|

|

市場調査レポート

商品コード

1339938

自動車用電子機器市場の2030年までの予測:コンポーネント別、推進別、車種別、用途別、販売チャネル別、地域別の世界分析Automotive Electronic Devices Market Forecasts to 2030 - Global Analysis By Component, Propulsion (Electric/Hybrid and Internal Combustion Engine ), Vehicle Type, Application, Sales Channel and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用電子機器市場の2030年までの予測:コンポーネント別、推進別、車種別、用途別、販売チャネル別、地域別の世界分析 |

|

出版日: 2023年08月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の自動車用電子機器市場は2023年に2,576億7,000万米ドルを占め、CAGR7.8%で推移し、2030年には4,359億1,000万米ドルに達すると予測されています。

自動車用電子機器とは、車両制御、安全性、通信、エンターテインメント、ネットワークなど、さまざまな機能を実現するための電子システムやコンポーネントを自動車に搭載することを指します。自動車の性能、有効性、快適性、全体的なユーザー体験はすべて、これらの技術部品によって改善されます。エンジン管理、イグニッション、ラジオ、自動車コンピューター、テレマティックス、車内エンターテインメントなど、多くのシステムで利用されています。

ドイツ自動車工業会(VDA)によると、欧州では2020年上半期に510万台の乗用車が登録されました。

研究開発投資の増加

高性能エレクトロニクスとエネルギー貯蔵技術をリーズナブルな価格で提供するため、自動車業界は研究開発に多額の資源を投入しています。高い安全性を実現するため、OEMはエレクトロニクスへの依存度を高めています。しかし、自動車産業はハードウェア駆動の自動車から、ソフトウェア駆動の自動車へとシフトしつつあります。市場の成長には、自動車1台当たりの電子・ソフトウェア部品の平均量が大幅に増加していることが影響しています。

OEM部品は割高

OEM部品のコストは、アフターマーケット部品よりも高い可能性があります。これは、OEM部品が純正部品メーカーによって製造され、ディーラーのマークアップが入る可能性があるためです。入手可能性が限られていることも、高価格の要因です。ディーラーやオンラインで提供されていても、現在必要な部品を持っているものを発見するのは珍しいです。入手に何週間も何カ月も待たされることもあります。このことが市場拡大を阻害しています。

電気自動車の需要増加

電気自動車の革命は、業界を再構築する重要なテーマのひとつです。この革命には、電気自動車とそれに関連する電子技術の採用拡大が含まれます。電気自動車市場は、環境問題、再生可能エネルギーを支援する法律、バッテリー技術の市場開拓などを背景に、世界規模で徐々に拡大しています。ハイブリッド電気自動車や電気自動車は、バッテリー性能、モーター制御、エネルギー経済性、充電インフラを管理する複雑な電子システムを必要とするため、電気自動車の需要増加は自動車用電子機器市場に直接的な影響を及ぼしています。

高い実装コスト

最先端の電気システムや技術を取り入れることで、自動車全体のコストが劇的に上昇する可能性があります。部品コスト、ソフトウェア開発コスト、テストコスト、統合コストなどがこれに含まれます。特に価格に敏感な経済圏では、カーエレクトロニクスの高コストが顧客にとっての自動車コストを上昇させ、自動車の値ごろ感や普及を制限する可能性があります。その結果、市場全体の拡大が妨げられます。

COVID-19影響:

COVID-19の流行により、世界経済と自動車製造は深刻な影響を受けた。COVID-19の余波により、サプライチェーンに問題が生じ、いくつかの生産施設が閉鎖されました。パンデミックは乗用車と商用車の販売を減少させ、自動車用電子機器部門の需要にも影響を与えました。パンデミック中の困難にもかかわらず、デジタル化とコネクティビティに向けた自動車業界のデジタル変革の加速は、パンデミック後の市場を推進すると予想されます。

予測期間中、センサー分野が最大になる見込み

センサー分野は有利な成長が見込まれます。車両の接近と位置、化学的特性、プロセス変数、物理的側面はすべて、機器カテゴリのセンサーによって検出することができます。乗客の安全とセキュリティを支援する政府の行動は、多くの異なる国々で収益開発を刺激すると予測されます。これらのガジェットは、温度、速度、タイヤ空気圧、状態などを記録し、危険な場合には予防措置を講じるため、現在ではすべての自動車に必要な部分となっています。

