|

|

市場調査レポート

商品コード

1359048

ロボットアーム市場の2030年までの予測:タイプ別、可搬容量別、軸別、用途別、エンドユーザー別、地域別の世界分析Robotic Arms Market Forecasts to 2030 - Global Analysis By Type, Payload Capacity, Axes, Application, End User and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| ロボットアーム市場の2030年までの予測:タイプ別、可搬容量別、軸別、用途別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2023年10月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界のロボットアーム市場は2023年に238億4,000万米ドルを占め、予測期間中のCAGRは31.0%で成長し、2030年には1,578億4,000万米ドルに達すると予測されています。

ロボットアームは、プログラム可能な機械的アームであり、軸に沿って回転または移動する複数の関節で構成されています。技術の向上により、ロボットアームはより効果的な作業ができるようになっています。コンピューター制御のマニピュレーターと接続し、適切な選択を行うことができます。ロボットアームは、繰り返し作業や重作業を正確にこなすことができます。さらに、ロボットアームは、過酷な環境下での単純作業、反復作業、連続作業を、正確に、素早く、安全に、長時間行うために特に有用です。

国際ロボット連盟(IFR)によると、現在270万台以上のロボットが世界中の工場で働いています。

重量物用ロボットアームの需要

ロボットアームの市場は、重可搬ロボットアームの開発によって大きな可能性を与えられています。重いペイロードを持つロボットアームは、重い物体を運搬したり移動させたりするために、主に産業現場で使用されます。自動化が進み、生産における生産性と効率性を高める必要性から、大可搬質量のロボットアームのニーズが徐々に高まっています。さらに、重いペイロードを持つロボットアームは、従来の重量物持ち上げやマテリアルハンドリング技術よりも多くの利点があります。これらのロボットアームは、高精度で正確な作業を実行するようにプログラム可能であり、その結果、生産量が増加し、人的ミスが減少します。また、メンテナンスもほとんど必要なく、継続的な作業も可能です。

高いコストと安全性への懸念

ロボットアームの購入、設置、メンテナンスにかかるコストは、多くの中小企業(SME)にとって法外なものです。高い初期投資コストは、潜在的な購入者が市場に参入することを躊躇させる可能性があります。しかし、ロボットアームを使用する場合、特に人間とロボットが協働する場面では、安全性が最優先されなければならないです。人間の作業員の安全を確保し、事故を防止するには、高度な安全対策と厳しい規制の遵守が必要であり、コストと複雑さを増大させる可能性があります。

産業オートメーションへの需要と技術開発

産業オートメーションへの需要は高まり続けており、ロボットアームにチャンスをもたらしています。ロボットアームは製造工程の生産性、効率、精度を向上させ、コスト削減と製品品質の向上につながります。自動車、エレクトロニクス、ロジスティクスなどの産業は、自動化の進展から恩恵を受けることができます。さらに、人工知能、機械学習、コンピューター・ビジョンなど、ロボットアーム技術の進歩が続いており、より高度で高性能なロボットアームを実現する機会がもたらされています。これらの改善により、複雑な作業、多様な環境への適応性、自律性の強化が可能になります。こうした要因が市場の需要を後押ししています。

雇用の喪失

ロボットアームが人間の労働者に取って代わる可能性があるため、雇用の喪失はロボットアームに関連する主要な懸念事項のひとつです。ロボットアームがより高度になり、複雑な作業をこなせるようになると、特定の産業では人間の労働者に取って代わり、雇用の喪失や経済的混乱につながる可能性があります。これは特に、製造業や組立ラインなど、手作業に大きく依存している産業に影響を与える可能性があります。

COVID-19の影響:

COVID-19の流行は、ロボットアーム市場にプラスとマイナスの両方の影響を与えました。プラス面では、社会隔離政策と労働力の混乱が、自動化と非接触操作の需要を高めました。その結果、製造業、ヘルスケア、物流などの業界ではロボットアームに対する需要が増加しました。しかし、パンデミックはまた、いくつかの産業でサプライチェーンの混乱、プロジェクトの遅延、支出の減少をもたらし、市場の拡大に影響を与えました。全体として、パンデミックはある分野では困難と不確実性をもたらし、他の分野ではロボットアームの展開を加速させました。

