|

|

市場調査レポート

商品コード

1371892

人工関節の2030年までの市場予測: タイプ別、素材別、用途別、地域別の世界分析Artificial Joints Market Forecasts to 2030 - Global Analysis By Type (Non Cemented Artificial Joints, Cemented Artificial Joints and Other Types), Material, Application and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 人工関節の2030年までの市場予測: タイプ別、素材別、用途別、地域別の世界分析 |

|

出版日: 2023年10月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の人工関節市場は2023年に215億3,000万米ドルを占め、予測期間中のCAGRは6.6%で成長し、2030年には336億2,000万米ドルに達すると予想されています。

人工関節は、人工関節や関節インプラントとしても知られ、損傷したり老化したりした人体の関節を置き換えるために設計された医療機器です。これらの器具は、自然の関節と同じように機能するように作られており、関節の可動性を高め、痛みを軽減し、身体機能を回復させる。人工関節は、変形性関節症、関節リウマチ、関節変性症、関節外傷などの疾患によって深刻な損傷を受けた関節を置き換えるために、人工関節置換術などの整形外科手術で頻繁に使用されます。

米国国立医学図書館によると、2022年、米国における人工膝関節全置換術(TKA)の需要は、2005年から2030年にかけて673%増加し、年間528万件のTKAが行われると予想されています。

意識の高まりと高齢化

関節の健康や利用可能な治療法に関する意識の高まりや患者教育の向上は、個人が適時に医療介入や人工関節置換術を受けることを奨励しています。さらに、世界人口の高齢化が進むにつれ、変形性関節症や関節リウマチのような関節関連疾患の有病率が増加し、人工関節置換術や人工関節の需要を牽引しています。

限られた寿命と手術のリスク

人工関節は年々進歩しているとはいえ、永久的な解決策ではありません。ほとんどの人工関節の寿命には限りがあり、患者は再手術が必要になることがあり、それには費用と手間がかかります。さらに、人工関節置換術には、感染症、血栓、麻酔合併症などの固有のリスクが伴うため、患者さんによっては、この手術を選択することを躊躇する場合もあります。

技術の進歩

材料、インプラントの設計、手術技術における継続的な進歩は、患者の転帰を改善できる、より耐久性が高く、効率的で革新的な人工関節製品を開発する機会を提供します。さらに、これらの地域では予測期間中に人工関節置換術や人工関節の需要が増加する可能性があるため、メーカーはヘルスケア・ニーズが高まる新興市場を開拓することができます。

規制上の課題

厳しい規制要件や承認プロセスは、人工関節新製品のイントロダクションを遅らせ、開発コストを増加させる可能性があります。さらに、人工関節に関連する有害事象や安全性への懸念が報告されると、患者の信頼が損なわれ、人工関節製品に対する需要の減少につながる可能性があります。こうした制約が市場の拡大を妨げています。

COVID-19の影響:

COVID-19パンデミックは当初、サプライチェーンの混乱と選択手術の延期により人工関節市場を混乱させました。しかし、手術が再開されるにつれて市場は回復し、手技の滞留が生じた。パンデミックは遠隔医療の導入を加速させ、患者の診察とフォローアップ・ケアに影響を与える可能性があります。高齢化による人工関節の持続的需要に加え、医療技術や研究の進歩が続いているため、長期的な見通しは引き続き明るいです。

予測期間中はセメント製人工関節分野が最大となる見込み

2022年の市場シェアはセメント製人工関節が最も大きく、予測期間中もその地位を維持すると予想されます。セメント製の関節は弾力性があり、安定性が高く、骨にしっかりと固定されます。さらに、生体適合性の高いセラミック材料やセラミック含有率の高い人工関節は、関節の摩擦や摩耗を軽減することができます。このような要素は、予測期間中の同分野の成長に寄与しています。

人工膝関節分野は予測期間中最も高いCAGRが見込まれる

変形性膝関節症の有病率の上昇と人工膝関節置換術の件数の増加により、人工膝関節セグメントは予測期間中に最も高い成長を遂げると予想されます。加えて、骨粗しょう症や関節炎のような加齢に関連した筋骨格系の疾患の有病率を高めている人口の高齢化や、肥満率の上昇といった要因も、膝関節置換術や股関節置換術、それに対応するインプラントの需要を高める大きな要因となっており、このセグメントの成長を後押ししています。