先進運転支援システム(ADAS)分野は予測期間中最も高いCAGRが見込まれる

先進運転支援システム(ADAS)分野は、その用途と機能の拡大により、予測期間中に最も速いCAGRの成長が見込まれています。自動車事故を減らし人命を救うために、 促進要因に安全上重要な機能を提供する数多くのADASアプリケーションの1つが視線検出です。その他のADASアプリケーションには、自動緊急ブレーキ、歩行者検知、サラウンドビュー、駐車支援、 促進要因疲労検知、視線検知などがあります。ADASの重要なコンポーネントはセンサーです。基本的なステレオカメラから最新のLiDARまで、センサーは複雑なタスクを実行するために単独で、あるいは組み合わせて使用されます。このように、予想される期間を通じて、車載用電子機器のニーズは、自律走行への欲求の高まりによって煽られると予想されます。

最大のシェアを占める地域

予測期間中、アジア太平洋地域が最大の市場シェアを占めると予測されます。台湾、韓国、マレーシア、タイなどの国々は、電子部品製造活動が盛んであるため、車載エレクトロニクス分野の成長に大きく貢献しています。アジア太平洋地域で必要とされる自動車用電子部品の大半は、中国と日本から供給されています。その他アジア太平洋地域は、自動車用電子部品メーカーの数が少ないため、投資先として最適であり、国内需要を活用する地元サプライヤーに多大なビジネスチャンスを提供しています。さらに、この地域で自動車用電子機器の市場が最も急成長しているのはインドであり、中国市場が最大の市場シェアを占めています。

CAGRが最も高い地域:

人と車の安全・安心に対する関心が高まっていることから、予測期間中、欧州のCAGRが最も高くなると予測されます。欧州はADAS推進の最前線にあり、自動車の安全性を重視しています。自動車への最先端エレクトロニクスの統合は、これらの機能を実現し、より安全な道路を保証し、運転体験全体を向上させるために、こうした安全基準によって推進されています。この地域に、フォルクスワーゲン、シュコダ、アウディ、BMW、ダイムラーなど、評判の高い自動車メーカーがあることは有益です。欧州連合(EU)もまた、交通事故を減らし、安全装備を義務付けるために多くの規制を設けており、これが市場の成長をさらに後押ししています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下のいずれかの無料カスタマイズオプションをご提供いたします:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 仮定

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の自動車用電子機器市場:コンポーネント別

- 電子制御ユニット

- パワーエレクトロニクス

- ハーネス

- センサー

- コントロール

- アクチュエーター

- マイクロコントローラー

- プロセッサー

- ディスプレイ

- スイッチ

- その他のコンポーネント

第6章 世界の自動車用電子機器市場:推進別

- 電気/ハイブリッド

- 内燃機関(ICE)

第7章 世界の車載電子機器市場:車種別

- 二輪車

- 電気自動車

- 小型商用車

- 大型商用車

- 乗用車

第8章 世界の自動車用電子機器市場:用途別

- パワートレイン

- ボディエレクトロニクス

- インフォテイメント

- シャーシ

- ADAS(先進運転支援システム)(ADAS)

- 自動運転システム(ADS)

- 安全システム

第9章 世界の自動車用電子機器市場:販売チャネル別

- アフターマーケット

- OEMメーカー

第10章 世界の自動車用電子機器市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 会社概要

- Robert Bosch GmbH

- HARMAN

- CONTINENTAL AG

- Hitachi Automotive Systems, Ltd.

- Lumotive, Inc.

- DENSO CORPORATION

- Xilinx, Inc.

- Delta Electronics Inc

- Infineon Technologies AG

- Atotech

- MRON Corporation

- Hella Gmbh & Co. Kgaa

- Koninklijke Philips N.V.

- HGM Automotive Electronics

- Valeo Inc.

- Visteon Corporation

- ZF Friedrichshafen AG

- NXP Semiconductors

List of Tables

- Table 1 Global Automotive Electronic Devices Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Automotive Electronic Devices Market Outlook, By Component (2021-2030) ($MN)

- Table 3 Global Automotive Electronic Devices Market Outlook, By Electronic Control Unit (2021-2030) ($MN)

- Table 4 Global Automotive Electronic Devices Market Outlook, By Power Electronics (2021-2030) ($MN)

- Table 5 Global Automotive Electronic Devices Market Outlook, By Harnesses (2021-2030) ($MN)

- Table 6 Global Automotive Electronic Devices Market Outlook, By Sensors (2021-2030) ($MN)

- Table 7 Global Automotive Electronic Devices Market Outlook, By Controls (2021-2030) ($MN)

- Table 8 Global Automotive Electronic Devices Market Outlook, By Actuators (2021-2030) ($MN)

