|

|

市場調査レポート

商品コード

1235877

ポリウレタン分散液の世界市場:2028年までの予測- タイプ別(低溶剤、溶剤ベース、水性、その他のタイプ)、用途別(皮革仕上げ、塗料・コーティング、その他の用途)、地域別Polyurethane Dispersions Market Forecasts to 2028 - Global Analysis By Type (Low-Solvent, Solvent Based, Water Based and Other Types), Application (Leather Finishing, Paints & Coatings and Other Applications) and Geography |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ポリウレタン分散液の世界市場:2028年までの予測- タイプ別(低溶剤、溶剤ベース、水性、その他のタイプ)、用途別(皮革仕上げ、塗料・コーティング、その他の用途)、地域別 |

|

出版日: 2023年03月03日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界のポリウレタン分散液市場は、2022年に22億6000万米ドルを占め、2028年には38億1000万米ドルに達すると予測され、予測期間中に9.1%のCAGRで成長すると予想されています。

PUD(ポリウレタン分散液)は、ポリウレタンポリマー樹脂を溶剤ではなく水に分散させたものです。自動車産業、塗料・コーティング、繊維、皮革コーティングなど多くの産業からの需要増により、市場は拡大しています。皮革は靴やバッグなどの材料として使用されるため、皮革製品の需要は消費財が中心となっており、ポリウレタン分散液の需要もあると考えられています。水性ポリウレタン分散液は、揮発性有機成分が少ないため、自動車用塗料に多く利用されています。

国際貿易センター(ITC)によると、2017-2018年の中国における履物(ゴム、プラスチック、革組成のアウターショールを持つ)の数量における輸出の伸びは73%でした。

市場力学

促進要因

繊維・皮革産業からの需要拡大

ポリウレタン分散液の優れた引張強度、極端な温度耐久性、高弾性、大きな耐摩耗性は、革や繊維の仕上げによく使われています。そのため、財布、靴、シートカバー、衣料品などの生産における革の使用量の増加により、ポリウレタン分散液のニーズが高まると予測されます。したがって、革製品の需要の増加は、ポリウレタン分散液の需要を増加させると予測されます。

抑制要因

酸エポキシコーティングの需要増加

PUDはコーティングの分野に大きな影響を与えます。しかし、コーティング業界は、ポリウレタンコーティングの揮発性有機化合物(VOC)濃度を非常に懸念しています。ゼロVOC」を目指し、より新しい技術を生み出すためには、原料供給者は研究開発に大きな投資をしなければなりません。その結果、人の健康や環境への悪影響が軽減されるでしょう。ポリウレタン塗料の触媒としてスズを使用しないためには、欧州連合(EU)が規制を設ける必要があります。これらの問題に対処するために、酸エポキシ系接着剤の使用が増加しています。このエポキシ系塗料は、溶剤を含まないフェノール樹脂ベースのコーティング液で、耐久性があり滑らかな表面仕上げが必要な鉄骨構造、床、壁などを対象としています。

機会

厳しい政府規制

世界各国の政府機関による厳しい環境基準の導入と設計は、ポリウレタン分散液に大きな市場機会をもたらしています。これらのディスパージョンは、NEP、NMP、DMSOなどの多数の溶剤を使用して製造されており、VOC排出量を増加させます。蒸留プロセスでは、これらの溶剤を容易に取り除くことはできません。これらの溶剤の毒性により、ポリウレタン分散液の市場は非常に大きな成長の可能性を秘めています。

脅威

原油価格の変動

ポリウレタン分散液の製造に使用されるイソシアネートのうち、MDIとTDIの価格は、原油価格の変動に影響されます。さらに、原油価格の変動はメーカーの原料供給能力にも影響を及ぼし、市場の損失を補うためにイソシアネート製品の価格を上げざるを得ません。これらは、ポリウレタン分散液の需要を阻害し、市場拡大を妨げる主な要因となっています。

COVID-19の影響

最近のCOVID-19パンデミックの流行は、ポリウレタン分散液市場を含む世界数カ国の経済だけでなく、産業にも影響を及ぼしています。政府が個人が一箇所に集まることを禁止していることが、産業の発展に大きな悪影響を及ぼしています。建設業界、航空宇宙、自動車、輸出入ビジネスと同様に、ポリウレタン分散液市場もこの流行期に収益の伸びを世界的に減少させた。

