|

|

市場調査レポート

商品コード

1218861

ポリシリコンの世界市場:2028年までの予測- グレード別(電子グレード、ソーラーグレード)、形態別(グラニュール、チャンク、ロッド)、製品タイプ別、技術別、アプリケーション別、地域別の分析Polysilicon Market Forecasts to 2028 - Global Analysis By Grade (Electronic Grade and Solar Grade), By Form (Granules, Chunks and Rods), By Product Type, By Technology, By Application and By Geography |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ポリシリコンの世界市場:2028年までの予測- グレード別(電子グレード、ソーラーグレード)、形態別(グラニュール、チャンク、ロッド)、製品タイプ別、技術別、アプリケーション別、地域別の分析 |

|

出版日: 2023年02月02日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

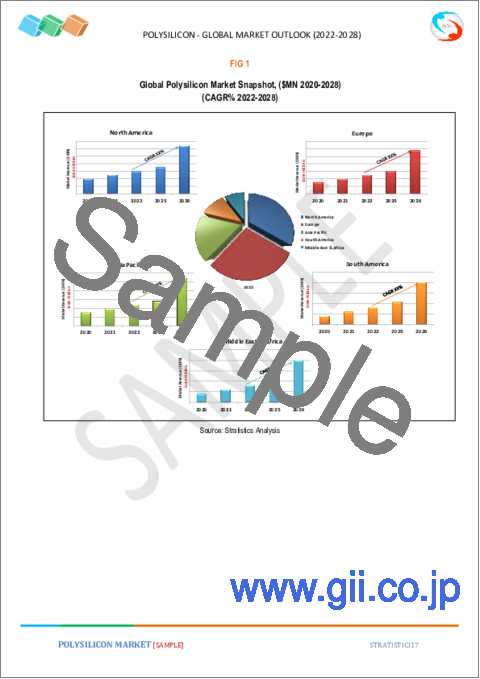

Stratistics MRCによると、世界のポリシリコン市場は2022年に102億2000万米ドルを占め、2028年には238億8000万米ドルに達すると予測され、予測期間中に15.2%のCAGRで成長する見込みです。

冶金グレードのシリコンは、多結晶シリコンとして知られるポリシリコンを開発するために使用されます。多結晶シリコンは、無数の小さな結晶で構成された非常に純度の高いシリコンです。この物質は、太陽電池などの電子機器の製造に欠かせない成分です。

国際再生可能エネルギー機関(IRENA)によると、2021年の世界の太陽光発電の総容量拡大は19%増加し、133GWの追加設置を記録しています。さらに、世界経済フォーラムによると、2021年には初めて太陽光と風力を合わせた発電量が世界全体の10%を超え、太陽光発電はそのうちの約5%のシェアを占めています。

市場力学

促進要因

太陽光発電の需要

太陽光発電産業からのポリシリコン需要の増加が、市場成長率を押し上げる主な要因となっています。新興国におけるさまざまなエンドユーザー分野の開拓と拡大、多結晶ソーラーパネル、電子機器、民生用小型ソーラー機器などの製造を含むさまざまな産業用途におけるポリシリコンの需要増加も、市場の成長率に直接的かつ有利な影響を与えるでしょう。

抑制要因

原材料の不足とコスト高

ロックアップや価格変動による原材料の需給不足は、市場成長の大きな障害となります。研究開発費の高騰、産業活動に対する政府の厳しい規制、輸出入税の上昇、厳しい国際貿易障壁などが、市場の成長率を減速させるでしょう。また、高い資本コストによって、市場の成長力は制限されるでしょう。

機会

政府の取り組み

工業化の進展、再生可能エネルギー源への依存度の増加、特に発展途上国における中小企業の増加、技術の進歩と生産方式の近代化の重視などが、この産業の成長に寄与すると考えられます。また、政府は太陽電池製品のコスト低減に一層力を入れるでしょう。

脅威

資本集約的な製造プロセスの使用

製造設備の開発にはコストがかかり、最新鋭の設備と優秀な人材が必要です。現在、中国が世界の約8割を生産し、市場を独占しています。パンデミックによるサプライチェーンの寸断がもたらしたシリコンチップ不足は、半導体部品に依存する自動車や家電など、半導体エレクトロニクスに関連するすべての産業に影響を及ぼしました。サプライチェーンの脆弱性を目の当たりにして、半導体依存産業における国内生産の意義とその地政学的な意味を認識した国もいくつかあります。

