|

|

市場調査レポート

商品コード

1603763

自動車用eアクスルの2030年までの市場予測: タイプ別、コンポーネント別、車種別、出力定格別、シャフトタイプ別、用途別、地域別の世界分析Automotive E-Axle Market Forecasts to 2030 - Global Analysis By Type (Front axle, Rear axle and Other Types), Component, Vehicle Type, Power Rating, Shaft Type, Application and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用eアクスルの2030年までの市場予測: タイプ別、コンポーネント別、車種別、出力定格別、シャフトタイプ別、用途別、地域別の世界分析 |

|

出版日: 2024年11月11日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の自動車用eアクスル市場は2024年に232億8,000万米ドルを占め、予測期間中のCAGRは39.7%で成長し、2030年には1,730億6,000万米ドルに達すると予測されています。

自動車用eアクスルは、電気モーター、パワーエレクトロニクス、ギアボックスが一体化したもので、電気アクスルとも呼ばれます。モーターから車輪に効率的に動力を伝達することで、従来の内燃エンジンドライブトレインに取って代わる。電動ドライブトレインでは、eアクスルは性能の向上、軽量化、エネルギー効率の向上を実現します。

2021年4月に発表された国際エネルギー機関(IEA)の世界EV年間見通し報告書によると、2020年には約370の電気自動車モデルが発売されました。

高まる電気自動車(EV)需要

最新のEVは、電気モーター、パワーエレクトロニクス、ギアボックスを1つのコンパクトなユニットに統合し、車両性能とエネルギー経済性を向上させるeアクスルなしでは成り立たないです。自動車メーカーが排出ガス規制や環境目標を達成するために電動パワートレインにシフトする中、モーター、パワーエレクトロニクス、トランスミッションを組み合わせた完全に統合されたドライブソリューションであるeアクスルは、EVの効率化に不可欠なものとなっています。eアクスルは、EVの性能に不可欠な出力密度の向上、軽量化、航続距離の延長を実現します。この需要は、政府のインセンティブや、持続可能な選択肢に対する消費者の関心も後押ししており、自動車メーカーは、拡大するEV市場で競争するために、コンパクトで高性能なeアクスルを電気自動車ラインナップに採用するようになっています。

限られた充電インフラ

eアクスルは、EVの効率的な電気ドライブトレインに不可欠ですが、その潜在能力をフルに発揮できるかどうかは、信頼できる充電ステーションネットワークにかかっています。充電ステーションがまばらな地域では、消費者は航続距離への不安に直面し、eアクスル技術に依存する完全な電気自動車やハイブリッド車の採用をためらうことになります。この限られたインフラは、効率的な運行のために頻繁で信頼できる充電を必要とする商用車にも影響を与えます。その結果、eアクスルソリューションに対する市場の需要と投資が妨げられ、EVセクター全体の技術進歩と採用率の両方が鈍化しています。

ハイブリッドEVと商用EVの拡大

eアクスルは、電気モーター、パワーエレクトロニクス、トランスミッションを1つのコンパクトなユニットに統合し、ハイブリッドおよび電気アプリケーションに不可欠な効率と電力密度を向上させます。環境規制の高まりに伴い、ハイブリッド車、プラグインハイブリッド車、配送トラックやバスなどの商用EVの需要が急増しています。このシフトは、eアクスルを促進します。eアクスルは、車両重量を減らし、航続距離を延ばし、排出ガスを削減しながら、商用EVに不可欠なトルクと耐荷重能力を向上させます。これらの要件を満たす柔軟で高性能なドライブトレインへのニーズが、eアクスル技術への革新と投資に拍車をかけています。

代替パワートレインとの競合

水素燃料電池や従来型の内燃機関(ICE)ハイブリッドといった代替パワートレインオプションは、大型用途に実行可能な低排出ガス・オプションを提供することで競合します。そのため、商用EV車軸の開発への投資が抑制される可能性があります。その一方で、ICEハイブリッド技術の向上は、信頼性が高く、拡張可能で、効果的な選択肢を提供し、特にEVインフラが脆弱な地域では、生産者や顧客の人気を維持しています。バッテリー技術の限界もeアクスルの魅力に影響します。用途によっては、バッテリー要件の低い競合システムの方が実行可能な場合があるからです。このような代替ソリューションは、より幅広い車種や運転条件に適合する費用対効果が高く実績のあるオプションを提供するため、eアクスルの採用を妨げる可能性があります。

COVID-19の影響

COVID-19の流行は当初、サプライチェーンの課題、工場の操業停止、車両生産の遅れにより、自動車用eアクスル市場を混乱させました。しかし、世界の自動車産業が徐々に電気自動車(EV)と持続可能な輸送ソリューションにシフトするにつれて、eアクスル市場は回復し始めました。政府のインセンティブ、クリーンエネルギーへの注目の高まり、EV需要の高まりが、パンデミック後の市場成長を牽引しました。特にAPAC地域では、電動モビリティの急速な進歩が見られ、eアクスルシステムの採用がさらに加速しました。

