|

|

市場調査レポート

商品コード

1351057

過活動膀胱治療市場の2030年までの予測-タイプ別、疾患タイプ別、流通チャネル別、地域別の世界分析Overactive Bladder Treatment Market Forecasts to 2030 - Global Analysis By Type, Disease Type, Distribution Channel and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 過活動膀胱治療市場の2030年までの予測-タイプ別、疾患タイプ別、流通チャネル別、地域別の世界分析 |

|

出版日: 2023年09月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、過活動膀胱治療の世界市場は2023年に36億米ドルを占め、予測期間中のCAGRは6.2%で成長し、2030年には48億米ドルに達すると予測されています。

過活動膀胱(OAB)として知られる疾患は、頻繁で予期せぬ尿意を引き起こし、そのコントロールが課題となります。日中や夜間に頻繁に尿意を催したり、不注意でおしっこが漏れてしまったりします。医療専門家は、症状を分析し、骨盤や直腸に近い臓器を物理的に検査することで、過活動膀胱を特定することができます。過活動膀胱の治療にはさまざまな方法があります。特定の行動を変えたり、薬を使ったり、神経を刺激したりすることは、すべて可能な治療法です。

2021年6月にKrager Journalに掲載された「Mechanism and Priority of Botulinum Neurotoxin A versus Sacral Neuromodulation」という難治性過活動膀胱に対する論文によると、過活動膀胱は世界的に非常に多く、全体の有病率は11.8%であることがわかっています。

神経疾患の有病率の上昇

抗てんかん薬、抗精神病薬、鎮痛薬、抗コリン薬など複数の薬剤が神経疾患の治療に使用されています。人口の高齢化は、新薬や新装置の開発への支出の増加とともに、市場拡大の原動力となっています。さらに、政府規制機関や民間団体は、早期障害診断に関する一般市民の知識を高めるための啓発活動を開始すると予測されます。さらに、強力な開発パイプラインの結果、効果的な医薬品が間もなく市場に投入され、市場拡大を後押しすると予想されます。

頻繁な製品回収

人口の多くが過活動膀胱を患っており、QOLに悪影響を及ぼす慢性疾患です。今後数年間は、OAB治療薬の頻繁なリコールが市場の拡大を妨げる可能性があります。製造上の問題により、シプラ社は2021年6月に米国でソリフェナシン・サクシネート錠7,228瓶をリコールしました。大手製薬企業が自社製品を頻繁にリコールすることは、市場の拡大に水を差します。

研究開発費の増加と新たな治療法の導入

製薬会社やバイオ医薬品会社は現在、過活動膀胱の治療のために最先端の医薬品に投資しており、それらは予測期間を通じて導入されると予想されます。また、現在30以上のOAB治療薬候補が臨床開発段階にあります。これらは3つのフェーズII、7つのフェーズIII、16のフェーズIVプロジェクトに分かれています。過活動膀胱の治療市場は、このような強力なパイプラインと最終的な追加薬や治療法のイントロダクションの結果、成長すると予想されます。サムスン医療センターは、アデノシン三リン酸(ATP)、プロスタグランジンE2(PGE2)、神経成長因子(NGF)など、OAB患者の潜在的バイオマーカーを調査しています。OAB治療市場のプレーヤーは、このような進歩の結果、大きな成長の見通しから利益を得ることが期待できます。

普及に関する知識不足

市場の拡大を妨げている要因のひとつは、第III相開発段階または登録前の段階にある薬剤が少ないことです。さらに、予測期間を通じて、補完療法の利用可能性、新興市場のヘルスケアインフラの不足、適格な専門医の不足が市場拡大の妨げとなっています。製品の回収や政府の厳しい規制も業界の拡大を妨げています。

COVID-19の影響:

COVID-19の発生は、過活動膀胱分野の世界的拡大に有益な影響を与えました。患者の膀胱機能障害はCOVID-19関連膀胱炎(CAC)によって大きく悪化し、他の臓器に特有の問題も引き起こしました。このことは、流行中も流行後も過活動膀胱の治療薬市場に好影響を与えました。一方、COVID-19の流行は、ヘルスケアシステムにとって最大の難関のひとつとなっています。米国、中国、日本、インド、ドイツといった重要な国々で長期にわたる封鎖措置がとられたため、COVID-19パンデミックの流行は生産施設の一部または全停止を招いた。これは過活動膀胱治療薬の生産に若干の影響を与えました。

