|

|

市場調査レポート

商品コード

1462716

軍用ロボット自律システム市場の2030年までの予測:製品タイプ、技術、用途、エンドユーザー、地域別の世界分析Military Robotics Autonomous Systems Market Forecasts to 2030 - Global Analysis By Product Type, Technology, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 軍用ロボット自律システム市場の2030年までの予測:製品タイプ、技術、用途、エンドユーザー、地域別の世界分析 |

|

出版日: 2024年04月04日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の軍用ロボット自律システム市場は2023年に98億米ドルを占め、予測期間中にCAGR 15.0%で成長し、2030年には260億米ドルに達すると予測されています。

軍用ロボット自律システムは、防衛用途に設計された無人車両とプラットフォームの範囲を包含します。これらのシステムは、単独または半独立で動作し、監視、偵察、ロジスティクス、戦闘などのタスクを実行します。高度なセンサー、AI、通信技術を備え、多様な地形を航行し、情報を収集し、正確に目標を捕捉します。無人航空機(UAV)から地上ベースのドローンや自律走行車に至るまで、これらのシステムは状況認識を強化し、人的リスクを低減し、作戦能力を拡張します。

ロボット工学、人工知能(AI)、センサー技術の急速な進歩

AIアルゴリズムの進歩により、軍事用ロボットはリアルタイムの意思決定を行い、ダイナミックな環境に適応し、複雑なタスクを自律的に実行できるようになり、作戦の有効性が高まる。さらにロボット工学とAI技術は、反復作業を自動化し、人的ミスを減らし、応答時間を改善することで軍事作戦を合理化し、最終的に防衛任務の効率を高める。このように、危険な環境に自律型システムを配備することで、軍は人命へのリスクを最小限に抑えることができます。ロボットは危険な地域での爆弾処理、地雷除去、偵察などの作業を引き受けることができるため、市場の成長を後押ししています。

高い開発・配備コスト

こうしたシステムの開発・配備には高いコストがかかるため、国防予算が少ない国や国家にとっては利用が制限される可能性があり、財源が異なる国家間で軍事能力に格差が生じる可能性があります。国防予算は有限であり、軍用ロボット自律システムに必要な多額の財政支出は、他の重要な国防優先事項から資金を流用し、即応性、訓練、または人員に影響を与える可能性があります。さらに、高い参入コストが市場内の技術革新と競争を阻害し、市場を阻害する新技術の出現を制限する可能性もあります。

地政学的緊張と安全保障上の脅威

地政学的緊張の高まりと安全保障上の脅威は、しばしば国家に防衛能力の強化を促し、軍用ロボット自律システムの需要増につながります。各国政府は、軍事態勢を強化し、潜在的な敵対勢力を抑止し、国境、海上境界線、領土保全の監視と安全を確保するための無人航空機(UAV)や無人地上車両(UGV)など、戦略的優位性を維持するための先進技術を求めています。このように地政学的緊張の高まりは国家間の軍拡競争を引き起こし、軍用ロボット自律システムの開発と配備における競争の激化につながり、市場の成長を後押しします。

自律型兵器システムは倫理的懸念を引き起こす

自律型兵器の倫理的意味合いに対する懸念から、各国政府はその開発、配備、輸出に厳しい規制を課したり、禁止措置を取ったりする可能性があります。これは、軍事用ロボット企業の市場機会を制限し、自律型システムの技術革新を阻害する可能性があります。また、顧客、投資家、利害関係者からの信頼を失い、事業の見通しや市場競争に影響を与える可能性もあります。さらに、自律型兵器が関係する事件や事故に関連する法的措置、訴訟、賠償請求は、メーカーに財政的な影響や法的結果をもたらす可能性があります。

COVID-19の影響

サプライチェーンを混乱させ、生産を遅延させ、実地試験や配備を妨げ、景気後退による予算の制約が自律システムの調達や投資を鈍らせる可能性があります。しかし、パンデミック(世界的大流行)により、人手への依存を減らす上での自律型技術の重要性も浮き彫りになり、監視、偵察、ロジスティクス用の無人システムに対する需要が高まる可能性もあります。各国が将来の危機に直面した際の回復力と適応力の強化を模索する中で、遠隔操作と無人化能力が軍事戦略で脚光を浴びるようになるかもしれないです。

予測期間中、無人航空機(UAV)分野が最大になる見込み

無人航空機(UAV)セグメントは、軍事作戦における無人航空機の使用増加により、自律システム市場の成長を牽引し、有利な成長を遂げると推定されます。高度なセンサー、AI、通信技術を搭載した無人航空機の需要は、自律能力の開発と展開を後押しします。さらに、無人航空機は監視、偵察、情報収集、目標捕捉、攻撃任務など幅広い任務能力を提供します。その多用途性により、特定の任務要件に合わせた自律システムの需要が高まっています。

