|

|

市場調査レポート

商品コード

1324337

次世代データストレージ市場の2030年までの予測- ストレージシステム別、ストレージメディア別、ストレージアーキテクチャ別、導入タイプ別、エンドユーザー別、地域別の世界分析Next-Generation Data Storage Market Forecasts to 2030 - Global Analysis By Storage System, Storage Medium, Storage Architecture, Deployment Type, End User and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 次世代データストレージ市場の2030年までの予測- ストレージシステム別、ストレージメディア別、ストレージアーキテクチャ別、導入タイプ別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2023年08月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の次世代データストレージ市場は2023年に1,045億米ドルを占め、2030年には2,696億2,000万米ドルに達すると予測され、予測期間中のCAGRは14.5%です。

次世代データストレージとは、大量のデータと多様なワークロードを管理する組織の変化する要件を満たすために開発された、最先端のストレージ技術と製品群を指します。従来のストレージ・システムと比較して、次世代データ・ストレージは、より高いパフォーマンス、拡張性の向上、エネルギー効率の向上により、リアルタイムのデータ処理、シームレスなデータ統合、迅速なデータ・アクセスを容易にします。

アドバンスト・ストレージ・テクノロジー・コンソーシアムの技術ロードマップによると、HDDの容量は2025年までに100TBまで増加し、シャイニング磁気記録、垂直磁気記録、強化キャッシング、さらにはケーシング内にヘリウムを設置するなどの新しい書き込み技術が可能になります。

市場力学:

クラウド・コンピューティングの利用拡大

業界全体でクラウド・コンピューティング・サービスが広く採用された結果、データの保存、アクセス、管理は急激な変化を遂げました。クラウドベースのアプリケーションやサービスには、スケーラブルで信頼性が高く、高性能なストレージ・ソリューションが必要です。クラウドベースの環境の変化する要求に対応するためには、分散ストレージシステム、ソフトウェア定義ストレージ(SDS)、オブジェクトストレージなどの次世代データストレージ技術が必要です。さらに、これらのソリューションは、異なるクラウドプラットフォーム間でのデータの移動、複製、移動を容易にします。

互換性とデータ移行の問題

レガシーデータストレージシステムから次世代ソリューションに切り替える際、データ移行や互換性の問題が発生する可能性があります。従来のストレージ・インフラに投資してきた組織では、データ・フォーマットの不整合、データ損失のリスク、移行中の混乱に遭遇する可能性があります。さらに、ストレージ技術は急速に進化しているため、新しいストレージソリューションを既存のインフラに統合する際、企業は互換性の課題に直面することがよくあります。レガシーシステムから先進的なストレージプラットフォームに移行する際、データ移行の課題が現れ、データフォーマットの不一致、データ損失のリスク、移行プロセス中の混乱が生じる可能性があります。

ストレージ技術の近代化

NVMe(Non-Volatile Memory Express)、ストレージクラスメモリ、SMR(Shingled Magnetic Recording)などのストレージ技術の革新により、データストレージ市場は継続的な成長を遂げています。さらに、これらの技術的進歩を利用して、より迅速で信頼性が高く、エネルギー効率の高いストレージ・ソリューションを提供できる企業は優位に立つことができます。これらの開発を利用して、高性能ストレージ アレイや最先端のストレージ システムを作成する市場機会が存在します。

持続可能性と環境問題

環境と持続可能性の問題は、市場にとって深刻な脅威です。データセンターとストレージ・インフラは大量のエネルギーを使用するため、二酸化炭素排出量が増加し、データストレージのニーズが増大するにつれて環境に悪影響を及ぼします。さらに、クラウド・コンピューティングやデータ集約型アプリケーションの急成長により、データ・ストレージ施設はエネルギー需要を増大させています。また、古くなったり使用期限が切れたストレージ・ハードウェアの廃棄は、電子廃棄物(e-waste)の蓄積に拍車をかけ、すでに困難な環境問題を悪化させています。