最大のシェアを占める地域:

北米地域は、予想される期間を通じて引き続き市場を独占すると予想されます。この地域の2大経済大国である米国とカナダが、この地域の市場価値の主な収益源です。変形性関節症患者の増加と高齢化は、北米における市場拡大の需要を最も増大させる2つの主要因です。さらに、米国の人工関節市場は、コンピュータ支援によるインプラントデザイン、ロボット手術、有利な償還条件の利用の増加によって、予測期間中に活性化すると予測されています。

CAGRが最も高い地域:

膝関節疾患がより一般的になり、医療ツーリズムが活況を呈し、可処分所得が増加し、この地域のヘルスケア・インフラが着実に改善されていることから、アジア太平洋市場は予測期間中に急成長すると予測されます。さらに、老年人口と変形性関節症の有病率が増加しています。変形性関節症の患者数は増加し、人工関節や人工関節置換術の需要も増加すると予想されます。したがって、これらの要因がアジア太平洋における人工関節市場の開拓を促進すると予想されます。

無料のカスタマイズ提供:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の人工関節市場:種類別

- 非セメント式人工関節

- セメント固定式人工関節

- その他のタイプ

第6章 世界の人工関節市場:素材別

- 合金

- セラミックス

- その他の素材

第7章 世界の人工関節市場:用途別

- 人工股関節

- 人工膝関節

- 病院

- 補綴クリニック

- リハビリテーションセンター

- その他の用途

第8章 世界の人工関節市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイル

- Zimmer Biomet Holding Inc

- Conformis Inc

- Smith & Nephew plc

- Stryker Corporation

- B. Braun Melsungen AG

- Medtronic plc

- Johnson and Johnson

- Exactech

- Medacta International SA

- MicroPort Orthopedics Inc

List of Tables

- Table 1 Global Artificial Joints Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Artificial Joints Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Artificial Joints Market Outlook, By Non Cemented Artificial Joints (2021-2030) ($MN)

- Table 4 Global Artificial Joints Market Outlook, By Cemented Artificial Joints (2021-2030) ($MN)

- Table 5 Global Artificial Joints Market Outlook, By Other Types (2021-2030) ($MN)

- Table 6 Global Artificial Joints Market Outlook, By Material (2021-2030) ($MN)

- Table 7 Global Artificial Joints Market Outlook, By Alloy (2021-2030) ($MN)

- Table 8 Global Artificial Joints Market Outlook, By Ceramics (2021-2030) ($MN)

- Table 9 Global Artificial Joints Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 10 Global Artificial Joints Market Outlook, By Application (2021-2030) ($MN)

- Table 11 Global Artificial Joints Market Outlook, By Artificial Hip Joints (2021-2030) ($MN)

- Table 12 Global Artificial Joints Market Outlook, By Artificial Knee Joints (2021-2030) ($MN)

- Table 13 Global Artificial Joints Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 14 Global Artificial Joints Market Outlook, By Prosthetics Clinics (2021-2030) ($MN)

- Table 15 Global Artificial Joints Market Outlook, By Rehabilitation Center (2021-2030) ($MN)

- Table 16 Global Artificial Joints Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 17 North America Artificial Joints Market Outlook, By Country (2021-2030) ($MN)

- Table 18 North America Artificial Joints Market Outlook, By Type (2021-2030) ($MN)

- Table 19 North America Artificial Joints Market Outlook, By Non Cemented Artificial Joints (2021-2030) ($MN)

- Table 20 North America Artificial Joints Market Outlook, By Cemented Artificial Joints (2021-2030) ($MN)

- Table 21 North America Artificial Joints Market Outlook, By Other Types (2021-2030) ($MN)

- Table 22 North America Artificial Joints Market Outlook, By Material (2021-2030) ($MN)

- Table 23 North America Artificial Joints Market Outlook, By Alloy (2021-2030) ($MN)

