|

|

市場調査レポート

商品コード

1662713

固定無線アクセス市場の2030年までの予測: コンポーネント別、サービスプロバイダー別、展開タイプ別、周波数帯域別、技術別、エンドユーザー別、地域別の世界分析Fixed Wireless Access Market Forecasts to 2030 - Global Analysis By Component (Hardware, Software and Services), Service Provider, Deployment Type, Frequency Band, Technology, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 固定無線アクセス市場の2030年までの予測: コンポーネント別、サービスプロバイダー別、展開タイプ別、周波数帯域別、技術別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2025年02月02日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の固定無線アクセス市場は2024年に1,749億1,000万米ドルを占め、予測期間中のCAGRは21.8%で、2030年には5,711億米ドルに達すると予測されています。

固定無線アクセス(FWA)は、一般的に光ファイバーや銅線ケーブルのような従来の有線インフラの代わりに無線信号を使用し、無線接続を介して家庭や企業に配信される高速インターネットサービスです。FWAは、特定の場所に設置された固定無線送信機を通じてエンドユーザーをインターネットに接続するもので、多くの場合、4G、5G、その他の無線技術を利用します。このサービスは、ケーブル敷設が現実的でない地域にとって、費用対効果が高く、より高速な代替手段であり、各ユーザーに物理的なケーブルを敷設することなく、信頼性の高いブロードバンドを記載しています。

高速インターネットへの需要の高まり

固定無線アクセスは、従来のブロードバンドオプションに代わる選択肢を提供し、遠隔地やサービスが十分でない地域にとって費用対効果の高いソリューションとなります。5G技術の普及に伴い、FWAは高速化と低遅延化の恩恵を受けています。リモートワーク、オンライン学習、ストリーミングサービスへのシフトは、信頼性の高いインターネット接続への需要をさらに加速させています。政府や通信事業者は、データ消費の急増に対応するため、FWAネットワークの拡大に投資しています。この動向は今後も続き、世界中でFWAソリューションの採用を後押しすると予想されます。

光ファイバーやケーブル・ネットワークとの競合

光ファイバー・ネットワークは、より広帯域で高速かつ信頼性の高い接続を提供するため、より高速なインターネットを求める消費者にとって魅力的です。ケーブル・ネットワークも、一般的に高価ではあるが、安定した高速ブロードバンドサービスを提供しています。こうした従来の選択肢は、特に都市部ではFWA市場の影に隠れがちです。その結果、消費者は確立されたファイバーやケーブルの選択肢を好み、ワイヤレスソリューションの採用を減らす可能性があります。このような競争により、FWAプロバイダーは競合価格設定と性能向上を提供し、顧客を引きつける必要に迫られています。

IoT機器との統合

IoT機器との統合には安定した高速ネットワークが必要だが、FWAソリューションは特に従来のブロードバンドインフラが不足している地域でこれを提供できます。スマートシティや産業オートメーションなど、より多くのIoTアプリケーションが登場するにつれ、信頼性の高い無線ブロードバンドへの需要が高まっています。FWA技術は低遅延で広帯域のサービスを提供するため、多数のIoTデバイスを同時に接続するのに理想的です。この統合は、接続されたデバイス間のシームレスな通信とデータ交換をサポートし、運用効率を向上させています。全体として、IoTとFWAの相乗効果は、複数のセクターにわたるデジタルトランスフォーメーションを加速し、市場拡大を促進します。

技術の陳腐化

より高速で信頼性の高いインターネット接続へのニーズは高まっており、古いシステムでは新しく改良された技術に対応することが難しくなっています。その結果、サービス品質に格差が生じるため、企業は改善を迫られるか、市場での存在感が薄れるかのどちらかです。さらに、技術の開発は非常に速いため、通信事業者は定期的に新しいインフラに高額な投資を行わなければならない可能性があります。古いFWA機器は時折、より新しいモデルやネットワークプロトコルと互換性がなくなり、その有用性が低下することがあります。次世代技術の採用は消費者の期待をさらに高め、古くなったFWAシステムの競合を低下させています。