COVID-19の影響

次世代データストレージ市場は、COVID-19の大流行によって大きな影響を受けた。リモートワーク、オンライン学習、デジタル化の増加により、拡張性があり、効果的で安全なデータストレージ・ソリューションの需要が高まっています。クラウドベースのストレージやデータ管理サービスの利用は、組織が増大するデータ量を管理しようとして急速に増加しました。対照的に、サプライチェーンの混乱と経済の乱高下は、ハードウェアの販売とインフラ投資を一時的に減速させました。しかし、企業が今後の課題に直面した際の回復力と適応力の強化に注力する中、パンデミックはデータストレージ技術の革新を加速させ、エッジコンピューティングやハイブリッドクラウドソリューションのような先進技術へと市場を牽引しました。

予測期間中、オンプレミス部門が最大になる見込み

予測期間中、オンプレミス・セグメントが最大のシェアを占めると予想されます。データおよびストレージインフラを完全に管理できる企業は、カスタマイズされたセキュリティ対策を講じることができ、このセグメントではデータ主権と業界固有の規制への適合が保証されます。さらに、セキュリティとプライバシー機能の強化により、データ漏洩や不正アクセスも減少します。データがローカルに保存されるという事実により、オンプレミス・ストレージは低レイテンシーと迅速なデータ・アクセスも提供し、重要な情報の検索をスピードアップします。このような利点から、オンプレミスのデータ・ストレージは、特に機密データを扱い、データ・プライバシー規制が厳しい部門にとって、望ましい選択肢となっています。

予測期間中、ファイル&オブジェクトベースストレージセグメントのCAGRが最も高くなる見込み

ファイルベース&オブジェクトベースのストレージ分野は、予測期間中に最も速いCAGR成長が見込まれます。同市場では、ファイルベースとオブジェクトベースのストレージセグメントが顕著に増加しています。ビッグデータ分析、モノのインターネット(IoT)、クラウドコンピューティングの採用により、スケーラブルで適応性の高いストレージソリューションが求められていることが、この成長の背景にあると考えられます。そのシンプルさと使いやすさから、ネットワーク接続型ストレージ(NAS)のようなファイルベースのストレージは、中小企業にとって理想的なものとなっています。ファイルベースのストレージは今でも広く使われています。さらに、ファイルベースとオブジェクトベースのストレージは、企業が増え続けるデータセットを作成・管理する中で、今後も成長を続け、現代企業の多様なストレージニーズに応えていくことができます。

最大のシェアを占める地域:

予測期間中、北米が次世代データストレージの最大市場シェアを占めると予想されます。先進的なデータストレージ技術は北米で最初に採用されました。消費者も多国籍企業も米国に集中しています。さらに、ハイパースケールデータセンターも急速に普及し、主にこの地域のクラウドコンピューティングプロバイダーやソーシャルネットワークサービスプロバイダーによって利用されています。予想される期間中、3Dプリンティングや分子ストレージのような技術的に先進的な製品に簡単にアクセスできるようになることで、北米市場の成長見通しがさらに促進される可能性が高いです。

CAGRが最も高い地域:

アジア太平洋地域の次世代データストレージ市場は、予測期間中に最も高いCAGRを記録すると予測されます。同地域の次世代データストレージシステムに対する需要の高まりは、急速な都市化と次世代データストレージソリューションのプロバイダーによる研究開発費の増加に大きく影響されています。中国と日本はともに急速な経済成長を遂げています。これらの国の企業は、熾烈な競争に勝ち抜くために最先端技術を取り入れています。さらに、この地域の企業は、競争力を維持し、業務効率、業務成果、財務収益性を向上させるため、IT能力の強化に投資しています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下のいずれかの無料カスタマイズオプションをご提供いたします:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- エグゼクティブサマリー

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 一次調査情報源

- 二次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 次世代データストレージ世界市場:ストレージシステム別

- 直接接続型ストレージ(DAS)

- ネットワーク接続型ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- その他のストレージシステム

第6章 次世代データストレージの世界市場:ストレージメディア別

- ハードディスクドライブ(HDD)

- ソリッド・ステート・ドライブ(SSD)

- 磁気テープ

- オールフラッシュ・アレイ

- ハイブリッド・フラッシュ・アレイ

- その他のストレージ媒体

第7章 次世代データストレージ世界市場:ストレージアーキテクチャ別

- ファイルベースとオブジェクトベースのストレージ

- ファイルストレージ

- オブジェクトストレージ

- ブロックストレージ

- その他のストレージアーキテクチャ

第8章 次世代データストレージの世界市場:導入タイプ別

- オンプレミス

- クラウド

- ハイブリッド

- その他の展開タイプ

第9章 次世代データストレージの世界市場:エンドユーザー別

- BFSI(銀行、金融サービス、保険)