予測期間中、多関節セグメントが最大になる見込み

多関節セグメントが最大のシェアを占めると予測されています。多関節ロボットアームは、複数の関節によって特徴付けられ、人間の腕の動きを精密かつ柔軟に模倣することができます。これらのロボットアームの需要は、製造、自動車、ヘルスケア、エレクトロニクスなどの様々な産業によって牽引されており、組立、溶接、マテリアルハンドリング、外科手術などの作業に使用されています。自動化の導入が進み、産業革命が進行していることから、ロボットアーム市場の多関節セグメントは拡大を続けると予想されます。

ヘルスケア&メディカル分野は予測期間中に最も高いCAGRが見込まれる

ヘルスケア・医療分野は、予測期間中に有利な成長が見込まれます。ロボットアームは、様々な医療処置に正確で低侵襲なソリューションを提供し、ヘルスケア分野に革命をもたらしました。これらのロボットアームは、外科医が複雑な治療をより正確に、より低侵襲に、より良い患者の転帰で実施することを可能にします。ロボットアームは、腹腔鏡手術、整形外科、神経学、眼科などの外科手術に使用されています。ヘルスケアにおけるロボットアームの能力は、画像誘導システム、触覚フィードバック、機械学習アルゴリズムなどの最先端技術を取り入れることでさらに向上しています。このように、ロボットアーム市場のヘルスケア・医療分野は、ロボット支援手術に対するニーズの高まりや、より良い手術結果や患者の安全性に対する需要の拡大により、力強い成長が見込まれています。

最大シェアの地域

アジア太平洋地域が予測期間中最大の市場シェアを占めました。自動車、エレクトロニクス、航空宇宙などの分野におけるロボットアームの需要は、特に中国、日本、韓国などの国々の強固な産業基盤によって拍車がかかっています。また、人件費の高騰や効率化の必要性から、企業は自動化技術に投資しています。産業オートメーションを支援する分野における政府の規制や措置も、ロボットアームの使用を増加させています。アジア太平洋地域のロボットアーム産業の巨大な可能性を活用するため、市場プレーヤーは規制のハードル、スキル不足、現地化ソリューションの必要性といった難題に積極的に取り組んでいます。

CAGRが最も高い地域:

北米地域は、予測期間中に有益な成長を遂げると予想されます。北米は、様々な要因によってロボットアームの顕著な市場となっています。ロボットアームのニーズは、自動車、航空宇宙、エレクトロニクス、ヘルスケアなどの産業で高まっており、特に米国とカナダでは高度な製造業が存在しています。ロボットアームがこの地域で採用されるようになったのは、自動化と効率改善が重視されるようになった結果です。