予測期間中、情報・監視・偵察(ISR)分野のCAGRが最も高くなると予想されます。

諜報・監視・偵察(ISR)分野は、リアルタイムでの情報収集、処理、発信が可能な自律型システムの需要により、予測期間中に最も高いCAGR成長が見込まれます。これには、高度なセンサーとAIを搭載した無人航空機(UAV)、地上ロボット、海上ドローンが含まれます。さらに自律型ISRシステムは、遠隔地や敵対的な環境での情報収集のために迅速に配備することができ、人的リスクを軽減することができます。この俊敏性と柔軟性が、軍事的対応力と作戦の有効性を高め、市場の成長を後押ししています。

最大のシェアを占める地域:

中国、インド、日本、韓国、オーストラリアなど、アジア太平洋地域の複数の国々が軍隊の近代化のために国防支出を強化しているため、予測期間中、アジア太平洋地域が最大の市場シェアを占めると予測されます。この投資の増加は、軍用ロボット自律システムの調達機会を生み出します。アジア太平洋地域には広大な海洋領域があることから、海軍は海洋監視、機雷対策、対潜水艦戦に自律システムを活用するようになっており、無人海上車両(UMV)の需要を牽引しています。

CAGRが最も高い地域:

北米、特に米国は軍事技術革新の世界的リーダーであるため、予測期間中のCAGRは北米が最も高いと予測されます。この地域は、防衛請負業者、テクノロジー企業、研究機関、政府機関が軍用ロボット自律システムの進歩を推進する強固なエコシステムを誇っています。さらに、北米の政府機関は、さまざまなプログラムやイニシアチブを通じて軍用ロボット自律システムの開発と調達を支援しており、この地域の市場を後押ししています。

無料のカスタマイズ提供:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかを提供させていただきます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査資料

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- テクノロジー分析

- アプリケーション分析

- エンドユーザー分析

- 新興市場

- COVID-19症の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の軍用ロボット自律システム市場:製品タイプ

- 航空無人機(UAV)

- 地上無人機(UGV)

- 無人潜水機(UUV)

- その他の製品タイプ

第6章 世界の軍用ロボット自律システム市場:技術別

- コンピュータビジョン

- センサーフュージョン

- 機械学習(ML)

- 人工知能(AI)

- その他のテクノロジー

第7章 世界の軍用ロボット自律システム市場:用途別

- 爆発物処理(EOD)

- 国境と海上安全保障

- 戦闘支援

- 情報・監視・偵察(ISR)

- 目標捕捉と火力支援

- 災害対応と人道支援

- その他の用途

第8章 世界の軍用ロボット自律システム市場:エンドユーザー別

- 空軍

- 陸軍

- 海軍

- 緊急管理機関

- その他のエンドユーザー

第9章 世界の軍用ロボット自律システム市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第10章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第11章 企業プロファイリング

- AeroVironment, Inc.

- BAE Systems

- Boston Dynamics

- Cobham Plc

- Elbit Systems Ltd

- Endeavor Robotics

- General Dynamics Corporation

- Irobot

- Israel Aerospace Industries

- L3Harris Technologies

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- QinetiQ

- SAAB AB

- SAfran

- Teledyne FLIR LLC

- Thales Group

- Turkish Aerospace Industries Inc.

List of Tables

- Table 1 Global Military Robotics Autonomous Systems Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Military Robotics Autonomous Systems Market Outlook, By Product Type (2021-2030) ($MN)

- Table 3 Global Military Robotics Autonomous Systems Market Outlook, By Unmanned Aerial Vehicles (UAVs) (2021-2030) ($MN)

- Table 4 Global Military Robotics Autonomous Systems Market Outlook, By Unmanned Ground Vehicles (UGVs) (2021-2030) ($MN)

- Table 5 Global Military Robotics Autonomous Systems Market Outlook, By Unmanned Underwater Vehicles (UUVs) (2021-2030) ($MN)

- Table 6 Global Military Robotics Autonomous Systems Market Outlook, By Other Product Types (2021-2030) ($MN)

- Table 7 Global Military Robotics Autonomous Systems Market Outlook, By Technology (2021-2030) ($MN)

- Table 8 Global Military Robotics Autonomous Systems Market Outlook, By Computer Vision (2021-2030) ($MN)

