|

|

市場調査レポート

商品コード

1755917

ナイロン66市場の2032年までの予測:グレード別、販売チャネル別、用途別、地域別の世界分析Nylon 66 Market Forecasts to 2032 - Global Analysis By Grade (Fiber Grade, Resin Grade, Standard Grade, Heat Stabilized Grade and Other Grades), Sales Channel, Application and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ナイロン66市場の2032年までの予測:グレード別、販売チャネル別、用途別、地域別の世界分析 |

|

出版日: 2025年06月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、ナイロン66の世界市場は2025年に61億米ドルを占め、予測期間中のCAGRは3.7%で、2032年には78億米ドルに達する見込みです。

ナイロン66は、ヘキサメチレンジアミンとアジピン酸から縮合重合法で作られる合成ポリマーです。高い機械強度、耐熱性、耐久性で知られ、自動車、繊維、電気、工業用途に広く使用されています。ナイロン66は、耐摩耗性、化学的安定性、寸法安定性に優れ、要求の厳しいエンジニアリング用途や性能重視の用途に適しています。また、剛性と耐摩耗性も評価されています。

米国DOEの商業可能性評価報告書によると、2018年の世界のナイロン66供給には約38億ポンドのアジポニトリル原料が必要でした。

自動車分野での高い需要

自動車産業は、ナイロン66の高い引張強度、耐熱性、耐久性を生かし、ナイロン66市場の主要促進要因となっています。自動車メーカーは、軽量部品の製造にナイロン66を使用することが増えており、これにより車両全体の重量を減らし、重量を10%減らすごとに燃費を5~7%も向上させることができます。ナイロン66の用途は、エンジン部品や燃料システムから電気コネクターや車室内装まで多岐にわたる。さらに、電気自動車へのシフトは、バッテリーモジュールや配線システムでの使用を拡大し、高性能で軽量なプラスチックの需要拡大を支えています。

不安定な原料価格

特に石油化学製品に由来するヘキサメチレンジアミンとアジピン酸の原料価格の変動は、大きな抑制要因となっています。原油価格の変動はこれらの原料の生産コストに直接影響し、生産者の製造経費と利益率に不確実性をもたらします。このような価格の不安定さは、メーカーが安定した価格設定を維持することを困難にし、サプライ・チェーンを混乱させ、価格に敏感な産業が予測可能なコスト効果の高い代替材料を求めるきっかけとなります。

材料工学の進歩

技術革新により、強度、熱安定性、耐摩耗性などの材料特性が向上し、航空宇宙や3Dプリンティングなどの高性能用途での使用が拡大しています。さらに、持続可能性が重視されるようになり、バイオベースやリサイクル可能なナイロン66の研究開発が推進されています。これらの環境にやさしい代替品は、より厳しい環境規制や企業の持続可能性目標に合致しており、新たな市場ニッチと用途を開拓しています。

厳しい環境規制

合成ポリマーは化石燃料に由来するため、ナイロン66はプラスチック汚染と炭素排出の一因となり、生分解性でないため廃棄処理も複雑になります。規制圧力と社会意識の高まりが、より環境に優しい生分解性代替品へと産業を押し上げています。この動向は、メーカーが持続可能な生産慣行やリサイクル技術に投資することを課題としており、初期費用がかさみ、競争上の位置づけに影響を与える可能性があります。

COVID-19の影響:

COVID-19の流行は、ナイロン66市場にさまざまな影響を与えました。当初は、サプライチェーンの混乱、製造施設の一時的な操業停止、自動車や繊維製品などの主要セクターからの需要の急激な減少により、市場はマイナスの影響を受けた。しかし、パンデミックは個人用保護具(PPE)の需要急増という好材料も生み出しました。フェイスマスク、医療用ガウン、その他の繊維製品へのニーズの高まりが、高機能ナイロン66繊維の消費を押し上げました。

予測期間中、樹脂グレードが最大になる見込み

樹脂グレード分野は、高性能エンジニアリング・プラスチックとして幅広い用途があるため、予測期間中最大の市場シェアを占めると予想されます。自動車、配電、消費財、包装フィルムなど、多様な産業で広く使用されています。この素材固有の強度、耐久性、熱安定性により、電化製品や自動車部品の製造に理想的な選択肢となっています。さらに、その汎用性により、成形プロセスと押出プロセスの両方で使用することができ、幅広い産業ニーズに応えることができます。

予測期間中、電気・電子分野が最も高いCAGRが見込まれる

予測期間中、電気・電子分野が最も高い成長率を示すと予測されます。これは、ナイロン66の優れた電気絶縁特性、耐熱性、機械的強度が、コネクター、絶縁体、回路基板などの部品に理想的な特性をもたらしているためです。電子製品の生産増加、自動車産業における電化の進展、5Gインフラの世界の拡大が需要を大きく促進しています。さらに、スマート・デバイスや再生可能エネルギー・システムへの応用が、その重要性を高めています。