- 製造業

- 消費財・小売

- ヘルスケア・ライフサイエンス

- メディアとエンターテインメント

- 政府機関

- クラウドサービスプロバイダー

- 通信事業者

- その他エンドユーザー

第10章 次世代データストレージの世界市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、提携、合弁事業

- 買収と合併

- 新製品の上市

- 事業拡大

- その他の主要戦略

第12章 企業プロファイル

- Adesto Technologies Corporation.

- Avalanche Technology

- Cypress Semiconductor Corporation.

- DataDirect Networks

- Dell Technologies Inc.

- Everspin Technologies Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Company

- Hitachi, Ltd.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- International Business Machines Corporation

- MicronTechnology Inc.

- NXP Semiconductors.

- Pure Storage, Inc.

- Samsung

- SK HYNIX INC.

- Spin Memory Inc.

- Texas Instruments Incorporated.

- Toshiba CORPORATION

- Western Digital Corporation

List of Tables

- Table 1 Global Next-Generation Data Storage Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Next-Generation Data Storage Market Outlook, By Storage System (2021-2030) ($MN)

- Table 3 Global Next-Generation Data Storage Market Outlook, By Direct-attached Storage (DAS) (2021-2030) ($MN)

- Table 4 Global Next-Generation Data Storage Market Outlook, By Network-attached Storage (NAS) (2021-2030) ($MN)

- Table 5 Global Next-Generation Data Storage Market Outlook, By Storage Area Network (SAN) (2021-2030) ($MN)

- Table 6 Global Next-Generation Data Storage Market Outlook, By Other Storage Systems (2021-2030) ($MN)

- Table 7 Global Next-Generation Data Storage Market Outlook, By Storage Medium (2021-2030) ($MN)

- Table 8 Global Next-Generation Data Storage Market Outlook, By Hard Disk Drive (HDD) (2021-2030) ($MN)

- Table 9 Global Next-Generation Data Storage Market Outlook, By Solid-state Drive (SSD) (2021-2030) ($MN)

- Table 10 Global Next-Generation Data Storage Market Outlook, By Magnetic Tape (2021-2030) ($MN)

- Table 11 Global Next-Generation Data Storage Market Outlook, By All-Flash Array (2021-2030) ($MN)

- Table 12 Global Next-Generation Data Storage Market Outlook, By Hybrid Flash Array (2021-2030) ($MN)

- Table 13 Global Next-Generation Data Storage Market Outlook, By Other Storage Mediums (2021-2030) ($MN)

- Table 14 Global Next-Generation Data Storage Market Outlook, By Storage Architecture (2021-2030) ($MN)

- Table 15 Global Next-Generation Data Storage Market Outlook, By File- & Object-based Storage (2021-2030) ($MN)

- Table 16 Global Next-Generation Data Storage Market Outlook, By File Storage (2021-2030) ($MN)

- Table 17 Global Next-Generation Data Storage Market Outlook, By Object Storage (2021-2030) ($MN)

- Table 18 Global Next-Generation Data Storage Market Outlook, By Block Storage (2021-2030) ($MN)

- Table 19 Global Next-Generation Data Storage Market Outlook, By Other Storage Architectures (2021-2030) ($MN)

- Table 20 Global Next-Generation Data Storage Market Outlook, By Deployment Type (2021-2030) ($MN)

- Table 21 Global Next-Generation Data Storage Market Outlook, By On-premises (2021-2030) ($MN)

- Table 22 Global Next-Generation Data Storage Market Outlook, By Cloud (2021-2030) ($MN)

- Table 23 Global Next-Generation Data Storage Market Outlook, By Hybrid (2021-2030) ($MN)

- Table 24 Global Next-Generation Data Storage Market Outlook, By Other Deployment Types (2021-2030) ($MN)

- Table 25 Global Next-Generation Data Storage Market Outlook, By End User (2021-2030) ($MN)

