|

|

市場調査レポート

商品コード

1359004

色素増感太陽電池(DSSC)の2030年までの市場予測:セグメント別、地域別の世界分析Dye Sensitized Solar Cell Market Forecasts to 2030 - Global Analysis By Product, Process, Technology, Application, End User and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 色素増感太陽電池(DSSC)の2030年までの市場予測:セグメント別、地域別の世界分析 |

|

出版日: 2023年10月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、色素増感太陽電池(DSSC)の世界市場は2023年に1億5,501万米ドルを占め、2030年には3億9,750万米ドルに達すると予測され、予測期間中のCAGRは14.4%です。

色素増感太陽電池(DSSC)が属する薄膜太陽電池は、分子染色された二酸化チタンナノ粒子でできており、太陽光の吸収を助ける。光増感された陽極と電解液の間に半導体が形成されることで生じる光電気化学システムが、DSSCの基盤となっています。さらに、金属酸化物半導体と光を吸収する色素がこの太陽電池を構成しています。色素は太陽光線によってエネルギーを得て、そのエネルギーを金属酸化物に伝え、電気を発生させます。

国際再生可能エネルギー機関によると、米国における太陽電池の設置容量は2009年に1,614MWで、2020年には75,572MWに増加します。米国エネルギー効率・再生可能エネルギー局によると、2030年までに米国の住宅所有者の7人に1人以上が太陽光発電システムを導入します。

エネルギー利用の効率性と持続可能性

DSSCはエネルギー効率が高いことで知られており、光から電子への変換効率が優れているため、低照度下でも発電することができます。さらに、その持続可能性がDSSCを採用する動機となっています。よりクリーンなエネルギー・システムに切り替える際、DSSCは二酸化炭素排出量を削減する再生可能エネルギー源となるため、望ましい選択肢となります。DSSCの低体積エネルギー、つまり製造に使用されるエネルギーと耐用年数中に生産されるエネルギーの比率は、その持続可能性をさらに高めています。

シリコン太陽電池より低い効率

エネルギー変換効率の点で、DSSCはこれまでシリコン系太陽電池に遅れをとってきました。この制限により、限られた設置面積の中でエネルギー出力を最大化することが重要な大規模太陽光発電設備での使用が制限されています。DSSCの効率は現在進行中の研究によって積極的に改善されているが、性能向上への道に課題がないわけではないです。効率を向上させるためには、より複雑な工学技術や高度な材料を取り入れる必要があり、DSSCの設計を複雑にしています。さらに、こうした開発は生産コストの上昇を招く可能性があり、DSSCの費用対効果は、より確立された太陽電池技術の影に隠れてしまうかもしれないです。

ウェアラブル技術と家電

ウェアラブルおよびポータブル・エレクトロニクスの成長市場において、DSSCには有望な機会が存在します。軽量で柔軟な構造のため、スマートフォン、スマートウォッチ、アウトドアウェア、機器などの消費財に簡単に組み込むことができます。さらに、DSSCはこれらの機器のバッテリーの寿命を延ばしたり、追加電力を供給したりすることで、これらの機器が充電を必要とする頻度を減らし、ユーザーの利便性を向上させ、使い捨てバッテリーの環境への影響を低減することもできます。消費者と電子機器の長期的な存続は、この恩恵を受ける。

シリコン系太陽電池との競合

太陽エネルギー市場を長年支配してきたシリコン系太陽電池は、DSSCに手ごわい競争をもたらしています。シリコン系太陽電池技術のエネルギー変換効率の高さ、実証済みの信頼性、規模の経済性により、DSSCが市場のかなりの部分を占めることは難しいです。さらに、大規模な太陽光発電設備では効率が極めて重要であり、DSSCでは競争に勝つことが難しい場合が多いです。この脅威に対抗し、DSSCが成功できる市場を見つけるためには、柔軟性やアーキテクチャの統合といったDSSCの特徴的な利点を強調することが重要です。

COVID-19のインパクト:

色素増感太陽電池(DSSC)市場は、COVID-19の大流行によってさまざまな面で大きな影響を受けた。一方では、世界の製造・サプライチェーンの混乱がもたらした課題により、生産と流通が一時的に停滞しました。パンデミックは、国や企業がより強靭で持続可能なエネルギー・システムの構築に取り組む中で、DSSCのような再生可能エネルギー源への転換を早めました。さらに、建築物への統合や分散型エネルギー発電の可能性を持つDSSCは、環境問題への意識が高まるにつれ、解決策の一要素として注目されるようになっています。

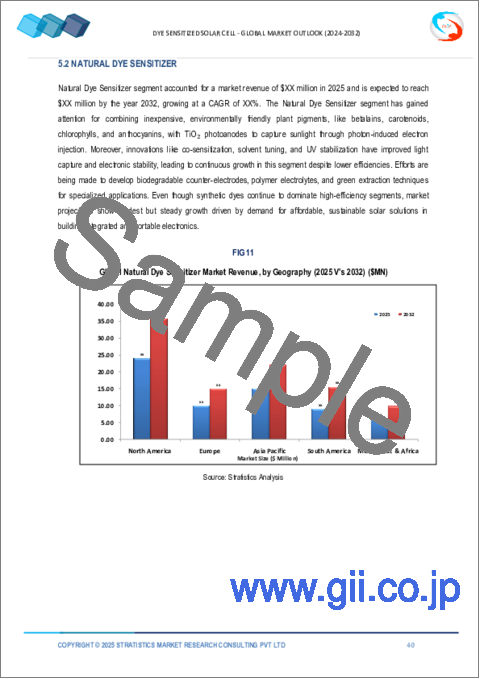

予測期間中、合成色素増感剤セグメントが最大になる見込み

予測期間中、合成色素増感剤が最大の市場シェアを占めると予想されます。天然色素増感剤と比較すると、合成色素はその特性や安定性などを精密にコントロールできるため、高い効果を発揮することが多いです。合成色素は化学構造の適応性が高いため、光吸収特性や電子伝達特性を調整することが可能で、DSSCの性能を高めることができます。さらに、合成色素は環境劣化が少ないため、DSSCの堅牢性と寿命を高めることができます。その結果、市場における合成色素増感剤技術の優位性は、これらの要素に影響されています。

予測期間中、建築物一体型太陽光発電(BIPV)分野のCAGRが最も高くなる見込み

予測期間中、建築物一体型太陽光発電(BIPV)分野のCAGRが最も高かったです。屋根、ファサード、窓などの建築部材や構造物にソーラーパネルを直接組み込むことは、BIPVとして知られています。さらに、この斬新な方法は再生可能エネルギーを生産するだけでなく、建物の美観を向上させ、建設の二酸化炭素排出量を削減します。BIPVソリューションは、持続可能でエネルギー効率の高い建物への注目が高まるにつれ、特に再生可能エネルギー源の利用を奨励する地域で大きな支持を得ています。

最大のシェアを持つ地域

色素増感太陽電池(DSSC)市場では、北米が最大のシェアを占めると予想されています。これは主に、再生可能エネルギー技術への投資の増加、持続可能性の重要性の高まり、さまざまな用途へのDSSCの組み込みによってもたらされました。アーキテクチャーの統合、ポータブル・エレクトロニクス、軍事アプリケーションのために、DSSCは特に米国で多くの関心を集めています。また、DSSCの創造と革新に積極的に貢献しているのは、北米の研究機関と企業です。

CAGRが最も高い地域:

アジア太平洋地域は、予測期間中に有利な成長を遂げると予想されています。この地域の製造能力の拡大、特に再生可能エネルギー技術に多額の投資が行われた中国や韓国などの国々が、この堅調な成長の主な原動力となっています。さらに、民生用電子機器や建物一体型太陽光発電にDSSCが採用されていることや、アジア太平洋地域の環境持続可能性に対する意識の高まりも、同地域の著しい成長に寄与しています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の色素増感太陽電池(DSSC)市場:タイプ別