予測期間中、水性セグメントが最大になると予想される

水性セグメントは有利な成長を遂げると推定されます。数多くの商業・工業用途で水性ポリウレタン分散液が使用されています。水性ポリウレタン分散液の市場は、最小限のVOC排出を保証する法律の高まりによって増加すると予想されます。VOC排出量は、水性塗料によって削減されます。溶剤系PUDは厳しい環境基準を守る必要があるため、水性PUDの需要は高いです。

予測期間中、塗料・コーティング分野のCAGRが最も高くなると予想されます。

塗料・コーティング分野では、優れた耐久性、高い耐摩耗性、揮発性有機化合物の排出量の少なさ、有害なモノマーを含まないことから、塗料にポリウレタン分散液が使用され、予測期間中に最も速いCAGRの成長が予測されています。したがって、自動車生産台数の増加により塗料需要が増加し、ポリウレタン分散液の消費量が増加すると予測されます。

最もシェアの高い地域

アジア太平洋地域は、建設、自動車、接着剤・シーラント、皮革・繊維、塗料・コーティングなど、さまざまな産業からの需要が増加しており、予測期間中に最大の市場シェアを占めると予測されます。合成皮革や靴の製造には、ポリウレタン分散液が原料として使用されています。そのため、フットウェア分野の成長により、市場が拡大すると予測されています。さらに、消費者の快適性への欲求の高まりやファッショナブルなライフスタイルがフットウェアの需要を後押ししており、これがポリウレタン分散液の市場を牽引すると予想されます。

CAGRが最も高い地域

予測期間中、欧州のCAGRが最も高いと予測されます。欧州連合は、塗料やコーティング剤に含まれるVOCの最大許容量を引き下げました(EU)。これにより、近い将来、塗料メーカーのコストが上昇し、溶剤をベースとしたポリマーディスパージョンの使用が減少すると予想されます。BASFはスペインのカステルビスバル工場で、水性ポリウレタン分散液の生産能力を増強するため、一桁万ユーロ以下の投資を行うと発表しました。

主な発展

Covestroは2021年2月、アジア太平洋地域における環境対応型塗料・接着剤の需要増に対応するため、中国にポリウレタン分散液の新生産施設を計画しました。同社は、この工場の完成を2024年に予定しています。

2019年11月、Perstorpは、EO chainが長いymer n90と、鎖が短いn180という2つの新しいグレードを製品群に加えました。最新の製品は、新しい用途の機会を提供し、人の健康や環境にとってより良いものです。本製品は、皮革の表面感を向上させるために使用することができます。

私たちのレポートが提供するもの

- 地域別・国別セグメントの市場シェア評価

- 新規参入企業への戦略的提言

- 2020年、2021年、2022年、2025年、2028年の市場データを網羅

- 市場促進要因(市場動向、制約要因、機会、脅威、課題、投資機会、推奨事項など)

- 市場推定に基づく主要なビジネスセグメントにおける戦略的な提言

- 競合情勢とその動向

- 詳細な戦略、財務、最近の動向を含む企業プロファイル

- サプライチェーンの動向は、最新の技術進歩をマッピングしています。

無料カスタマイズの提供

本レポートをご購入いただいたお客様には、以下の無料カスタマイズオプションのいずれかをご提供いたします。

- 企業プロファイルの作成

- 追加市場企業の包括的なプロファイリング(最大3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域別セグメント

- お客様のご希望に応じて、主要国の市場推計・予測・CAGRを提供(注:フィージビリティチェック別)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 仮定

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のポリウレタン分散剤市場:タイプ別

- 低溶剤

- 溶剤系

- 水性

- その他のタイプ

第6章 世界のポリウレタン分散剤市場:用途別

- 革の仕上げ

- 塗料とコーティング

- 繊維仕上げ

- 接着剤・シーラント

- グラスファイバーサイジング

- 工事

- 紙とインク

- 自動車補修

- その他のアプリケーション

第7章 世界のポリウレタン分散剤市場:地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東

第8章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第9章 企業プロファイル

- Covestro AG

- Dow Chemical Company

- Lanxess AG

- Lubrizol Corporation

- BASF SE

- Alberdingk Boley GmbH

- Perstorp AB

- Huntsman Corporation

- Mitsui Chemical Inc.

- Rudolf GMBH

- Cytec Solvay Group

- Chase Corporation

- Lamberti SPA

- 3M

- Michelman, Inc.

