|

|

市場調査レポート

商品コード

1423668

体外式ペースメーカー市場の2030年までの予測:デバイス別、用途別、エンドユーザー別、地域別の世界分析External Pacemaker Market Forecasts to 2030 - Global Analysis By Device (Single Chamber and Dual Chamber), By Application (Acute Myocardial Infarction, Bradycardia, Heart Block and Other Applications), End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 体外式ペースメーカー市場の2030年までの予測:デバイス別、用途別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2024年02月02日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、体外式ペースメーカーの世界市場は2023年に17億6,000万米ドルを占め、予測期間中にCAGR 5.4%で成長し、2030年には25億4,000万米ドルに達すると予測されています。

体外式ペースメーカーは、電気インパルスを外部に供給することによって心臓のリズムを調整するように設計された医療機器です。制御された電気信号を発する外部ジェネレーターに接続された電極で構成されています。この装置は患者の胸に装着され、心臓に電気パルスを送信し、恒久的な解決策が実施されるまでの間、徐脈やその他の伝導異常のような異常な心臓リズムに対処します。

米国疾病予防管理センター(CDC)によると、約40秒に1人の割合でアメリカ人が心臓発作を起こしています。毎年、805,000人のアメリカ人が心臓発作を起こし、そのうち605,000人が初めて心臓発作を起こします。

増加する老人人口

高齢者は一般的に徐脈や心ブロックのような心拍異常を経験します。高齢者層が拡大するにつれて、ペースメーカーの介入を必要とする心臓疾患の有病率が高くなっています。体外式ペースメーカーは、このような場合に一時的な解決策として機能し、患者が恒久的な植え込みを待つ間、または心臓処置後の一時的な措置の間、即時の心臓サポートを提供します。さらに、世界の高齢化の進展は、ペースメーカの需要増に直結しており、市場の成長を促進しています。

ペースメーカーの高コスト

これらのデバイスは心臓管理に不可欠であるが、調達とメンテナンスの両方に多額の費用がかかります。高度な技術、材料、製造工程が価格高騰の一因となっています。さらに、特定の地域ではヘルスケア予算の制約や保険適用範囲の狭さが経済的な障壁となり、患者の救命機器へのアクセスを妨げています。

新興国における可処分所得の増加

所得水準の上昇により、新興国ではペースメーカーを含む高度なヘルスケアサービスや医療機器を購入できるようになった。そのため、心臓治療に対する需要が高まり、高価な医療技術へのアクセスが向上しています。手ごろな価格で購入できるようになったことで、より多くの国民がペースメーカーの植え込みや治療を選択するようになり、市場の成長を後押ししています。さらに、ヘルスケア支出の増加と保険適用率の向上が普及率の拡大に寄与し、これらの経済圏における市場情勢を好転させています。

代替療法との競合

薬物療法、生活習慣の改善、その他の非侵襲的な心臓治療などの代替療法は、ペースメーカー植え込みに代わる治療法です。ある種の心臓疾患では、患者は手術、デバイス依存性、コストへの懸念から、ペースメーカーを考慮する前に代替療法を選ぶかもしれないです。さらに、非侵襲的手技の進歩や代替療法の研究は、実行可能な選択肢を提供し、ペースメーカーの必要性を直ちに減らす可能性があります。

COVID-19の影響:

COVID-19の大流行は、体外式ペースメーカー市場に大きな影響を与えました。ヘルスケアサービス、選択的処置、通院の混乱により、ペースメーカー移植を含む緊急性のない治療が延期されました。サプライチェーンの混乱とパンデミック関連医療へのリソースの優先順位付けは、デバイスの入手可能性に影響を与えました。患者の医療への消極的な姿勢や入院もペースメーカー処置の減少に寄与し、その結果、市場の成長は一時的に低下しました。

予測期間中、病院セグメントが最大になる見込み

予測期間中、病院セグメントが最大となる見込みです。病院は、専門的なインフラと体外式ペースメーカーを必要とする複雑な心臓疾患の診断と治療が可能な熟練した医療専門家を備えた心臓治療の主要なセンターとして機能しています。さらに、これらの施設は、即時の心臓治療を必要とする患者の流入が多いため、ペースメーカーの植え込みと管理の主要な拠点となっています。病院の包括的なヘルスケアサービスと専門的な心臓病部門は、体外式ペースメーカー市場の最大の貢献者としての地位を確固たるものにしています。