COVID-19の影響

COVID-19の大流行は、リモートワーク、教育、オンラインサービスの急増に伴い、固定無線アクセス(FWA)の需要を大幅に加速させました。デジタルプラットフォームへの依存度が高まる中、多くの地域で信頼性の高いインターネットソリューションが求められ、FWA配備の成長が促進されました。パンデミックは既存のブロードバンドインフラの限界を露呈し、政府も民間セクターもFWA技術への投資を促しました。FWAプロバイダー、特に5Gベースのサービスを提供するプロバイダーは、より高速で信頼性の高いインターネットを提供できる可能性があるため、需要が増加しました。しかし、サプライチェーンの混乱や景気減速といった課題が、短期的には市場の成長軌道に影響を与えました。

予測期間中はハードウェアセグメントが最大になる見込み

ハードウェアセグメントは、高速インターネット接続に必要なインフラのため、予測期間中に最大の市場シェアを占めると予想されます。ルーター、アンテナ、ワイヤレスゲートウェイはFWA展開に不可欠であり、安定した信頼性の高いパフォーマンスを保証します。サービスが行き届いていない地域でのブロードバンド需要の高まりが、費用対効果の高いFWAハードウェアソリューションの採用を後押ししています。5G技術の進歩に伴い、FWAハードウェアのアップグレードにより、消費者向けの高速化と低遅延が可能になります。先進的なチップセットやアンテナ設計などのハードウェアの革新は、信号品質とカバレッジを向上させます。このハードウェアの進化は、FWAネットワークのスケーラビリティをサポートし、データ集約型アプリケーションのニーズの高まりに対応します。

予測期間中、CAGRが最も高くなるのは中小企業セグメント

予測期間中、手頃な価格でスケーラブルなインターネットソリューションを求める中小企業セグメントが最も高い成長率を示すと予測されます。FWAは、特に光ファイバーや有線接続が実現不可能な地域において、従来のブロードバンドサービスに代わるコスト効率の高い選択肢をこれらの企業に記載しています。中小企業は、ダウンタイムを最小限に抑え、設置コストを削減できるFWAの迅速な展開から恩恵を受けます。デジタル化が進む中、中小企業は業務に高速で信頼性の高いインターネットを必要としており、FWAは魅力的な選択肢となっています。地方や未開拓の地域でもカバレッジを拡大できることも重要な要素で、中小企業はこれまでアクセスできなかった市場に参入できます。

最大のシェアを占める地域

予測期間中、高速インターネットと手頃な価格のブロードバンドソリューションに対する需要の高まりから、アジア太平洋が最大の市場シェアを占めると予想されます。FWAは、4Gと5Gネットワークの成長に伴い、サービスが行き届いていない地域や農村部において、従来の有線インターネットに代わる有力な選択肢として台頭しています。FWAの導入は、中国、日本、インドといった国々の政府によって、デジタル変革への取り組みの一環として支援されています。スマートシティの出現や、クラウドベースのサービスやIoTへの依存度の高まりも、この産業を支える要因となっています。信頼性が高く高速なインターネット接続への高まるニーズを満たすため、このセグメントの大手企業は5G FWAなどの最先端技術に投資しています。T

CAGRが最も高い地域

予測期間中、南米地域が最も高いCAGRを示すと予想されるが、これは都市部と農村部の両方で高速インターネット接続に対する需要が増加しているためです。通信事業者は、サービスが行き届いていない地域にブロードバンドサービスを提供するためにFWAネットワークを急速に拡大しており、大規模な光ファイバーインフラの必要性を減らしています。ブラジル、アルゼンチン、コロンビアは、4Gと5Gネットワークに多額の投資を行い、FWA導入の先頭を走っています。リモートワークやデジタルサービスの人気の高まりは、信頼性が高く費用対効果の高いブロードバンドソリューションの需要をさらに押し上げています。市場の主要参入企業は、手頃な価格のインターネット包装と革新的なFWA技術を提供し、市場シェアを獲得することに注力しています。