- Hauthaway Corporation

- Allnex

- Chemtura Corporation

List of Tables

- Table 1 Global Polyurethane Dispersions Market Outlook, By Region (2020-2028) ($MN)

- Table 2 Global Polyurethane Dispersions Market Outlook, By Type (2020-2028) ($MN)

- Table 3 Global Polyurethane Dispersions Market Outlook, By Low-Solvent (2020-2028) ($MN)

- Table 4 Global Polyurethane Dispersions Market Outlook, By Solvent Based (2020-2028) ($MN)

- Table 5 Global Polyurethane Dispersions Market Outlook, By Water Based (2020-2028) ($MN)

- Table 6 Global Polyurethane Dispersions Market Outlook, By Other Types (2020-2028) ($MN)

- Table 7 Global Polyurethane Dispersions Market Outlook, By Application (2020-2028) ($MN)

- Table 8 Global Polyurethane Dispersions Market Outlook, By Leather Finishing (2020-2028) ($MN)

- Table 9 Global Polyurethane Dispersions Market Outlook, By Paints & Coatings (2020-2028) ($MN)

- Table 10 Global Polyurethane Dispersions Market Outlook, By Textile Finishing (2020-2028) ($MN)

- Table 11 Global Polyurethane Dispersions Market Outlook, By Adhesives & Sealants (2020-2028) ($MN)

- Table 12 Global Polyurethane Dispersions Market Outlook, By Fiber Glass Sizing (2020-2028) ($MN)

- Table 13 Global Polyurethane Dispersions Market Outlook, By Construction (2020-2028) ($MN)

- Table 14 Global Polyurethane Dispersions Market Outlook, By Paper and Ink (2020-2028) ($MN)

- Table 15 Global Polyurethane Dispersions Market Outlook, By Automotive Refinishing (2020-2028) ($MN)

- Table 16 Global Polyurethane Dispersions Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 17 North America Polyurethane Dispersions Market Outlook, By Country (2020-2028) ($MN)

- Table 18 North America Polyurethane Dispersions Market Outlook, By Type (2020-2028) ($MN)

- Table 19 North America Polyurethane Dispersions Market Outlook, By Low-Solvent (2020-2028) ($MN)

- Table 20 North America Polyurethane Dispersions Market Outlook, By Solvent Based (2020-2028) ($MN)

- Table 21 North America Polyurethane Dispersions Market Outlook, By Water Based (2020-2028) ($MN)

- Table 22 North America Polyurethane Dispersions Market Outlook, By Other Types (2020-2028) ($MN)

- Table 23 North America Polyurethane Dispersions Market Outlook, By Application (2020-2028) ($MN)

- Table 24 North America Polyurethane Dispersions Market Outlook, By Leather Finishing (2020-2028) ($MN)

- Table 25 North America Polyurethane Dispersions Market Outlook, By Paints & Coatings (2020-2028) ($MN)

- Table 26 North America Polyurethane Dispersions Market Outlook, By Textile Finishing (2020-2028) ($MN)

- Table 27 North America Polyurethane Dispersions Market Outlook, By Adhesives & Sealants (2020-2028) ($MN)

- Table 28 North America Polyurethane Dispersions Market Outlook, By Fiber Glass Sizing (2020-2028) ($MN)

- Table 29 North America Polyurethane Dispersions Market Outlook, By Construction (2020-2028) ($MN)

- Table 30 North America Polyurethane Dispersions Market Outlook, By Paper and Ink (2020-2028) ($MN)

- Table 31 North America Polyurethane Dispersions Market Outlook, By Automotive Refinishing (2020-2028) ($MN)

- Table 32 North America Polyurethane Dispersions Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 33 Europe Polyurethane Dispersions Market Outlook, By Country (2020-2028) ($MN)

- Table 34 Europe Polyurethane Dispersions Market Outlook, By Type (2020-2028) ($MN)

- Table 35 Europe Polyurethane Dispersions Market Outlook, By Low-Solvent (2020-2028) ($MN)

- Table 36 Europe Polyurethane Dispersions Market Outlook, By Solvent Based (2020-2028) ($MN)

- Table 37 Europe Polyurethane Dispersions Market Outlook, By Water Based (2020-2028) ($MN)

- Table 38 Europe Polyurethane Dispersions Market Outlook, By Other Types (2020-2028) ($MN)

- Table 39 Europe Polyurethane Dispersions Market Outlook, By Application (2020-2028) ($MN)