COVID-19の影響

2020年、中国が世界市場を席巻し、COVID-19発生の中心的な役割を果たしました。パンデミック時に課された地域的なロックダウン規制は、サプライチェーンを混乱させ、多くの最終使用産業に悪影響を及ぼしました。さらに、貿易制限、労働力や原材料の不足、貨物用コンテナの不足、物流の困難さなどが、パンデミックによる世界のサプライチェーンの混乱につながりました。さらに、半導体の生産能力は原材料の不足により大きな影響を受け、シリコンチップの全面的な不足を招きました。

予測期間中、太陽光発電分野が最大になると予想される

半導体や太陽光発電パネルの製造に広く使用されていることから、予測期間中は太陽光発電セグメントが市場を独占すると予想されます。しかし、このセグメントの成長を促す主な要因は、太陽光発電システムの設置に対する世界の需要の高まりであり、これが需要を押し上げる要因となっています。

予測期間中、エレクトロニクスグレードのセグメントが最も高いCAGRを記録すると予想される

エレクトロニクス分野の急成長と太陽エネルギー利用の増加により、エレクトロニクス分野は予測期間中に最も高いCAGRを示すと予想されます。従来のエネルギー源の枯渇や環境の持続可能性に対する懸念が高まっていることから、メーカーはさまざまな事業分野において、太陽エネルギーのような他の再生可能エネルギーの選択肢を検討しています。さらに、ソーラーパネルは、電力網や商業ビル・住宅のさまざまな電化製品とともに、代替電力源として使用されています。

最もシェアの高い地域

中国、韓国、インドといった国々で消費量が増加していることから、アジア太平洋地域が予測期間中にポリシリコンの世界市場を独占すると予想されます。中国政府の発表によると、中国におけるポリシリコンの年間生産能力は12万2,000トンに達しています。さらに、2021年6月時点で世界最大の太陽光発電施設の大半は、中国とインドで確認されています。さらに、総出力容量2,245メガワットのBhadla太陽光発電所は、インドのラジャスタン州ジョードプル地区に位置しています。

CAGRが最も高い地域

停電の増加、安定した電力供給の必要性、さまざまな最終用途産業からの需要増加、研究開発活動の活発化など、さまざまな要因から、アジア太平洋地域は予測期間中にポリシリコン市場のCAGRが最も高くなると予想されています。さらに、中国やインドなどの国々における消費と需要の増加、産業成長を支援する政府による投資政策、高い経済成長が、この地域の市場成長を促進しています。

主な発展

2022年8月、REC Silicon ASAとMississippi Siliconは、米国でソーラーサプライチェーンを開発するために協業しました。彼らは、このソーラーサプライチェーンを原料シリコンからポリシリコン、そして最終的に完全組み立てモジュールまで発展させる計画です。

2022年4月、OCI Company Ltdは、韓国の太陽光発電メーカーHanwha Solutions(ハンファの一部門)とポリシリコンの供給に関する抑制要因力のある覚書(MoU)に調印しました。受注金額は約12億米ドル。これにより、同社は利益率を高めることができました。

本レポートの内容

- 地域別・国別セグメントにおける市場セグメンテーション

- 新規参入企業への戦略的提言

- 2020年、2021年、2022年、2025年、2028年の市場データを網羅

- 市場動向(市場促進要因・促進要因・機会・脅威・課題・投資機会・提言)を網羅

- 市場推定に基づく、主要ビジネスセグメントにおける戦略的推奨事項

- 主要な共通トレンドをマッピングした競合情勢

- 詳細な戦略、財務、最近の開発状況を含む企業プロファイル

- 最新の技術的進歩をマッピングしたサプライチェーン動向

無料カスタマイズサービス

本レポートをご購読のお客様には、以下のカスタマイズオプションのいずれかを無償でご提供いたします。

- 企業プロファイル

- 追加市場プレイヤーの包括的なプロファイリング(最大3社まで)

- 主要プレイヤーのSWOT分析(3社まで)

- 地域別セグメンテーション

- お客様のご希望に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによります。)

- 競合ベンチマーキング

製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要プレイヤーのベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 仮定

