|

|

市場調査レポート

商品コード

1453971

防曇フィルムおよびシートの2030年までの世界市場予測:材料タイプ別、厚さ別、技術別、用途別、エンドユーザー別、地域別分析Anti-fog Films & Sheets Market Forecasts to 2030 - Global Analysis By Material Type, By Thickness, Technology, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 防曇フィルムおよびシートの2030年までの世界市場予測:材料タイプ別、厚さ別、技術別、用途別、エンドユーザー別、地域別分析 |

|

出版日: 2024年03月03日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の防曇フィルムおよびシート市場は2023年に37億米ドルを占め、予測期間中のCAGRは6.1%で成長し、2030年には56億米ドルに達する見込みです。

防曇フィルムおよびシートは、表面の結露や曇りを防ぎ、透明性と視認性を確保するために設計された透明素材です。これらのフィルムは通常、水分を吸収し、表面張力を低下させ、水滴の形成を防ぐ特殊コーティングや添加剤を備えています。防曇フィルムは、包装、光学レンズ、自動車窓、温室などの用途に広く使用されており、透明な視界を維持することで安全性を向上させ、製品のプレゼンテーションを強化します。

食品包装業界の成長

世界中でパッケージングされた食品の需要が増加する中、メーカーは製品のプレゼンテーションと保存性を高めるために先進パッケージング・ソリューションを採用しています。防曇フィルムと防曇シートは、視認性を維持し、包装表面の結露を防止して、消費者がパッケージの内容物をはっきりと確認できるようにする上で重要な役割を果たしています。これは消費者へのアピール、食品の安全性、パッケージング全体の性能向上に貢献し、市場の成長を促進します。

高い製造コスト

このような特殊フィルムの製造プロセスには、望ましい防曇特性を実現するための高度な材料と技術が組み込まれています。これには、結露を効果的に防止するための特殊コーティング、添加剤、処理剤の使用が含まれます。このような材料や工程は割高になることが多く、製造コストを押し上げます。その結果、生産コストが高いため、製造業者やエンドユーザーにとって、防曇フィルムやシートの入手しやすさや利用しやすさが制限され、市場成長への課題となっています。

バイオベースの防曇フィルムの開発

バイオベースの防曇フィルムの開拓は、防曇フィルムおよびシート市場に大きなチャンスをもたらします。持続可能性が世界中の産業で重要な焦点となるにつれ、従来の石油ベースの材料に代わる環境に優しい材料への需要が高まっています。植物由来のポリマーや生分解性材料など再生可能な資源に由来するバイオベースフィルムは、環境への影響やカーボンフットプリントを低減します。さらに、持続可能な製品に対する消費者の嗜好の高まりに対応しているため、市場の成長を促進し、環境に優しい防曇ソリューションの採用を拡大しています。

曇り止めフィルムに関する限られた認識

結露を防ぎ視界を確保するという利点があるにもかかわらず、多くの消費者や企業は防曇フィルムの存在や利点を認識していない可能性があります。この認知度の低さは、潜在顧客が従来の素材を選んだり、防曇ソリューションの必要性を見落としたりする可能性があり、市場成長の妨げとなります。さらに、十分な教育と宣伝がなければ、メーカーは製品の差別化と市場シェアの獲得に苦戦するかもしれないです。

COVID-19の影響:

COVID-19の流行は、防曇フィルムおよびシート市場にさまざまな影響を与えました。食品や医療用品のような必需品の包装における防曇フィルムの需要は増加したが、製造やサプライチェーンの混乱は生産と流通の課題につながっています。さらに、特定の分野における個人消費の減少が、非必需品に対する需要全体を減退させ、市場の成長軌道に影響を及ぼしています。

予測期間中、食品包装用フィルム分野が最大になる見込み

食品包装用フィルム分野は、利便性、都市化、消費者のライフスタイルの変化などの要因によって、包装された食品の需要が増加しているため、予測期間中、防曇フィルムおよびシート市場を独占すると予測されます。防曇フィルムは、包装表面の結露や曇りを防止することで、製品の視認性と品質を維持する上で重要な役割を果たしています。食品の安全性と衛生に対する意識の高まりにより、食品包装における防曇フィルムの需要は引き続き高いと予想されます。