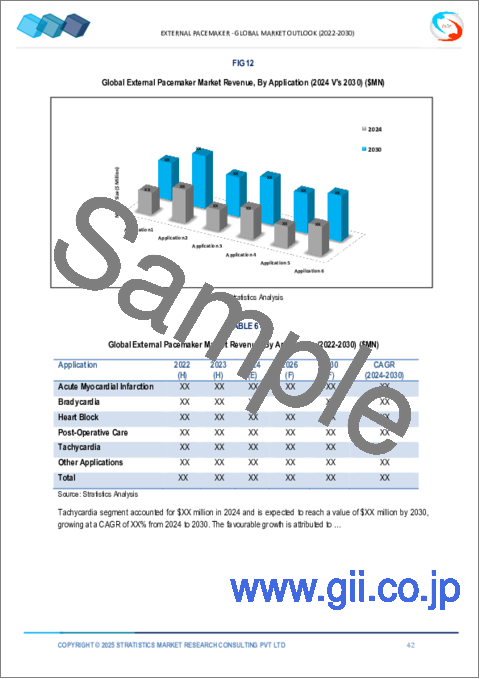

予測期間中、心臓ブロック分野のCAGRが最も高くなる見込み

予測期間中、心臓ブロックセグメントは有利な成長率を経験すると予測されています。これは、心臓の電気信号が遅れたり阻害されたりする心臓ブロックの有病率が増加していることに起因しています。体外式ペースメーカーは、このような場合に心臓のリズムを調整するために不可欠な一時的ソリューションとして機能し、需要の高まりに寄与しています。さらに、技術の進歩や心臓の健康に対する意識の高まりが、心臓ブロック管理のための体外式ペースメーカーの採用を促進し、このセグメントの急成長に拍車をかけると予想されます。

最大のシェアを占める地域

北米は、先進的なヘルスケアインフラ、心臓疾患の高い有病率、多額の医療費により、体外式ペースメーカー市場において最大の市場シェアを確保する見込みです。さらに、主要市場プレイヤーの存在と広範な研究開発活動が市場の優位性に寄与しています。さらに、心臓治療における技術的進歩のためのイニシアチブの増加と革新的な医療ソリューションの採用に対する積極的なアプローチが、体外式ペースメーカー市場における北米の優位性を強化しています。

CAGRが最も高い地域:

アジア太平洋地域は、心臓疾患の有病率が上昇し、老年人口が拡大していることから、外部ペースメーカ市場において大きな成長が見込まれています。さらに、ヘルスケアインフラの改善、先進医療に対する意識の高まり、可処分所得の増加などが、体外式ペースメーカーの採用率を高めています。さらに、国際的な医療機器メーカーとの提携や政府の支援策が市場拡大をさらに後押ししており、アジア太平洋地域の体外式ペースメーカー市場の大幅な成長見通しを示しています。

無料のカスタマイズ提供

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかを提供させていただきます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- エンドユーザー分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の体外式ペースメーカー市場:デバイス別

- シングルチャンバー

- デュアルチャンバー

第6章 世界の体外式ペースメーカー市場:用途別

- 急性心筋梗塞

- 徐脈

- 心臓ブロック

- 術後ケア

- 頻脈

- その他の用途

第7章 世界の体外式ペースメーカー市場:エンドユーザー別

- 病院

- 外来手術センター

- クリニック

- 在宅ヘルスケア

- その他のエンドユーザー

第8章 世界の体外式ペースメーカー市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイル

- Abbott Laboratories

- Biotronik

- Boston Scientific Corporation

- Cardiac Science Corporation

- Cook Medical

- Galix Biomedical Instrumentation

- LivaNova Plc

- Medtronic

- Osypka Medical GmbH

- Reka Health Pte Ltd.

- Schiller AG

- Shree Pacetronix Ltd.

- Spacelabs Healthcare

- ZOLL Medical Corporation

List of Tables

- Table 1 Global External Pacemaker Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global External Pacemaker Market Outlook, By Device (2021-2030) ($MN)

- Table 3 Global External Pacemaker Market Outlook, By Single Chamber (2021-2030) ($MN)

- Table 4 Global External Pacemaker Market Outlook, By Dual Chamber (2021-2030) ($MN)

- Table 5 Global External Pacemaker Market Outlook, By Application (2021-2030) ($MN)

- Table 6 Global External Pacemaker Market Outlook, By Acute Myocardial Infarction (2021-2030) ($MN)

- Table 7 Global External Pacemaker Market Outlook, By Bradycardia (2021-2030) ($MN)