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- 技術分析

- アプリケーション分析

- 新興市場

- COVID-19の影響

第4章 ポーターズファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のポリシリコン市場:グレード別

- 電子グレード

- ソーラーグレード

第6章 世界のポリシリコン市場:形態別

- 顆粒

- チャンク

- ロッド

第7章 世界のポリシリコン市場:製品タイプ別

- 並列接続

- 直列接続

第8章 世界のポリシリコン市場:技術別

- アップグレードされた冶金グレードのシリコンプロセス

- 流動床反応器(FBR)プロセス

- シーメンスプロセス

第9章 世界のポリシリコン市場:用途別

- 太陽光発電

- 太陽光発電

- 単結晶ソーラーパネル

- 多結晶ソーラーパネル

- 民間のソーラー小型機器

第10章 世界のポリシリコン市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイル

- SunEdison Inc

- Hemlock Semiconductor Operations And Hemlock Semiconductor

- REC Silicon ASA

- Tokuyama Corporation

- Mitsubishi Polycrystalline Silicon America Corporation

- Qatar Solar Technologies

- Wacker Chemie AG

- Osaka Titanium Technologies Co. Ltd

- OCI Solar Power LLC

- Daqo New Energy Corp.

- GCL-Poly Energy Holdings Limited

List of Tables

- 1 Global Polysilicon Market Outlook, By Region (2020-2028) ($MN)

- 2 Global Polysilicon Market Outlook, By Grade (2020-2028) ($MN)

- 3 Global Polysilicon Market Outlook, By Electronic Grade (2020-2028) ($MN)

- 4 Global Polysilicon Market Outlook, By Solar Grade (2020-2028) ($MN)

- 5 Global Polysilicon Market Outlook, By Form (2020-2028) ($MN)

- 6 Global Polysilicon Market Outlook, By Granules (2020-2028) ($MN)

- 7 Global Polysilicon Market Outlook, By Chunks (2020-2028) ($MN)

- 8 Global Polysilicon Market Outlook, By Rods (2020-2028) ($MN)

- 9 Global Polysilicon Market Outlook, By Product Type (2020-2028) ($MN)

- 10 Global Polysilicon Market Outlook, By Parallel Connection (2020-2028) ($MN)

- 11 Global Polysilicon Market Outlook, By Series Connection (2020-2028) ($MN)

- 12 Global Polysilicon Market Outlook, By Technology (2020-2028) ($MN)

- 13 Global Polysilicon Market Outlook, By Upgraded Metallurgical-Grade Silicon Process (2020-2028) ($MN)

- 14 Global Polysilicon Market Outlook, By Fluidized Bed Reactor (FBR) Process (2020-2028) ($MN)

- 15 Global Polysilicon Market Outlook, By Siemens Process (2020-2028) ($MN)

- 16 Global Polysilicon Market Outlook, By Application (2020-2028) ($MN)

- 17 Global Polysilicon Market Outlook, By Photovoltaic (2020-2028) ($MN)

- 18 Global Polysilicon Market Outlook, By Solar Power Generation (2020-2028) ($MN)

- 19 Global Polysilicon Market Outlook, By Monocrystalline Solar Panel (2020-2028) ($MN)

- 20 Global Polysilicon Market Outlook, By Multicrystalline Solar Panel (2020-2028) ($MN)

- 21 Global Polysilicon Market Outlook, By Civilian Solar Small Equipment (2020-2028) ($MN)

- 22 North America Polysilicon Market Outlook, By Country (2020-2028) ($MN)

- 23 North America Polysilicon Market Outlook, By Grade (2020-2028) ($MN)

- 24 North America Polysilicon Market Outlook, By Electronic Grade (2020-2028) ($MN)

- 25 North America Polysilicon Market Outlook, By Solar Grade (2020-2028) ($MN)

- 26 North America Polysilicon Market Outlook, By Form (2020-2028) ($MN)

- 27 North America Polysilicon Market Outlook, By Granules (2020-2028) ($MN)

- 28 North America Polysilicon Market Outlook, By Chunks (2020-2028) ($MN)

- 29 North America Polysilicon Market Outlook, By Rods (2020-2028) ($MN)

- 30 North America Polysilicon Market Outlook, By Product Type (2020-2028) ($MN)

- 31 North America Polysilicon Market Outlook, By Parallel Connection (2020-2028) ($MN)

- 32 North America Polysilicon Market Outlook, By Series Connection (2020-2028) ($MN)