- Table 9 Global Military Robotics Autonomous Systems Market Outlook, By Sensor Fusion (2021-2030) ($MN)

- Table 10 Global Military Robotics Autonomous Systems Market Outlook, By Machine Learning (ML) (2021-2030) ($MN)

- Table 11 Global Military Robotics Autonomous Systems Market Outlook, By Artificial Intelligence (AI) (2021-2030) ($MN)

- Table 12 Global Military Robotics Autonomous Systems Market Outlook, By Other Technologies (2021-2030) ($MN)

- Table 13 Global Military Robotics Autonomous Systems Market Outlook, By Application (2021-2030) ($MN)

- Table 14 Global Military Robotics Autonomous Systems Market Outlook, By Explosive Ordnance Disposal (EOD) (2021-2030) ($MN)

- Table 15 Global Military Robotics Autonomous Systems Market Outlook, By Border & Maritime Security (2021-2030) ($MN)

- Table 16 Global Military Robotics Autonomous Systems Market Outlook, By Combat Support (2021-2030) ($MN)

- Table 17 Global Military Robotics Autonomous Systems Market Outlook, By Intelligence, Surveillance, & Reconnaissance (ISR) (2021-2030) ($MN)

- Table 18 Global Military Robotics Autonomous Systems Market Outlook, By Target Acquisition & Fire Support (2021-2030) ($MN)

- Table 19 Global Military Robotics Autonomous Systems Market Outlook, By Disaster Response & Humanitarian Assistance (2021-2030) ($MN)

- Table 20 Global Military Robotics Autonomous Systems Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 21 Global Military Robotics Autonomous Systems Market Outlook, By End User (2021-2030) ($MN)

- Table 22 Global Military Robotics Autonomous Systems Market Outlook, By Air Force (2021-2030) ($MN)

- Table 23 Global Military Robotics Autonomous Systems Market Outlook, By Army (2021-2030) ($MN)

- Table 24 Global Military Robotics Autonomous Systems Market Outlook, By Navy (2021-2030) ($MN)

- Table 25 Global Military Robotics Autonomous Systems Market Outlook, By Emergency Management Agencies (2021-2030) ($MN)

- Table 26 Global Military Robotics Autonomous Systems Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Military Robotics Autonomous Systems Market is accounted for $9.8 billion in 2023 and is expected to reach $26.0 billion by 2030 growing at a CAGR of 15.0% during the forecast period. Military robotics autonomous systems encompass a range of unmanned vehicles and platforms designed for defense applications. These systems operate independently or semi-independently, executing tasks such as surveillance, reconnaissance, logistics, and combat. Equipped with advanced sensors, AI, and communication technologies, they navigate diverse terrains, gather intelligence, and engage targets with precision. From unmanned aerial vehicles (UAVs) to ground-based drones and autonomous vehicles, these systems offer enhanced situational awareness, reduce risk to human personnel, and extend operational capabilities.

Market Dynamics:

Driver:

Rapid progress in robotics, artificial intelligence (AI), and sensor technologies

Advancements in AI algorithms enable military robots to make real-time decisions, adapt to dynamic environments, and perform complex tasks autonomously, thereby enhancing their operational effectiveness. Further robotics and AI technologies streamline military operations by automating repetitive tasks, reducing human error, and improving response times, ultimately increasing the efficiency of defense missions. Thus, by deploying autonomous systems in hazardous environments, militaries can minimize the risk to human lives, as robots can undertake tasks such as bomb disposal, mine clearance, and reconnaissance in dangerous areas drive the growth of the market.

Restraint:

High development and deployment costs

The high costs of developing and deploying these systems may limit accessibility for smaller defense budgets or nations, potentially creating disparities in military capabilities between nations with varying financial resources. Defense budgets are finite, and the significant financial commitment required for military robotics autonomous systems may divert funds from other critical defense priorities, potentially impacting readiness, training, or personnel. Further, high entry costs may discourage innovation and competition within the market, limiting the emergence of new technologies hampering the market.

Opportunity:

Geopolitical tensions and security threats

Heightened geopolitical tensions and security threats often prompt nations to bolster their defense capabilities, leading to increased demand for military robotics autonomous systems. Governments seek advanced technologies to enhance their military readiness, deter potential adversaries, and maintain strategic superiority such as unmanned aerial vehicles (UAVs) and unmanned ground vehicles (UGVs) for monitoring and securing borders, maritime boundaries, and territorial integrity. Thus heightened geopolitical tensions can trigger an arms race among nations, leading to increased competition in the development and deployment of military robotics autonomous systems propelling the market growth.