予測期間中、モーターセグメントが最大になる見込み

モーターセグメントは、eアクスルシステムのパワーと効率性により、有利な成長を遂げると推定されます。これらのモーターは電気エネルギーを機械的動力に変換し、EVやハイブリッド車のスムーズで効率的な推進を可能にします。eアクスルの高性能モーターは、トルク、速度、全体的なエネルギー効率の向上に役立ち、これはEVが従来のパワートレインと同等以上の能力を発揮するために不可欠です。軽量設計や強化された冷却システムなど、モーター技術における革新は、乗用車から商用トラックまで、様々な車種におけるeアクスルの用途を拡大しています。

商用車セグメントは予測期間中に最も高いCAGRが見込まれる

商用車セグメントは、排ガス規制と運用コストの削減により、予測期間中に最も高いCAGR成長が見込まれています。eアクスルは、電気モーター、パワーエレクトロニクス、トランスミッションを組み合わせたコンパクトで統合されたソリューションを提供し、トラックやバスのような高トルクとパワー密度を必要とするヘビーデューティアプリケーションに最適です。都市がより環境に優しい公共輸送を推進する中、商用車の電動化は不可欠となり、効率的なeアクスルシステムの需要が高まっています。積載効率をサポートし、車両航続距離を延長するeアクスルの能力は、商用セグメントでの魅力を高めています。

最大のシェアを占める地域:

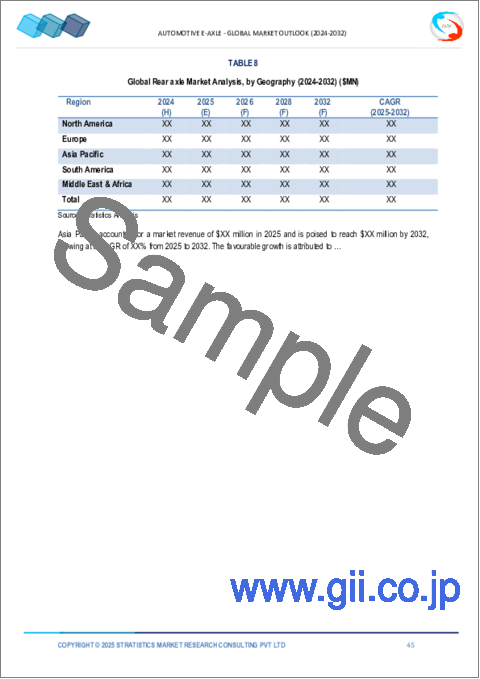

アジア太平洋地域は、電気自動車(EV)の普及が進み、政府の政策も後押ししていることから、予測期間中に最大の市場シェアを占めると予測されます。中国、日本、インドのような国々は、電気自動車(EV)とハイブリッド電気自動車(HEV)の需要が高まっている主要貢献国です。アジア太平洋地域は最大の急成長市場であり、電動モビリティ・インフラと技術の進歩に多額の投資が行われています。同市場は、クリーンエネルギー・ソリューションへのシフトの高まりとともに、強力な製造能力、技術革新、有利な政策イニシアチブにより、主導的地位を維持すると予想されます。

CAGRが最も高い地域:

北米は、電気自動車とハイブリッド車の需要増に牽引され、予測期間中に最も高いCAGRを示すと予測されます。政府の奨励策、環境問題への関心、技術の進歩がこの市場を押し上げる主な要因です。北米は、電気自動車の性能と効率を高めることを目的としたeアクスル技術に対する自動車メーカーの強力な投資により、大きなシェアを占めると予想されます。さらに、この地域は再生可能エネルギーの消費者導入の恩恵を受けており、電気推進システムの良好な市場環境に寄与しています。

無料のカスタマイズサービス

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 用途分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の自動車用eアクスル市場:タイプ別

- フロントアクスル

- リアアクスル

- その他のタイプ

第6章 世界の自動車用eアクスル市場:コンポーネント別

- モーター

- パワーエレクトロニクス

- トランスミッション

- その他のコンポーネント

第7章 世界の自動車用eアクスル市場:車種別

- 乗用車

- 商用車

- その他の車種別

第8章 世界の自動車用eアクスル市場:出力定格別

- 低電力(100kW以下)

- 中出力(100~200kW)

- 高出力(200kW以上)

第9章 世界の自動車用eアクスル市場:シャフトタイプ別

- シングル

- マルチピース

- その他のシャフトタイプ

第10章 世界の自動車用eアクスル市場:用途別

- 後輪駆動(RWD)

- 前輪駆動(FWD)

- その他の用途

第11章 世界の自動車用eアクスル市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第12章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第13章 企業プロファイリング

- Robert Bosch GmbH

- Magna International Inc.