- Table 9 Global Automotive Electronic Devices Market Outlook, By Microcontrollers (2021-2030) ($MN)

- Table 10 Global Automotive Electronic Devices Market Outlook, By Processors (2021-2030) ($MN)

- Table 11 Global Automotive Electronic Devices Market Outlook, By Displays (2021-2030) ($MN)

- Table 12 Global Automotive Electronic Devices Market Outlook, By Switches (2021-2030) ($MN)

- Table 13 Global Automotive Electronic Devices Market Outlook, By Other Components (2021-2030) ($MN)

- Table 14 Global Automotive Electronic Devices Market Outlook, By Propulsion (2021-2030) ($MN)

- Table 15 Global Automotive Electronic Devices Market Outlook, By Electric/Hybrid (2021-2030) ($MN)

- Table 16 Global Automotive Electronic Devices Market Outlook, By Internal Combustion Engine (ICE) (2021-2030) ($MN)

- Table 17 Global Automotive Electronic Devices Market Outlook, By Vehicle Type (2021-2030) ($MN)

- Table 18 Global Automotive Electronic Devices Market Outlook, By Two Wheeler (2021-2030) ($MN)

- Table 19 Global Automotive Electronic Devices Market Outlook, By Electric Vehicle (2021-2030) ($MN)

- Table 20 Global Automotive Electronic Devices Market Outlook, By Light Commercial Vehicles (2021-2030) ($MN)

- Table 21 Global Automotive Electronic Devices Market Outlook, By Heavy Commercial Vehicles (2021-2030) ($MN)

- Table 22 Global Automotive Electronic Devices Market Outlook, By Passenger Cars (2021-2030) ($MN)

- Table 23 Global Automotive Electronic Devices Market Outlook, By Application (2021-2030) ($MN)

- Table 24 Global Automotive Electronic Devices Market Outlook, By Powertrain (2021-2030) ($MN)

- Table 25 Global Automotive Electronic Devices Market Outlook, By Body Electronics (2021-2030) ($MN)

- Table 26 Global Automotive Electronic Devices Market Outlook, By Infotainment (2021-2030) ($MN)

- Table 27 Global Automotive Electronic Devices Market Outlook, By Chassis (2021-2030) ($MN)

- Table 28 Global Automotive Electronic Devices Market Outlook, By Advanced Driver Assistance Systems (ADAS) (2021-2030) ($MN)

- Table 29 Global Automotive Electronic Devices Market Outlook, By Automated Driving Systems (ADS) (2021-2030) ($MN)

- Table 30 Global Automotive Electronic Devices Market Outlook, By Safety Systems (2021-2030) ($MN)

- Table 31 Global Automotive Electronic Devices Market Outlook, By Sales Channel (2021-2030) ($MN)

- Table 32 Global Automotive Electronic Devices Market Outlook, By Aftermarket (2021-2030) ($MN)

- Table 33 Global Automotive Electronic Devices Market Outlook, By Original Equipment Manufacturer (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Automotive Electronic Devices Market is accounted for $257.67 billion in 2023 and is expected to reach $435.91 billion by 2030 growing at a CAGR of 7.8% during the forecast period. Automotive electronic devices refer to the application of electronic systems and components in vehicles for a variety of functions, such as vehicle control, safety, communication, entertainment, and networking. The performance, effectiveness, comfort, and overall user experience of automotive vehicles are all to be improved by these technological components. They are utilized in many systems, including engine management, ignition, radio, automobile computers, telematics, and in-car entertainment.

According to the German Association of the Automotive Industry (VDA), in Europe, 5.1 million passenger cars were registered in the first half of 2020.

Market Dynamics:

Driver:

Raising investments in R&D

In order to provide high-performance electronics and energy storage technologies at a reasonable price, the automobile industry is devoting a sizable amount of resources to research and development. In order to reach a high level of safety, OEMs are now depending increasingly on electronics. However, the automobile sector is shifting away from hardware-driven cars and toward vehicles that are powered by software. The market's growth is impacted by the average amount of electronic and software components per vehicle, which is growing significantly.

Restraint:

OEM parts more expensive

The cost of OEM components may be higher than that of aftermarket parts. This is due to the fact that they are created by the original equipment manufacturer and may have a dealership mark-up. Limited availability is a factor in the high price as well. Even though they are offered by dealerships and online, it is uncommon to discover one that currently has the components you need. There are times when getting one requires a wait of many weeks or months. This factor inhibits market expansion.