- 天然色素増感剤

- クロロフィルの色素

- アントシアニン色素

- ベータカロテンの色素

- ベタニンの染料

- その他の天然色素増感剤

- 合成色素増感剤

- コバルトベースの染料

- ポルフィリン系色素

- ルテニウムベースの染料

- テトラヒドロキノリン系染料

- アゾ染料

- ペリレン系染料

- チアシアニン色素

- トリフェニルアミン系染料

- その他の合成色素増感剤

第6章 世界の色素増感太陽電池(DSSC)市場:用途別

- ポータブル充電

- 建物一体型太陽光発電

- 組み込みエレクトロニクス

- 車載用統合型太陽光発電(AIP)

- 建築応用太陽光発電(BAPV)

- 屋外広告

- ソーラーチャージャー

- ワイヤレスキーボード

- 軍事における非常用電源

- その他の用途

第7章 世界の色素増感太陽電池(DSSC)市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第8章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第9章 企業プロファイル

- 3GSolar, Ltd.

- Everlight Chemical Industrial Corp.

- Exeger Operations AB

- Fujikura Ltd.

- G24 Power Ltd.

- Greatcell Energy

- Merck Group

- Nissha Co., Ltd.

- Oxford Photovoltaics

- Peccell Technologies, Inc.

- Renesas Electronics Corporation.

- Sharp Corporation

- Sinovoltaics Group Limited

- Solaris Nanosciences

- Sony Corporation

- The Ricoh Company, Ltd

List of Tables

- Table 1 Global Dye Sensitized Solar Cell Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Dye Sensitized Solar Cell Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Dye Sensitized Solar Cell Market Outlook, By Natural Dye Sensitizer (2021-2030) ($MN)

- Table 4 Global Dye Sensitized Solar Cell Market Outlook, By Dye of Chlorophyll (2021-2030) ($MN)

- Table 5 Global Dye Sensitized Solar Cell Market Outlook, By Dye of Anthocyanin (2021-2030) ($MN)

- Table 6 Global Dye Sensitized Solar Cell Market Outlook, By Dye of Beta-Carotene (2021-2030) ($MN)

- Table 7 Global Dye Sensitized Solar Cell Market Outlook, By Dye of Betanin (2021-2030) ($MN)

- Table 8 Global Dye Sensitized Solar Cell Market Outlook, By Other Natural Dye Sensitizers (2021-2030) ($MN)

- Table 9 Global Dye Sensitized Solar Cell Market Outlook, By Synthetic Dye Sensitizer (2021-2030) ($MN)

- Table 10 Global Dye Sensitized Solar Cell Market Outlook, By Cobalt-Based Dyes (2021-2030) ($MN)

- Table 11 Global Dye Sensitized Solar Cell Market Outlook, By Porphyrin-Based Dyes (2021-2030) ($MN)

- Table 12 Global Dye Sensitized Solar Cell Market Outlook, By Ruthenium-Based Dyes (2021-2030) ($MN)

- Table 13 Global Dye Sensitized Solar Cell Market Outlook, By Tetrahydroquinoline-Based Dyes (2021-2030) ($MN)

- Table 14 Global Dye Sensitized Solar Cell Market Outlook, By Azo Dyes (2021-2030) ($MN)

- Table 15 Global Dye Sensitized Solar Cell Market Outlook, By Perylene-Based Dyes (2021-2030) ($MN)

- Table 16 Global Dye Sensitized Solar Cell Market Outlook, By Thiacyanine Dyes (2021-2030) ($MN)

- Table 17 Global Dye Sensitized Solar Cell Market Outlook, By Triphenylamine-Based Dyes (2021-2030) ($MN)

- Table 18 Global Dye Sensitized Solar Cell Market Outlook, By Other Synthetic Dye Sensitizers (2021-2030) ($MN)

- Table 19 Global Dye Sensitized Solar Cell Market Outlook, By Application (2021-2030) ($MN)

- Table 20 Global Dye Sensitized Solar Cell Market Outlook, By Portable Charging (2021-2030) ($MN)