- Nidec Corporation

- GKN Automotive Limited

- Allison Transmission Inc.

- Schaeffler AG

- ZF Friedrichshafen AG

- Dana Limited

- Linamar Corporation

- Vitesco Technologies Group AG

- Meritor, Inc.

- BorgWarner Inc.

- Valeo SA

- Continental AG

- Siemens AG

- Hitachi Automotive Systems

- Mitsubishi Electric Corporation

- Hyundai Mobis

- JTEKT Corporation

- Unipres Corporation

List of Tables

- Table 1 Global Automotive E-Axle Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Automotive E-Axle Market Outlook, By Type (2022-2030) ($MN)

- Table 3 Global Automotive E-Axle Market Outlook, By Front axle (2022-2030) ($MN)

- Table 4 Global Automotive E-Axle Market Outlook, By Rear axle (2022-2030) ($MN)

- Table 5 Global Automotive E-Axle Market Outlook, By Other Types (2022-2030) ($MN)

- Table 6 Global Automotive E-Axle Market Outlook, By Component (2022-2030) ($MN)

- Table 7 Global Automotive E-Axle Market Outlook, By Motor (2022-2030) ($MN)

- Table 8 Global Automotive E-Axle Market Outlook, By Power Electronics (2022-2030) ($MN)

- Table 9 Global Automotive E-Axle Market Outlook, By Transmission (2022-2030) ($MN)

- Table 10 Global Automotive E-Axle Market Outlook, By Other Components (2022-2030) ($MN)

- Table 11 Global Automotive E-Axle Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 12 Global Automotive E-Axle Market Outlook, By Passenger Vehicles (2022-2030) ($MN)

- Table 13 Global Automotive E-Axle Market Outlook, By Commercial Vehicles (2022-2030) ($MN)

- Table 14 Global Automotive E-Axle Market Outlook, By Other Vehicle Types (2022-2030) ($MN)

- Table 15 Global Automotive E-Axle Market Outlook, By Power Rating (2022-2030) ($MN)

- Table 16 Global Automotive E-Axle Market Outlook, By Low-power (Below 100 kW (2022-2030) ($MN)

- Table 17 Global Automotive E-Axle Market Outlook, By Medium-power (100-200 kW) (2022-2030) ($MN)

- Table 18 Global Automotive E-Axle Market Outlook, By High-power (Above 200 kW) (2022-2030) ($MN)

- Table 19 Global Automotive E-Axle Market Outlook, By Shaft Type (2022-2030) ($MN)

- Table 20 Global Automotive E-Axle Market Outlook, By Single (2022-2030) ($MN)

- Table 21 Global Automotive E-Axle Market Outlook, By Multi Piece (2022-2030) ($MN)

- Table 22 Global Automotive E-Axle Market Outlook, By Other Shaft Types (2022-2030) ($MN)

- Table 23 Global Automotive E-Axle Market Outlook, By Application (2022-2030) ($MN)

- Table 24 Global Automotive E-Axle Market Outlook, By Rear-wheel Drive (RWD) (2022-2030) ($MN)

- Table 25 Global Automotive E-Axle Market Outlook, By Front-wheel Drive (FWD) (2022-2030) ($MN)

- Table 26 Global Automotive E-Axle Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 27 North America Automotive E-Axle Market Outlook, By Country (2022-2030) ($MN)

- Table 28 North America Automotive E-Axle Market Outlook, By Type (2022-2030) ($MN)

- Table 29 North America Automotive E-Axle Market Outlook, By Front axle (2022-2030) ($MN)

- Table 30 North America Automotive E-Axle Market Outlook, By Rear axle (2022-2030) ($MN)

- Table 31 North America Automotive E-Axle Market Outlook, By Other Types (2022-2030) ($MN)

- Table 32 North America Automotive E-Axle Market Outlook, By Component (2022-2030) ($MN)

- Table 33 North America Automotive E-Axle Market Outlook, By Motor (2022-2030) ($MN)

- Table 34 North America Automotive E-Axle Market Outlook, By Power Electronics (2022-2030) ($MN)

- Table 35 North America Automotive E-Axle Market Outlook, By Transmission (2022-2030) ($MN)

- Table 36 North America Automotive E-Axle Market Outlook, By Other Components (2022-2030) ($MN)

- Table 37 North America Automotive E-Axle Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 38 North America Automotive E-Axle Market Outlook, By Passenger Vehicles (2022-2030) ($MN)

- Table 39 North America Automotive E-Axle Market Outlook, By Commercial Vehicles (2022-2030) ($MN)