最大シェアの地域:

予測期間中、アジア太平洋地域が最大の市場シェアを占めると予想されるが、これは同地域の急速な工業化と、特に中国やインドのような国々における世界の製造拠点としての位置づけに後押しされたものです。拡大する自動車、エレクトロニクス、繊維産業がナイロン66の主要消費者です。さらに、競争力のある人件費、強固なサプライ・チェーン、可処分所得の増加、産業の成長を促進する政府の取り組みといった要因が、この地域の重要な市場地位を支えています。

CAGRが最も高い地域:

予測期間中、アジア太平洋地域が最も高いCAGRを示すと予測されます。同地域の急速な経済成長、都市化、製造基盤の拡大が、この高成長を牽引する主な要因です。特に中国やインドのような新興経済圏では、自動車、繊維、電気・電子といったエンドユーザー産業からの需要が旺盛で伸びており、市場の推進力となっています。さらに、インフラ開発への投資の増加や、耐久性のある高性能商品に対する消費者の需要の高まりが、ナイロン66の消費をさらに加速させています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査資料

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 用途分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のナイロン66市場:グレード別

- 繊維グレード

- 樹脂グレード

- 標準グレード

- 熱安定化グレード

- その他のグレード

第6章 世界のナイロン66市場:販売チャネル別

- 直接販売

- 間接販売

第7章 世界のナイロン66市場:用途別

- 自動車

- 電気・電子

- テキスタイル・アパレル

- 産業機械

- パッケージ

- カーペット

- 消費財・家電製品

- その他の用途

第8章 世界のナイロン66市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、ジョイントベンチャー

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイリング

- BASF SE

- DuPont de Nemours, Inc.

- Ascend Performance Materials

- Lanxess AG

- Solvay S.A.

- Evonik Industries AG

- Toray Industries, Inc.

- Mitsubishi Chemical Holdings Corporation

- RadiciGroup

- Huntsman Corporation

- Celanese Corporation

- Kuraray Co., Ltd.

- China National Chemical Corporation(ChemChina)

- Reliance Industries Limited

- Arkema S.A.

- China Petrochemical Corporation(Sinopec)

- Dairen Chemical Corporation

List of Tables

- Table 1 Global Nylon 66 Market Outlook, By Region (2024-2032) ($MN)

- Table 2 Global Nylon 66 Market Outlook, By Grade (2024-2032) ($MN)

- Table 3 Global Nylon 66 Market Outlook, By Fiber Grade (2024-2032) ($MN)

- Table 4 Global Nylon 66 Market Outlook, By Resin Grade (2024-2032) ($MN)

- Table 5 Global Nylon 66 Market Outlook, By Standard Grade (2024-2032) ($MN)

- Table 6 Global Nylon 66 Market Outlook, By Heat Stabilized Grade (2024-2032) ($MN)

- Table 7 Global Nylon 66 Market Outlook, By Other Grades (2024-2032) ($MN)

- Table 8 Global Nylon 66 Market Outlook, By Sales Channel (2024-2032) ($MN)

- Table 9 Global Nylon 66 Market Outlook, By Direct Sales (2024-2032) ($MN)

- Table 10 Global Nylon 66 Market Outlook, By Indirect Sales (2024-2032) ($MN)

- Table 11 Global Nylon 66 Market Outlook, By Application (2024-2032) ($MN)

- Table 12 Global Nylon 66 Market Outlook, By Automotive (2024-2032) ($MN)

- Table 13 Global Nylon 66 Market Outlook, By Electrical & Electronics (2024-2032) ($MN)

- Table 14 Global Nylon 66 Market Outlook, By Textile & Apparel (2024-2032) ($MN)

- Table 15 Global Nylon 66 Market Outlook, By Industrial & Machinery (2024-2032) ($MN)

- Table 16 Global Nylon 66 Market Outlook, By Packaging (2024-2032) ($MN)

- Table 17 Global Nylon 66 Market Outlook, By Carpets (2024-2032) ($MN)

- Table 18 Global Nylon 66 Market Outlook, By Consumer Goods & Appliances (2024-2032) ($MN)

- Table 19 Global Nylon 66 Market Outlook, By Other Applications (2024-2032) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Nylon 66 Market is accounted for $6.1 billion in 2025 and is expected to reach $7.8 billion by 2032 growing at a CAGR of 3.7% during the forecast period. Nylon 66 is a synthetic polymer made from hexamethylenediamine and adipic acid through a condensation polymerization process. It is known for its high mechanical strength, heat resistance, and durability and is widely used in automotive, textile, electrical, and industrial applications. Nylon 66 offers excellent wear resistance, chemical stability, and dimensional integrity, making it suitable for demanding engineering and performance-based uses. It is also valued for its stiffness and abrasion resistance.