- Table 24 North America Artificial Joints Market Outlook, By Ceramics (2021-2030) ($MN)

- Table 25 North America Artificial Joints Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 26 North America Artificial Joints Market Outlook, By Application (2021-2030) ($MN)

- Table 27 North America Artificial Joints Market Outlook, By Artificial Hip Joints (2021-2030) ($MN)

- Table 28 North America Artificial Joints Market Outlook, By Artificial Knee Joints (2021-2030) ($MN)

- Table 29 North America Artificial Joints Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 30 North America Artificial Joints Market Outlook, By Prosthetics Clinics (2021-2030) ($MN)

- Table 31 North America Artificial Joints Market Outlook, By Rehabilitation Center (2021-2030) ($MN)

- Table 32 North America Artificial Joints Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 33 Europe Artificial Joints Market Outlook, By Country (2021-2030) ($MN)

- Table 34 Europe Artificial Joints Market Outlook, By Type (2021-2030) ($MN)

- Table 35 Europe Artificial Joints Market Outlook, By Non Cemented Artificial Joints (2021-2030) ($MN)

- Table 36 Europe Artificial Joints Market Outlook, By Cemented Artificial Joints (2021-2030) ($MN)

- Table 37 Europe Artificial Joints Market Outlook, By Other Types (2021-2030) ($MN)

- Table 38 Europe Artificial Joints Market Outlook, By Material (2021-2030) ($MN)

- Table 39 Europe Artificial Joints Market Outlook, By Alloy (2021-2030) ($MN)

- Table 40 Europe Artificial Joints Market Outlook, By Ceramics (2021-2030) ($MN)

- Table 41 Europe Artificial Joints Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 42 Europe Artificial Joints Market Outlook, By Application (2021-2030) ($MN)

- Table 43 Europe Artificial Joints Market Outlook, By Artificial Hip Joints (2021-2030) ($MN)

- Table 44 Europe Artificial Joints Market Outlook, By Artificial Knee Joints (2021-2030) ($MN)

- Table 45 Europe Artificial Joints Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 46 Europe Artificial Joints Market Outlook, By Prosthetics Clinics (2021-2030) ($MN)

- Table 47 Europe Artificial Joints Market Outlook, By Rehabilitation Center (2021-2030) ($MN)

- Table 48 Europe Artificial Joints Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 49 Asia Pacific Artificial Joints Market Outlook, By Country (2021-2030) ($MN)

- Table 50 Asia Pacific Artificial Joints Market Outlook, By Type (2021-2030) ($MN)

- Table 51 Asia Pacific Artificial Joints Market Outlook, By Non Cemented Artificial Joints (2021-2030) ($MN)

- Table 52 Asia Pacific Artificial Joints Market Outlook, By Cemented Artificial Joints (2021-2030) ($MN)

- Table 53 Asia Pacific Artificial Joints Market Outlook, By Other Types (2021-2030) ($MN)

- Table 54 Asia Pacific Artificial Joints Market Outlook, By Material (2021-2030) ($MN)

- Table 55 Asia Pacific Artificial Joints Market Outlook, By Alloy (2021-2030) ($MN)

- Table 56 Asia Pacific Artificial Joints Market Outlook, By Ceramics (2021-2030) ($MN)

- Table 57 Asia Pacific Artificial Joints Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 58 Asia Pacific Artificial Joints Market Outlook, By Application (2021-2030) ($MN)

- Table 59 Asia Pacific Artificial Joints Market Outlook, By Artificial Hip Joints (2021-2030) ($MN)

- Table 60 Asia Pacific Artificial Joints Market Outlook, By Artificial Knee Joints (2021-2030) ($MN)

- Table 61 Asia Pacific Artificial Joints Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 62 Asia Pacific Artificial Joints Market Outlook, By Prosthetics Clinics (2021-2030) ($MN)

- Table 63 Asia Pacific Artificial Joints Market Outlook, By Rehabilitation Center (2021-2030) ($MN)

- Table 64 Asia Pacific Artificial Joints Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 65 South America Artificial Joints Market Outlook, By Country (2021-2030) ($MN)

- Table 66 South America Artificial Joints Market Outlook, By Type (2021-2030) ($MN)