- Table 40 North America Automotive E-Axle Market Outlook, By Other Vehicle Types (2022-2030) ($MN)

- Table 41 North America Automotive E-Axle Market Outlook, By Power Rating (2022-2030) ($MN)

- Table 42 North America Automotive E-Axle Market Outlook, By Low-power (Below 100 kW (2022-2030) ($MN)

- Table 43 North America Automotive E-Axle Market Outlook, By Medium-power (100-200 kW) (2022-2030) ($MN)

- Table 44 North America Automotive E-Axle Market Outlook, By High-power (Above 200 kW) (2022-2030) ($MN)

- Table 45 North America Automotive E-Axle Market Outlook, By Shaft Type (2022-2030) ($MN)

- Table 46 North America Automotive E-Axle Market Outlook, By Single (2022-2030) ($MN)

- Table 47 North America Automotive E-Axle Market Outlook, By Multi Piece (2022-2030) ($MN)

- Table 48 North America Automotive E-Axle Market Outlook, By Other Shaft Types (2022-2030) ($MN)

- Table 49 North America Automotive E-Axle Market Outlook, By Application (2022-2030) ($MN)

- Table 50 North America Automotive E-Axle Market Outlook, By Rear-wheel Drive (RWD) (2022-2030) ($MN)

- Table 51 North America Automotive E-Axle Market Outlook, By Front-wheel Drive (FWD) (2022-2030) ($MN)

- Table 52 North America Automotive E-Axle Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 53 Europe Automotive E-Axle Market Outlook, By Country (2022-2030) ($MN)

- Table 54 Europe Automotive E-Axle Market Outlook, By Type (2022-2030) ($MN)

- Table 55 Europe Automotive E-Axle Market Outlook, By Front axle (2022-2030) ($MN)

- Table 56 Europe Automotive E-Axle Market Outlook, By Rear axle (2022-2030) ($MN)

- Table 57 Europe Automotive E-Axle Market Outlook, By Other Types (2022-2030) ($MN)

- Table 58 Europe Automotive E-Axle Market Outlook, By Component (2022-2030) ($MN)

- Table 59 Europe Automotive E-Axle Market Outlook, By Motor (2022-2030) ($MN)

- Table 60 Europe Automotive E-Axle Market Outlook, By Power Electronics (2022-2030) ($MN)

- Table 61 Europe Automotive E-Axle Market Outlook, By Transmission (2022-2030) ($MN)

- Table 62 Europe Automotive E-Axle Market Outlook, By Other Components (2022-2030) ($MN)

- Table 63 Europe Automotive E-Axle Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 64 Europe Automotive E-Axle Market Outlook, By Passenger Vehicles (2022-2030) ($MN)

- Table 65 Europe Automotive E-Axle Market Outlook, By Commercial Vehicles (2022-2030) ($MN)

- Table 66 Europe Automotive E-Axle Market Outlook, By Other Vehicle Types (2022-2030) ($MN)

- Table 67 Europe Automotive E-Axle Market Outlook, By Power Rating (2022-2030) ($MN)

- Table 68 Europe Automotive E-Axle Market Outlook, By Low-power (Below 100 kW (2022-2030) ($MN)

- Table 69 Europe Automotive E-Axle Market Outlook, By Medium-power (100-200 kW) (2022-2030) ($MN)

- Table 70 Europe Automotive E-Axle Market Outlook, By High-power (Above 200 kW) (2022-2030) ($MN)

- Table 71 Europe Automotive E-Axle Market Outlook, By Shaft Type (2022-2030) ($MN)

- Table 72 Europe Automotive E-Axle Market Outlook, By Single (2022-2030) ($MN)

- Table 73 Europe Automotive E-Axle Market Outlook, By Multi Piece (2022-2030) ($MN)

- Table 74 Europe Automotive E-Axle Market Outlook, By Other Shaft Types (2022-2030) ($MN)

- Table 75 Europe Automotive E-Axle Market Outlook, By Application (2022-2030) ($MN)

- Table 76 Europe Automotive E-Axle Market Outlook, By Rear-wheel Drive (RWD) (2022-2030) ($MN)

- Table 77 Europe Automotive E-Axle Market Outlook, By Front-wheel Drive (FWD) (2022-2030) ($MN)

- Table 78 Europe Automotive E-Axle Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 79 Asia Pacific Automotive E-Axle Market Outlook, By Country (2022-2030) ($MN)

- Table 80 Asia Pacific Automotive E-Axle Market Outlook, By Type (2022-2030) ($MN)

- Table 81 Asia Pacific Automotive E-Axle Market Outlook, By Front axle (2022-2030) ($MN)

- Table 82 Asia Pacific Automotive E-Axle Market Outlook, By Rear axle (2022-2030) ($MN)