- Table 21 Global Dye Sensitized Solar Cell Market Outlook, By Building Integrated Photovoltaic (2021-2030) ($MN)

- Table 22 Global Dye Sensitized Solar Cell Market Outlook, By Embedded Electronics (2021-2030) ($MN)

- Table 23 Global Dye Sensitized Solar Cell Market Outlook, By Automotive Integrated Photovoltaic (AIP) (2021-2030) ($MN)

- Table 24 Global Dye Sensitized Solar Cell Market Outlook, By Building-Applied Photovoltaics (BAPVs) (2021-2030) ($MN)

- Table 25 Global Dye Sensitized Solar Cell Market Outlook, By Outdoor Advertising (2021-2030) ($MN)

- Table 26 Global Dye Sensitized Solar Cell Market Outlook, By Solar Chargers (2021-2030) ($MN)

- Table 27 Global Dye Sensitized Solar Cell Market Outlook, By Wireless Keyboards (2021-2030) ($MN)

- Table 28 Global Dye Sensitized Solar Cell Market Outlook, By Emergency Power in Military (2021-2030) ($MN)

- Table 29 Global Dye Sensitized Solar Cell Market Outlook, By Other Applications (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Dye Sensitized Solar Cell Market is accounted for $155.01 million in 2023 and is expected to reach $397.50 million by 2030 growing at a CAGR of 14.4% during the forecast period. The class of thin-film solar cells that dye-sensitized solar cells (DSSC) are a part of is made of molecularly dyed titanium dioxide nanoparticles and aids in absorbing sunlight. The photo electrochemical system that results from the formation of a semiconductor between a photo-sensitized anode and an electrolyte is the foundation of the DSSC. Moreover, a metal oxide semiconductor and a dye that absorbs light make up this solar cell. The dye is energized by solar radiation and transfers this energy to the metal oxide, which then produces electricity.

According to the International Renewable Energy Agency, the installed capacity of solar photovoltaic (PV) cells in the U.S. stood at 1,614 MW in 2009 and increased to 75,572 MW in 2020. According to the U.S Office of Energy Efficiency & Renewable Energy, by 2030 more than 1 in 7 U.S. homeowners will have solar roof systems.

Market Dynamics:

Driver:

Efficiency in energy use and sustainability

DSSCs are renowned for their energy efficiency, and because of their superior photon-to-electron conversion efficiency, they can produce electricity even in low-light situations. Additionally, their sustainability is what motivates people to adopt them. When switching to cleaner energy systems, DSSCs are a desirable option because they provide a renewable energy source that lowers the carbon footprint. Their low embodied energy, or the ratio of the energy used in their manufacture to the energy they produce over their lifetime, adds to their sustainability profile.

Restraint:

Lower efficiency than silicon solar cells

In terms of energy conversion efficiency, DSSCs have historically lagged behind silicon-based solar cells, primarily because they have lower photon-to-electron conversion rates. This limitation limits their use in large-scale solar installations, where it is crucial to maximize energy output within a constrained footprint. DSSC efficiency is actively being improved by ongoing research, but the path to better performance is not without its challenges. The incorporation of more complex engineering and advanced materials is frequently necessary to increase efficiency, complicating DSSC designs. Furthermore, these developments might result in higher production costs, which might put DSSCs' cost-effectiveness in the shadow of more established solar technologies.

Opportunity:

Wearable technology and consumer electronics

A promising opportunity exists for DSSCs in the growing market for wearable and portable electronics. Due to their lightweight and flexible construction, they can be easily incorporated into consumer goods like smartphones, smart watches, outdoor clothing, and equipment. Moreover, DSSCs can also lessen the frequency with which these devices need to be recharged, improving user convenience and lowering the environmental impact of disposable batteries by extending the life of the batteries in these devices or providing additional power. Consumers and the long-term viability of electronic devices benefit from this.