- Table 67 South America Artificial Joints Market Outlook, By Non Cemented Artificial Joints (2021-2030) ($MN)

- Table 68 South America Artificial Joints Market Outlook, By Cemented Artificial Joints (2021-2030) ($MN)

- Table 69 South America Artificial Joints Market Outlook, By Other Types (2021-2030) ($MN)

- Table 70 South America Artificial Joints Market Outlook, By Material (2021-2030) ($MN)

- Table 71 South America Artificial Joints Market Outlook, By Alloy (2021-2030) ($MN)

- Table 72 South America Artificial Joints Market Outlook, By Ceramics (2021-2030) ($MN)

- Table 73 South America Artificial Joints Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 74 South America Artificial Joints Market Outlook, By Application (2021-2030) ($MN)

- Table 75 South America Artificial Joints Market Outlook, By Artificial Hip Joints (2021-2030) ($MN)

- Table 76 South America Artificial Joints Market Outlook, By Artificial Knee Joints (2021-2030) ($MN)

- Table 77 South America Artificial Joints Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 78 South America Artificial Joints Market Outlook, By Prosthetics Clinics (2021-2030) ($MN)

- Table 79 South America Artificial Joints Market Outlook, By Rehabilitation Center (2021-2030) ($MN)

- Table 80 South America Artificial Joints Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 81 Middle East & Africa Artificial Joints Market Outlook, By Country (2021-2030) ($MN)

- Table 82 Middle East & Africa Artificial Joints Market Outlook, By Type (2021-2030) ($MN)

- Table 83 Middle East & Africa Artificial Joints Market Outlook, By Non Cemented Artificial Joints (2021-2030) ($MN)

- Table 84 Middle East & Africa Artificial Joints Market Outlook, By Cemented Artificial Joints (2021-2030) ($MN)

- Table 85 Middle East & Africa Artificial Joints Market Outlook, By Other Types (2021-2030) ($MN)

- Table 86 Middle East & Africa Artificial Joints Market Outlook, By Material (2021-2030) ($MN)

- Table 87 Middle East & Africa Artificial Joints Market Outlook, By Alloy (2021-2030) ($MN)

- Table 88 Middle East & Africa Artificial Joints Market Outlook, By Ceramics (2021-2030) ($MN)

- Table 89 Middle East & Africa Artificial Joints Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 90 Middle East & Africa Artificial Joints Market Outlook, By Application (2021-2030) ($MN)

- Table 91 Middle East & Africa Artificial Joints Market Outlook, By Artificial Hip Joints (2021-2030) ($MN)

- Table 92 Middle East & Africa Artificial Joints Market Outlook, By Artificial Knee Joints (2021-2030) ($MN)

- Table 93 Middle East & Africa Artificial Joints Market Outlook, By Hospitals (2021-2030) ($MN)

- Table 94 Middle East & Africa Artificial Joints Market Outlook, By Prosthetics Clinics (2021-2030) ($MN)

- Table 95 Middle East & Africa Artificial Joints Market Outlook, By Rehabilitation Center (2021-2030) ($MN)

- Table 96 Middle East & Africa Artificial Joints Market Outlook, By Other Applications (2021-2030) ($MN)

According to Stratistics MRC, the Global Artificial Joints Market is accounted for $21.53 billion in 2023 and is expected to reach $33.62 billion by 2030 growing at a CAGR of 6.6% during the forecast period. Artificial joints, also known as prosthetic joints or joint implants, are medical gadgets designed to replace a human body joint that has been damaged or is aging. These devices are made to function like a natural joint would, enhancing joint mobility, reducing pain, and regaining physical function. Artificial joints are frequently used in orthopedic procedures like joint replacement surgeries to replace joints that have suffered severe damage from diseases like osteoarthritis, rheumatoid arthritis, joint degeneration, or joint trauma.

According to, National Library of Medicine, in 2022, the demand for total knee arthroplasty (TKA) in the U.S. was anticipated to increase 673% from 2005 to 2030, with 5.28 million TKAs to be done annually.