- Table 26 Global Next-Generation Data Storage Market Outlook, By BFSI(Banking, Financial Services and Insurance) (2021-2030) ($MN)

- Table 27 Global Next-Generation Data Storage Market Outlook, By Manufacturing (2021-2030) ($MN)

- Table 28 Global Next-Generation Data Storage Market Outlook, By Consumer Goods and Retail (2021-2030) ($MN)

- Table 29 Global Next-Generation Data Storage Market Outlook, By Healthcare and Life Sciences (2021-2030) ($MN)

- Table 30 Global Next-Generation Data Storage Market Outlook, By Media and Entertainment (2021-2030) ($MN)

- Table 31 Global Next-Generation Data Storage Market Outlook, By Government Bodies (2021-2030) ($MN)

- Table 32 Global Next-Generation Data Storage Market Outlook, By Cloud Service Providers (2021-2030) ($MN)

- Table 33 Global Next-Generation Data Storage Market Outlook, By Telecom Companies (2021-2030) ($MN)

- Table 34 Global Next-Generation Data Storage Market Outlook, By Other End Users (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Next-Generation Data Storage Market is accounted for $104.50 billion in 2023 and is expected to reach $269.62 billion by 2030 growing at a CAGR of 14.5% during the forecast period. Next-generation data storage refers to a group of cutting-edge storage techniques and products developed to meet the changing requirements of organizations managing large amounts of data and a variety of workloads. Comparing with the conventional storage systems, next-generation data storage facilitates real-time data processing, seamless data integration, and quicker data access by providing higher performance, improved scalability, and increased energy efficiency.

According to a technology roadmap put forward by the Advanced Storage Technology Consortium, the capacity of HDDs will rise to 100TB by 2025, enabled by new writing technologies such as Shingled Magnetic Recording, Perpendicular Magnetic Recording, Enhanced Caching, and even installing helium inside the casing.

Market Dynamics:

Driver:

Growing use of cloud computing

Data storage, access, and management have undergone radical changes as a result of the widespread adoption of cloud computing services across industries. Scalable, dependable, and high-performance storage solutions are necessary for cloud-based applications and services. To meet the changing demands of cloud-based environments, next-generation data storage technologies are required, such as distributed storage systems, software-defined storage (SDS), and object storage. Moreover, these solutions make it easy to move, replicate, and move data between different cloud platforms.

Restraint:

Compatibility and data migration issues

Data migration and compatibility problems may arise when switching from legacy data storage systems to next-generation solutions. Data format inconsistencies, risks of data loss, or disruptions during migration may be encountered by organizations that have invested in traditional storage infrastructures. Moreover, organizations frequently face compatibility challenges when integrating new storage solutions with existing infrastructures because of the quick evolution of storage technologies. When moving from legacy systems to advanced storage platforms, data migration challenges appear, which may result in discrepancies in data formats, risks of data loss, or disruptions during the migration process.

Opportunity:

Modernization of storage technologies

The market for data storage is experiencing continued growth thanks to innovations in storage technologies like Non-Volatile Memory Express (NVMe), storage-class memory, and shingled magnetic recording (SMR). Furthermore, Businesses that can use these technological advancements to deliver storage solutions that are quicker, more dependable, and more energy-efficient can gain an advantage. A market opportunity exists for utilizing these developments to create high-performance storage arrays and cutting-edge storage systems.

Threat:

Sustainability and environmental issues

Environmental and sustainability issues present a serious threat to the Market. Data centers and storage infrastructures use a lot of energy, which increases carbon emissions and has a negative impact on the environment as data storage needs keep growing. Moreover, Data storage facilities are increasing their energy needs as a result of the rapid growth of cloud computing and data-intensive applications. The disposal of outdated or end-of-life storage hardware can also add to the buildup of electronic waste (e-waste), aggravating already difficult environmental problems.

COVID-19 Impact:

The market for Next-Generation Data Storage was significantly impacted by the COVID-19 pandemic. Scalable, effective, and secure data storage solutions are in greater demand due to the rise in remote work, online learning, and digitalization. The use of cloud-based storage and data management services increased quickly as organizations tried to manage the growing volume of data. Contrarily, supply chain disruptions and economic turbulence caused a temporary slowdown in hardware sales and infrastructure investments. However, as organizations concentrated on boosting their resilience and adaptability in the face of upcoming challenges, the pandemic also accelerated innovations in data storage technologies, driving the market toward advancements like edge computing and hybrid cloud solutions.