- Table 83 Asia Pacific Automotive E-Axle Market Outlook, By Other Types (2022-2030) ($MN)

- Table 84 Asia Pacific Automotive E-Axle Market Outlook, By Component (2022-2030) ($MN)

- Table 85 Asia Pacific Automotive E-Axle Market Outlook, By Motor (2022-2030) ($MN)

- Table 86 Asia Pacific Automotive E-Axle Market Outlook, By Power Electronics (2022-2030) ($MN)

- Table 87 Asia Pacific Automotive E-Axle Market Outlook, By Transmission (2022-2030) ($MN)

- Table 88 Asia Pacific Automotive E-Axle Market Outlook, By Other Components (2022-2030) ($MN)

- Table 89 Asia Pacific Automotive E-Axle Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 90 Asia Pacific Automotive E-Axle Market Outlook, By Passenger Vehicles (2022-2030) ($MN)

- Table 91 Asia Pacific Automotive E-Axle Market Outlook, By Commercial Vehicles (2022-2030) ($MN)

- Table 92 Asia Pacific Automotive E-Axle Market Outlook, By Other Vehicle Types (2022-2030) ($MN)

- Table 93 Asia Pacific Automotive E-Axle Market Outlook, By Power Rating (2022-2030) ($MN)

- Table 94 Asia Pacific Automotive E-Axle Market Outlook, By Low-power (Below 100 kW (2022-2030) ($MN)

- Table 95 Asia Pacific Automotive E-Axle Market Outlook, By Medium-power (100-200 kW) (2022-2030) ($MN)

- Table 96 Asia Pacific Automotive E-Axle Market Outlook, By High-power (Above 200 kW) (2022-2030) ($MN)

- Table 97 Asia Pacific Automotive E-Axle Market Outlook, By Shaft Type (2022-2030) ($MN)

- Table 98 Asia Pacific Automotive E-Axle Market Outlook, By Single (2022-2030) ($MN)

- Table 99 Asia Pacific Automotive E-Axle Market Outlook, By Multi Piece (2022-2030) ($MN)

- Table 100 Asia Pacific Automotive E-Axle Market Outlook, By Other Shaft Types (2022-2030) ($MN)

- Table 101 Asia Pacific Automotive E-Axle Market Outlook, By Application (2022-2030) ($MN)

- Table 102 Asia Pacific Automotive E-Axle Market Outlook, By Rear-wheel Drive (RWD) (2022-2030) ($MN)

- Table 103 Asia Pacific Automotive E-Axle Market Outlook, By Front-wheel Drive (FWD) (2022-2030) ($MN)

- Table 104 Asia Pacific Automotive E-Axle Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 105 South America Automotive E-Axle Market Outlook, By Country (2022-2030) ($MN)

- Table 106 South America Automotive E-Axle Market Outlook, By Type (2022-2030) ($MN)

- Table 107 South America Automotive E-Axle Market Outlook, By Front axle (2022-2030) ($MN)

- Table 108 South America Automotive E-Axle Market Outlook, By Rear axle (2022-2030) ($MN)

- Table 109 South America Automotive E-Axle Market Outlook, By Other Types (2022-2030) ($MN)

- Table 110 South America Automotive E-Axle Market Outlook, By Component (2022-2030) ($MN)

- Table 111 South America Automotive E-Axle Market Outlook, By Motor (2022-2030) ($MN)

- Table 112 South America Automotive E-Axle Market Outlook, By Power Electronics (2022-2030) ($MN)

- Table 113 South America Automotive E-Axle Market Outlook, By Transmission (2022-2030) ($MN)

- Table 114 South America Automotive E-Axle Market Outlook, By Other Components (2022-2030) ($MN)

- Table 115 South America Automotive E-Axle Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 116 South America Automotive E-Axle Market Outlook, By Passenger Vehicles (2022-2030) ($MN)

- Table 117 South America Automotive E-Axle Market Outlook, By Commercial Vehicles (2022-2030) ($MN)

- Table 118 South America Automotive E-Axle Market Outlook, By Other Vehicle Types (2022-2030) ($MN)

- Table 119 South America Automotive E-Axle Market Outlook, By Power Rating (2022-2030) ($MN)

- Table 120 South America Automotive E-Axle Market Outlook, By Low-power (Below 100 kW (2022-2030) ($MN)

- Table 121 South America Automotive E-Axle Market Outlook, By Medium-power (100-200 kW) (2022-2030) ($MN)

- Table 122 South America Automotive E-Axle Market Outlook, By High-power (Above 200 kW) (2022-2030) ($MN)

- Table 123 South America Automotive E-Axle Market Outlook, By Shaft Type (2022-2030) ($MN)

- Table 124 South America Automotive E-Axle Market Outlook, By Single (2022-2030) ($MN)