- Table 8 Global External Pacemaker Market Outlook, By Heart Block (2021-2030) ($MN)

- Table 9 Global External Pacemaker Market Outlook, By Post-Operative Care (2021-2030) ($MN)

- Table 10 Global External Pacemaker Market Outlook, By Tachycardia (2021-2030) ($MN)

- Table 11 Global External Pacemaker Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 12 Global External Pacemaker Market Outlook, By End User (2021-2030) ($MN)

- Table 13 Global External Pacemaker Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 14 Global External Pacemaker Market Outlook, By Ambulatory Surgical Centers (2021-2030) ($MN)

- Table 15 Global External Pacemaker Market Outlook, By Clinics (2021-2030) ($MN)

- Table 16 Global External Pacemaker Market Outlook, By Home Healthcare (2021-2030) ($MN)

- Table 17 Global External Pacemaker Market Outlook, By Other End Users (2021-2030) ($MN)

- Table 18 North America External Pacemaker Market Outlook, By Country (2021-2030) ($MN)

- Table 19 North America External Pacemaker Market Outlook, By Device (2021-2030) ($MN)

- Table 20 North America External Pacemaker Market Outlook, By Single Chamber (2021-2030) ($MN)

- Table 21 North America External Pacemaker Market Outlook, By Dual Chamber (2021-2030) ($MN)

- Table 22 North America External Pacemaker Market Outlook, By Application (2021-2030) ($MN)

- Table 23 North America External Pacemaker Market Outlook, By Acute Myocardial Infarction (2021-2030) ($MN)

- Table 24 North America External Pacemaker Market Outlook, By Bradycardia (2021-2030) ($MN)

- Table 25 North America External Pacemaker Market Outlook, By Heart Block (2021-2030) ($MN)

- Table 26 North America External Pacemaker Market Outlook, By Post-Operative Care (2021-2030) ($MN)

- Table 27 North America External Pacemaker Market Outlook, By Tachycardia (2021-2030) ($MN)

- Table 28 North America External Pacemaker Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 29 North America External Pacemaker Market Outlook, By End User (2021-2030) ($MN)

- Table 30 North America External Pacemaker Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 31 North America External Pacemaker Market Outlook, By Ambulatory Surgical Centers (2021-2030) ($MN)

- Table 32 North America External Pacemaker Market Outlook, By Clinics (2021-2030) ($MN)

- Table 33 North America External Pacemaker Market Outlook, By Home Healthcare (2021-2030) ($MN)

- Table 34 North America External Pacemaker Market Outlook, By Other End Users (2021-2030) ($MN)

- Table 35 Europe External Pacemaker Market Outlook, By Country (2021-2030) ($MN)

- Table 36 Europe External Pacemaker Market Outlook, By Device (2021-2030) ($MN)

- Table 37 Europe External Pacemaker Market Outlook, By Single Chamber (2021-2030) ($MN)

- Table 38 Europe External Pacemaker Market Outlook, By Dual Chamber (2021-2030) ($MN)

- Table 39 Europe External Pacemaker Market Outlook, By Application (2021-2030) ($MN)

- Table 40 Europe External Pacemaker Market Outlook, By Acute Myocardial Infarction (2021-2030) ($MN)

- Table 41 Europe External Pacemaker Market Outlook, By Bradycardia (2021-2030) ($MN)

- Table 42 Europe External Pacemaker Market Outlook, By Heart Block (2021-2030) ($MN)

- Table 43 Europe External Pacemaker Market Outlook, By Post-Operative Care (2021-2030) ($MN)

- Table 44 Europe External Pacemaker Market Outlook, By Tachycardia (2021-2030) ($MN)

- Table 45 Europe External Pacemaker Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 46 Europe External Pacemaker Market Outlook, By End User (2021-2030) ($MN)

- Table 47 Europe External Pacemaker Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 48 Europe External Pacemaker Market Outlook, By Ambulatory Surgical Centers (2021-2030) ($MN)

- Table 49 Europe External Pacemaker Market Outlook, By Clinics (2021-2030) ($MN)

- Table 50 Europe External Pacemaker Market Outlook, By Home Healthcare (2021-2030) ($MN)

- Table 51 Europe External Pacemaker Market Outlook, By Other End Users (2021-2030) ($MN)

- Table 52 Asia Pacific External Pacemaker Market Outlook, By Country (2021-2030) ($MN)

- Table 53 Asia Pacific External Pacemaker Market Outlook, By Device (2021-2030) ($MN)