The on-premises segment is expected to be the largest during the forecast period

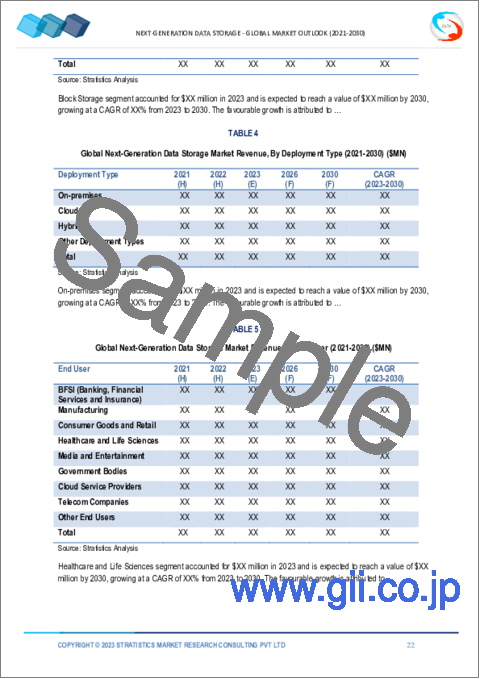

During the forecast period, the on-premises segment is anticipated to have the largest share. Businesses that have complete control over their data and storage infrastructure can put customized security measures in place, guaranteeing data sovereignty and conformity with industry-specific regulations in this segment. Moreover, data breaches and unauthorized access are reduced by the enhanced security and privacy features. Due to the fact that data is stored locally, on-premises storage also provides low latency and quick data access, speeding up the retrieval of crucial information. These benefits make on-premises data storage a desirable option, particularly for sectors dealing with sensitive data and demanding data privacy regulations.

The file- & object-based storage segment is expected to have the highest CAGR during the forecast period

The file- & object-based storage segment is anticipated to witness the fastest CAGR growth during the forecast period. In the market, there has been a notable increase in the file and object-based storage segments. The adoption of big data analytics, the Internet of Things (IoT), and cloud computing, all of which call for scalable and adaptable storage solutions, can be credited with this growth. Its simplicity and usability make file-based storage, like network-attached storage (NAS), ideal for small to medium-sized businesses. File-based storage is still widely used. Moreover, file and object-based storage is well-positioned to continue growing and meeting the varied storage needs of contemporary enterprises as companies create and manage ever-growing datasets.

Region with largest share:

During the forecast period, North America is anticipated to hold the largest market share for next-generation data storage. Advanced data-storage technologies were first adopted in North America. Both consumers and multinational corporations are heavily concentrated in the United States. Moreover, hyperscale data centers have also proliferated quickly, and they are primarily used by cloud computing providers and social network service providers in this region. Over the anticipated period, the easy accessibility of technologically advanced products like 3D printing and molecular storage is likely to further fuel the growth prospects of the North American market.

Region with highest CAGR:

The Next-Generation Data Storage market in Asia Pacific is anticipated to experience the highest CAGR during the forecast period. The region's rising demand for next-generation data storage systems is significantly influenced by rapid urbanization and increased R&D spending by providers of next-generation data storage solutions. China and Japan are both experiencing rapid economic growth. Businesses in these nations have embraced cutting-edge technology to thrive in fierce competition. Moreover, companies in this region are investing in enhancing their IT capabilities in order to stay competitive and improve operational efficiency, operational outcomes, and financial profitability.

Key players in the market:

Some of the key players in Next-Generation Data Storage market include: Adesto Technologies Corporation., Avalanche Technology, Cypress Semiconductor Corporation., Data Direct Networks, Dell Technologies Inc., Everspin Technologies Inc., Fujitsu Ltd., Hewlett Packard Enterprise Company, Hitachi, Ltd., Huawei Technologies Co., Ltd., IBM Corporation, International Business Machines Corporation, Micron Technology Inc., NXP Semiconductors, Pure Storage, Inc, Samsung, Sk Hynix Inc., Spin Memory Inc., Texas Instruments Incorporated, Toshiba Corporation and Western Digital Corporation.