無料のカスタマイズ提供

本レポートをご購読の顧客には、以下の無料カスタマイズオプションのいずれかを提供いたします。

- 企業プロファイル

- 追加市場参入企業の包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推定・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携による主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- イントロダクション

- 促進要因

- 抑制要因

- 機会

- 脅威

- 技術分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の固定無線アクセス市場:コンポーネント別

- イントロダクション

- ハードウェア

- 顧客構内設備(CPE)

- ワイヤレスルーター

- アンテナ

- 基地局

- ソフトウェア

- ネットワーク管理ソフトウェア

- セキュリティソフトウェア

- サービス

- インストール

- メンテナンス

- コンサルティング

- マネージドサービス

第6章 世界の固定無線アクセス市場:サービスプロバイダー別

- イントロダクション

- 通信事業者

- ケーブル事業者

- インターネットサービスプロバイダー(ISP)

- その他

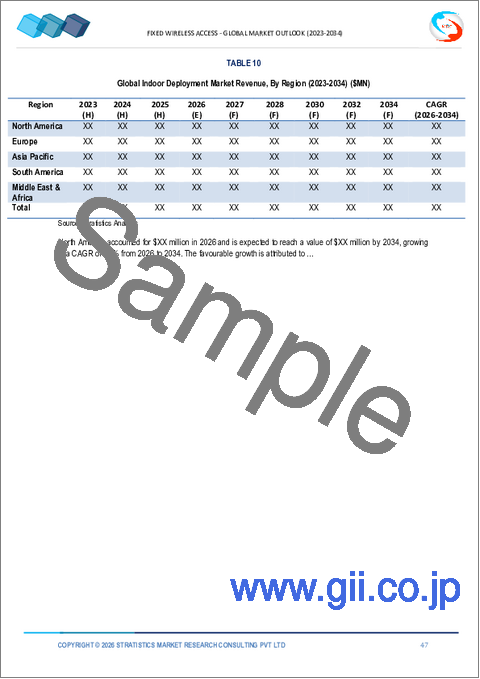

第7章 世界の固定無線アクセス市場:展開タイプ別

- イントロダクション

- 屋外展開

- 屋内展開

第8章 世界の固定無線アクセス市場:周波数帯域別

- イントロダクション

- 6GHz以下

- 6GHz以上

- ミリ波(mmWave)

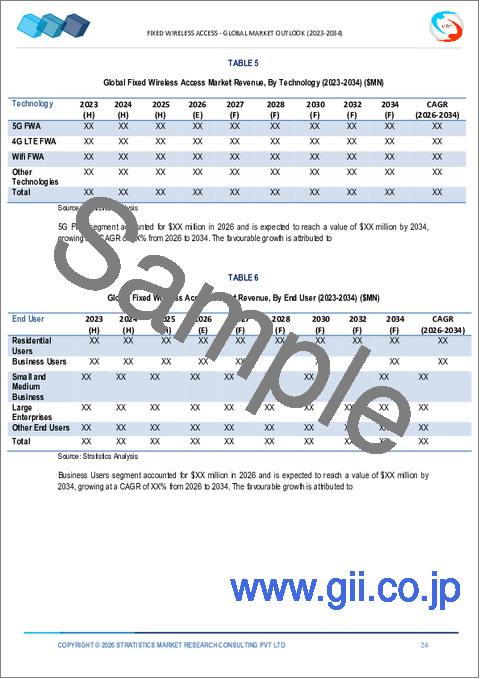

第9章 世界の固定無線アクセス市場:技術別

- イントロダクション

- 5Gワイヤレス

- 4G LTE FWA

- Wi-Fi FWA

- その他

第10章 世界の固定無線アクセス市場:エンドユーザー別

- イントロダクション

- 住宅ユーザー

- ビジネスユーザー

- 中小企業

- 大企業

- その他

第11章 世界の固定無線アクセス市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他のアジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他の中東・アフリカ

第12章 主要開発

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第13章 企業プロファイリング

- Huawei Technologies Co., Ltd.