ヘルスケア分野は予測期間中に最も高いCAGRが見込まれる

防曇フィルムおよびシート市場では、ヘルスケア分野が予測期間中に有利な成長を遂げると予測されています。この成長は、医療処置中のクリアな視界を確保し曇りを防止するために、ゴーグル、フェイスシールド、保護メガネなどの医療機器への防曇フィルムの採用が増加していることに起因しています。さらに、ヘルスケア環境における衛生・安全対策への意識の高まりが、曇り止めソリューションの需要をさらに押し上げています。

最大のシェアを占める地域:

様々な要因から、北米地域が防曇フィルムおよびシート市場で最大のシェアを占めると推定されます。同地域は成熟した包装業界を誇り、食品包装用途に防曇フィルムの使用を促進する厳しい規制があります。さらに、衛生と安全性に関する消費者の意識の高まりとコンビニエンス食品の需要の増加が、防曇フィルムの採用を後押ししています。さらに、技術の進歩と主要市場プレイヤーの存在が、北米の市場成長見通しに寄与しています。

CAGRが最も高い地域:

アジア太平洋地域は、以下の理由により、防曇フィルムおよびシート市場の大幅な成長が見込まれています。急速な工業化と、製品の利点に関する消費者の意識の高まりが、食品包装、農業、ヘルスケアなど様々な産業における防曇フィルムの需要を促進しています。さらに、持続可能なパッケージング・ソリューションを推進する政府の積極的な取り組みが、市場の成長をさらに後押ししています。さらに、この地域の人口拡大と可処分所得の増加は、包装商品の消費拡大に寄与し、防曇ソリューションのニーズを促進しています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 技術分析

- アプリケーション分析

- エンドユーザー分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の防曇フィルムおよびシート市場:材料タイプ別

- ポリエステルフィルム

- 二軸延伸ポリプロピレン(BOPP)フィルム

- ポリカーボネートフィルム

- その他の材料タイプ

第6章 世界の防曇フィルムおよびシート市場:厚さ別

- 15ミクロン未満

- 15~30ミクロン

- 30~45ミクロン

- 45ミクロン以上

第7章 世界の防曇フィルムおよびシート市場:技術別

- コーティング系

- 化学ベース

- ナノテクノロジーベース

- その他の技術

第8章 世界の防曇フィルムおよびシート市場:用途別

- 食品包装フィルム

- 農業フィルム

- 温室フィルム

- 条カバー

- 産業用途

- 産業用バイザーとゴーグル

- 計器レンズおよび表示パネル

- 鏡

- 冷蔵庫のドア

- ソーラーパネル

- 窓とフロントガラス

- その他の用途

第9章 世界の防曇フィルムおよびシート市場:エンドユーザー別

- 食品および飲料

- 自動車

- 建設

- 家電

- ヘルスケア

- 光学

- その他のエンドユーザー

第10章 世界の防曇フィルムおよびシート市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイル

- 3M Company

- Armando Alvarez

- Berry Global Inc.

- BioBag International AS

- Dupont Teijin Films

- FSI Coating Technologies, Inc.

- Futamura Chemical Co., Ltd.

- Haining Duletai New Material Co., Ltd.

- Inteplast Group

- Klockner Pentaplast

- Mitsubishi Chemical Corporation

- Nitto Denko Corporation

- Novamont S.p.A.

- RKW Group

- Saint-Gobain

- Toray Plastics(America), Inc.

- Vibac Group S.p.a.

List of Tables

- Table 1 Global Anti-fog Films and Sheets Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Anti-fog Films and Sheets Market Outlook, By Material Type (2021-2030) ($MN)

- Table 3 Global Anti-fog Films and Sheets Market Outlook, By Polyester Films (2021-2030) ($MN)

- Table 4 Global Anti-fog Films and Sheets Market Outlook, By Biaxially Oriented Polypropylene (BOPP) Films (2021-2030) ($MN)

- Table 5 Global Anti-fog Films and Sheets Market Outlook, By Polycarbonate Films (2021-2030) ($MN)

- Table 6 Global Anti-fog Films and Sheets Market Outlook, By Other Material Types (2021-2030) ($MN)

- Table 7 Global Anti-fog Films and Sheets Market Outlook, By Thickness (2021-2030) ($MN)

- Table 8 Global Anti-fog Films and Sheets Market Outlook, By Up to 15 microns (2021-2030) ($MN)

- Table 9 Global Anti-fog Films and Sheets Market Outlook, By 15-30 microns (2021-2030) ($MN)