- Table 40 Europe Polyurethane Dispersions Market Outlook, By Leather Finishing (2020-2028) ($MN)

- Table 41 Europe Polyurethane Dispersions Market Outlook, By Paints & Coatings (2020-2028) ($MN)

- Table 42 Europe Polyurethane Dispersions Market Outlook, By Textile Finishing (2020-2028) ($MN)

- Table 43 Europe Polyurethane Dispersions Market Outlook, By Adhesives & Sealants (2020-2028) ($MN)

- Table 44 Europe Polyurethane Dispersions Market Outlook, By Fiber Glass Sizing (2020-2028) ($MN)

- Table 45 Europe Polyurethane Dispersions Market Outlook, By Construction (2020-2028) ($MN)

- Table 46 Europe Polyurethane Dispersions Market Outlook, By Paper and Ink (2020-2028) ($MN)

- Table 47 Europe Polyurethane Dispersions Market Outlook, By Automotive Refinishing (2020-2028) ($MN)

- Table 48 Europe Polyurethane Dispersions Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 49 Asia Pacific Polyurethane Dispersions Market Outlook, By Country (2020-2028) ($MN)

- Table 50 Asia Pacific Polyurethane Dispersions Market Outlook, By Type (2020-2028) ($MN)

- Table 51 Asia Pacific Polyurethane Dispersions Market Outlook, By Low-Solvent (2020-2028) ($MN)

- Table 52 Asia Pacific Polyurethane Dispersions Market Outlook, By Solvent Based (2020-2028) ($MN)

- Table 53 Asia Pacific Polyurethane Dispersions Market Outlook, By Water Based (2020-2028) ($MN)

- Table 54 Asia Pacific Polyurethane Dispersions Market Outlook, By Other Types (2020-2028) ($MN)

- Table 55 Asia Pacific Polyurethane Dispersions Market Outlook, By Application (2020-2028) ($MN)

- Table 56 Asia Pacific Polyurethane Dispersions Market Outlook, By Leather Finishing (2020-2028) ($MN)

- Table 57 Asia Pacific Polyurethane Dispersions Market Outlook, By Paints & Coatings (2020-2028) ($MN)

- Table 58 Asia Pacific Polyurethane Dispersions Market Outlook, By Textile Finishing (2020-2028) ($MN)

- Table 59 Asia Pacific Polyurethane Dispersions Market Outlook, By Adhesives & Sealants (2020-2028) ($MN)

- Table 60 Asia Pacific Polyurethane Dispersions Market Outlook, By Fiber Glass Sizing (2020-2028) ($MN)

- Table 61 Asia Pacific Polyurethane Dispersions Market Outlook, By Construction (2020-2028) ($MN)

- Table 62 Asia Pacific Polyurethane Dispersions Market Outlook, By Paper and Ink (2020-2028) ($MN)

- Table 63 Asia Pacific Polyurethane Dispersions Market Outlook, By Automotive Refinishing (2020-2028) ($MN)

- Table 64 Asia Pacific Polyurethane Dispersions Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 65 South America Polyurethane Dispersions Market Outlook, By Country (2020-2028) ($MN)

- Table 66 South America Polyurethane Dispersions Market Outlook, By Type (2020-2028) ($MN)

- Table 67 South America Polyurethane Dispersions Market Outlook, By Low-Solvent (2020-2028) ($MN)

- Table 68 South America Polyurethane Dispersions Market Outlook, By Solvent Based (2020-2028) ($MN)

- Table 69 South America Polyurethane Dispersions Market Outlook, By Water Based (2020-2028) ($MN)

- Table 70 South America Polyurethane Dispersions Market Outlook, By Other Types (2020-2028) ($MN)

- Table 71 South America Polyurethane Dispersions Market Outlook, By Application (2020-2028) ($MN)

- Table 72 South America Polyurethane Dispersions Market Outlook, By Leather Finishing (2020-2028) ($MN)

- Table 73 South America Polyurethane Dispersions Market Outlook, By Paints & Coatings (2020-2028) ($MN)

- Table 74 South America Polyurethane Dispersions Market Outlook, By Textile Finishing (2020-2028) ($MN)

- Table 75 South America Polyurethane Dispersions Market Outlook, By Adhesives & Sealants (2020-2028) ($MN)

- Table 76 South America Polyurethane Dispersions Market Outlook, By Fiber Glass Sizing (2020-2028) ($MN)

