospitals segment accounted for a larger market share in 2022.

Based on country, the North America surgical stapling devices market is segmented into the US, Canada, and Mexico. The US dominated the market in this region in 2022.

3M Co, B. Braun SE, Conmed Corp, Ethicon USA LLC, Intuitive Surgical Inc, and Medtronic Plc are the leading companies operating in the North America surgical stapling devices market.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the North America surgical stapling devices market.

- Highlights key business priorities in order to assist companies to realign their business strategies

- The key findings and recommendations highlight crucial progressive industry trends in the North America surgical stapling devices market, thereby allowing players across the value chain to develop effective long-term strategies

- develop/modify business expansion plans by using substantial growth offering developed and emerging markets

- Scrutinize in-depth North America market trends and outlook coupled with the factors driving the surgical stapling devices market, as well as those hindering it

- Enhance the decision-making process by understanding the strategies that underpin commercial interest with respect to client products, segmentation, pricing, and distribution

Table Of Contents

1. Introduction

- 1.1 Scope of the Study

- 1.2 The Insight Partners Research Report Guidance

- 1.3 Market Segmentation

- 1.3.1 North America Surgical Stapling Devices Market - by Product

- 1.3.2 North America Surgical Stapling Devices Market - by Type

- 1.3.3 North America Surgical Stapling Devices Market - by Application

- 1.3.4 North America Surgical Stapling Devices Market - by End User

- 1.3.5 North America Surgical Stapling Devices Market - by Country

2. North America Surgical Stapling Devices Market - Key Takeaways

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Surgical Stapling Devices Market - Market Landscape

- 4.1 Overview

- 4.2 North America PEST Analysis

- 4.3 Expert's Opinion

5. North America Surgical Stapling Devices Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increase in Wounds and Surgical Procedures

- 5.1.2 Launch of New Products and Strategic Collaborations Between Companies

- 5.2 Market Restraints

- 5.2.1 Product Recalls and High Device Costs

- 5.3 Market Opportunities

- 5.3.1 Surging Popularity of Cosmetic Surgery and Growth in Medical Tourism in Developing Countries

- 5.4 Future Trends

- 5.4.1 Technological Advancements

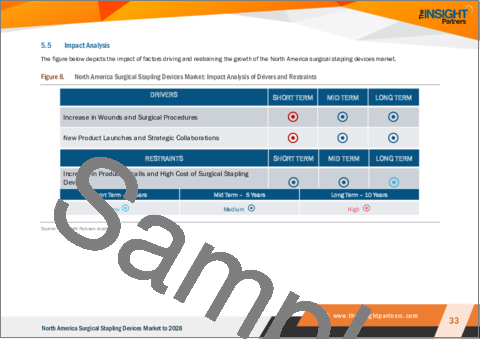

- 5.5 Impact Analysis

6. Surgical Stapling Devices Market - North America Analysis

- 6.1 North America Surgical Stapling Devices Market Revenue Forecast and Analysis

7. North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 - by Product

- 7.1 Overview

- 7.2 North America Surgical Stapling Devices Market Revenue Share, by Product 2021 & 2028 (%)

- 7.3 Powered Surgical Staplers

- 7.3.1 Overview

- 7.3.2 Powered Surgical Staplers: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- 7.4 Manual Surgical Staplers

- 7.4.1 Overview

- 7.4.2 Manual Surgical Staplers: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

8. North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 - by Type

- 8.1 Overview

- 8.2 North America Surgical Stapling Devices Market Revenue Share, by Type 2021 & 2028 (%)

- 8.3 Disposable Surgical Staplers

- 8.3.1 Overview

- 8.3.2 Disposable Surgical Staplers: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- 8.4 Reusable Surgical Staplers

- 8.4.1 Overview

- 8.4.2 Reusable Surgical Staplers: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

9. North America Surgical Stapling Devices Market Analysis and Forecast to 2028 - by Application

- 9.1 Overview

- 9.2 North America Surgical Stapling Devices Market, by Application 2021 & 2028 (%)

- 9.3 Orthopedic Surgery

- 9.3.1 Overview

- 9.3.2 Orthopedic Surgery: North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4 Endoscopic Surgery

- 9.4.1 Overview

- 9.4.2 Endoscopic Surgery: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- 9.5 Cardiac and Thoracic Surgery

- 9.5.1 Overview

- 9.5.2 Cardio and Thoracic Surgery: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- 9.6 Abdominal and Pelvic Surgery

- 9.6.1 Overview

- 9.6.2 Abdominal and Pelvic Surgery: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- 9.7 Others