Threat:

Competition from silicon-based solar cell

The silicon-based solar cells that have long dominated the solar energy market present DSSCs with formidable competition. Due to silicon solar technology's higher energy conversion efficiencies, proven dependability, and economies of scale, it is difficult for DSSCs to capture a sizable portion of the market. Additionally, efficiency is crucial in large-scale solar installations, where DSSCs frequently find it difficult to successfully compete. It's critical to highlight the distinctive benefits of DSSCs, such as flexibility and architectural integration, in order to counter this threat and locate markets where they can succeed.

COVID-19 Impact:

The dye-sensitive solar cell (DSSC) market was significantly impacted by the COVID-19 pandemic in a number of ways. On the one hand, challenges presented by disruptions in global manufacturing and supply chains caused temporary slowdowns in production and distribution. Positively, the pandemic has hastened the switch to renewable energy sources, such as DSSCs, as nations and businesses work to create more resilient and sustainable energy systems. Furthermore, DSSCs, with their potential for architectural integration and decentralized energy generation, gained attention as a component of the solution as awareness of environmental issues grew.

The synthetic dye sensitizers segment is expected to be the largest during the forecast period

During the forecast period, the synthetic dye sensitizers segment is anticipated to hold the largest market share. When compared to natural dye sensitizers, synthetic dyes often have higher efficacy due to their precision control over their properties, stability, and other factors. Because of their chemical structures' adaptability, it is possible to tailor their light absorption and electron transfer characteristics, which boosts DSSC performance. Moreover, synthetic dyes are also less prone to environmental degradation, which can increase the robustness and longevity of DSSCs. As a result, the dominance of synthetic dye sensitizer technology in the market has been influenced by these elements.

The Building Integrated Photovoltaic (BIPV) segment is expected to have the highest CAGR during the forecast period

During the anticipated period, the Building Integrated Photovoltaic (BIPV) segment had the highest CAGR. Direct integration of solar panels into building components and structures, such as roofs, facades, and windows, is known as BIPV. Moreover, this novel method not only produces renewable energy but also improves building aesthetics and lessens construction's carbon footprint. BIPV solutions have gained a lot of traction as the focus on sustainable and energy-efficient buildings has increased, especially in areas encouraging the use of renewable energy sources.

Region with largest share:

In the dye-sensitive solar cell (DSSC) market, North America is anticipated to account for the largest share. This was mainly brought about by increased investments in renewable energy technologies, a rise in the importance of sustainability, and the incorporation of DSSCs into various applications. For architectural integration, portable electronics, and military applications, DSSCs have attracted a lot of interest, particularly in the United States. Also, contributing actively to the creation and innovation of the DSSC were research organizations and businesses in North America.

Region with highest CAGR:

The Asia-Pacific region is anticipated to have lucrative growth during the forecast period. Factors like the region's expanding manufacturing capacities, especially in nations like China and South Korea, where significant investments were made in renewable energy technologies, were the main drivers of this robust growth. Additionally, the adoption of DSSCs in consumer electronics and building-integrated photovoltaics, along with Asia-Pacific's growing awareness of environmental sustainability, contributed to its remarkable growth.

Key players in the market:

Some of the key players in Dye Sensitized Solar Cell Market include: 3GSolar, Ltd., Everlight Chemical Industrial Corp., Exeger Operations AB, Fujikura Ltd., G24 Power Ltd., Greatcell Energy, Merck Group, Nissha Co., Ltd., Oxford Photovoltaics, Peccell Technologies, Inc., Renesas Electronics Corporation., Sharp Corporation, Sinovoltaics Group Limited, Solaris Nanosciences, Sony Corporation and The Ricoh Company, Ltd.

Key Developments:

In July 2023, Renesas Electronics Corporation, a premier supplier of advanced semiconductor solutions, and Wolf speed, Inc., the global leader in silicon carbide technology, today announced the execution of a wafer supply agreement and $2 billion (USD) deposit by Renesas to secure a 10 year supply commitment of silicon carbide bare and epitaxial wafers from Wolf speed.