無料のカスタマイズ提供:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 用途分析

- エンドユーザー分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のロボットアーム市場:タイプ別

- 多関節型

- スカラ

- 円筒形

- デカルト座標

- 球状または極性

- デルタ

第6章 世界のロボットアーム市場:可搬容量別

- 500KG未満

- 1001-2000KG

- 501-1000KG

- 2001KG以上

第7章 世界のロボットアーム市場:軸別

- 1軸

- 3軸

- 5軸

- 7軸

- 2軸

- 4軸

- 6軸

第8章 世界のロボットアーム市場:用途別

- マテリアルハンドリングと輸送

- はんだ付けと溶接

- 接着と封止

- 仕分け

- 組み立てと分解

- 切断・加工

- ビンピッキング

- アンビエント・アシステッド・リビング

- その他の用途

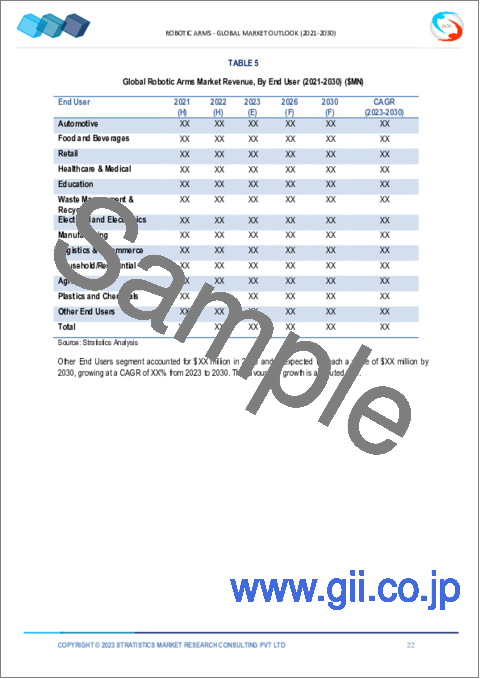

第9章 世界のロボットアーム市場:エンドユーザー別

- 自動車

- 飲食品

- 小売り

- ヘルスケア・医療

- 教育

- 廃棄物管理とリサイクル

- 電気および電子

- 製造業

- 物流とeコマース

- 家庭用/住宅

- 農業

- プラスチックと化学薬品

- その他のエンドユーザー

第10章 世界のロボットアーム市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイル

- Kuka AG

- Yaskawa Electric Corporation

- Fanuc Corporation

- Kawasaki Heavy Industries, Ltd.

- Mitsubishi Electric Corporation

- Denso Wave Incorporated

- Nachi-Fujikoshi Corp.

- Omron Corporation

- Flexiv Ltd.

- Gridbots Technologies Private Limited.

- ABB

- Adept Technologies

- Rockwell Automation, Inc.

- Universal Robots

- Seiko Epson Corporation.

- Asimov Robotics.

- Dobot.cc

- Staubli Corporation

List of Tables

- Table 1 Global Robotic Arms Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Robotic Arms Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Robotic Arms Market Outlook, By Articulated (2021-2030) ($MN)

- Table 4 Global Robotic Arms Market Outlook, By SCARA (2021-2030) ($MN)

- Table 5 Global Robotic Arms Market Outlook, By Cylindrical (2021-2030) ($MN)

- Table 6 Global Robotic Arms Market Outlook, By Cartesian (2021-2030) ($MN)

- Table 7 Global Robotic Arms Market Outlook, By Spherical or Polar (2021-2030) ($MN)

- Table 8 Global Robotic Arms Market Outlook, By Delta (2021-2030) ($MN)

- Table 9 Global Robotic Arms Market Outlook, By Payload Capacity (2021-2030) ($MN)

- Table 10 Global Robotic Arms Market Outlook, By Less than 500KG (2021-2030) ($MN)

- Table 11 Global Robotic Arms Market Outlook, By 1001-2000KG (2021-2030) ($MN)

- Table 12 Global Robotic Arms Market Outlook, By 501-1000KG (2021-2030) ($MN)

- Table 13 Global Robotic Arms Market Outlook, By 2001KG Above (2021-2030) ($MN)

- Table 14 Global Robotic Arms Market Outlook, By Axes (2021-2030) ($MN)

- Table 15 Global Robotic Arms Market Outlook, By 1-Axis (2021-2030) ($MN)

- Table 16 Global Robotic Arms Market Outlook, By 2-Axis (2021-2030) ($MN)

- Table 17 Global Robotic Arms Market Outlook, By 3-Axis (2021-2030) ($MN)

- Table 18 Global Robotic Arms Market Outlook, By 4-Axis (2021-2030) ($MN)

- Table 19 Global Robotic Arms Market Outlook, By 5-Axis (2021-2030) ($MN)

- Table 20 Global Robotic Arms Market Outlook, By 6-Axis (2021-2030) ($MN)

- Table 21 Global Robotic Arms Market Outlook, By 7-Axis (2021-2030) ($MN)

- Table 22 Global Robotic Arms Market Outlook, By Application (2021-2030) ($MN)

- Table 23 Global Robotic Arms Market Outlook, By Materials Handling & Transportation (2021-2030) ($MN)

- Table 24 Global Robotic Arms Market Outlook, By Soldering and Welding (2021-2030) ($MN)

- Table 25 Global Robotic Arms Market Outlook, By Bonding and sealing (2021-2030) ($MN)