- 9.7.1 Overview

- 9.7.2 Others: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

10. North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 - by End User

- 10.1 Overview

- 10.2 North America Surgical Stapling Devices Market Revenue Share, by End User 2021 & 2028 (%)

- 10.3 Hospitals

- 10.3.1 Overview

- 10.3.2 Hospitals: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

- 10.4 Ambulatory Surgical Centers

- 10.4.1 Overview

- 10.4.2 Ambulatory Surgical Centers: Surgical Stapling Devices Market - Revenue and Forecast to 2028 (US$ Million)

11. North America Surgical Stapling Devices Market - Revenue and Forecast to 2028 - Country Analysis

- 11.1 Overview

- 11.1.1 North America: Surgical Stapling Devices Market, by Country, 2021 & 2028 (%)

- 11.1.1.1 United States: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- 11.1.1.1.1 Overview

- 11.1.1.1.2 United States: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- 11.1.1.1.3 United States: Surgical Stapling Devices Market, by Product, 2019-2028 (USD Million)

- 11.1.1.1.4 United States: Surgical Stapling Devices Market, by Type, 2019-2028 (USD Million)

- 11.1.1.1.5 United States: Surgical Stapling Devices Market, by Application, 2019-2028 (USD Million)

- 11.1.1.1.6 United States: Surgical Stapling Devices Market, by End User, 2019-2028 (USD Million)

- 11.1.1.2 Canada: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- 11.1.1.2.1 Overview

- 11.1.1.2.2 Canada: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- 11.1.1.2.3 Canada: Surgical Stapling Devices Market, by Product, 2019-2028 (USD Million)

- 11.1.1.2.4 Canada: Surgical Stapling Devices Market, by Type, 2019-2028 (USD Million)

- 11.1.1.2.5 Canada: Surgical Stapling Devices Market, by Application, 2019-2028 (USD Million)

- 11.1.1.2.6 Canada: Surgical Stapling Devices Market, by End User, 2019-2028 (USD Million)

- 11.1.1.3 Mexico: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- 11.1.1.3.1 Overview

- 11.1.1.3.2 Mexico: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- 11.1.1.3.3 Mexico: Surgical Stapling Devices Market, by Product, 2019-2028 (USD Million)

- 11.1.1.3.4 Mexico: Surgical Stapling Devices Market, by Type, 2019-2028 (USD Million)

- 11.1.1.3.5 Mexico: Surgical Stapling Devices Market, by Application, 2019-2028 (USD Million)

- 11.1.1.3.6 Mexico: Surgical Stapling Devices Market, by End User, 2019-2028 (USD Million)

- 11.1.1.1 United States: Surgical Stapling Devices Market - Revenue and forecast to 2028 (USD Million)

- 11.1.1 North America: Surgical Stapling Devices Market, by Country, 2021 & 2028 (%)

12. North America Surgical Stapling Devices Market-Industry Landscape

- 12.1 Overview

- 12.2 Organic Growth Strategies

- 12.2.1 Overview

13. Company Profiles

- 13.1 Intuitive Surgical Inc

- 13.1.1 Key Facts

- 13.1.2 Business Description

- 13.1.3 Products and Services

- 13.1.4 Financial Overview

- 13.1.5 SWOT Analysis

- 13.1.6 Key Developments

- 13.2 Medtronic Plc

- 13.2.1 Key Facts

- 13.2.2 Business Description

- 13.2.3 Products and Services

- 13.2.4 Financial Overview

- 13.2.5 SWOT Analysis

- 13.2.6 Key Developments

- 13.3 Ethicon USA LLC

- 13.3.1 Key Facts

- 13.3.2 Business Description

- 13.3.3 Products and Services

- 13.3.4 Financial Overview

- 13.3.5 SWOT Analysis

- 13.3.6 Key Developments

- 13.5 B. Braun SE

- 13.5.1 Key Facts

- 13.5.2 Business Description

- 13.5.3 Products and Services

- 13.5.4 Financial Overview

- 13.5.5 SWOT Analysis

- 13.5.6 Key Developments

- 13.6 Conmed Corp

- 13.6.1 Key Facts

- 13.6.2 Business Description

- 13.6.3 Products and Services

- 13.6.4 Financial Overview

- 13.6.5 SWOT Analysis

- 13.6.6 Key Developments

- 13.7 3M Co

- 13.7.1 Key Facts

- 13.7.2 Business Description

- 13.7.3 Products and Services

- 13.7.4 Financial Overview

- 13.7.5 SWOT Analysis

- 13.7.6 Key Developments

14. Appendix

- 14.1 About The Insight Partners

- 14.2 Glossary of Terms