Threat:

Autonomous weapons systems raise ethical concerns

Concerns about the ethical implications of autonomous weapons may prompt governments to impose stringent regulations or even bans on their development, deployment, or export. This could limit the market opportunities for military robotics companies and stifle innovation in autonomous systems and could also lead to loss of trust from customers, investors, and stakeholders, impacting their business prospects and competitiveness. Moreover legal actions, lawsuits, and compensation claims related to incidents or accidents involving autonomous weapons could have financial repercussions and legal consequences for manufacturers.

Covid-19 Impact

Disrupting supply chains, delaying production, and hindering field trials and deployments, budgetary constraints caused by economic downturns may slow procurement and investment in autonomous systems. However, the pandemic has also highlighted the importance of autonomous technologies in reducing reliance on human personnel, potentially driving increased demand for unmanned systems for surveillance, reconnaissance, and logistics. Remote operations and unmanned capabilities may gain prominence in military strategies as nations seek to enhance resilience and adaptability in the face of future crises.

The unmanned aerial vehicles (UAVs) segment is expected to be the largest during the forecast period

The unmanned aerial vehicles (UAVs) segment is estimated to have a lucrative growth, due to the increasing use of unmanned aerial vehicles in military operations drives growth in the autonomous systems market. Demand for unmanned aerial vehicles equipped with advanced sensors, AI, and communication technologies boosts development and deployment of autonomous capabilities. Moreover, unmanned aerial vehicles offer a wide range of mission capabilities, including surveillance, reconnaissance, intelligence gathering, target acquisition, and strike missions. Their versatility drives demand for autonomous systems tailored to specific mission requirements.

The intelligence, surveillance, & reconnaissance (ISR) segment is expected to have the highest CAGR during the forecast period

The intelligence, surveillance, & reconnaissance (ISR) segment is anticipated to witness the highest CAGR growth during the forecast period, owing to demand for autonomous systems capable of gathering, processing, and disseminating intelligence in real-time. This includes unmanned aerial vehicles (UAVs), ground-based robots, and maritime drones equipped with advanced sensors and AI. Further the autonomous ISR systems can be rapidly deployed to gather intelligence in remote or hostile environments, reducing the risk to human personnel. This agility and flexibility enhance military responsiveness and operational effectiveness encourage the market growth.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period owing to the several countries in the Asia Pacific region, including China, India, Japan, South Korea, and Australia, are ramping up their defense spending to modernize their armed forces. This increased investment creates opportunities for the procurement of military robotics autonomous systems. Given the vast maritime domains in the Asia Pacific region, navies are increasingly utilizing autonomous systems for maritime surveillance, mine countermeasures, and anti-submarine warfare, driving demand for unmanned maritime vehicles (UMVs).

Region with highest CAGR:

North America is projected to have the highest CAGR over the forecast period, because North America, particularly the United States, is a global leader in military technology innovation. The region boasts a robust ecosystem of defense contractors, technology companies, research institutions, and government agencies driving advancements in military robotics autonomous systems. Moreover, government agencies in North America support the development and procurement of military robotics autonomous systems through various programs and initiatives boosts the market in this region.

Key players in the market

Some of the key players in the Military Robotics Autonomous Systems Market include AeroVironment, Inc., BAE Systems, Boston Dynamics, Cobham Plc, Elbit Systems Ltd, Endeavor Robotics, General Dynamics Corporation, iRobot Corporation, Israel Aerospace Industries, L3Harris Technologies, Lockheed Martin Corporation , Northrop Grumman Corporation, QinetiQ, SAAB AB, SAfran, Teledyne FLIR LLC, Thales Group and Turkish Aerospace Industries Inc.

Key Developments:

In March 2024, BAE Systems launches MethaneSAT satellite to provide critical global greenhouse gas emissions data. The satellite will provide the public with reliable scientific data about the sources and scale of methane emissions globally, with the ultimate goal of driving reductions in the near future.

In February 2024, BAE Systems signs a 15 year support agreement for the Danish CV90 fleet. The agreement covers repair and maintenance services for the Danish Army's fleet of 44 CV90s, such as the delivery of spare parts at a time when the service's operational tempo remains at a high level.

In January 2024, AeroVironment, Inc. announced the first successful multi-drop, live fire GPS-guided Shryke munitions from the VAPOR(R) 55 MX, all-electric unmanned aircraft system in collaboration with Corvid and L3Harris Technologies.