- Table 26 Global Robotic Arms Market Outlook, By Sorting (2021-2030) ($MN)

- Table 27 Global Robotic Arms Market Outlook, By Assembling and Disassembling (2021-2030) ($MN)

- Table 28 Global Robotic Arms Market Outlook, By Cutting and Processing (2021-2030) ($MN)

- Table 29 Global Robotic Arms Market Outlook, By Bin Picking (2021-2030) ($MN)

- Table 30 Global Robotic Arms Market Outlook, By Ambient Assisted Living (2021-2030) ($MN)

- Table 31 Global Robotic Arms Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 32 Global Robotic Arms Market Outlook, By End User (2021-2030) ($MN)

- Table 33 Global Robotic Arms Market Outlook, By Automotive (2021-2030) ($MN)

- Table 34 Global Robotic Arms Market Outlook, By Food and Beverages (2021-2030) ($MN)

- Table 35 Global Robotic Arms Market Outlook, By Retail (2021-2030) ($MN)

- Table 36 Global Robotic Arms Market Outlook, By Healthcare & Medical (2021-2030) ($MN)

- Table 37 Global Robotic Arms Market Outlook, By Education (2021-2030) ($MN)

- Table 38 Global Robotic Arms Market Outlook, By Waste Management & Recycling (2021-2030) ($MN)

- Table 39 Global Robotic Arms Market Outlook, By Electrical and Electronics (2021-2030) ($MN)

- Table 40 Global Robotic Arms Market Outlook, By Manufacturing (2021-2030) ($MN)

- Table 41 Global Robotic Arms Market Outlook, By Logistics & E-commerce (2021-2030) ($MN)

- Table 42 Global Robotic Arms Market Outlook, By Household/Residential (2021-2030) ($MN)

- Table 43 Global Robotic Arms Market Outlook, By Agriculture (2021-2030) ($MN)

- Table 44 Global Robotic Arms Market Outlook, By Plastics and Chemicals (2021-2030) ($MN)

- Table 45 Global Robotic Arms Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Robotic Arms Market is accounted for $23.84 billion in 2023 and is expected to reach $157.84 billion by 2030 growing at a CAGR of 31.0% during the forecast period. A robotic arm is a mechanical arm that can be programmed and is made up of several joints that may rotate or move along an axis. Due to their improved technology, robotic arms are more effective at their tasks. It has a connection to a computer-controlled manipulator that can make appropriate choices. They can perform repetitive and heavy tasks with great precision. Moreover, Robotic arms are especially useful for performing simple, repetitive, and continuous tasks in harsh environments accurately, quickly, and safely, for extended periods of time.

According to the International Federation of Robotics (IFR), more than 2.7 million robots are currently working in factories around the world.

Market Dynamics:

Driver:

Demand for heavy-payload robotic arms.

The market for robotic arms is given huge potential by the development of heavy-payload robotic arms. Robotic arms with heavy payloads are used mostly in industrial settings to transport and move heavy objects. The need for large payload robotic arms has been gradually increasing due to the rise of automation and the need for greater productivity and efficiency in production. Additionally, robotic arms with heavy payloads have a number of advantages over more conventional heavy lifting and material handling techniques. These robotic arms are programmable to carry out tasks with high precision and accuracy, resulting in increased production and decreased human error. They also require little maintenance and can work continuously.

Restraint:

High cost and safety concerns

The cost of purchasing, installing, and maintaining robotic arms can make them prohibitive for many small and medium-sized businesses (SMEs). High initial investment costs can deter potential buyers from entering the market. However, safety must be a top priority when using robotic arms, especially in settings where humans and robots collaborate. Ensuring the safety of human workers and preventing accidents requires sophisticated safety measures and compliance with strict regulations, which can increase costs and complexity.

Opportunity:

Demand for industrial automation and technical developments

The demand for industrial automation continues to rise, creating opportunities for robotic arms. They can improve productivity, efficiency, and precision in manufacturing processes, leading to cost savings and enhanced product quality. Industries such as automotive, electronics, and logistics can benefit from increased automation. Additionally, ongoing advancements in robotic arm technology, including artificial intelligence, machine learning, and computer vision, provide opportunities for more sophisticated and capable robotic arms. These improvements can enable complex tasks, adaptability to diverse environments, and enhanced autonomy. These factors are propelling market demand.