Key Developments:

In July 2022, Samsung Electronics Co. unveiled a second-generation smart solid-state drive (SSD), an upgraded data storage device that significantly reduces the computer processing time and energy consumption.

In May 2022, Terra Master introduced a new eight-bay Direct-Attached Storage (DAS) device for customers who require centralized data storage. Unlike NAS, DAS is used locally via cables that connect directly to a PC or other device. The new TerraMaster D8-332 is a professional RAID storage device with up to 160TB of capacity.

In September 2020, Pure Storage acquired Portworx, a provider of cloud-native storage and data-management platform based on Kubernetes, for $370 million.

Storage Systems Covered:

- Direct-attached Storage (DAS)

- Network-attached Storage (NAS)

- Storage Area Network (SAN)

- Other Storage Systems

Storage Mediums Covered:

- Hard Disk Drive (HDD)

- Solid-state Drive (SSD)

- Magnetic Tape

- All-Flash Array

- Hybrid Flash Array

- Other Storage Mediums

Storage Architectures Covered:

- File- & Object-based Storage

- File Storage

- Object Storage

- Block Storage

- Other Storage Architectures

Deployment Types Covered:

- On-premises

- Cloud

- Hybrid

- Other Deployment Types

End Users Covered:

- BFSI (Banking, Financial Services and Insurance)

- Manufacturing

- Consumer Goods and Retail

- Healthcare and Life Sciences

- Media and Entertainment

- Government Bodies

- Cloud Service Providers

- Telecom Companies

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 End User Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Next-Generation Data Storage Market, By Storage System

- 5.1 Introduction

- 5.2 Direct-attached Storage (DAS)

- 5.3 Network-attached Storage (NAS)

- 5.4 Storage Area Network (SAN)

- 5.5 Other Storage Systems

6 Global Next-Generation Data Storage Market, By Storage Medium

- 6.1 Introduction

- 6.2 Hard Disk Drive (HDD)

- 6.3 Solid-state Drive (SSD)

- 6.4 Magnetic Tape

- 6.5 All-Flash Array

- 6.6 Hybrid Flash Array

- 6.7 Other Storage Mediums

7 Global Next-Generation Data Storage Market, By Storage Architecture

- 7.1 Introduction

- 7.2 File- & Object-based Storage

- 7.3 File Storage

- 7.4 Object Storage

- 7.5 Block Storage

- 7.6 Other Storage Architectures

8 Global Next-Generation Data Storage Market, By Deployment Type

- 8.1 Introduction

- 8.2 On-premises

- 8.3 Cloud

- 8.4 Hybrid

- 8.5 Other Deployment Types

9 Global Next-Generation Data Storage Market, By End User

- 9.1 Introduction

- 9.2 BFSI(Banking, Financial Services and Insurance)

- 9.3 Manufacturing

- 9.4 Consumer Goods and Retail

- 9.5 Healthcare and Life Sciences

- 9.6 Media and Entertainment

- 9.7 Government Bodies

- 9.8 Cloud Service Providers

- 9.9 Telecom Companies

- 9.10 Other End Users

10 Global Next-Generation Data Storage Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.6 South America

- 10.6.1 Argentina

- 10.6.2 Brazil

- 10.6.3 Chile

- 10.6.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 Adesto Technologies Corporation.

- 12.2 Avalanche Technology

- 12.3 Cypress Semiconductor Corporation.

- 12.4 DataDirect Networks

- 12.5 Dell Technologies Inc.

- 12.6 Everspin Technologies Inc.

- 12.7 Fujitsu Ltd.

- 12.8 Hewlett Packard Enterprise Company

- 12.9 Hitachi, Ltd.

- 12.10 Huawei Technologies Co., Ltd.

- 12.11 IBM Corporation

- 12.12 International Business Machines Corporation

- 12.13 MicronTechnology Inc.

- 12.14 NXP Semiconductors.

- 12.15 Pure Storage, Inc.

- 12.16 Samsung

- 12.17 SK HYNIX INC.

- 12.18 Spin Memory Inc.

- 12.19 Texas Instruments Incorporated.

- 12.20 Toshiba CORPORATION

- 12.21 Western Digital Corporation