Opportunity:

Increasing demand for electric vehicles

The revolution in electric vehicles is one of the key themes reshaping the industry. It encompasses the increasing adoption of electric vehicles and the associated electronic technologies. The market for electric vehicles has been gradually increasing on a worldwide scale, driven by environmental concerns, laws supporting renewable energy, and developments in battery technology. Since hybrid electric vehicles and electric automobiles need complex electronic systems to manage battery performance, motor control, energy economy, and charging infrastructure, the increase in demand for EVs has a direct influence on the market for automotive electronic equipment.

Threat:

High implementation cost

The cost of a vehicle as a whole might climb dramatically with the incorporation of cutting-edge electrical systems and technology. Component costs, software development costs, testing costs, and integration costs are included in this. Particularly in price-sensitive economies, the high cost of automotive electronics can increase the cost of automobiles for customers, restricting their affordability and uptake. The market's overall expansion is hampered as a result.

COVID-19 Impact:

The worldwide economy and the manufacture of automotives have both been severely affected by the COVID-19 epidemic. The aftermath of COVID-19 resulted in issues with the supply chain and the closure of several production facilities. The pandemic has decreased sales of both passenger and commercial automobiles, which has also impacted demand in the automotive electronic devices sector. Despite difficulties during the pandemic, the acceleration of digital transformation in the automobile industry's drive toward digitalization and connectivity is anticipated to propel the market after the epidemic.

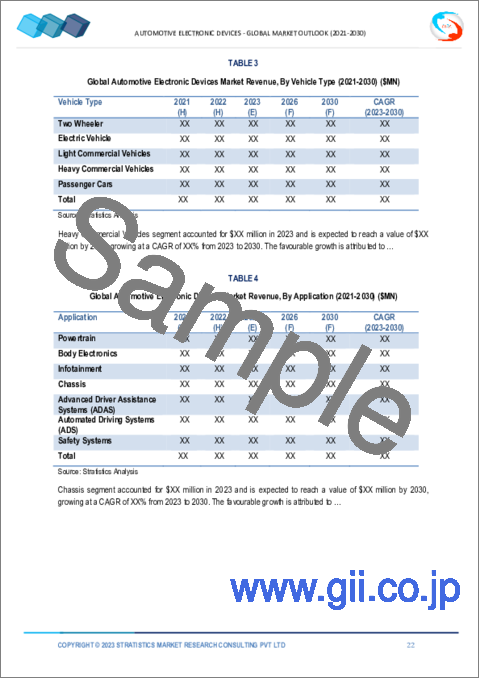

The sensors segment is expected to be the largest during the forecast period

The sensors segment is estimated to have a lucrative growth. A vehicle's proximity and location, chemical properties, process variables, and physical aspects can all be detected by sensors in the equipment category. Governmental actions that assist passenger safety and security are predicted to stimulate revenue development in a number of different countries. These gadgets are now a necessary part of all automotive vehicles since they keep track of things like temperature, speed, tire pressure, and condition while taking preventative action in case of danger.

The advanced driver assistance system (ADAS) segment is expected to have the highest CAGR during the forecast period

The advanced driver assistance system (ADAS) segment is anticipated to witness the fastest CAGR growth during the forecast period, due to its expanded applications and functions. One of the numerous ADAS applications that provide drivers with safety-critical functionality to lessen auto accidents and save lives is gaze detection. Other ADAS applications include automatic emergency braking, pedestrian detection, surround view, parking assist, driver fatigue detection, and gaze detection. An crucial component of ADAS are the sensors. From basic stereo cameras to the most recent LiDAR, sensors are used singly or in combination to carry out complex tasks. Thus, throughout the anticipated period, the need for automotive electronic devices is anticipated to be fueled by the rising desire for autonomous driving.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period. Countries like Taiwan, South Korea, Malaysia, and Thailand have significantly contributed to the rise of the automotive electronics sector due to their robust electronic component manufacturing activities. The majority of the automotive electronics required in the Asia-Pacific region are supplied by China and Japan. The rest of Asia Pacific is a great place to invest because of the small number of automotive electronics manufacturers, which offers tremendous business opportunities for local suppliers to capitalize on the domestic demand. Additionally, the region's fastest-growing market for automotive electronics was India, while the China market had the biggest market share.