Threat:

Loss of employment

Job displacement is one of the primary concerns associated with robotic arms, as they could potentially replace human workers. As robotic arms become more advanced and capable of performing complex tasks, they may replace human workers in certain industries, leading to job losses and economic disruption. This could particularly impact industries that heavily rely on manual labour, such as manufacturing and assembly lines.

COVID-19 Impact:

The COVID-19 pandemic has had both positive and negative effects on the market for robotic arms. Positively, social segregation policies and workforce disruptions raised the demand for automation and contactless operations. As a result, industries like manufacturing, healthcare, and logistics saw an increase in demand for robotic arms. However, the pandemic also brought about supply chain disruptions, project delays, and decreased expenditures in several industries, which had an impact on market expansion. Overall, the pandemic presented difficulties and uncertainty in some areas while accelerating the deployment of robotic arms in others.

The articulated segment is expected to be the largest during the forecast period

The articulated segment is estimated to hold the largest share. The articulated robotic arms are characterised by their multiple joints, allowing them to mimic human arm movements with precision and flexibility. The demand for these robotic arms has been driven by various industries such as manufacturing, automotive, healthcare, and electronics, where they are used for tasks such as assembly, welding, material handling, and surgical procedures. With the increasing adoption of automation and the ongoing industrial revolution, the articulated segment of the robotic arms market is expected to continue its expansion.

The Healthcare & Medical segment is expected to have the highest CAGR during the forecast period

The Healthcare & Medical segment is anticipated to have lucrative growth during the forecast period. Robotic arms, offering precise and minimally invasive solutions for a variety of medical procedures, have revolutionised the healthcare sector. These robotic arms allow surgeons to carry out complex treatments with increased precision, less invasiveness, and better patient outcomes. They are used in surgical applications such as laparoscopy, orthopaedics, neurology, and ophthalmology. The capabilities of robotic arms in healthcare have been further enhanced by the incorporation of cutting-edge technology, including image-guided systems, haptic feedback, and machine learning algorithms. Thus, the healthcare and medical section of the robotic arms market is anticipated to experience strong growth due to the rising need for robotic-assisted operations as well as the expanding demand for better surgical outcomes and patient safety.

Region with largest share:

Asia Pacific commanded the largest market share during the extrapolated period. The demand for robotic arms in sectors like automotive, electronics, and aerospace has been spurred by the region's robust industrial base, particularly in nations like China, Japan, and South Korea. Additionally, companies are investing in automation technologies due to the rising cost of labour and the need for higher efficiency. Government regulations and actions in the area supporting industrial automation have also increased the use of robotic arms. To capitalise on the enormous potential of the Asia Pacific robotic arms industry, market players are aggressively addressing difficulties such regulatory hurdles, skill shortfalls, and the need for localised solutions.

Region with highest CAGR:

North American region is expected to witness profitable growth over the projection period. The North American is a prominent market for robotic arms, driven by various factors. The need for robotic arms has increased across industries like automotive, aerospace, electronics, and healthcare due to the existence of advanced manufacturing businesses, particularly in the United States and Canada. Robotic arms have been adopted in the region as a result of the increased emphasis on automation and efficiency improvements.

Key players in the market:

Some of the key players in the Robotic Arms Market include: Kuka AG, Yaskawa Electric Corporation, Fanuc Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, Denso Wave Incorporated, Nachi-Fujikoshi Corp., Omron Corporation, Flexiv Ltd., Gridbots Technologies Private Limited., ABB, Adept Technologies, Rockwell Automation, Inc., Universal Robots, Seiko Epson Corporation., Asimov Robotics., Dobot.cc and Staubli Corporation

Key Developments:

In December 2022, ABB has opened its state-of-the-art, fully automated and flexible robotics factory in Shanghai, China. The 67,000m2 production and research facility represents a $150 million investment by ABB and will deploy the company's digital and automation technologies to manufacture next generation robots - enhancing ABB's robotics and automation leadership in China.