- Table 54 Asia Pacific External Pacemaker Market Outlook, By Single Chamber (2021-2030) ($MN)

- Table 55 Asia Pacific External Pacemaker Market Outlook, By Dual Chamber (2021-2030) ($MN)

- Table 56 Asia Pacific External Pacemaker Market Outlook, By Application (2021-2030) ($MN)

- Table 57 Asia Pacific External Pacemaker Market Outlook, By Acute Myocardial Infarction (2021-2030) ($MN)

- Table 58 Asia Pacific External Pacemaker Market Outlook, By Bradycardia (2021-2030) ($MN)

- Table 59 Asia Pacific External Pacemaker Market Outlook, By Heart Block (2021-2030) ($MN)

- Table 60 Asia Pacific External Pacemaker Market Outlook, By Post-Operative Care (2021-2030) ($MN)

- Table 61 Asia Pacific External Pacemaker Market Outlook, By Tachycardia (2021-2030) ($MN)

- Table 62 Asia Pacific External Pacemaker Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 63 Asia Pacific External Pacemaker Market Outlook, By End User (2021-2030) ($MN)

- Table 64 Asia Pacific External Pacemaker Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 65 Asia Pacific External Pacemaker Market Outlook, By Ambulatory Surgical Centers (2021-2030) ($MN)

- Table 66 Asia Pacific External Pacemaker Market Outlook, By Clinics (2021-2030) ($MN)

- Table 67 Asia Pacific External Pacemaker Market Outlook, By Home Healthcare (2021-2030) ($MN)

- Table 68 Asia Pacific External Pacemaker Market Outlook, By Other End Users (2021-2030) ($MN)

- Table 69 South America External Pacemaker Market Outlook, By Country (2021-2030) ($MN)

- Table 70 South America External Pacemaker Market Outlook, By Device (2021-2030) ($MN)

- Table 71 South America External Pacemaker Market Outlook, By Single Chamber (2021-2030) ($MN)

- Table 72 South America External Pacemaker Market Outlook, By Dual Chamber (2021-2030) ($MN)

- Table 73 South America External Pacemaker Market Outlook, By Application (2021-2030) ($MN)

- Table 74 South America External Pacemaker Market Outlook, By Acute Myocardial Infarction (2021-2030) ($MN)

- Table 75 South America External Pacemaker Market Outlook, By Bradycardia (2021-2030) ($MN)

- Table 76 South America External Pacemaker Market Outlook, By Heart Block (2021-2030) ($MN)

- Table 77 South America External Pacemaker Market Outlook, By Post-Operative Care (2021-2030) ($MN)

- Table 78 South America External Pacemaker Market Outlook, By Tachycardia (2021-2030) ($MN)

- Table 79 South America External Pacemaker Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 80 South America External Pacemaker Market Outlook, By End User (2021-2030) ($MN)

- Table 81 South America External Pacemaker Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 82 South America External Pacemaker Market Outlook, By Ambulatory Surgical Centers (2021-2030) ($MN)

- Table 83 South America External Pacemaker Market Outlook, By Clinics (2021-2030) ($MN)

- Table 84 South America External Pacemaker Market Outlook, By Home Healthcare (2021-2030) ($MN)

- Table 85 South America External Pacemaker Market Outlook, By Other End Users (2021-2030) ($MN)

- Table 86 Middle East & Africa External Pacemaker Market Outlook, By Country (2021-2030) ($MN)

- Table 87 Middle East & Africa External Pacemaker Market Outlook, By Device (2021-2030) ($MN)

- Table 88 Middle East & Africa External Pacemaker Market Outlook, By Single Chamber (2021-2030) ($MN)

- Table 89 Middle East & Africa External Pacemaker Market Outlook, By Dual Chamber (2021-2030) ($MN)

- Table 90 Middle East & Africa External Pacemaker Market Outlook, By Application (2021-2030) ($MN)

- Table 91 Middle East & Africa External Pacemaker Market Outlook, By Acute Myocardial Infarction (2021-2030) ($MN)

- Table 92 Middle East & Africa External Pacemaker Market Outlook, By Bradycardia (2021-2030) ($MN)

- Table 93 Middle East & Africa External Pacemaker Market Outlook, By Heart Block (2021-2030) ($MN)

- Table 94 Middle East & Africa External Pacemaker Market Outlook, By Post-Operative Care (2021-2030) ($MN)

- Table 95 Middle East & Africa External Pacemaker Market Outlook, By Tachycardia (2021-2030) ($MN)