In May 2023, Sony Corporation and Astellas Pharma Inc. today announced that they have entered into a collaborative research agreement to discover a novel Antibody-Drug Conjugate *1 platform in oncology based on Sony's unique polymeric material, "KIRAVIA™*2 Backbone*3." ADC is expected to selectively deliver anti-cancer drugs to target cells, thereby increasing efficacy and reducing side effects caused by anti-cancer drugs attacking normal cells.

In May 2023, Australia's largest solar distributor, OSW, has announced a partnership with Japanese residential PV module manufacturer Sharp, which has more than 60 years of experience in the global solar industry. The new distribution arrangement between the two companies promises to deliver high-quality solar products and services to Australian residents. OSW offers a wide range of solar products, including PV panels, inverters, EV chargers and solar storage options, with six warehouses located across Australia.

Types Covered:

- Natural Dye Sensitizer

- Synthetic Dye Sensitizer

- Other Types

Applications Covered:

- Portable Charging

- Building Integrated Photovoltaic

- Embedded Electronics

- Automotive Integrated Photovoltaic (AIP)

- Building-Applied Photovoltaic's (BAPVs)

- Outdoor Advertising

- Solar Chargers

- Wireless Keyboards

- Emergency Power in Military

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Dye Sensitized Solar Cell Market, By Type

- 5.1 Introduction

- 5.2 Natural Dye Sensitizer

- 5.2.1 Dye of Chlorophyll

- 5.2.2 Dye of Anthocyanin

- 5.2.3 Dye of Beta-Carotene

- 5.2.4 Dye of Betanin

- 5.2.5 Other Natural Dye Sensitizers

- 5.3 Synthetic Dye Sensitizer

- 5.3.1 Cobalt-Based Dyes

- 5.3.2 Porphyrin-Based Dyes

- 5.3.3 Ruthenium-Based Dyes

- 5.3.4 Tetrahydroquinoline-Based Dyes

- 5.3.5 Azo Dyes

- 5.3.6 Perylene-Based Dyes

- 5.3.7 Thiacyanine Dyes

- 5.3.8 Triphenylamine-Based Dyes

- 5.3.9 Other Synthetic Dye Sensitizers

6 Global Dye Sensitized Solar Cell Market, By Application

- 6.1 Introduction

- 6.2 Portable Charging

- 6.3 Building Integrated Photovoltaic

- 6.4 Embedded Electronics

- 6.5 Automotive Integrated Photovoltaic (AIP)

- 6.6 Building-Applied Photovoltaics (BAPVs)

- 6.7 Outdoor Advertising

- 6.8 Solar Chargers

- 6.9 Wireless Keyboards

- 6.10 Emergency Power in Military

- 6.11 Other Applications

7 Global Dye Sensitized Solar Cell Market, By Geography

- 7.1 Introduction

- 7.2 North America

- 7.2.1 US

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 Italy

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 New Zealand

- 7.4.6 South Korea

- 7.4.7 Rest of Asia Pacific

- 7.5 South America

- 7.5.1 Argentina

- 7.5.2 Brazil

- 7.5.3 Chile

- 7.5.4 Rest of South America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 Qatar

- 7.6.4 South Africa

- 7.6.5 Rest of Middle East & Africa

8 Key Developments

- 8.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 8.2 Acquisitions & Mergers

- 8.3 New Product Launch

- 8.4 Expansions

- 8.5 Other Key Strategies

9 Company Profiling

- 9.1 3GSolar, Ltd.

- 9.2 Everlight Chemical Industrial Corp.

- 9.3 Exeger Operations AB

- 9.4 Fujikura Ltd.

- 9.5 G24 Power Ltd.

- 9.6 Greatcell Energy

- 9.7 Merck Group

- 9.8 Nissha Co., Ltd.

- 9.9 Oxford Photovoltaics

- 9.10 Peccell Technologies, Inc.

- 9.11 Renesas Electronics Corporation.

- 9.12 Sharp Corporation

- 9.13 Sinovoltaics Group Limited

- 9.14 Solaris Nanosciences

- 9.15 Sony Corporation

- 9.16 The Ricoh Company, Ltd