- Table 10 Global Anti-fog Films and Sheets Market Outlook, By 30-45 microns (2021-2030) ($MN)

- Table 11 Global Anti-fog Films and Sheets Market Outlook, By Above 45 microns (2021-2030) ($MN)

- Table 12 Global Anti-fog Films and Sheets Market Outlook, By Technology (2021-2030) ($MN)

- Table 13 Global Anti-fog Films and Sheets Market Outlook, By Coating-based (2021-2030) ($MN)

- Table 14 Global Anti-fog Films and Sheets Market Outlook, By Chemical-based (2021-2030) ($MN)

- Table 15 Global Anti-fog Films and Sheets Market Outlook, By Nanotechnology-based (2021-2030) ($MN)

- Table 16 Global Anti-fog Films and Sheets Market Outlook, By Other Technologies (2021-2030) ($MN)

- Table 17 Global Anti-fog Films and Sheets Market Outlook, By Application (2021-2030) ($MN)

- Table 18 Global Anti-fog Films and Sheets Market Outlook, By Food Packaging Films (2021-2030) ($MN)

- Table 19 Global Anti-fog Films and Sheets Market Outlook, By Agricultural Films (2021-2030) ($MN)

- Table 20 Global Anti-fog Films and Sheets Market Outlook, By Greenhouse Films (2021-2030) ($MN)

- Table 21 Global Anti-fog Films and Sheets Market Outlook, By Row Covers (2021-2030) ($MN)

- Table 22 Global Anti-fog Films and Sheets Market Outlook, By Industrial Applications (2021-2030) ($MN)

- Table 23 Global Anti-fog Films and Sheets Market Outlook, By Industrial Visors & Goggles (2021-2030) ($MN)

- Table 24 Global Anti-fog Films and Sheets Market Outlook, By Instrument Lenses & Display Panels (2021-2030) ($MN)

- Table 25 Global Anti-fog Films and Sheets Market Outlook, By Mirrors (2021-2030) ($MN)

- Table 26 Global Anti-fog Films and Sheets Market Outlook, By Refrigerator Doors (2021-2030) ($MN)

- Table 27 Global Anti-fog Films and Sheets Market Outlook, By Solar Panels (2021-2030) ($MN)

- Table 28 Global Anti-fog Films and Sheets Market Outlook, By Windows & Windshields (2021-2030) ($MN)

- Table 29 Global Anti-fog Films and Sheets Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 30 Global Anti-fog Films and Sheets Market Outlook, By End User (2021-2030) ($MN)

- Table 31 Global Anti-fog Films and Sheets Market Outlook, By Food and Beverage (2021-2030) ($MN)

- Table 32 Global Anti-fog Films and Sheets Market Outlook, By Automotive (2021-2030) ($MN)

- Table 33 Global Anti-fog Films and Sheets Market Outlook, By Construction (2021-2030) ($MN)

- Table 34 Global Anti-fog Films and Sheets Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 35 Global Anti-fog Films and Sheets Market Outlook, By Healthcare (2021-2030) ($MN)

- Table 36 Global Anti-fog Films and Sheets Market Outlook, By Optical (2021-2030) ($MN)

- Table 37 Global Anti-fog Films and Sheets Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Anti-fog Films and Sheets Market is accounted for $3.7 billion in 2023 and is expected to reach $5.6 billion by 2030 growing at a CAGR of 6.1% during the forecast period. Anti-fog films and sheets are transparent materials designed to prevent condensation or fogging on surfaces, ensuring clarity and visibility. These films typically feature special coatings or additives that absorb moisture, reducing surface tension and preventing water droplets from forming. Widely used in packaging, optical lenses, automotive windows, and greenhouse applications, anti-fog films improve safety and enhance product presentation by maintaining clear visibility.

Market Dynamics:

Driver:

Growth in food packaging industry

With increasing demand for packaged food products worldwide, manufacturers are adopting advanced packaging solutions to enhance product presentation and shelf life. Anti-fog films and sheets play a crucial role in maintaining visibility and preventing condensation on packaging surfaces, ensuring that consumers can clearly see the contents of the package. This contributes to improved consumer appeal, food safety, and overall packaging performance, driving market growth.

Restraint:

High cost of production

The production process for these specialized films involves the incorporation of advanced materials and technologies to achieve the desired anti-fog properties. This includes the use of special coatings, additives, or treatments to prevent condensation effectively. Such materials and processes often come at a premium, driving up production costs. As a result, the high cost of production can limit the affordability and accessibility of anti-fog films and sheets for manufacturers and end-users, posing a challenge to market growth.