In February 2022, Flexiv partnered with Handplus Robotics, a Singapore-based automation integration firm. Flexiv and Handplus will enable the creation of customised smart solutions, reducing the effects of labour bottlenecks and shortening the ROI period.

In January 2022, Yaskawa Electric Corporation Electric Corporation acquired additional shares of Doolim-Yaskawa Electric Corporation Co., Ltd., one of Korea's leading manufacturers of painting and sealing robot systems. It has helped to establish a business in the robotic painting and sealing system market by leveraging synergies with Doolim-Yaskawa Electric Corporation.

Types Covered:

- Articulated

- SCARA

- Cylindrical

- Cartesian

- Spherical or Polar

- Delta

Payload Capacities Covered:

- Less than 500KG

- 1001-2000KG

- 501-1000KG

- 2001KG Above

Axes Covered:

- 1-Axis

- 3-Axis

- 5-Axis

- 7-Axis

- 2-Axis

- 4-Axis

- 6-Axis

Applications Covered:

- Materials Handling & Transportation

- Soldering and Welding

- Bonding and sealing

- Sorting

- Assembling and Disassembling

- Cutting and Processing

- Bin Picking

- Ambient Assisted Living

- Other Applications

End Users Covered:

- Automotive

- Food and Beverages

- Retail

- Healthcare & Medical

- Education

- Waste Management & Recycling

- Electrical and Electronics

- Manufacturing

- Logistics & E-commerce

- Household/Residential

- Agriculture

- Plastics and Chemicals

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 End User Analysis

- 3.8 Emerging Markets

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Robotic Arms Market, By Type

- 5.1 Introduction

- 5.2 Articulated

- 5.3 SCARA

- 5.4 Cylindrical

- 5.5 Cartesian

- 5.6 Spherical or Polar

- 5.7 Delta

6 Global Robotic Arms Market, By Payload Capacity

- 6.1 Introduction

- 6.2 Less than 500KG

- 6.3 1001-2000KG

- 6.4 501-1000KG

- 6.5 2001KG Above

7 Global Robotic Arms Market, By Axes

- 7.1 Introduction

- 7.2 1-Axis

- 7.3 3-Axis

- 7.4 5-Axis

- 7.5 7-Axis

- 7.6 2-Axis

- 7.7 4-Axis

- 7.8 6-Axis

8 Global Robotic Arms Market, By Application

- 8.1 Introduction

- 8.2 Materials Handling & Transportation

- 8.3 Soldering and Welding

- 8.4 Bonding and sealing

- 8.5 Sorting

- 8.6 Assembling and Disassembling

- 8.7 Cutting and Processing

- 8.8 Bin Picking

- 8.9 Ambient Assisted Living

- 8.10 Other Applications

9 Global Robotic Arms Market, By End User

- 9.1 Introduction

- 9.2 Automotive

- 9.3 Food and Beverages

- 9.4 Retail

- 9.5 Healthcare & Medical

- 9.6 Education

- 9.7 Waste Management & Recycling

- 9.8 Electrical and Electronics

- 9.9 Manufacturing

- 9.10 Logistics & E-commerce

- 9.11 Household/Residential

- 9.12 Agriculture

- 9.13 Plastics and Chemicals

- 9.14 Other End Users

10 Global Robotic Arms Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Kuka AG

- 12.2 Yaskawa Electric Corporation

- 12.3 Fanuc Corporation

- 12.4 Kawasaki Heavy Industries, Ltd.

- 12.5 Mitsubishi Electric Corporation

- 12.6 Denso Wave Incorporated

- 12.7 Nachi-Fujikoshi Corp.

- 12.8 Omron Corporation

- 12.9 Flexiv Ltd.

- 12.10 Gridbots Technologies Private Limited.

- 12.11 ABB

- 12.12 Adept Technologies

- 12.13 Rockwell Automation, Inc.

- 12.14 Universal Robots

- 12.15 Seiko Epson Corporation.

- 12.16 Asimov Robotics.

- 12.17 Dobot.cc

- 12.18 Staubli Corporation