|

|

市場調査レポート

商品コード

1494826

石灰の世界市場:分析 - 製品別、流通チャネル別、用途別、エンドユーザー別、地域別、予測(~2030年)Lime Market Forecasts to 2030 - Global Analysis By Product (Quick Lime and Slaked/Hydrated Lime), Distribution Channel (Offline and Online), Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 石灰の世界市場:分析 - 製品別、流通チャネル別、用途別、エンドユーザー別、地域別、予測(~2030年) |

|

出版日: 2024年06月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

世界の石灰の市場規模は、2024年に507億5,000万米ドルに達し、予測期間中にCAGR 5.5%で成長し、2030年には699億8,000万米ドルに達すると予測されています。

石灰は基本的に、石灰石から調製され、主に化学添加物として利用される、大量かつ低コストの汎用鉱物です。石灰は酸化物と水酸化物からなるカルシウム含有無機鉱物で、主にアルカリ性です。

世界保健機関(WHO)によると、2025年までに世界人口の半数が水不足地域に住むようになるといいます。欧州石灰協会によると、鉄鋼産業は水酸化カルシウムの最大の消費者であり、現在、世界中で生産される製品の35%以上が利用されています。

最終用途産業からの需要の増加

最近、世界中で鉱物の生産が著しく伸びています。これは主に、鉄、鋼鉄、アルミナ、金、銀、銅、鉛などの製造過程で不純物を除去するために石灰が使用されるため、自動車、建設、海運、加工などの最終用途産業からの鉄および非鉄金属に対する需要が増加しているためです。

石灰の高いカーボンフットプリント

石灰は主に石灰岩から製造され、加熱して炭酸カルシウムから酸化カルシウムと二酸化炭素に分解します。製造過程で発生する二酸化炭素は、温室効果ガスのひとつで、いくつかの災害や地球温暖化を引き起こし、深刻な事態を招いています。さらに、生産は非常にエネルギー集約的なプロセスであり、産業全体の二酸化炭素排出量に拍車をかけています。

廃水リサイクルへの注目の高まり

有害な排出物や非効率な廃水処理によって産業が引き起こす汚染への懸念が高まっています。米国や西欧諸国などでは、産産業の廃水処理とリサイクルに関する規制を強化しています。インドや中国などの新興国も、水不足や地下水汚染に対処するため、工業用水のリサイクルに力を入れています。

石灰の貯蔵に関する懸念

水分の吸収と大気中の二酸化炭素の存在により、石灰は使用できないです。また、6ヶ月以上保管すると石灰の物理的・化学的特性が変化するため、保管期間の短さも石灰市場のメーカーが直面する大きな課題となっています。

COVID-19の影響:

COVID-19の大流行は石灰市場に大きな影響を与え、サプライチェーンの様々な段階で混乱を引き起こしました。操業停止や制限により石灰生産地では労働力不足が生じ、収穫や加工作業に影響が出ました。さらに、輸送手段の減少や港の閉鎖など、物流の課題も石灰の流通を妨げました。需要の変動も起こり、健康や免疫に対する消費者の関心の高まりにより当初は急増したが、その後、外食産業が閉鎖に苦しむにつれて減少しました。

予測期間中、生石灰部門が最大となる見込み

石灰市場における生石灰分野は、様々な産業で広く使用されているため、大きな成長を遂げています。生石灰は酸化カルシウムとしても知られ、不純物を除去するフラックスとして鉄鋼製造に広く使用されています。建設分野でも、土壌の安定化やセメントの主成分として生石灰が需要を牽引しています。水処理と廃水処理に生石灰の使用を義務付ける環境規制は、生石灰市場の成長をさらに後押ししています。さらに、化学工業におけるカルシウム化合物の生産や、農業における土壌改良の役割も需要の増加に寄与しており、生石灰は様々な産業用途において重要な成分となっています。