Market Dynamics:

Driver:

Increasing awareness and aging population

Growing awareness about joint health and available treatment options, as well as improved patient education, encourages individuals to seek timely medical intervention and joint replacement surgeries. Additionally, as the global population continues to age, the prevalence of joint-related conditions like osteoarthritis and rheumatoid arthritis increases, driving the demand for joint replacement surgeries and artificial joints.

Restraint:

Limited lifespan and surgical risks

While artificial joints have improved over the years, they are not permanent solutions. Most joints have a limited lifespan, and patients may require revision surgeries, which can be costly and complicated. In addition to that joint replacement surgeries come with inherent risks, including infection, blood clots, and anesthesia complications, which can deter some patients from opting for the procedure.

Opportunity:

Technological advancements

Ongoing advancements in materials, implant design, and surgical techniques offer opportunities for the development of more durable, efficient, and innovative artificial joint products that can improve patient outcomes. Moreover, manufacturers can tap into emerging markets with growing healthcare needs, as these regions may experience increased demand for joint replacement surgeries and artificial joints over the forecast period.

Threat:

Regulatory challenges

Stringent regulatory requirements and approval processes can delay the introduction of new artificial joint products and increase development costs. In addition, reports of adverse events or safety concerns related to artificial joints can erode patient trust and lead to reduced demand for these products. Such limitations hinder the market expansion.

COVID-19 Impact:

The COVID-19 pandemic initially disrupted the artificial joints market due to supply chain disruptions and postponed elective surgeries. However, the market rebounded as surgeries resumed, creating a backlog of procedures. The pandemic accelerated the adoption of telehealth, potentially impacting patient consultations and follow-up care. Long-term prospects remain positive due to an aging population's sustained demand for joint replacements, coupled with ongoing advancements in medical technology and research.

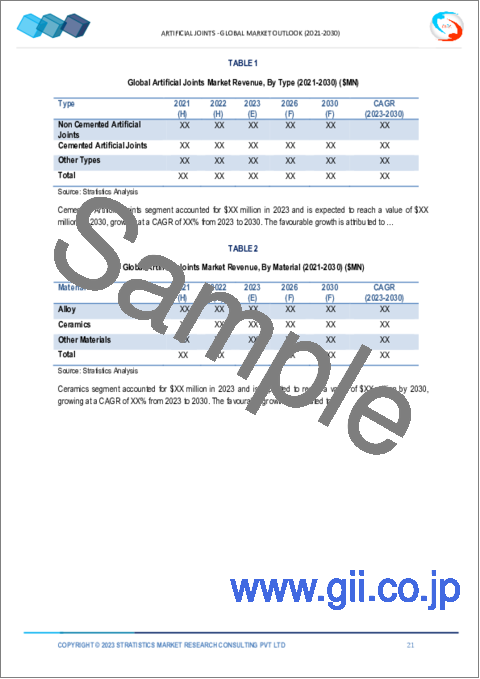

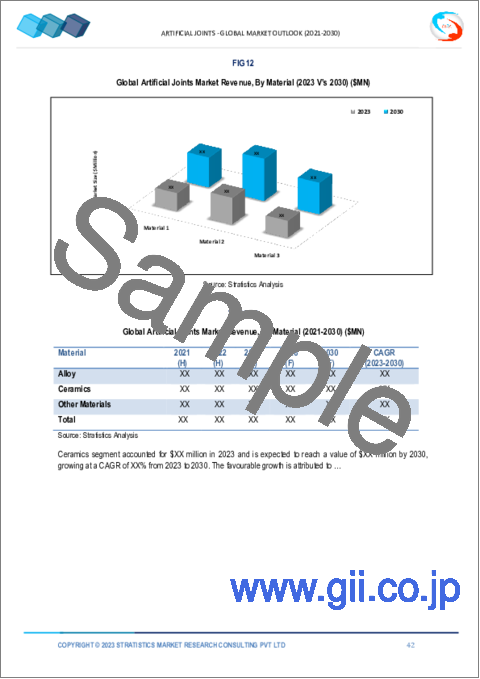

The cemented joints segment is expected to be the largest during the forecast period

The market's largest share was held by the cemented joints segment in 2022, and it is anticipated that it will hold that position throughout the forecast period. Joints made of cement are more elastic, stable, and securely attached to the bones. Additionally, biocompatible ceramic materials and artificial joints with a high ceramic content can lessen joint friction and wear. Such elements contribute to the segment's growth over the course of the forecast period.