- Table 125 South America Automotive E-Axle Market Outlook, By Multi Piece (2022-2030) ($MN)

- Table 126 South America Automotive E-Axle Market Outlook, By Other Shaft Types (2022-2030) ($MN)

- Table 127 South America Automotive E-Axle Market Outlook, By Application (2022-2030) ($MN)

- Table 128 South America Automotive E-Axle Market Outlook, By Rear-wheel Drive (RWD) (2022-2030) ($MN)

- Table 129 South America Automotive E-Axle Market Outlook, By Front-wheel Drive (FWD) (2022-2030) ($MN)

- Table 130 South America Automotive E-Axle Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 131 Middle East & Africa Automotive E-Axle Market Outlook, By Country (2022-2030) ($MN)

- Table 132 Middle East & Africa Automotive E-Axle Market Outlook, By Type (2022-2030) ($MN)

- Table 133 Middle East & Africa Automotive E-Axle Market Outlook, By Front axle (2022-2030) ($MN)

- Table 134 Middle East & Africa Automotive E-Axle Market Outlook, By Rear axle (2022-2030) ($MN)

- Table 135 Middle East & Africa Automotive E-Axle Market Outlook, By Other Types (2022-2030) ($MN)

- Table 136 Middle East & Africa Automotive E-Axle Market Outlook, By Component (2022-2030) ($MN)

- Table 137 Middle East & Africa Automotive E-Axle Market Outlook, By Motor (2022-2030) ($MN)

- Table 138 Middle East & Africa Automotive E-Axle Market Outlook, By Power Electronics (2022-2030) ($MN)

- Table 139 Middle East & Africa Automotive E-Axle Market Outlook, By Transmission (2022-2030) ($MN)

- Table 140 Middle East & Africa Automotive E-Axle Market Outlook, By Other Components (2022-2030) ($MN)

- Table 141 Middle East & Africa Automotive E-Axle Market Outlook, By Vehicle Type (2022-2030) ($MN)

- Table 142 Middle East & Africa Automotive E-Axle Market Outlook, By Passenger Vehicles (2022-2030) ($MN)

- Table 143 Middle East & Africa Automotive E-Axle Market Outlook, By Commercial Vehicles (2022-2030) ($MN)

- Table 144 Middle East & Africa Automotive E-Axle Market Outlook, By Other Vehicle Types (2022-2030) ($MN)

- Table 145 Middle East & Africa Automotive E-Axle Market Outlook, By Power Rating (2022-2030) ($MN)

- Table 146 Middle East & Africa Automotive E-Axle Market Outlook, By Low-power (Below 100 kW (2022-2030) ($MN)

- Table 147 Middle East & Africa Automotive E-Axle Market Outlook, By Medium-power (100-200 kW) (2022-2030) ($MN)

- Table 148 Middle East & Africa Automotive E-Axle Market Outlook, By High-power (Above 200 kW) (2022-2030) ($MN)

- Table 149 Middle East & Africa Automotive E-Axle Market Outlook, By Shaft Type (2022-2030) ($MN)

- Table 150 Middle East & Africa Automotive E-Axle Market Outlook, By Single (2022-2030) ($MN)

- Table 151 Middle East & Africa Automotive E-Axle Market Outlook, By Multi Piece (2022-2030) ($MN)

- Table 152 Middle East & Africa Automotive E-Axle Market Outlook, By Other Shaft Types (2022-2030) ($MN)

- Table 153 Middle East & Africa Automotive E-Axle Market Outlook, By Application (2022-2030) ($MN)

- Table 154 Middle East & Africa Automotive E-Axle Market Outlook, By Rear-wheel Drive (RWD) (2022-2030) ($MN)

- Table 155 Middle East & Africa Automotive E-Axle Market Outlook, By Front-wheel Drive (FWD) (2022-2030) ($MN)

- Table 156 Middle East & Africa Automotive E-Axle Market Outlook, By Other Applications (2022-2030) ($MN)

According to Stratistics MRC, the Global Automotive E-Axle Market is accounted for $23.28 billion in 2024 and is expected to reach $173.06 billion by 2030 growing at a CAGR of 39.7% during the forecast period. An electric motor, power electronics, and gearbox are all combined into one unit by an automotive E-Axle, also known as an electric axle. It replaces conventional internal combustion engine drivetrain by effectively transferring power from the motor to the wheels. In electric drive trains, e-axles provide improved performance, lower weight, and increase energy efficiency.

According to the International Energy Agency (IEA) global annual EV outlook report published in April 2021, around 370 electric car models were available in 2020.