肥料・砂糖生産分野は予測期間中最も高いCAGRが見込まれる

肥料と砂糖生産分野は石灰市場成長の促進要因です。肥料生産において、石灰は土壌の酸性度を中和し、栄養分の利用可能性を高め、土壌構造を改善し、それによって作物の収量を高めるために不可欠です。この分野における石灰の需要は、世界の食糧需要を満たすために効率的な農法へのニーズが高まっていることから伸びています。新興国を中心とした世界の砂糖産業の拡大も、石灰消費量の増加に寄与しています。農業技術の進歩や世界の砂糖消費量の増加に支えられ、両者とも上昇基調を続けると予想されます。

最大のシェアを持つ地域

北米の石灰市場は、いくつかの要因によって大きな成長を遂げています。土壌安定化やアスファルト製造などの用途で石灰の主要消費者である建設産業は、インフラプロジェクトの増加により拡大しています。さらに、鉄鋼の浄化に石灰を使用する鉄鋼産業も復活しつつあります。排ガスを減らすために排煙脱硫に石灰の使用を促進する環境規制が需要をさらに押し上げています。農業部門も土壌の質と作物の収量を向上させるために石灰を利用し、市場の成長に貢献しています。技術の進歩と石灰生産能力の増強がこの増加傾向を支えており、需要増に対応した安定供給が確保されています。

CAGRが最も高い地域:

アジア太平洋は、中国、インド、東南アジア諸国などの急速な工業化と都市化によって、石灰市場が大きく成長しています。特にインフラ整備を中心とした建設産業の発展が、セメントやコンクリート製造の主な材料として石灰の需要を押し上げています。さらに、浄化プロセス用の石灰の主要な消費者である鉄鋼産業は、製造活動の増加により繁栄しています。廃水処理と排煙脱硫に石灰の使用を促進する環境規制は、市場の成長にさらに貢献しています。

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- 用途分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の石灰市場:製品別

- 生石灰

- 消石灰/水和石灰

第6章 世界の石灰市場:流通チャネル別

- オフライン

- オンライン

第7章 世界の石灰市場:用途別

- パルプ・紙

- ガラス

- セメント

- 環境

- 排煙脱硫

- 汚泥

- 畜産廃棄物

- 有害廃棄物

- 肥料・砂糖生産

- その他の用途

第8章 世界の石灰市場:エンドユーザー別

- 建設

- 農業

- 鉱業・冶金

- 鋼鉄

- 非鉄金属

- 鉄

- 化学薬品

- 廃水処理

- 産業

- その他のエンドユーザー

第9章 世界の石灰市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他のアジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他の中東・アフリカ

第10章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第11章 企業プロファイリング

- Adbri

- Boral Limited

- Carmeuse

- CSR Limited

- Graymont Limited

- Imerys

- Lhoist

- Linwood Mining & Minerals Corp.

- Louisiana-Pacific

- Mississippi Lime Company

- Nordkalk

- Pete Lien & Sons, Inc.

- Shandong Zhongxin Calcium Industry Co., Ltd.

- Sibelco Ltd.

- United States Lime & Minerals Inc.

- Valley Minerals LLC

- Wagners

List of Tables

- Table 1 Global Lime Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Lime Market Outlook, By Product (2022-2030) ($MN)

- Table 3 Global Lime Market Outlook, By Quick Lime (2022-2030) ($MN)

- Table 4 Global Lime Market Outlook, By Slaked/Hydrated Lime (2022-2030) ($MN)

- Table 5 Global Lime Market Outlook, By Distribution Channel (2022-2030) ($MN)

- Table 6 Global Lime Market Outlook, By Offline (2022-2030) ($MN)

- Table 7 Global Lime Market Outlook, By Online (2022-2030) ($MN)

- Table 8 Global Lime Market Outlook, By Application (2022-2030) ($MN)

- Table 9 Global Lime Market Outlook, By Pulp & Paper (2022-2030) ($MN)