According to a U.S. DOE Commercial Potential Evaluation report, the global Nylon 66 supply in 2018 required approximately 3.8 billion pounds of adiponitrile feedstock.

Market Dynamics:

Driver:

High demand in automotive sector

The automotive industry is a primary driver for the Nylon 66 market, leveraging the material's high tensile strength, heat resistance, and durability. Automakers increasingly use Nylon 66 to manufacture lightweight components, which helps reduce overall vehicle weight and improve fuel efficiency by as much as 5-7% for every 10% reduction in weight. Its applications are diverse, ranging from engine components and fuel systems to electrical connectors and cabin interiors. Furthermore, the shift towards electric vehicles expands its use in battery modules and wiring systems, supporting the growing demand for high-performance, lightweight plastics.

Restraint:

Volatile raw material prices

The volatility of raw material prices, particularly for hexamethylene diamine and adipic acid, which are derived from petrochemicals, is a significant restraint. Fluctuations in crude oil prices directly impact the production costs of these inputs, creating uncertainty in manufacturing expenses and profit margins for producers. This price instability makes it difficult for manufacturers to maintain stable pricing, which can disrupt supply chains and lead price-sensitive industries to seek more cost-effective alternative materials with predictable costs.

Opportunity:

Advancements in material engineering

Innovations are enhancing material properties like strength, thermal stability, and wear resistance, broadening its use in high-performance applications such as aerospace and 3D printing. Additionally, the growing emphasis on sustainability is driving R&D toward bio-based and recyclable Nylon 66 variants. These eco-friendly alternatives align with stricter environmental regulations and corporate sustainability goals, opening up new market niches and applications.

Threat:

Stringent environmental regulations

Synthetic polymer is derived from fossil fuels, as a result, Nylon 66 contributes to plastic pollution and carbon emissions, and its non-biodegradable nature complicates disposal. Increasing regulatory pressure and public awareness are pushing industries toward greener, biodegradable alternatives. This trend challenges manufacturers to invest in sustainable production practices and recycling technologies, which can incur high initial costs and potentially impact their competitive positioning.

Covid-19 Impact:

The COVID-19 pandemic had a mixed impact on the Nylon 66 market. Initially, the market experienced a negative effect due to widespread supply chain disruptions, temporary shutdowns of manufacturing facilities, and a sharp decline in demand from key sectors like automotive and textiles. However, the pandemic also created positive momentum through a surge in demand for personal protective equipment (PPE). The increased need for face masks, medical gowns, and other textiles boosted the consumption of high-performance Nylon 66 fibers.

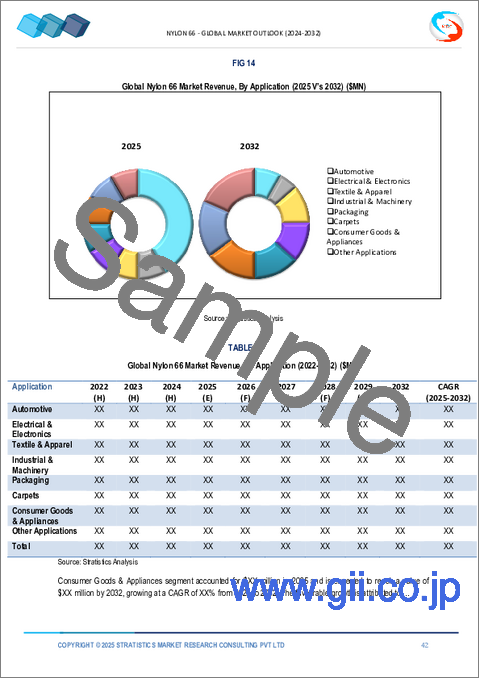

The resin grade segment is expected to be the largest during the forecast period

The resin grade segment is expected to account for the largest market share during the forecast period due to its extensive application as a high-performance engineering plastic. It is widely used across diverse industries, including automotive, electrical power distribution, consumer goods, and packaging films. The material's inherent strength, durability, and thermal stability make it an ideal choice for manufacturing appliance and automotive parts. Additionally, its versatility allows for its use in both molding and extrusion processes, catering to a broad spectrum of industrial needs.

The electrical & electronics segment is expected to have the highest CAGR during the forecast period

Over the forecast period, the electrical & electronics segment is predicted to witness the highest growth rate, driven by Nylon 66's excellent electrical insulating properties, heat resistance, and mechanical strength, making it ideal for components like connectors, insulators, and circuit boards. The increasing production of electronic products, growing electrification in the automotive industry, and the global expansion of 5G infrastructure are significantly fueling demand. Furthermore, its application in smart devices and renewable energy systems reinforces its growing importance.