Region with highest CAGR:

Europe is projected to have the highest CAGR over the forecast period, owing rising concern for the safety and security of both people and vehicles. Europe has been in the forefront of promoting ADAS and places a high priority on car safety. The integration of cutting-edge electronics into cars is driven by these safety criteria in order to make these features possible, assuring safer roads and improving the entire driving experience. It is beneficial that this region is home to reputable automakers like Volkswagen, Skoda, Audi, BMW, and Daimler, among others. The European Union has also put in place a number of regulations to lower traffic accidents and require safety features which is further propelling the market growth.

Key players in the market:

Some of the key players profiled in the Automotive Electronic Devices Market include: Robert Bosch GmbH, HARMAN, CONTINENTAL AG, Hitachi Automotive Systems, Ltd., Lumotive, Inc., DENSO CORPORATION, Xilinx, Inc., Delta Electronics Inc, Infineon Technologies AG, Atotech, MRON Corporation, Hella Gmbh & Co. Kgaa, Koninklijke Philips N.V., HGM Automotive Electronics, Valeo Inc., Visteon Corporation, ZF Friedrichshafen AG and NXP Semiconductors.

Key Developments:

- In December 2022, NXP and Delta Electronics formed a strategic partnership to develop platforms for future automobiles. The two companies' collaboration labs have also been made public. This partnership's goals include improving electrification alternatives and implementing real-time products based on NXP S32E and S32Z processors. The S32E microcontroller is used to develop smart actuation, safety processing, domain and zonal control, and EV control.

- In May 2022, Continental is widening its broad sensor portfolio by launching two new sensors for electrified vehicles: the Current Sensor Module (CSM) and the Battery Impact Detection (BID) system. Both new solutions focus on protecting the battery and/or on battery parameter retention. This compact modular sensor design measures the current and simultaneously detects temperature. Both values are highly relevant as input for the battery management.

Components Covered:

- Electronic Control Unit

- Power Electronics

- Harnesses

- Sensors

- Controls

- Actuators

- Microcontrollers

- Processors

- Displays

- Switches

- Other Components

Propulsions Covered:

- Electric/Hybrid

- Internal Combustion Engine (ICE)

Vehicle Types Covered:

- Two Wheeler

- Electric Vehicle

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Passenger Cars

Applications Covered:

- Powertrain

- Body Electronics

- Infotainment

- Chassis

- Advanced Driver Assistance Systems (ADAS)

- Automated Driving Systems (ADS)

- Safety Systems

Sales Channels Covered:

- Aftermarket

- Original Equipment Manufacturer

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Automotive Electronic Devices Market, By Component

- 5.1 Introduction

- 5.2 Electronic Control Unit

- 5.3 Power Electronics

- 5.4 Harnesses

- 5.5 Sensors

- 5.6 Controls

- 5.7 Actuators

- 5.8 Microcontrollers

- 5.9 Processors

- 5.10 Displays

- 5.11 Switches

- 5.12 Other Components

6 Global Automotive Electronic Devices Market, By Propulsion

- 6.1 Introduction

- 6.2 Electric/Hybrid

- 6.3 Internal Combustion Engine (ICE)

7 Global Automotive Electronic Devices Market, By Vehicle Type

- 7.1 Introduction

- 7.2 Two Wheeler

- 7.3 Electric Vehicle

- 7.4 Light Commercial Vehicles

- 7.5 Heavy Commercial Vehicles

- 7.6 Passenger Cars

8 Global Automotive Electronic Devices Market, By Application

- 8.1 Introduction

- 8.2 Powertrain

- 8.3 Body Electronics

- 8.4 Infotainment

- 8.5 Chassis

- 8.6 Advanced Driver Assistance Systems (ADAS)

- 8.7 Automated Driving Systems (ADS)

- 8.8 Safety Systems

9 Global Automotive Electronic Devices Market, By Sales Channel

- 9.1 Introduction

- 9.2 Aftermarket

- 9.3 Original Equipment Manufacturer

10 Global Automotive Electronic Devices Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Robert Bosch GmbH

- 12.2 HARMAN

- 12.3 CONTINENTAL AG

- 12.4 Hitachi Automotive Systems, Ltd.

- 12.5 Lumotive, Inc.

- 12.6 DENSO CORPORATION

- 12.7 Xilinx, Inc.

- 12.8 Delta Electronics Inc

- 12.9 Infineon Technologies AG

- 12.10 Atotech

- 12.11 MRON Corporation

- 12.12 Hella Gmbh & Co. Kgaa

- 12.13 Koninklijke Philips N.V.

- 12.14 HGM Automotive Electronics

- 12.15 Valeo Inc.

- 12.16 Visteon Corporation

- 12.17 ZF Friedrichshafen AG

- 12.18 NXP Semiconductors