- Ericsson AB

- Nokia Corporation

- ZTE Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems, Inc.

- Qualcomm Technologies, Inc.

- Intel Corporation

- Cradlepoint

- Cambium Networks, Inc.

- Airspan Networks, Inc.

- Redline Communications Inc.

- Altiostar Networks, Inc.

- Commscope Holding Company, Inc.

- T-Mobile USA, Inc.

- Verizon Communications Inc.

- AT&T Inc.

- BT Group plc

List of Tables

- Table 1 Global Fixed Wireless Access Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Fixed Wireless Access Market Outlook, By Component (2022-2030) ($MN)

- Table 3 Global Fixed Wireless Access Market Outlook, By Hardware (2022-2030) ($MN)

- Table 4 Global Fixed Wireless Access Market Outlook, By Customer Premises Equipment (CPE) (2022-2030) ($MN)

- Table 5 Global Fixed Wireless Access Market Outlook, By Wireless Routers (2022-2030) ($MN)

- Table 6 Global Fixed Wireless Access Market Outlook, By Antennas (2022-2030) ($MN)

- Table 7 Global Fixed Wireless Access Market Outlook, By Base Stations (2022-2030) ($MN)

- Table 8 Global Fixed Wireless Access Market Outlook, By Software (2022-2030) ($MN)

- Table 9 Global Fixed Wireless Access Market Outlook, By Network Management Software (2022-2030) ($MN)

- Table 10 Global Fixed Wireless Access Market Outlook, By Security Software (2022-2030) ($MN)

- Table 11 Global Fixed Wireless Access Market Outlook, By Services (2022-2030) ($MN)

- Table 12 Global Fixed Wireless Access Market Outlook, By Installation (2022-2030) ($MN)

- Table 13 Global Fixed Wireless Access Market Outlook, By Maintenance (2022-2030) ($MN)

- Table 14 Global Fixed Wireless Access Market Outlook, By Consulting (2022-2030) ($MN)

- Table 15 Global Fixed Wireless Access Market Outlook, By Managed Services (2022-2030) ($MN)

- Table 16 Global Fixed Wireless Access Market Outlook, By Service Provider (2022-2030) ($MN)

- Table 17 Global Fixed Wireless Access Market Outlook, By Telecom Operators (2022-2030) ($MN)

- Table 18 Global Fixed Wireless Access Market Outlook, By Cable Operators (2022-2030) ($MN)

- Table 19 Global Fixed Wireless Access Market Outlook, By Internet Service Providers (ISPs) (2022-2030) ($MN)

- Table 20 Global Fixed Wireless Access Market Outlook, By Other Service Providers (2022-2030) ($MN)

- Table 21 Global Fixed Wireless Access Market Outlook, By Deployment Type (2022-2030) ($MN)

- Table 22 Global Fixed Wireless Access Market Outlook, By Outdoor Deployment (2022-2030) ($MN)

- Table 23 Global Fixed Wireless Access Market Outlook, By Indoor Deployment (2022-2030) ($MN)

- Table 24 Global Fixed Wireless Access Market Outlook, By Frequency Band (2022-2030) ($MN)

- Table 25 Global Fixed Wireless Access Market Outlook, By Sub 6 GHz (2022-2030) ($MN)

- Table 26 Global Fixed Wireless Access Market Outlook, By Above 6 GHz (2022-2030) ($MN)

- Table 27 Global Fixed Wireless Access Market Outlook, By Millimeter Wave (mmWave) (2022-2030) ($MN)

- Table 28 Global Fixed Wireless Access Market Outlook, By Technology (2022-2030) ($MN)

- Table 29 Global Fixed Wireless Access Market Outlook, By 5G FWA (2022-2030) ($MN)

- Table 30 Global Fixed Wireless Access Market Outlook, By 4G LTE FWA (2022-2030) ($MN)