予測期間中、抗コリン薬セグメントが最大となる見込み

過活動膀胱症候群の治療薬の主な選択肢は抗コリン薬であるため、抗コリン薬セグメントは有利な成長を遂げると推定されます。また、米国食品医薬品局によるジェネリック医薬品の迅速な製品承認が、抗コリン薬市場の拡大を支えています。さらに、侵襲的な手術や経口薬よりもボトックス治療を好むエンドユーザーの動きが、過活動膀胱治療市場における同分野の発展の可能性を予測期間中に高めると予測されています。

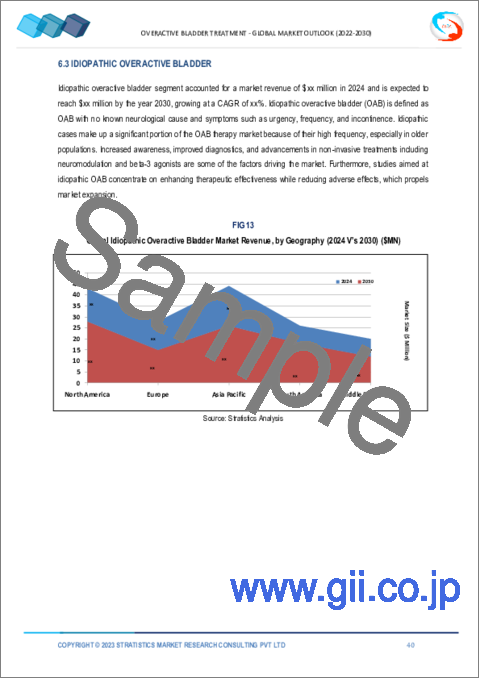

特発性過活動膀胱分野は予測期間中に最も高いCAGRが見込まれる

特発性過活動膀胱分野は、患者の特発性過活動膀胱発症率の上昇と特発性過活動膀胱治療に対する需要の高まりにより、予測期間中に最も高いCAGR成長が見込まれます。一方、神経因性過活動膀胱の分野は、過活動膀胱の発生率を増加させると予測される神経疾患の増加により、予測期間中に最も速い速度で拡大すると予測されます。

最大のシェアを占める地域

北米は、ヘルスケア分野が堅調であることから、予測期間中に最大の市場シェアを占めると予測されます。加えて、過活動膀胱治療に対する償還、高齢化に伴う発症率の増加、同地域における重要な業界プレイヤーの存在といった要因もあります。さらに、同市場は高齢者人口の増加や、同地域における高齢化人口の実質的な存在からも恩恵を受けるとみられます。

CAGRが最も高い地域:

欧州は、同地域における製薬企業の存在と、中国やインドのような人口の多い国の購買力の上昇により、予測期間中のCAGRが最も高くなると予測されます。さらに、医療支出の増加や、過活動膀胱の治療薬の生産を強化するためのハイテク製造技術の使用は、最大の製薬部門と医薬品の最大の供給量を持ち、この地域の医薬品生産者にとって豊富な原材料へのアクセスが容易です。加えて、産業インフラが拡大し、可処分所得が増加し、この地域における国内企業のプレゼンスが確立されているためです。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の過活動膀胱治療市場:タイプ別

- 抗コリン薬

- ダリフェナシン

- フェソテロジン

- オキシブチニン

- ソリフェナシン

- トルテロジン

- トロスピウム

- その他の抗コリン薬

- ミラベグロン

- ボトックス

- 神経調節

- その他の治療法

第6章 世界の過活動膀胱治療市場:疾患タイプ別

- 神経因性過活動膀胱

- パーキンソン病

- ストローク

- 多発性硬化症

- 脊髄損傷

- 特発性過活動膀胱

- 他の種類の病気

第7章 世界の過活動膀胱治療市場:流通チャネル別

- 病院薬局

- ドラッグストアおよび小売薬局

- オンラインプロバイダー

- その他の流通チャネル

第8章 世界の過活動膀胱治療市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイル

- Dr. Reddy's Laboratories Ltd

- Pfizer Inc.

- Cipla Ltd

- Lupin

- Sun Pharmaceutical Industries Ltd.

- Astellas Pharma Inc.

- AbbVie Inc.