The artificial knee joint segment is expected to have the highest CAGR during the forecast period

Due to the rising prevalence of knee osteoarthritis and the rising number of knee replacement surgeries, the artificial knee joint segment is anticipated to experience the highest growth over the course of the forecast period. In addition, factors like the aging population, which is increasing the prevalence of age-related musculoskeletal conditions like osteoporosis and arthritis, and the rising obesity rate are all significant drivers of the demand for knee and hip replacement surgeries and the corresponding implants, which is boosting the segment's growth.

Region with largest share:

The North American region is expected to continue to dominate the market throughout the anticipated period. The two largest economies in the area, the U.S. and Canada, are the main revenue generators for the market value in the area. An increase in osteoarthritis patients and an aging population are the two primary factors that are most likely to increase demand for market expansion in North America. Additionally, it is anticipated that the U.S. artificial joints market will be fueled by an increase in the use of computer-aided implant designs, robotic surgery, and favorable reimbursement conditions over the course of the projection period.

Region with highest CAGR:

As knee disorders are becoming more prevalent, medical tourism is booming, disposable income is rising, and the healthcare infrastructure in this region is steadily improving, the Asia Pacific market is predicted to grow quickly over the forecasted period. Additionally, there is a rise in geriatric populations and osteoarthritis prevalence. The number of people with osteoarthritis is expected to rise, as will the demand for artificial joints and arthroplasty surgeries. Thus, it is anticipated that these factors will fuel the development of the artificial joint market in Asia-Pacific.

Key players in the market:

Some of the key players in Artificial Joints market include: Zimmer Biomet Holding Inc, Conformis Inc, Smith & Nephew plc, Stryker Corporation, B. Braun Melsungen AG, Medtronic plc, Johnson and Johnson, Exactech, Medacta International SA and MicroPort Orthopedics Inc.

Key Developments:

In June 2023, BioMed X has announced that it has begun a joint research project with Sanofi on artificial intelligence (AI)-driven drug development. The two companies initially announced their partnership late last year, and are now ready to begin work on their AI drug discovery platform. The "Next Generation Virtual Patient Engine for Clinical Translation of Drug Candidates" (VPE) project aims to develop a computational platform capable of predicting the efficacy of first or best-in-class drug candidates.

In August 2023, Corentec, a company specializing in the production of artificial joints, announced that the inaugural surgery involving its patient-specific implant (PSI) designed for artificial shoulder joints was effectively carried out at Kyungpook National University Hospital in Korea.

Types Covered:

- Non Cemented Artificial Joints

- Cemented Artificial Joints

- Other Types

Materials Covered:

- Alloy

- Ceramics

- Other Materials

Applications Covered:

- Artificial Hip Joints

- Artificial Knee Joints

- Hospitals

- Prosthetics Clinics

- Rehabilitation Center

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Artificial Joints Market, By Type

- 5.1 Introduction

- 5.2 Non Cemented Artificial Joints

- 5.3 Cemented Artificial Joints

- 5.4 Other Types

6 Global Artificial Joints Market, By Material

- 6.1 Introduction

- 6.2 Alloy

- 6.3 Ceramics

- 6.4 Other Materials

7 Global Artificial Joints Market, By Application

- 7.1 Introduction

- 7.2 Artificial Hip Joints

- 7.3 Artificial Knee Joints

- 7.4 Hospitals

- 7.5 Prosthetics Clinics

- 7.6 Rehabilitation Center

- 7.7 Other Applications

8 Global Artificial Joints Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 Zimmer Biomet Holding Inc

- 10.2 Conformis Inc

- 10.3 Smith & Nephew plc

- 10.4 Stryker Corporation

- 10.5 B. Braun Melsungen AG

- 10.6 Medtronic plc

- 10.7 Johnson and Johnson

- 10.8 Exactech

- 10.9 Medacta International SA

- 10.10 MicroPort Orthopedics Inc