- Table 77 South America Polyurethane Dispersions Market Outlook, By Construction (2020-2028) ($MN)

- Table 78 South America Polyurethane Dispersions Market Outlook, By Paper and Ink (2020-2028) ($MN)

- Table 79 South America Polyurethane Dispersions Market Outlook, By Automotive Refinishing (2020-2028) ($MN)

- Table 80 South America Polyurethane Dispersions Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 81 Middle East & Africa Polyurethane Dispersions Market Outlook, By Country (2020-2028) ($MN)

- Table 82 Middle East & Africa Polyurethane Dispersions Market Outlook, By Type (2020-2028) ($MN)

- Table 83 Middle East & Africa Polyurethane Dispersions Market Outlook, By Low-Solvent (2020-2028) ($MN)

- Table 84 Middle East & Africa Polyurethane Dispersions Market Outlook, By Solvent Based (2020-2028) ($MN)

- Table 85 Middle East & Africa Polyurethane Dispersions Market Outlook, By Water Based (2020-2028) ($MN)

- Table 86 Middle East & Africa Polyurethane Dispersions Market Outlook, By Other Types (2020-2028) ($MN)

- Table 87 Middle East & Africa Polyurethane Dispersions Market Outlook, By Application (2020-2028) ($MN)

- Table 88 Middle East & Africa Polyurethane Dispersions Market Outlook, By Leather Finishing (2020-2028) ($MN)

- Table 89 Middle East & Africa Polyurethane Dispersions Market Outlook, By Paints & Coatings (2020-2028) ($MN)

- Table 90 Middle East & Africa Polyurethane Dispersions Market Outlook, By Textile Finishing (2020-2028) ($MN)

- Table 91 Middle East & Africa Polyurethane Dispersions Market Outlook, By Adhesives & Sealants (2020-2028) ($MN)

- Table 92 Middle East & Africa Polyurethane Dispersions Market Outlook, By Fiber Glass Sizing (2020-2028) ($MN)

- Table 93 Middle East & Africa Polyurethane Dispersions Market Outlook, By Construction (2020-2028) ($MN)

- Table 94 Middle East & Africa Polyurethane Dispersions Market Outlook, By Paper and Ink (2020-2028) ($MN)

- Table 95 Middle East & Africa Polyurethane Dispersions Market Outlook, By Automotive Refinishing (2020-2028) ($MN)

- Table 96 Middle East & Africa Polyurethane Dispersions Market Outlook, By Other Applications (2020-2028) ($MN)

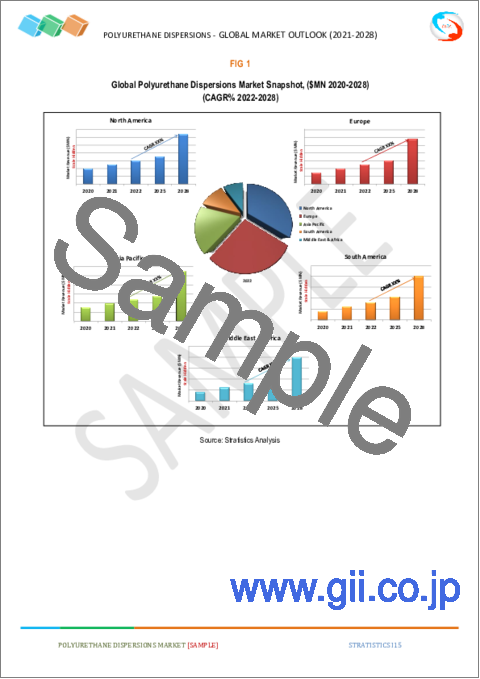

According to Stratistics MRC, the Global Polyurethane Dispersions Market is accounted for $2.26 billion in 2022 and is expected to reach $3.81 billion by 2028 growing at a CAGR of 9.1% during the forecast period. PUD, or polyurethane dispersion, is a polyurethane polymer resin that has been dispersed in water as opposed to a solvent. The market is expanding because of increased demand from many industries, including the automotive industry, paint & coatings, textile, and leather coatings. Since leather is used to make footwear, handbags, and other items, the demand for leather products is mostly driven by consumer goods, which are also thought to generate demand for polyurethane dispersions. Because water-based polyurethane dispersion has less volatile organic ingredient, it is frequently utilised in car paints.