Market Dynamics:

Driver:

Growing demand for electric vehicles (EVs)

Modern EVs would not be the same without e-axles, which combine electric motors, power electronics, and gearboxes into a single, compact unit that improves vehicle performance and energy economy. As automakers shift towards electric power trains to meet emissions regulations and environmental goals, the E-Axle-a fully integrated drive solution combining motor, power electronics, and transmission-has become essential for EV efficiency. E-Axles improve power density, reduce weight, and enhance range, which are critical for EV performance. This demand is also fuelled by government incentives and consumer interest in sustainable options, pushing automakers to adopt compact, high-performance E-Axles in their electric line-ups to compete in the expanding EV market.

Restraint:

Limited charging infrastructure

E-Axles are essential for efficient electric drive trains in EVs, but their full potential depends on a reliable network of charging stations. In regions where charging stations are sparse, consumers face range anxiety, making them hesitant to adopt fully electric or hybrid vehicles that rely on E-Axle technology. This limited infrastructure also affects commercial fleets, which need frequent and dependable charging to operate efficiently. As a result, market demand and investment in E-Axle solutions are hindered, slowing both technological advancements and adoption rates across the EV sector.

Opportunity:

Expansion of hybrid and commercial EVs

E-Axles integrate electric motors, power electronics, and transmissions into a single compact unit, providing enhanced efficiency and power density essential for hybrid and electric applications. With rising environmental regulations, the demand for hybrids, plug-in hybrids, and commercial EVs, such as delivery trucks and buses, has surged. This shift promotes E-Axles as they support increased torque and load-bearing capabilities, crucial for commercial EVs, while reducing vehicle weight, boosting range, and lowering emissions. The need for flexible, high-performance drive trains to meet these requirements is fuelling innovations and investments in E-Axle technologies.

Threat:

Competition from alternative power train solutions

Alternative power train options, such as hydrogen fuel cells and conventional internal combustion engine (ICE) hybrids, compete with them by providing a viable low-emission option for heavy-duty applications. This could deter investment in the development of commercial EV axles. In the meanwhile, improvements in ICE hybrid technology offer a dependable, scalable, and effective choice that remains popular with producers and customers, particularly in areas with weak EV infrastructure. Battery technology limitations also influence the appeal of E-Axles, as competing systems with lower battery requirements may be more viable in certain applications. These alternative solutions can hinder E-Axle adoption by offering cost-effective, proven options that suit a wider range of vehicle types and operating conditions.

Covid-19 Impact

The COVID-19 pandemic initially disrupted the Automotive E-Axle market due to supply chain challenges, factory shutdowns, and delays in vehicle production. However, as the global automotive industry gradually shifted toward electric vehicles (EVs) and sustainable transportation solutions, the E-Axle market began recovering. Government incentives, an increased focus on clean energy, and rising demand for EVs drove market growth post-pandemic. The APAC region, in particular, saw rapid advancements in electric mobility, further accelerating the adoption of E-Axle systems.

The motor segment is expected to be the largest during the forecast period

The motor segment is estimated to have a lucrative growth, due to the power and efficiency of E-Axle systems. These motors convert electrical energy into mechanical power, enabling smooth and efficient propulsion in EVs and hybrids. High-performance motors in E-Axles help improve torque, speed, and overall energy efficiency, which is essential for EVs to match or exceed the capabilities of traditional power trains. Innovations in motor technology, such as lightweight designs and enhanced cooling systems, are expanding E-Axle applications across various vehicle types, from passenger cars to commercial trucks.

The commercial vehicles segment is expected to have the highest CAGR during the forecast period

The commercial vehicles segment is anticipated to witness the highest CAGR growth during the forecast period, due to the emission regulations and reduce operating costs. E-Axles offer a compact and integrated solution that combines electric motors, power electronics, and transmissions, making them ideal for heavy-duty applications that require high torque and power density, like trucks and buses. As cities push for greener public transport, electrified commercial vehicles become essential, increasing demand for efficient E-Axle systems. The ability of E-Axles to support payload efficiency and extend vehicle range enhances their appeal in the commercial segment.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period due to increased electric vehicle (EV) adoption and supportive government policies. Countries like China, Japan, and India are key contributors, with rising demand for electric vehicles (EVs) and hybrid electric vehicles (HEVs). APAC is the largest and fastest-growing market, with substantial investments in electric mobility infrastructure and technology advancements. This market is expected to maintain its leadership position due to strong manufacturing capabilities, technological innovation, and favourable policy initiatives, along with the growing shift towards clean energy solutions.

Region with highest CAGR:

North America is projected to have the highest CAGR over the forecast period, driven by rising demand for electric and hybrid vehicles. Government incentives, environmental concerns, and technological advancements are major factors pushing this market. North America is expected to hold a significant share due to strong investments from automakers in e-axle technology, aimed at enhancing electric vehicle performance and efficiency. Moreover, the region benefits from consumer adoption of renewable energy, contributing to a favorable market environment for electric propulsion systems.