- Alembic Pharmaceuticals Limited

- Sumitomo Pharma Co., Ltd

- Teva Pharmaceutical Industries Limited

- Johnson & Johnson Services, Inc.

- Medtronic

- Sanofi

- Uro Medical

- Urovant Sciences

- Macleods Pharmaceuticals Ltd

- Endo International PLC

- Hisamitsu Pharmaceutical Co., Inc.

- Laborie

List of Tables

- Table 1 Global Overactive Bladder Treatment Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Overactive Bladder Treatment Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Overactive Bladder Treatment Market Outlook, By Anticholinergics (2021-2030) ($MN)

- Table 4 Global Overactive Bladder Treatment Market Outlook, By Darifenacin (2021-2030) ($MN)

- Table 5 Global Overactive Bladder Treatment Market Outlook, By Fesoterodine (2021-2030) ($MN)

- Table 6 Global Overactive Bladder Treatment Market Outlook, By Oxybutynin (2021-2030) ($MN)

- Table 7 Global Overactive Bladder Treatment Market Outlook, By Solifenacin (2021-2030) ($MN)

- Table 8 Global Overactive Bladder Treatment Market Outlook, By Tolterodine (2021-2030) ($MN)

- Table 9 Global Overactive Bladder Treatment Market Outlook, By Trospium (2021-2030) ($MN)

- Table 10 Global Overactive Bladder Treatment Market Outlook, By Other Anticholinergics (2021-2030) ($MN)

- Table 11 Global Overactive Bladder Treatment Market Outlook, By Mirabegron (2021-2030) ($MN)

- Table 12 Global Overactive Bladder Treatment Market Outlook, By BOTOX (2021-2030) ($MN)

- Table 13 Global Overactive Bladder Treatment Market Outlook, By Neuromodulation (2021-2030) ($MN)

- Table 14 Global Overactive Bladder Treatment Market Outlook, By Other Treatments (2021-2030) ($MN)

- Table 15 Global Overactive Bladder Treatment Market Outlook, By Disease Type (2021-2030) ($MN)

- Table 16 Global Overactive Bladder Treatment Market Outlook, By Neurogenic Overactive Bladder (2021-2030) ($MN)

- Table 17 Global Overactive Bladder Treatment Market Outlook, By Parkinson's disease (2021-2030) ($MN)

- Table 18 Global Overactive Bladder Treatment Market Outlook, By Strokes (2021-2030) ($MN)

- Table 19 Global Overactive Bladder Treatment Market Outlook, By Multiple Sclerosis (2021-2030) ($MN)

- Table 20 Global Overactive Bladder Treatment Market Outlook, By Spinal Cord Injuries (2021-2030) ($MN)

- Table 21 Global Overactive Bladder Treatment Market Outlook, By Idiopathic Overactive Bladder (2021-2030) ($MN)

- Table 22 Global Overactive Bladder Treatment Market Outlook, By Other Disease Types (2021-2030) ($MN)

- Table 23 Global Overactive Bladder Treatment Market Outlook, By Distribution Channel (2021-2030) ($MN)

- Table 24 Global Overactive Bladder Treatment Market Outlook, By Hospital Pharmacies (2021-2030) ($MN)

- Table 25 Global Overactive Bladder Treatment Market Outlook, By Drug Stores and Retail Pharmacies (2021-2030) ($MN)

- Table 26 Global Overactive Bladder Treatment Market Outlook, By Online Providers (2021-2030) ($MN)

- Table 27 Global Overactive Bladder Treatment Market Outlook, By Other Distribution Channels (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Overactive Bladder Treatment Market is accounted for $3.6 billion in 2023 and is expected to reach $4.8 billion by 2030 growing at a CAGR of 6.2% during the forecast period. The condition known as overactive bladder (OAB) results in frequent, unexpected urinal urges that can be challenging to control. One can experience frequent urges to urinate during the day and at night, as well as inadvertent pee loss. A medical professional can identify overactive bladder by analyzing the symptoms and physically inspecting the organs close to the pelvic and rectum. Various treatments are available to treat hyperactive bladder. Changing certain behaviors, using medicine, and nerve stimulation are all possible treatments.

According to the article published in Krager Journal titled "Mechanism and Priority of Botulinum Neurotoxin A versus Sacral Neuromodulation" for refractory overactive bladder, in June 2021, overactive bladder is highly prevalent worldwide and found that its overall prevalence was 11.8%.