Region with largest share:

During the forecast period, the Asia Pacific region is expected to hold the largest market share, fueled by the region's rapid industrialization and its position as a global manufacturing hub, particularly in countries like China and India. The expanding automotive, electronics, and textile industries are major consumers of Nylon 66. Furthermore, factors such as competitive labor costs, robust supply chains, rising disposable incomes, and government initiatives promoting industrial growth contribute to the region's significant market position.

Region with highest CAGR:

Over the forecast period, the Asia Pacific region is anticipated to exhibit the highest CAGR. The region's rapid economic growth, urbanization, and expanding manufacturing base are key factors driving this high growth. Strong and growing demand from end-user industries such as automotive, textiles, and electrical & electronics, especially in emerging economies like China and India, propels the market forward. Additionally, increasing investments in infrastructure development and a rising consumer demand for durable, high-performance goods further accelerate the consumption of Nylon 66.

Key players in the market

Some of the key players in Nylon 66 Market include BASF SE, DuPont de Nemours, Inc., Ascend Performance Materials, Lanxess AG, Solvay S.A., Evonik Industries AG, Toray Industries, Inc., Mitsubishi Chemical Holdings Corporation, RadiciGroup, Huntsman Corporation, Celanese Corporation, Kuraray Co., Ltd., China National Chemical Corporation (ChemChina), Reliance Industries Limited, Arkema S.A., China Petrochemical Corporation (Sinopec), and Dairen Chemical Corporation.

Key Developments:

In May 2025, BASF announced its intention to acquire the remaining 49% share of the Alsachimie joint venture from DOMO Chemicals, which would give BASF 100% ownership. This move is aimed at strengthening BASF's production of polyamide (PA) 6.6 precursors, such as adipic acid and hexamethylenediamine adipate (AH salt), at its European hub in Chalampe, France. The transaction is expected to close by mid-2025.

In March 2025, Evonik announced it signed an agreement to license its hydrogen peroxide (H2O2) production technology to China Pingmei Shenma Group Nylon Technology (Shenma). Shenma is a major producer within the nylon 6 and nylon 66 value chains. The H2O2 from the new plant will be used to produce caprolactam, a precursor for nylon 6.

In November 2023, Solvay launched Rhodianyl(R) 27CR70N, a polyamide 6.6 polymer made from 100% pre-consumer recycled content that has achieved SCS Recycled Content Certification. This product is manufactured at the company's plant in Santo Andre, Brazil, as part of its integrated polyamide chain in Latin America.

Grades Covered:

- Fiber Grade

- Resin Grade

- Standard Grade

- Heat Stabilized Grade

- Other Grades

Sales Channels Covered:

- Direct Sales

- Indirect Sales

Applications Covered:

- Automotive

- Electrical & Electronics

- Textile & Apparel

- Industrial & Machinery

- Packaging

- Carpets

- Consumer Goods & Appliances

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2024, 2025, 2026, 2028, and 2032

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Nylon 66 Market, By Grade

- 5.1 Introduction

- 5.2 Fiber Grade

- 5.3 Resin Grade

- 5.4 Standard Grade

- 5.5 Heat Stabilized Grade

- 5.6 Other Grades

6 Global Nylon 66 Market, By Sales Channel

- 6.1 Introduction

- 6.2 Direct Sales

- 6.3 Indirect Sales

7 Global Nylon 66 Market, By Application

- 7.1 Introduction

- 7.2 Automotive

- 7.3 Electrical & Electronics

- 7.4 Textile & Apparel

- 7.5 Industrial & Machinery

- 7.6 Packaging

- 7.7 Carpets

- 7.8 Consumer Goods & Appliances

- 7.9 Other Applications

8 Global Nylon 66 Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 BASF SE

- 10.2 DuPont de Nemours, Inc.

- 10.3 Ascend Performance Materials

- 10.4 Lanxess AG

- 10.5 Solvay S.A.

- 10.6 Evonik Industries AG

- 10.7 Toray Industries, Inc.

- 10.8 Mitsubishi Chemical Holdings Corporation

- 10.9 RadiciGroup

- 10.10 Huntsman Corporation

- 10.11 Celanese Corporation

- 10.12 Kuraray Co., Ltd.

- 10.13 China National Chemical Corporation (ChemChina)

- 10.14 Reliance Industries Limited

- 10.15 Arkema S.A.

- 10.16 China Petrochemical Corporation (Sinopec)

- 10.17 Dairen Chemical Corporation