- Table 96 Middle East & Africa External Pacemaker Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 97 Middle East & Africa External Pacemaker Market Outlook, By End User (2021-2030) ($MN)

- Table 98 Middle East & Africa External Pacemaker Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 99 Middle East & Africa External Pacemaker Market Outlook, By Ambulatory Surgical Centers (2021-2030) ($MN)

- Table 100 Middle East & Africa External Pacemaker Market Outlook, By Clinics (2021-2030) ($MN)

- Table 101 Middle East & Africa External Pacemaker Market Outlook, By Home Healthcare (2021-2030) ($MN)

- Table 102 Middle East & Africa External Pacemaker Market Outlook, By Other End Users (2021-2030) ($MN)

According to Stratistics MRC, the Global External Pacemaker Market is accounted for $1.76 billion in 2023 and is expected to reach $2.54 billion by 2030 growing at a CAGR of 5.4% during the forecast period. An external pacemaker is a medical device designed to regulate heart rhythm by delivering electrical impulses externally. It consists of electrodes connected to an external generator that emits controlled electrical signals. This device is placed on the patient's chest and transmits electrical pulses to the heart, addressing abnormal heart rhythms like bradycardia or other conduction abnormalities until a permanent solution is implemented.

According to the Centers for Disease Control and Prevention (CDC), approximately every 40 seconds an American will have a heart attack. Every year, 805,000 Americans have a heart attack, 605,000 of them for the first time.

Market Dynamics:

Driver:

Growing geriatric population

Elderly individuals commonly experience heart rhythm abnormalities like bradycardia or heart block. As the ageing demographic expands, there's a higher prevalence of cardiac conditions necessitating pacemaker intervention. External pacemakers serve as temporary solutions in these cases, providing immediate cardiac support while patients await permanent implantation or temporary measure post-cardiac procedures. Additionally, the rising ageing population worldwide directly correlates with an increased demand for external pacemakers, fostering market growth.

Restraint:

High cost of pacemakers

These devices are crucial for cardiac management, but they involve substantial expenses for both procurement and maintenance. The sophisticated technology, materials, and manufacturing processes contribute to elevated prices. Additionally, healthcare budget constraints and limited insurance coverage in certain regions create financial barriers, hindering patient access to these life-saving devices, which limits their accessibility to a broader population.

Opportunity:

Increasing disposable income in emerging economies

Due to the rise in income levels, emerging economies can afford advanced healthcare services and devices, including pacemakers. This leads to a higher demand for cardiac care and better access to expensive medical technologies. Improved affordability allows a larger segment of the population to opt for pacemaker implantations or treatments, boosting market growth. Moreover, increased healthcare spending and better insurance coverage contribute to expanded adoption rates, creating a favourable market landscape in these economies.

Threat:

Competition from alternative therapies

Alternative treatments like medication, lifestyle changes, or other non-invasive cardiac interventions present alternatives to pacemaker implantation. For certain cardiac conditions, patients might opt for alternative therapies before considering a pacemaker due to concerns about surgery, device dependency, or cost. Moreover, advancements in non-invasive procedures and research into alternative treatments offer viable options, potentially reducing the immediate need for pacemakers.

Covid-19 Impact:

The COVID-19 pandemic had a substantial impact on the external pacemaker market. Disruptions in healthcare services, elective procedures, and hospital visits led to deferred non-emergency treatments, including pacemaker implantations. Supply chain disruptions and the prioritisation of resources for pandemic-related care affected device availability. Patient reluctance to seek medical care and hospitalisations also contributed to reduced pacemaker procedures, resulting in a temporary decline in market growth.

The hospitals segment is expected to be the largest during the forecast period

During the forecast period, the hospitals segment is poised to dominate. Hospitals serve as primary centres for cardiac care, equipped with specialised infrastructure and skilled healthcare professionals capable of diagnosing and treating complex cardiac conditions requiring external pacemakers. Additionally, these facilities often witness a high influx of patients requiring immediate cardiac interventions, making them primary hubs for pacemaker implantations and management. The comprehensive healthcare services and specialised cardiology departments in hospitals solidify their position as the largest contributors to the external pacemaker market.

The heart block segment is expected to have the highest CAGR during the forecast period

Over the forecast period, the heart block segment is anticipated to experience a lucrative growth rate. This is attributed to the increasing prevalence of heart block conditions, where the heart's electrical signals are delayed or obstructed. External pacemakers serve as essential temporary solutions for regulating the heart's rhythm in such cases, contributing to their heightened demand. Additionally, advancements in technology and a growing awareness of cardiac health are expected to drive the adoption of external pacemakers for heart block management, fueling the segment's rapid growth.