Market Dynamics:

Driver:

Rising prevalence of neurological conditions

Several drugs, including antiepileptics, antipsychotics, analgesics, and anticholinergics, are used to treat neurological illnesses. The aging population is driving market expansion, along with increased spending on the development of new drugs and devices. Additionally, government regulatory agencies and private groups are projected to launch awareness efforts to raise public knowledge of early disorder diagnosis. Additionally, effective medications will soon enter the market as a result of a robust development pipeline, which is expected to fuel market expansion.

Restraint:

Frequent product recalls

A large portion of the population suffers from overactive bladder, a chronic medical condition that has an adverse effect on quality of life. The expansion of the market could be hampered in the coming years by frequent recalls of OAB-treating medications. Due to production problems, Cipla recalled 7,228 bottles of Solifenacin Succinate tablets in the US in June 2021. Leading pharmaceutical corporations frequently recalling their products hurts the market's expansion.

Opportunity:

Increasing R&D spending and the introduction of new treatments

Pharmaceutical and biopharmaceutical companies are now investing in cutting-edge medicines for the treatment of overactive bladders, which are anticipated to be introduced throughout the projected period. In addition, more than 30 OAB candidates are presently in clinical development pathways. These are divided into three Phase II, seven Phase III, and sixteen Phase IV projects. The market for treating overactive bladder is anticipated to grow as a result of this strong pipeline and the eventual introduction of additional medications and therapies. Samsung Medical Center is researching potential biomarkers in OAB patients, including adenosine triphosphate (ATP), prostaglandin E2 (PGE2), and nerve growth factor (NGF). Players in the OAB treatment market can anticipate benefiting from significant growth prospects as a result of such advances.

Threat:

Lack of knowledge about its prevalence

One of the things preventing the market from expanding is the dearth of medications in Phase III development or the pre-registration stages. Additionally, throughout the forecast period, market expansion is hampered by the availability of complementary therapies, a lack of healthcare infrastructure in developing nations, and a shortage of qualified specialists. Recalls of products and stringent government regulations are also impeding industry expansion.

COVID-19 Impact:

The COVID-19 outbreak had a beneficial effect on the expansion of the overactive bladder sector globally. The patient's bladder dysfunction was greatly exacerbated by COVID-19 association cystitis (CAC), which also caused issues unique to other organs. This had a favorable effect on the market for treatments for overactive bladder both during and after the epidemic. The COVID-19 epidemic, on the other hand, presented one of the greatest difficulties for the healthcare system. Due to the protracted lockdown in important nations like the United States, China, Japan, India, and Germany, the COVID-19 pandemic outbreak has resulted in the partial or total suspension of production facilities. This had some impact on the production of drugs for overactive bladder.

The anticholinergics segment is expected to be the largest during the forecast period

The anticholinergics segment is estimated to have a lucrative growth, due to the primary choice of medications for treating overactive bladder syndrome is anticholinergics. Additionally, the U.S. Food and Drug Administration's quick product approvals for generic medications support the expansion of the anticholinergic market. Additionally, it has been predicted that a movement in end users' preferences of botox treatment over invasive surgery or oral drugs will increase the segment's development potential in the overactive bladder therapeutics market over the course of the projection year.

The idiopathic overactive bladder segment is expected to have the highest CAGR during the forecast period

The idiopathic overactive bladder segment is anticipated to witness the highest CAGR growth during the forecast period, due to rising rates of idiopathic overactive bladder in patients and rising demand for overactive bladder drugs for the treatment of idiopathic overactive bladder. The sector for neurogenic overactive bladder, on the other hand, is anticipated to expand at the quickest rate during the forecast period due to the rise in neurological diseases, which is predicted to increase the incidence of overactive bladder.

Region with largest share:

North America is projected to hold the largest market share during the forecast period owing to its robust healthcare sector. In addition, factors such as reimbursement for overactive bladder treatment, an increasing incidence of the condition with advancing age, and the presence of significant industry players in the region. Moreover, the market is set to benefit from the growing elderly population, and the substantial presence of an aging demographic in the region.