- Table 10 Global Lime Market Outlook, By Glass (2022-2030) ($MN)

- Table 11 Global Lime Market Outlook, By Cement (2022-2030) ($MN)

- Table 12 Global Lime Market Outlook, By Environment (2022-2030) ($MN)

- Table 13 Global Lime Market Outlook, By Flue Gas Desulfurization (2022-2030) ($MN)

- Table 14 Global Lime Market Outlook, By Sludge (2022-2030) ($MN)

- Table 15 Global Lime Market Outlook, By Animal Waste (2022-2030) ($MN)

- Table 16 Global Lime Market Outlook, By Hazardous Wastes (2022-2030) ($MN)

- Table 17 Global Lime Market Outlook, By Fertilizer & Sugar Production (2022-2030) ($MN)

- Table 18 Global Lime Market Outlook, By Other Applications (2022-2030) ($MN)

- Table 19 Global Lime Market Outlook, By End User (2022-2030) ($MN)

- Table 20 Global Lime Market Outlook, By Construction (2022-2030) ($MN)

- Table 21 Global Lime Market Outlook, By Agriculture (2022-2030) ($MN)

- Table 22 Global Lime Market Outlook, By Mining and Metallurgy (2022-2030) ($MN)

- Table 23 Global Lime Market Outlook, By Steel (2022-2030) ($MN)

- Table 24 Global Lime Market Outlook, By Nonferrous Metal (2022-2030) ($MN)

- Table 25 Global Lime Market Outlook, By Iron (2022-2030) ($MN)

- Table 26 Global Lime Market Outlook, By Chemical (2022-2030) ($MN)

- Table 27 Global Lime Market Outlook, By Waste-Water Treatment (2022-2030) ($MN)

- Table 28 Global Lime Market Outlook, By Industrial (2022-2030) ($MN)

- Table 29 Global Lime Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Lime Market is accounted for $50.75 billion in 2024 and is expected to reach $69.98 billion by 2030 growing at a CAGR of 5.5% during the forecast period. Lime is basically a high-volume and low-cost commodity mineral that is prepared from limestone and mainly utilized as a chemical additive. It is a calcium-containing inorganic mineral composed of oxide and hydroxide compounds and is primarily alkaline in nature.

According to the World Health Organization (WHO), by 2025, half of the world's population will be living in water-stressed areas. According to the European Lime Association, the steel industry is the largest consumer of calcium hydroxide and currently utilizes more than 35% of the product produced worldwide.

Market Dynamics:

Driver:

Increasing demand from end use industries

There has been significant growth in the production of minerals across the globe in the recent past. This can be mainly attributed to the increasing demand for ferrous and non-ferrous metals from several end-use industries such as automotive, construction, shipping and fabrication, among others as lime is mainly used to eliminate impurities during the manufacturing process of iron, steel, alumina, gold, silver, copper and lead, among other metals.

Restraint:

High carbon footprint of lime

Lime is primarily manufactured from limestone, wherein it is heated to break from calcium carbonate to calcium oxide and carbon dioxide. The CO2 generated during the production process is one of the greenhouse gases that have led to several calamities and global warming while leading to drastic consequences. Furthermore, production is a highly energy-intensive process and adds to the industry's overall carbon footprint.

Opportunity:

The growing focus on wastewater recycling

There is growing concern about pollution caused by industries by way of harmful emissions and ineffective wastewater treatment. Countries such as the US and those in Western Europe are enforcing regulations on wastewater treatment and recycling among industries. Emerging countries such as India and China are also focusing on industrial water recycling to counter water scarcity and groundwater pollution.

Threat:

Storage concerns of lime

The absorption of moisture and presence of carbon dioxide in the atmosphere makes lime incompatible for use. Along with this, less storage time is a major challenge faced by manufacturers in the lime market as the physical and chemical characteristics of lime change when it is stored for more than six months.