Region with largest share:

North America is positioned to secure the largest market share in the external pacemaker market owing to its advanced healthcare infrastructure, high prevalence of cardiac disorders, and substantial healthcare expenditure. Additionally, the presence of key market players and extensive research and development activities contribute to market dominance. Furthermore, increasing initiatives for technological advancements in cardiac care and a proactive approach to adopting innovative medical solutions reinforce North America's prominence in the external pacemaker market.

Region with highest CAGR:

The Asia-Pacific region is poised for significant growth in the external pacemaker market due to the region's rising prevalence of cardiac disorders and an expanding geriatric population. Additionally, improving healthcare infrastructure, growing awareness about advanced medical treatments, and rising disposable incomes contribute to higher adoption rates of external pacemakers. Moreover, collaborations with international medical device manufacturers and supportive government initiatives further drive market expansion, indicating substantial growth prospects for the Asia-Pacific External Pacemaker market.

Key players in the market

Some of the key players in External Pacemaker Market include Abbott Laboratories, Biotronik, Boston Scientific Corporation, Cardiac Science Corporation, Cook Medical, Galix Biomedical Instrumentation, LivaNova Plc, Medtronic, Osypka Medical GmbH, Reka Health Pte Ltd., Schiller AG, Shree Pacetronix Ltd., Spacelabs Healthcare and ZOLL Medical Corporation.

Key Developments:

In December 2023, Medtronic plc, a global leader in healthcare technology, announces that it has entered into a definitive agreement to expand its partnership with Cosmo Intelligent Medical Devices, a subsidiary of Cosmo Pharmaceuticals. This AI-driven partnership will further capitalize on the achievements already realized with the GI Genius™ intelligent endoscopy module, offering continued innovation and scalable healthcare advancements for patients and caregivers globally.

In November 2023, Boston Scientific Corporation announced the close of its acquisition of Relievant Medsystems Inc., a company that offers the only U.S. Food and Drug Administration-cleared Intracept® Intraosseous Nerve Ablation System, a therapy to treat vertebrogenic pain that is a form of chronic low back pain. The Intracept system, a basivertebral nerve ablation therapy, will be an addition to the Boston Scientific chronic pain portfolio that includes spinal cord stimulation, radiofrequency ablation and an interspinous spacer procedure.

In July 2023, Abbott announced that the U.S. Food and Drug Administration (FDA) has approved the AVEIR™ dual chamber (DR) leadless pacemaker system, the world's first dual chamber leadless pacing system that treats people with abnormal or slow heart rhythms. With more than 80% of people who need a pacemaker requiring pacing in two chambers of the heart (both the right atrium and right ventricle), the approval significantly increases access to leadless pacing for millions of people across the U.S.

Devices Covered:

- Single Chamber

- Dual Chamber

Applications Covered:

- Acute Myocardial Infarction

- Bradycardia

- Heart Block

- Post-Operative Care

- Tachycardia

- Other Applications

End Users Covered:

- Hospitals

- Ambulatory Surgical Centers

- Clinics

- Home Healthcare

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 End User Analysis

- 3.8 Emerging Markets

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global External Pacemaker Market, By Device

- 5.1 Introduction

- 5.2 Single Chamber

- 5.3 Dual Chamber

6 Global External Pacemaker Market, By Application

- 6.1 Introduction

- 6.2 Acute Myocardial Infarction

- 6.3 Bradycardia

- 6.4 Heart Block

- 6.5 Post-Operative Care

- 6.6 Tachycardia

- 6.7 Other Applications

7 Global External Pacemaker Market, By End User

- 7.1 Introduction

- 7.2 Hospitals

- 7.3 Ambulatory Surgical Centers

- 7.4 Clinics

- 7.5 Home Healthcare

- 7.6 Other End Users

8 Global External Pacemaker Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 Abbott Laboratories

- 10.2 Biotronik

- 10.3 Boston Scientific Corporation

- 10.4 Cardiac Science Corporation

- 10.5 Cook Medical

- 10.6 Galix Biomedical Instrumentation

- 10.7 LivaNova Plc

- 10.8 Medtronic

- 10.9 Osypka Medical GmbH

- 10.10 Reka Health Pte Ltd.

- 10.11 Schiller AG

- 10.12 Shree Pacetronix Ltd.

- 10.13 Spacelabs Healthcare

- 10.14 ZOLL Medical Corporation