- Table 31 Global Fixed Wireless Access Market Outlook, By Wi-Fi FWA (2022-2030) ($MN)

- Table 32 Global Fixed Wireless Access Market Outlook, By Other technologies (2022-2030) ($MN)

- Table 33 Global Fixed Wireless Access Market Outlook, By End User (2022-2030) ($MN)

- Table 34 Global Fixed Wireless Access Market Outlook, By Residential Users (2022-2030) ($MN)

- Table 35 Global Fixed Wireless Access Market Outlook, By Business Users (2022-2030) ($MN)

- Table 36 Global Fixed Wireless Access Market Outlook, By Small and Medium Businesses (2022-2030) ($MN)

- Table 37 Global Fixed Wireless Access Market Outlook, By Large Enterprises (2022-2030) ($MN)

- Table 38 Global Fixed Wireless Access Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Fixed Wireless Access Market is accounted for $174.91 billion in 2024 and is expected to reach $571.10 billion by 2030 growing at a CAGR of 21.8% during the forecast period. Fixed Wireless Access (FWA) is a high-speed internet service delivered to homes or businesses via wireless connections, typically using radio signals instead of traditional wired infrastructure like fiber or copper cables. FWA connects end-users to the internet through fixed wireless transmitters installed in specific locations, often utilizing 4G, 5G, or other wireless technologies. This service is a cost-effective and faster alternative for areas where laying cables is impractical, providing reliable broadband without the need for physical cables to each user.

Market Dynamics:

Driver:

Rising demand for high-speed internet

Fixed Wireless Access provides an alternative to traditional broadband options, making it a cost-effective solution for remote and underserved areas. As 5G technology becomes more prevalent, FWA benefits from enhanced speeds and lower latency. The shift towards remote work, online learning, and streaming services has further accelerated the demand for reliable internet connections. Governments and telecom operators are investing in expanding FWA networks to meet the surge in data consumption. This trend is expected to continue, boosting the adoption of FWA solutions worldwide.

Restraint:

Competition from fiber and cable networks

Fiber-optic networks offer high-speed, reliable connections with greater bandwidth, making them more appealing for consumers seeking faster internet. Cable networks, though typically more expensive, also provide stable and fast broadband services. These traditional alternatives often overshadow the FWA market, especially in urban areas. As a result, consumers may prefer the established fiber and cable options, reducing the adoption of wireless solutions. This competition forces FWA providers to offer competitive pricing and better performance to attract customers.

Opportunity:

Integration with IoT devices

Integration with IoT devices require stable, high-speed networks, which FWA solutions can provide, particularly in areas lacking traditional broadband infrastructure. As more IoT applications emerge, such as smart cities and industrial automation, the demand for reliable wireless broadband grows. FWA technology offers low-latency, high-bandwidth services, making it ideal for connecting numerous IoT devices simultaneously. This integration supports seamless communication and data exchange across connected devices, improving operational efficiency. Overall, the IoT-FWA synergy accelerates digital transformation across multiple sectors, driving market expansion.

Threat:

Technological obsolescence

The need for faster and more dependable internet connections is growing, and older systems are finding it difficult to keep up with the new and improved technology. Due to the resulting service quality disparity, businesses are forced to either improve or become less relevant in the market. Furthermore, because technology is developing so quickly, carriers may have to make expensive investments in new infrastructure on a regular basis. Older FWA equipment can occasionally become incompatible with more recent models and network protocols, which reduces its usefulness. The introduction of next-generation technology further raises consumer expectations, making antiquated FWA systems less competitive.

Covid-19 Impact

The Covid-19 pandemic significantly accelerated the demand for Fixed Wireless Access (FWA) as remote work, education, and online services surged. With increased reliance on digital platforms, many areas sought reliable internet solutions, driving growth in FWA deployments. The pandemic exposed the limitations of existing broadband infrastructure, prompting both governments and private sectors to invest in FWA technology. FWA providers, especially those offering 5G-based services, saw a rise in demand due to its potential to deliver faster and more reliable internet. However, challenges such as supply chain disruptions and economic slowdowns impacted the market's growth trajectory in the short term.