Opportunity:

Development of bio-based anti-fog films

The development of bio-based anti-fog films presents a significant opportunity in the anti-fog films and sheets market. As sustainability becomes a key focus for industries worldwide, there is a growing demand for eco-friendly alternatives to traditional petroleum-based materials. Bio-based films, derived from renewable sources such as plant-based polymers or biodegradable materials, offer reduced environmental impact and carbon footprint. Additionally, they cater to consumers' increasing preference for sustainable products, thus driving market growth and expanding the adoption of eco-friendly anti-fog solutions.

Threat:

Limited awareness about anti-fog films

Despite their benefits in preventing condensation and maintaining visibility, many consumers and businesses may not be aware of the existence or advantages of anti-fog films. This lack of awareness can hinder market growth, as potential customers may opt for traditional materials or overlook the need for anti-fog solutions. Moreover, without adequate education and promotion, manufacturers may struggle to differentiate their products and capture market share.

Covid-19 Impact:

The COVID-19 pandemic has had a mixed impact on the anti-fog film and sheet market. While demand for anti-fog films in packaging for essential goods like food and medical supplies has increased, disruptions in manufacturing and supply chains have led to challenges in production and distribution. Additionally, reduced consumer spending in certain sectors has dampened overall demand for non-essential products, affecting the market's growth trajectory.

The food packaging films segment is expected to be the largest during the forecast period

The food packaging films segment is anticipated to dominate the anti-fog films and sheets market during the forecast period due to increasing demand for packaged food products, driven by factors such as convenience, urbanization, and changing consumer lifestyles. Anti-fog films play a crucial role in maintaining product visibility and quality by preventing condensation and fogging on packaging surfaces. With growing awareness about food safety and hygiene, the demand for anti-fog films in food packaging is expected to remain high.

The healthcare segment is expected to have the highest CAGR during the forecast period

The healthcare segment is anticipated to experience lucrative growth during the forecast period in the anti-fog films and sheets market. This growth can be attributed to the increasing adoption of anti-fog films in medical equipment, such as goggles, face shields, and protective eyewear, to ensure clear visibility and prevent fogging during medical procedures. Additionally, heightened awareness of hygiene and safety measures in healthcare settings further drives the demand for anti-fog solutions.

Region with largest share:

The North American region is estimated to have the largest market share in the anti-fog film and sheet market due to various factors. The region boasts a mature packaging industry with stringent regulations promoting the use of anti-fog films for food packaging applications. Additionally, increasing consumer awareness regarding hygiene and safety, coupled with the growing demand for convenience foods, drives the adoption of anti-fog films. Furthermore, advancements in technology and the presence of key market players contribute to the market's growth prospects in North America.

Region with highest CAGR:

The Asia Pacific region is poised for significant growth in the anti-fog films and sheets market owing to Rapid industrialization, coupled with increasing consumer awareness about product benefits, is driving demand for anti-fog films across various industries such as food packaging, agriculture, and healthcare. Additionally, favorable government initiatives promoting sustainable packaging solutions further boost market growth. Moreover, the region's expanding population and rising disposable incomes contribute to higher consumption of packaged goods, driving the need for anti-fog solutions.

Key players in the market

Some of the key players in Anti-fog Films and Sheets Market include 3M Company, Armando Alvarez, Berry Global Inc., BioBag International AS, Dupont Teijin Films, FSI Coating Technologies, Inc., Futamura Chemical Co., Ltd., Haining Duletai New Material Co., Ltd., Inteplast Group, Klockner Pentaplast, Mitsubishi Chemical Corporation, Nitto Denko Corporation, Novamont S.p.A., RKW Group, Saint-Gobain, Toray Plastics (America), Inc. and Vibac Group S.p.a.

Key Developments:

In October 2023, Grupo Armando Alvarez and RedSea sign an exclusive collaboration agreement for the production and distribution of the new intelligent greenhouse covers. These innovative greenhouse covers feature the advanced Iyris(R) technology, developed by RedSea, which allows greenhouse temperature control and is incorporated into the 100% recyclable covers produced by Armando Alvarez Group, saving water and energy as well as improving crop profitability in high temperature areas.