Key players in the market

Some of the key players profiled in the Automotive E-Axle Market include Robert Bosch GmbH, Magna International Inc., Nidec Corporation, GKN Automotive Limited, Allison Transmission Inc., Schaeffler AG, ZF Friedrichshafen AG, Dana Limited, Linamar Corporation, Vitesco Technologies Group AG, Meritor, Inc., BorgWarner Inc., Valeo SA, Continental AG, Siemens AG, Hitachi Automotive Systems, Mitsubishi Electric Corporation, Hyundai Mobis, JTEKT Corporation and Unipres Corporation.

Key Developments:

In October 2024, Nidec Motor Corporation (NMC), a subsidiary of Nidec, entered a key agreement with Ashok Leyland, a major Indian commercial vehicle manufacturer. This partnership focuses on developing electric motor-controller systems ("E-Drive") specifically for commercial vehicle electrification.

In May 2024, Mitsubishi Electric, Mitsubishi Electric Mobility, and AISIN announced their collaboration, intended to leverage Mitsubishi's expertise in power electronics and control optimization technologies alongside AISIN's vehicle integration capabilities. This joint venture will focus on creating an optimized E-Axle system that integrates both companies' technologies, including BluE Nexus systems.

In September 2024, Schaeffler highlighted its latest innovations and product expansions under its rebranded Schaeffler Vehicle Lifetime Solutions (VLS), showcasing repair and service solutions tailored for hybrid and electric vehicles.

Types Covered:

- Front axle

- Rear axle

- Other Types

Components Covered:

- Motor

- Power Electronics

- Transmission

- Other Components

Vehicle Types Covered:

- Passenger Vehicles

- Commercial Vehicles

- Other Vehicle Types

Power Ratings Covered:

- Low-power (Below 100 kW

- Medium-power (100-200 kW)

- High-power (Above 200 kW)

Shaft Types Covered:

- Single

- Multi Piece

- Other Shaft Types

Applications Covered:

- Rear-wheel Drive (RWD)

- Front-wheel Drive (FWD)

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Automotive E-Axle Market, By Type

- 5.1 Introduction

- 5.2 Front axle

- 5.3 Rear axle

- 5.4 Other Types

6 Global Automotive E-Axle Market, By Component

- 6.1 Introduction

- 6.2 Motor

- 6.3 Power Electronics

- 6.4 Transmission

- 6.5 Other Components

7 Global Automotive E-Axle Market, By Vehicle Type

- 7.1 Introduction

- 7.2 Passenger Vehicles

- 7.3 Commercial Vehicles

- 7.4 Other Vehicle Types

8 Global Automotive E-Axle Market, By Power Rating

- 8.1 Introduction

- 8.2 Low-power (Below 100 kW)

- 8.3 Medium-power (100-200 kW)

- 8.4 High-power (Above 200 kW)

9 Global Automotive E-Axle Market, By Shaft Type

- 9.1 Introduction

- 9.2 Single

- 9.3 Multi Piece

- 9.4 Other Shaft Types

10 Global Automotive E-Axle Market, By Application

- 10.1 Introduction

- 10.2 Rear-wheel Drive (RWD)

- 10.3 Front-wheel Drive (FWD)

- 10.4 Other Applications

11 Global Automotive E-Axle Market, By Geography

- 11.1 Introduction

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 Italy

- 11.3.4 France

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 Japan

- 11.4.2 China

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 New Zealand

- 11.4.6 South Korea

- 11.4.7 Rest of Asia Pacific

- 11.5 South America

- 11.5.1 Argentina

- 11.5.2 Brazil

- 11.5.3 Chile

- 11.5.4 Rest of South America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 Qatar

- 11.6.4 South Africa

- 11.6.5 Rest of Middle East & Africa

12 Key Developments

- 12.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 12.2 Acquisitions & Mergers

- 12.3 New Product Launch

- 12.4 Expansions

- 12.5 Other Key Strategies

13 Company Profiling

- 13.1 Robert Bosch GmbH

- 13.2 Magna International Inc.

- 13.3 Nidec Corporation

- 13.4 GKN Automotive Limited

- 13.5 Allison Transmission Inc.

- 13.6 Schaeffler AG

- 13.7 ZF Friedrichshafen AG

- 13.8 Dana Limited

- 13.9 Linamar Corporation

- 13.10 Vitesco Technologies Group AG

- 13.11 Meritor, Inc.

- 13.12 BorgWarner Inc.

- 13.13 Valeo SA

- 13.14 Continental AG

- 13.15 Siemens AG

- 13.16 Hitachi Automotive Systems

- 13.17 Mitsubishi Electric Corporation

- 13.18 Hyundai Mobis

- 13.19 JTEKT Corporation

- 13.20 Unipres Corporation