The hardware segment is expected to be the largest during the forecast period

The hardware segment is expected to account for the largest market share during the forecast period, due to the necessary infrastructure for high-speed internet connectivity. Routers, antennas, and wireless gateways are essential for FWA deployments, ensuring stable and reliable performance. The growing demand for broadband in underserved areas drives the adoption of cost-effective FWA hardware solutions. As 5G technology advances, FWA hardware upgrades enable faster speeds and lower latency for consumers. Innovations in hardware, such as advanced chipsets and antenna designs, improve signal quality and coverage. This hardware evolution supports the scalability of FWA networks, catering to the increasing need for data-intensive applications.

The small and medium businesses segment is expected to have the highest CAGR during the forecast period

Over the forecast period, the small and medium businesses segment is predicted to witness the highest growth rate by seeking affordable and scalable internet solutions. FWA offers these businesses a cost-effective alternative to traditional broadband services, especially in areas where fiber optics and wired connections are not feasible. SMBs benefit from the quick deployment of FWA, which minimizes downtime and reduces installation costs. With increasing digitalization, SMBs require high-speed, reliable internet for operations, making FWA an attractive choice. The ability to expand coverage in rural or underserved areas is another key factor, enabling SMBs to tap into previously inaccessible markets.

Region with largest share:

During the forecast period, the Asia Pacific region is expected to hold the largest market share due to rising demand for high-speed internet and reasonably priced broadband solutions. FWA is emerging as a compelling substitute for conventional wired internet in underserved and rural regions as 4G and 5G networks grow. FWA adoption is being supported by governments in nations like China, Japan, and India as part of their efforts to undergo digital transformation. The emergence of smart cities and increased dependence on cloud-based services and IoT are further factors supporting the industry. In order to satisfy the growing need for dependable and fast internet connections, major firms in the area are investing in cutting-edge technology like 5G FWA. T

Region with highest CAGR:

Over the forecast period, the South America region is anticipated to exhibit the highest CAGR, owing to increased demand for high-speed internet connectivity in both urban and rural areas. Telecom providers are rapidly expanding FWA networks to deliver broadband services to underserved regions, reducing the need for extensive fiber optic infrastructure. Brazil, Argentina, and Colombia are leading the charge in FWA adoption, with substantial investments in 4G and 5G networks. The growing popularity of remote work and digital services is further boosting the demand for reliable and cost-effective broadband solutions. Key market players are focusing on providing affordable internet packages and innovative FWA technologies to capture the market share.

Key players in the market

Some of the key players profiled in the Fixed Wireless Access Market include Huawei Technologies Co., Ltd., Ericsson AB, Nokia Corporation, ZTE Corporation, Samsung Electronics Co., Ltd., Cisco Systems, Inc., Qualcomm Technologies, Inc., Intel Corporation, Cradlepoint (part of Ericsson), Cambium Networks, Inc., Airspan Networks, Inc., Redline Communications Inc., Altiostar Networks, Inc., Commscope Holding Company, Inc., T-Mobile USA, Inc., Verizon Communications Inc., AT&T Inc. and BT Group plc.

Key Developments:

In December 2024, Ericsson signed a substantial "multi-billion" dollar agreement with India's Bharti Airtel to enhance its 4G and 5G services. Ericsson will provide centralized radio access network (RAN) and Open RAN-ready solutions, aiming to improve network speed, reliability, and coverage. This partnership continues a collaboration that has lasted over two decades.

In February 2024, Huawei unveiled four new solutions for Internet Service Providers (ISPs) and Managed Service Providers (MSPs), including the Fixed Access Network (FAN) Sharing Solution. These solutions aimed to accelerate the construction and upgrade of premium all-optical networks, enhancing the digital transformation of ISPs.

In September 2023, Sound Broadband, a subsidiary of LICT, partnered with Xtreme Enterprises and Ericsson to provide 5G ultra-high-speed Fixed Wireless Access in rural America. The collaboration demonstrated near gigabit internet speeds over FWA, utilizing Ericsson's 5G solutions.