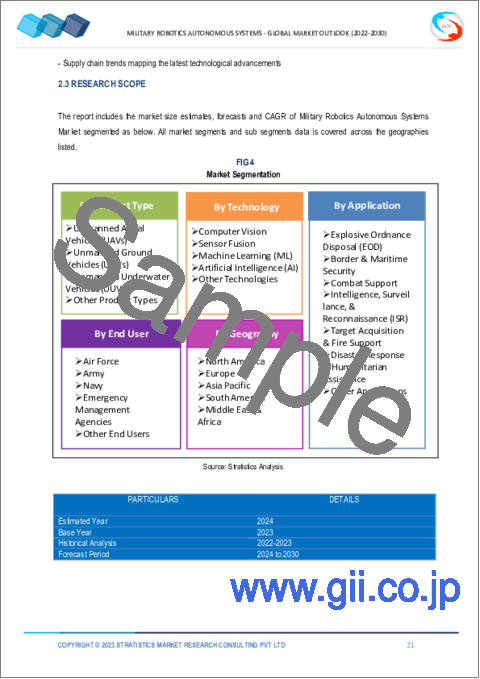

Product Types Covered:

- Unmanned Aerial Vehicles (UAVs)

- Unmanned Ground Vehicles (UGVs)

- Unmanned Underwater Vehicles (UUVs)

- Other Product Types

Technologies Covered:

- Computer Vision

- Sensor Fusion

- Machine Learning (ML)

- Artificial Intelligence (AI)

- Other Technologies

Applications Covered:

- Explosive Ordnance Disposal (EOD)

- Border & Maritime Security

- Combat Support

- Intelligence, Surveillance, & Reconnaissance (ISR)

- Target Acquisition & Fire Support

- Disaster Response & Humanitarian Assistance

- Other Applications

End Users Covered:

- Air Force

- Army

- Navy

- Emergency Management Agencies

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Technology Analysis

- 3.8 Application Analysis

- 3.9 End User Analysis

- 3.10 Emerging Markets

- 3.11 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Military Robotics Autonomous Systems Market, By Product Type

- 5.1 Introduction

- 5.2 Unmanned Aerial Vehicles (UAVs)

- 5.3 Unmanned Ground Vehicles (UGVs)

- 5.4 Unmanned Underwater Vehicles (UUVs)

- 5.5 Other Product Types

6 Global Military Robotics Autonomous Systems Market, By Technology

- 6.1 Introduction

- 6.2 Computer Vision

- 6.3 Sensor Fusion

- 6.4 Machine Learning (ML)

- 6.5 Artificial Intelligence (AI)

- 6.6 Other Technologies

7 Global Military Robotics Autonomous Systems Market, By Application

- 7.1 Introduction

- 7.2 Explosive Ordnance Disposal (EOD)

- 7.3 Border & Maritime Security

- 7.4 Combat Support

- 7.5 Intelligence, Surveillance, & Reconnaissance (ISR)

- 7.6 Target Acquisition & Fire Support

- 7.7 Disaster Response & Humanitarian Assistance

- 7.8 Other Applications

8 Global Military Robotics Autonomous Systems Market, By End User

- 8.1 Introduction

- 8.2 Air Force

- 8.3 Army

- 8.4 Navy

- 8.5 Emergency Management Agencies

- 8.6 Other End Users

9 Global Military Robotics Autonomous Systems Market, By Geography

- 9.1 Introduction

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 Italy

- 9.3.4 France

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 New Zealand

- 9.4.6 South Korea

- 9.4.7 Rest of Asia Pacific

- 9.5 South America

- 9.5.1 Argentina

- 9.5.2 Brazil

- 9.5.3 Chile

- 9.5.4 Rest of South America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 Qatar

- 9.6.4 South Africa

- 9.6.5 Rest of Middle East & Africa

10 Key Developments

- 10.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 10.2 Acquisitions & Mergers

- 10.3 New Product Launch

- 10.4 Expansions

- 10.5 Other Key Strategies

11 Company Profiling

- 11.1 AeroVironment, Inc.

- 11.2 BAE Systems

- 11.3 Boston Dynamics

- 11.4 Cobham Plc

- 11.5 Elbit Systems Ltd

- 11.6 Endeavor Robotics

- 11.7 General Dynamics Corporation

- 11.8 Irobot

- 11.9 Israel Aerospace Industries

- 11.10 L3Harris Technologies

- 11.11 Lockheed Martin Corporation

- 11.12 Northrop Grumman Corporation

- 11.13 QinetiQ

- 11.14 SAAB AB

- 11.15 SAfran

- 11.16 Teledyne FLIR LLC

- 11.17 Thales Group

- 11.18 Turkish Aerospace Industries Inc.