Covid-19 Impact:

The COVID-19 pandemic significantly impacted the lime market, causing disruptions across various stages of the supply chain. Lockdowns and restrictions led to labor shortages in lime-producing regions, affecting harvesting and processing operations. Additionally, logistical challenges, including reduced transportation options and port closures, hampered the distribution of limes. Demand fluctuations also occurred, with an initial surge due to increased consumer focus on health and immunity, followed by a decline as the foodservice sector suffered from closures.

The quick lime segment is expected to be the largest during the forecast period

The quick lime segment in the lime market is experiencing significant growth due to its widespread application across various industries. Quick lime, also known as calcium oxide, is extensively used in steel manufacturing, where it serves as a flux to remove impurities. The construction sector also drives demand, utilizing quick lime for soil stabilization and as a key ingredient in cement. Environmental regulations mandating the use of quick lime in water and wastewater treatment further bolster its market growth. Additionally, its role in the chemical industry for producing calcium compounds and in agriculture for soil conditioning contributes to the rising demand, making quick lime a critical component in diverse industrial applications.

The fertilizer & sugar production segment is expected to have the highest CAGR during the forecast period

The fertilizer and sugar production segments are significant drivers of growth in the lime market. In fertilizer production, lime is essential for neutralizing soil acidity, enhancing nutrient availability, and improving soil structure, thereby boosting crop yields. The demand for lime in this sector is growing due to the rising need for efficient agricultural practices to meet global food demand. The expansion of the global sugar industry, particularly in emerging economies, is contributing to increased lime consumption. Both are expected to continue their upward trajectory, supported by advancements in agricultural technologies and rising sugar consumption worldwide.

Region with largest share:

The lime market in North America is experiencing significant growth, driven by several factors. The construction industry, a major consumer of lime for applications such as soil stabilization and asphalt production, is expanding due to increased infrastructure projects. Additionally, the steel industry, which uses lime for purifying steel, is seeing resurgence. Environmental regulations promoting the use of lime in flue gas desulfurization to reduce emissions further boost demand. The agricultural sector also contributes to market growth, utilizing lime to improve soil quality and crop yields. Technological advancements and increased lime production capacities are supporting this upward trend, ensuring a steady supply to meet the rising demand.

Region with highest CAGR:

The Asia-Pacific region is experiencing significant growth in the lime market, driven by rapid industrialization and urbanization in countries like China, India, and Southeast Asian nations. The construction industry's expansion, particularly in infrastructure development, is boosting the demand for lime as a key material in cement and concrete production. Additionally, the steel industry, a major consumer of lime for purification processes, is flourishing due to increased manufacturing activities. Environmental regulations promoting the use of lime for wastewater treatment and flue gas desulfurization are further contributing to market growth.

Key players in the market

Some of the key players in Lime market include Adbri, Boral Limited, Carmeuse, CSR Limited, Graymont Limited, Imerys, Lhoist, Linwood Mining & Minerals Corp., Louisiana-Pacific, Mississippi Lime Company, Nordkalk, Pete Lien & Sons, Inc., Shandong Zhongxin Calcium Industry Co., Ltd., Sibelco Ltd., United States Lime & Minerals Inc., Valley Minerals LLC and Wagners.

Key Developments:

In May 2024, at the in-cosmetics show in Paris, Imerys has showcased its mineral-based solutions for the personal care industry. The company has highlighted two new product developments for make-up and toiletries. Among the new products presented at in-cosmetics, Imerys highlighted the use of ImerCare 400D, previously launched as an absorption agent, as a mattifying agent for lipsticks and a natural alternative to synthetic silica.

In October 2023, Sweden-based OX2 and Finland-based Nordkalk have announced plans to jointly investigate the opportunities for the production of e-fuel on Gotland, Sweden. Specifically, the parties will initiate a pilot study on how a facility should be planned, how the use of the area can be maximized and how the harbor of Storugns can be developed.