Products Covered:

- Hardware

- Software

- Services

Service Providers Covered:

- Telecom Operators

- Cable Operators

- Internet Service Providers (ISPs)

- Other Service Providers

Deployment Types Covered:

- Outdoor Deployment

- Indoor Deployment

Frequency Bands Covered:

- Sub 6 GHz

- Above 6 GHz

- Millimeter Wave (mmWave)

Technologies Covered:

- 5G FWA

- 4G LTE FWA

- Wi-Fi FWA

- Other technologies

End Users Covered:

- Residential Users

- Business Users

- Small and Medium Businesses

- Large Enterprises

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Technology Analysis

- 3.7 End User Analysis

- 3.8 Emerging Markets

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Fixed Wireless Access Market, By Component

- 5.1 Introduction

- 5.2 Hardware

- 5.2.1 Customer Premises Equipment (CPE)

- 5.2.2 Wireless Routers

- 5.2.3 Antennas

- 5.2.4 Base Stations

- 5.3 Software

- 5.3.1 Network Management Software

- 5.3.2 Security Software

- 5.4 Services

- 5.4.1 Installation

- 5.4.2 Maintenance

- 5.4.3 Consulting

- 5.4.4 Managed Services

6 Global Fixed Wireless Access Market, By Service Provider

- 6.1 Introduction

- 6.2 Telecom Operators

- 6.3 Cable Operators

- 6.4 Internet Service Providers (ISPs)

- 6.5 Other Service Providers

7 Global Fixed Wireless Access Market, By Deployment Type

- 7.1 Introduction

- 7.2 Outdoor Deployment

- 7.3 Indoor Deployment

8 Global Fixed Wireless Access Market, By Frequency Band

- 8.1 Introduction

- 8.2 Sub 6 GHz

- 8.3 Above 6 GHz

- 8.4 Millimeter Wave (mmWave)

9 Global Fixed Wireless Access Market, By Technology

- 9.1 Introduction

- 9.2 5G FWA

- 9.3 4G LTE FWA

- 9.4 Wi-Fi FWA

- 9.5 Other technologies

10 Global Fixed Wireless Access Market, By End User

- 10.1 Introduction

- 10.2 Residential Users

- 10.3 Business Users

- 10.4 Small and Medium Businesses

- 10.5 Large Enterprises

- 10.6 Other End Users

11 Global Fixed Wireless Access Market, By Geography

- 11.1 Introduction

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 Italy

- 11.3.4 France

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 Japan

- 11.4.2 China

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 New Zealand

- 11.4.6 South Korea

- 11.4.7 Rest of Asia Pacific

- 11.5 South America

- 11.5.1 Argentina

- 11.5.2 Brazil

- 11.5.3 Chile

- 11.5.4 Rest of South America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 Qatar

- 11.6.4 South Africa

- 11.6.5 Rest of Middle East & Africa

12 Key Developments

- 12.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 12.2 Acquisitions & Mergers

- 12.3 New Product Launch

- 12.4 Expansions

- 12.5 Other Key Strategies

13 Company Profiling

- 13.1 Huawei Technologies Co., Ltd.

- 13.2 Ericsson AB

- 13.3 Nokia Corporation

- 13.4 ZTE Corporation

- 13.5 Samsung Electronics Co., Ltd.

- 13.6 Cisco Systems, Inc.

- 13.7 Qualcomm Technologies, Inc.

- 13.8 Intel Corporation

- 13.9 Cradlepoint

- 13.10 Cambium Networks, Inc.

- 13.11 Airspan Networks, Inc.

- 13.12 Redline Communications Inc.

- 13.13 Altiostar Networks, Inc.

- 13.14 Commscope Holding Company, Inc.

- 13.15 T-Mobile USA, Inc.

- 13.16 Verizon Communications Inc.

- 13.17 AT&T Inc.

- 13.18 BT Group plc