According to the International Trade Center (ITC), exportation growth in the quantity of footwear (with outer shole of rubber, plastic, and leather composition) was 73% in 2017-2018 in China.

Market Dynamics:

Driver:

Growing demand from textile and leather industry

The outstanding tensile strength, extreme temperature durability, high elasticity, and great abrasion resistance of polyurethane dispersions make them a popular choice for finishing leather and textiles. Therefore, it is predicted that the need for polyurethane dispersions would increase due to the growing use of leather in the production of purses, shoes, seat coverings, garments, and other goods. Thus, it is predicted that rising demand for leather goods will increase demand for polyurethane dispersions.

Restraint:

Increasing demand for acid-epoxy coatings

PUDs have a significant impact on the coatings sector. However, the coating industry is very concerned about the volatile organic compound (VOC) concentration of polyurethane coatings. To address the "zero-VOC" aim and create newer technologies, raw material providers must make large investments in R&D. This will lessen the adverse effects on human health and the environment. To stop using tin as a catalyst for polyurethane coatings, the European Union (EU) must establish regulations. Acid-epoxy adhesives are increasingly being used to address these problems. These epoxy-based coatings are phenolic resin-based coating solutions devoid of solvents and intended for steel structures, floors, and walls that require a durable, smooth surface finish.

Opportunity:

Strict government regulations

The implementation and design of strict environmental standards by governing agencies of many economies across the world presents a significant market opportunity for polyurethane dispersion. These dispersions are produced using numerous solvents, including NEP, NMP, and DMSO, which raises VOC emissions. The distillation process cannot readily get rid of these solvents. Due to the toxicity of these solvents, the market for polyurethane dispersion has tremendous growth potential.

Threat:

Fluctuation in the prices of crude oil

As the two main isocyanates that have been chosen for the production of polyurethane dispersion, MDI and TDI prices are affected by changes in the price of crude oil. Additionally, the fluctuation in crude oil prices has an impact on the manufacturers' ability to supply raw materials, which forces them to increase the price of their isocyanate products in order to make up for market losses. These are the main factors that impede the demand for polyurethane dispersion and limit market expansion.

COVID-19 Impact

The recent COVID-19 pandemic epidemic has had an effect on industry as well as the economy of several nations worldwide, including the polyurethane dispersion market. The government's prohibitions on individuals congregating in one location have had a significant negative influence on the development of the industry. Similar to the construction industry, aerospace, automotive, and import and export businesses, the polyurethane dispersion market also experienced a global reduction in revenue growth during this pandemic period.

The water-based segment is expected to be the largest during the forecast period

The Water-based segment is estimated to have a lucrative growth. Numerous commercial and industrial applications use water-based polyurethane dispersion. The market for water-based polyurethane dispersion is anticipated to increase due to rising laws ensuring minimal VOC emissions. VOC emissions are reduced by water-based paint. Water-based PUDs are in high demand since solvent-based PUDs must adhere to strict environmental standards.

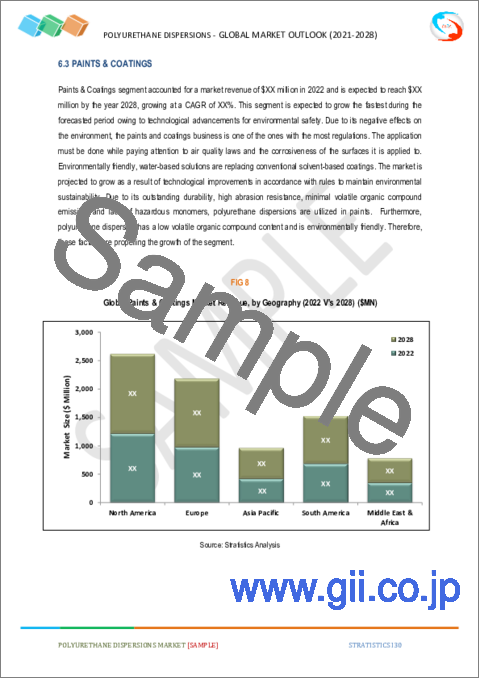

The paints & coatings segment is expected to have the highest CAGR during the forecast period

The paints & coatings segment is anticipated to witness the fastest CAGR growth during the forecast period, due to its outstanding durability, high abrasion resistance, minimal volatile organic compound emission, and lack of hazardous monomers, polyurethane dispersions are utilised in paints. Therefore, it is predicted that rising vehicle production will increase paint demand, which will then increase consumption of polyurethane dispersions.