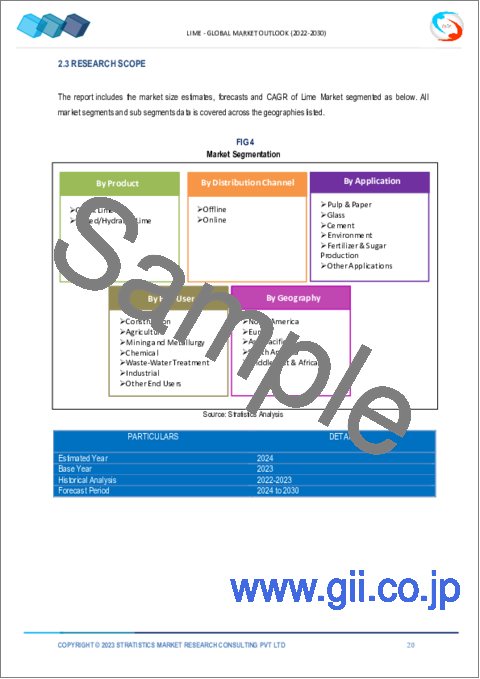

Products Covered:

- Quick Lime

- Slaked/Hydrated Lime

Distribution Channels Covered:

- Offline

- Online

Applications Covered:

- Pulp & Paper

- Glass

- Cement

- Environment

- Fertilizer & Sugar Production

- Other Applications

End Users Covered:

- Construction

- Agriculture

- Mining and Metallurgy

- Chemical

- Waste-Water Treatment

- Industrial

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Lime Market, By Product

- 5.1 Introduction

- 5.2 Quick Lime

- 5.3 Slaked/Hydrated Lime

6 Global Lime Market, By Distribution Channel

- 6.1 Introduction

- 6.2 Offline

- 6.3 Online

7 Global Lime Market, By Application

- 7.1 Introduction

- 7.2 Pulp & Paper

- 7.3 Glass

- 7.4 Cement

- 7.5 Environment

- 7.5.1 Flue Gas Desulfurization

- 7.5.2 Sludge

- 7.5.3 Animal Waste

- 7.5.4 Hazardous Wastes

- 7.6 Fertilizer & Sugar Production

- 7.7 Other Applications

8 Global Lime Market, By End User

- 8.1 Introduction

- 8.2 Construction

- 8.3 Agriculture

- 8.4 Mining and Metallurgy

- 8.4.1 Steel

- 8.4.2 Nonferrous Metal

- 8.4.3 Iron

- 8.5 Chemical

- 8.6 Waste-Water Treatment

- 8.7 Industrial

- 8.8 Other End Users

9 Global Lime Market, By Geography

- 9.1 Introduction

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 Italy

- 9.3.4 France

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 New Zealand

- 9.4.6 South Korea

- 9.4.7 Rest of Asia Pacific

- 9.5 South America

- 9.5.1 Argentina

- 9.5.2 Brazil

- 9.5.3 Chile

- 9.5.4 Rest of South America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 Qatar

- 9.6.4 South Africa

- 9.6.5 Rest of Middle East & Africa

10 Key Developments

- 10.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 10.2 Acquisitions & Mergers

- 10.3 New Product Launch

- 10.4 Expansions

- 10.5 Other Key Strategies

11 Company Profiling

- 11.1 Adbri

- 11.2 Boral Limited

- 11.3 Carmeuse

- 11.4 CSR Limited

- 11.5 Graymont Limited

- 11.6 Imerys

- 11.7 Lhoist

- 11.8 Linwood Mining & Minerals Corp.

- 11.9 Louisiana-Pacific

- 11.10 Mississippi Lime Company

- 11.11 Nordkalk

- 11.12 Pete Lien & Sons, Inc.

- 11.13 Shandong Zhongxin Calcium Industry Co., Ltd.

- 11.14 Sibelco Ltd.

- 11.15 United States Lime & Minerals Inc.

- 11.16 Valley Minerals LLC

- 11.17 Wagners