Region with highest CAGR:

Europe is projected to have the highest CAGR over the forecast period, due to the presence of pharmaceutical businesses in the area and the rise in the purchasing power of populous nations like China and India. Moreover, an increase in medical spending and the use of high-tech manufacturing techniques to enhance the production of drugs for treating overactive bladder with largest pharmaceutical sector and the largest supply of medicines, with easy access to a plentiful supply of raw materials for pharmaceutical product producers in this region. In addition, because of the expanding industrial infrastructure, rising disposable incomes, and established domestic company presence in the area.

Key players in the market:

Some of the key players profiled in the Overactive Bladder Treatment Market include: Dr. Reddy's Laboratories Ltd, Pfizer Inc. , Cipla Ltd, Lupin, Sun Pharmaceutical Industries Ltd., Astellas Pharma Inc., AbbVie Inc., Alembic Pharmaceuticals Limited, Sumitomo Pharma Co., Ltd, Teva Pharmaceutical Industries Limited, Johnson & Johnson Services, Inc., Medtronic, Sanofi, Uro Medical, Urovant Sciences, Macleods Pharmaceuticals Ltd, Endo International PLC, Hisamitsu Pharmaceutical Co., Inc. and Laborie

Key Developments:

In July 2022, Dr. Reddy's Laboratories introduced fesoterodine fumarate extended-release tablets, a therapeutic generic equivalent to Pfizer's Toviaz (fesoterodine fumarate) ER tablets in the United States for the treatment of overactive bladder.

In April 2022, Dr Reddy's launched generic Methylprednisolone Sodium Succinate for injection in US, The injection is the generic equivalent of SOLUMEDROL and has been approved by the US Food and Drug Administration (USFDA), the company said in a regulatory filing.

In May 2022, Urovant Sciences, a wholly owned subsidiary of Sumitovant Biopharma Ltd., presented data from the Phase 3 EMPOWUR Extension Study of GEMTESA(vibegron) 75 mg overactive bladder therapy.

Treatments Covered:

- Anticholinergics

- Mirabegron

- BOTOX

- Neuromodulation

- Other Treatments

Disease Types Covered:

- Neurogenic Overactive Bladder

- Idiopathic Overactive Bladder

- Other Disease Types

Distribution Channels Covered:

- Hospital Pharmacies

- Drug Stores and Retail Pharmacies

- Online Providers

- Other Distribution Channels

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Emerging Markets

- 3.7 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Overactive Bladder Treatment Market, By Type

- 5.1 Introduction

- 5.2 Anticholinergics

- 5.2.1 Darifenacin

- 5.2.2 Fesoterodine

- 5.2.3 Oxybutynin

- 5.2.4 Solifenacin

- 5.2.5 Tolterodine

- 5.2.6 Trospium

- 5.2.7 Other Anticholinergics

- 5.3 Mirabegron

- 5.4 BOTOX

- 5.5 Neuromodulation

- 5.6 Other Treatments

6 Global Overactive Bladder Treatment Market, By Disease Type

- 6.1 Introduction

- 6.2 Neurogenic Overactive Bladder

- 6.2.1 Parkinson's disease

- 6.2.2 Strokes

- 6.2.3 Multiple Sclerosis

- 6.2.4 Spinal Cord Injuries

- 6.3 Idiopathic Overactive Bladder

- 6.4 Other Disease Types

7 Global Overactive Bladder Treatment Market, By Distribution Channel

- 7.1 Introduction

- 7.2 Hospital Pharmacies

- 7.3 Drug Stores and Retail Pharmacies

- 7.4 Online Providers

- 7.5 Other Distribution Channels

8 Global Overactive Bladder Treatment Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 Dr. Reddy's Laboratories Ltd

- 10.2 Pfizer Inc.

- 10.3 Cipla Ltd

- 10.4 Lupin

- 10.5 Sun Pharmaceutical Industries Ltd.

- 10.6 Astellas Pharma Inc.

- 10.7 AbbVie Inc.

- 10.8 Alembic Pharmaceuticals Limited

- 10.9 Sumitomo Pharma Co., Ltd

- 10.10 Teva Pharmaceutical Industries Limited

- 10.11 Johnson & Johnson Services, Inc.

- 10.12 Medtronic

- 10.13 Sanofi

- 10.14 Uro Medical

- 10.15 Urovant Sciences

- 10.16 Macleods Pharmaceuticals Ltd

- 10.17 Endo International PLC

- 10.18 Hisamitsu Pharmaceutical Co., Inc.

- 10.19 Laborie