Region with highest share:

Asia Pacific is projected to hold the largest market share during the forecast period owing to an increase in demand from different industries, including construction, automotive, adhesives & sealants, leather & textiles, and paint & coatings in Asian nations. For the production of synthetic leather and footwear, polyurethane dispersion is employed as a raw material. As a result, it is predicted that the market would grow due to the growing footwear sector. Additionally, consumers' increasing desire for comfort and fashionable lifestyles are boosting demand for footwear, which is anticipated to drive the market for polyurethane dispersions.

Region with highest CAGR:

Europe is projected to have the highest CAGR over the forecast period. The European Union has reduced the maximum permitted level of VOCs in paint and coating formulations (EU). This is anticipated to increase costs for coating manufacturers in the near future and reduce the use of polymer dispersions based on solvents. At its Castellbisbal factory in Spain, BASF announced a low-single-digit million-euro investment to increase the capacity of water-based polyurethane dispersions.

Key players in the market

Some of the key players profiled in the Polyurethane Dispersions Market include: Covestro AG, Dow Chemical Company, Lanxess AG, Lubrizol Corporation, BASF SE, Alberdingk Boley GmbH, Perstorp AB, Huntsman Corporation, Mitsui Chemical Inc., Rudolf GMBH, Cytec Solvay Group, Chase Corporation, Lamberti SPA, 3M, Michelman, Inc., Hauthaway Corporation, Allnex and Chemtura Corporation.

Key Developments:

In February 2021, Covestro planned for a new production facility for polyurethane dispersion in China to address the rising demand for environmentally compatible coatings and adhesives in the Asia-Pacific region. The company has scheduled the completion of this plant for 2024.

In November 2019, Perstorp launched two new grades - ymer n90, with a longer EO chain, and n180, with a shorter chain to its range. The latest products present opportunities for new applications and are better for human health and the environment. The product can be used to improve the surface feeling of leather.

Types Covered:

- Low-Solvent

- Solvent Based

- Water Based

- Other Types

Applications Covered:

- Leather Finishing

- Paints & Coatings

- Textile Finishing

- Adhesives & Sealants

- Fiber Glass Sizing

- Construction

- Paper and Ink

- Automotive Refinishing

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2020, 2021, 2022, 2025, and 2028

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Polyurethane Dispersions Market, By Type

- 5.1 Introduction

- 5.2 Low-Solvent

- 5.3 Solvent Based

- 5.4 Water Based

- 5.5 Other Types

6 Global Polyurethane Dispersions Market, By Application

- 6.1 Introduction

- 6.2 Leather Finishing

- 6.3 Paints & Coatings

- 6.4 Textile Finishing

- 6.5 Adhesives & Sealants

- 6.6 Fiber Glass Sizing

- 6.7 Construction

- 6.8 Paper and Ink

- 6.9 Automotive Refinishing

- 6.10 Other Applications

7 Global Polyurethane Dispersions Market, By Geography

- 7.1 Introduction

- 7.2 North America

- 7.2.1 US

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 Italy

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 New Zealand

- 7.4.6 South Korea

- 7.4.7 Rest of Asia Pacific

- 7.5 South America

- 7.5.1 Argentina

- 7.5.2 Brazil

- 7.5.3 Chile

- 7.5.4 Rest of South America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 Qatar

- 7.6.4 South Africa

- 7.6.5 Rest of Middle East & Africa

8 Key Developments

- 8.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 8.2 Acquisitions & Mergers

- 8.3 New Product Launch

- 8.4 Expansions

- 8.5 Other Key Strategies

9 Company Profiling

- 9.1 Covestro AG

- 9.2 Dow Chemical Company

- 9.3 Lanxess AG

- 9.4 Lubrizol Corporation

- 9.5 BASF SE

- 9.6 Alberdingk Boley GmbH

- 9.7 Perstorp AB

- 9.8 Huntsman Corporation

- 9.9 Mitsui Chemical Inc.

- 9.10 Rudolf GMBH

- 9.11 Cytec Solvay Group

- 9.12 Chase Corporation

- 9.13 Lamberti SPA

- 9.14 3M

- 9.15 Michelman, Inc.

- 9.16 Hauthaway Corporation

- 9.17 Allnex

- 9.18 Chemtura Corporation