In October 2023, FSI Coating Technologies, Inc. (FSICT), a renowned leader in high-performance anti-fog coatings, is proud to announce the launch of its groundbreaking PFAS-free anti-fog coating, Visgard(R) Ultra. The Ultra coating platform is designed to enhance the surface feel and aesthetics of safety eyewear and ophthalmic lenses.

Material Types Covered:

- Polyester Films

- Biaxially Oriented Polypropylene (BOPP) Films

- Polycarbonate Films

- Other Material Types

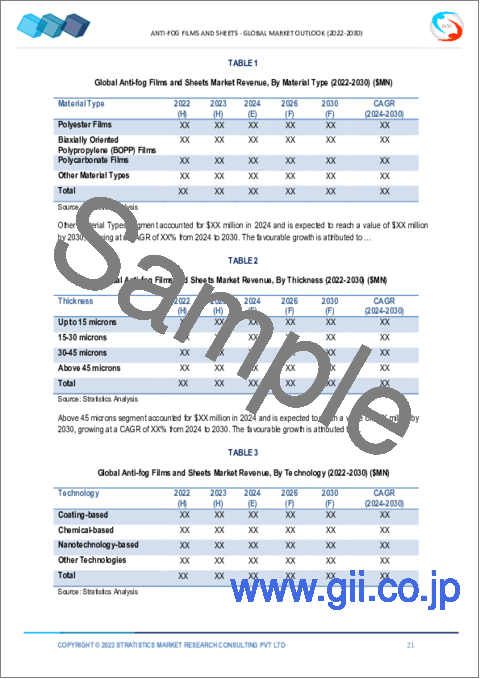

Thickness Covered:

- Up to 15 microns

- 15-30 microns

- 30-45 microns

- Above 45 microns

Technologies Covered:

- Coating-based

- Chemical-based

- Nanotechnology-based

- Other Technologies

Applications Covered:

- Food Packaging Films

- Agricultural Films

- Industrial Applications

- Other Applications

End Users Covered:

- Food and Beverage

- Automotive

- Construction

- Consumer Electronics

- Healthcare

- Optical

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Technology Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Anti-fog Films and Sheets Market, By Material Type

- 5.1 Introduction

- 5.2 Polyester Films

- 5.3 Biaxially Oriented Polypropylene (BOPP) Films

- 5.4 Polycarbonate Films

- 5.5 Other Material Types

6 Global Anti-fog Films and Sheets Market, By Thickness

- 6.1 Introduction

- 6.2 Up to 15 microns

- 6.3 15-30 microns

- 6.4 30-45 microns

- 6.5 Above 45 microns

7 Global Anti-fog Films and Sheets Market, By Technology

- 7.1 Introduction

- 7.2 Coating-based

- 7.3 Chemical-based

- 7.4 Nanotechnology-based

- 7.5 Other Technologies

8 Global Anti-fog Films and Sheets Market, By Application

- 8.1 Introduction

- 8.2 Food Packaging Films

- 8.3 Agricultural Films

- 8.3.1 Greenhouse Films

- 8.3.2 Row Covers

- 8.4 Industrial Applications

- 8.4.1 Industrial Visors & Goggles

- 8.4.2 Instrument Lenses & Display Panels

- 8.4.3 Mirrors

- 8.4.4 Refrigerator Doors

- 8.4.5 Solar Panels

- 8.4.6 Windows & Windshields

- 8.5 Other Applications

9 Global Anti-fog Films and Sheets Market, By End User

- 9.1 Introduction

- 9.2 Food and Beverage

- 9.3 Automotive

- 9.4 Construction

- 9.5 Consumer Electronics

- 9.6 Healthcare

- 9.7 Optical

- 9.8 Other End Users

10 Global Anti-fog Films and Sheets Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 3M Company

- 12.2 Armando Alvarez

- 12.3 Berry Global Inc.

- 12.4 BioBag International AS

- 12.5 Dupont Teijin Films

- 12.6 FSI Coating Technologies, Inc.

- 12.7 Futamura Chemical Co., Ltd.

- 12.8 Haining Duletai New Material Co., Ltd.

- 12.9 Inteplast Group

- 12.10 Klockner Pentaplast

- 12.11 Mitsubishi Chemical Corporation

- 12.12 Nitto Denko Corporation

- 12.13 Novamont S.p.A.

- 12.14 RKW Group

- 12.15 Saint-Gobain

- 12.16 Toray Plastics (America), Inc.

- 12.17 Vibac Group S.p.a.