- 33 North America Polysilicon Market Outlook, By Technology (2020-2028) ($MN)

- 34 North America Polysilicon Market Outlook, By Upgraded Metallurgical-Grade Silicon Process (2020-2028) ($MN)

- 35 North America Polysilicon Market Outlook, By Fluidized Bed Reactor (FBR) Process (2020-2028) ($MN)

- 36 North America Polysilicon Market Outlook, By Siemens Process (2020-2028) ($MN)

- 37 North America Polysilicon Market Outlook, By Application (2020-2028) ($MN)

- 38 North America Polysilicon Market Outlook, By Photovoltaic (2020-2028) ($MN)

- 39 North America Polysilicon Market Outlook, By Solar Power Generation (2020-2028) ($MN)

- 40 North America Polysilicon Market Outlook, By Monocrystalline Solar Panel (2020-2028) ($MN)

- 41 North America Polysilicon Market Outlook, By Multicrystalline Solar Panel (2020-2028) ($MN)

- 42 North America Polysilicon Market Outlook, By Civilian Solar Small Equipment (2020-2028) ($MN)

- 43 Europe Polysilicon Market Outlook, By Country (2020-2028) ($MN)

- 44 Europe Polysilicon Market Outlook, By Grade (2020-2028) ($MN)

- 45 Europe Polysilicon Market Outlook, By Electronic Grade (2020-2028) ($MN)

- 46 Europe Polysilicon Market Outlook, By Solar Grade (2020-2028) ($MN)

- 47 Europe Polysilicon Market Outlook, By Form (2020-2028) ($MN)

- 48 Europe Polysilicon Market Outlook, By Granules (2020-2028) ($MN)

- 49 Europe Polysilicon Market Outlook, By Chunks (2020-2028) ($MN)

- 50 Europe Polysilicon Market Outlook, By Rods (2020-2028) ($MN)

- 51 Europe Polysilicon Market Outlook, By Product Type (2020-2028) ($MN)

- 52 Europe Polysilicon Market Outlook, By Parallel Connection (2020-2028) ($MN)

- 53 Europe Polysilicon Market Outlook, By Series Connection (2020-2028) ($MN)

- 54 Europe Polysilicon Market Outlook, By Technology (2020-2028) ($MN)

- 55 Europe Polysilicon Market Outlook, By Upgraded Metallurgical-Grade Silicon Process (2020-2028) ($MN)

- 56 Europe Polysilicon Market Outlook, By Fluidized Bed Reactor (FBR) Process (2020-2028) ($MN)

- 57 Europe Polysilicon Market Outlook, By Siemens Process (2020-2028) ($MN)

- 58 Europe Polysilicon Market Outlook, By Application (2020-2028) ($MN)

- 59 Europe Polysilicon Market Outlook, By Photovoltaic (2020-2028) ($MN)

- 60 Europe Polysilicon Market Outlook, By Solar Power Generation (2020-2028) ($MN)

- 61 Europe Polysilicon Market Outlook, By Monocrystalline Solar Panel (2020-2028) ($MN)

- 62 Europe Polysilicon Market Outlook, By Multicrystalline Solar Panel (2020-2028) ($MN)

- 63 Europe Polysilicon Market Outlook, By Civilian Solar Small Equipment (2020-2028) ($MN)

- 64 Asia Pacific Polysilicon Market Outlook, By Country (2020-2028) ($MN)

- 65 Asia Pacific Polysilicon Market Outlook, By Grade (2020-2028) ($MN)

- 66 Asia Pacific Polysilicon Market Outlook, By Electronic Grade (2020-2028) ($MN)

- 67 Asia Pacific Polysilicon Market Outlook, By Solar Grade (2020-2028) ($MN)

- 68 Asia Pacific Polysilicon Market Outlook, By Form (2020-2028) ($MN)

- 69 Asia Pacific Polysilicon Market Outlook, By Granules (2020-2028) ($MN)

- 70 Asia Pacific Polysilicon Market Outlook, By Chunks (2020-2028) ($MN)

- 71 Asia Pacific Polysilicon Market Outlook, By Rods (2020-2028) ($MN)

- 72 Asia Pacific Polysilicon Market Outlook, By Product Type (2020-2028) ($MN)

- 73 Asia Pacific Polysilicon Market Outlook, By Parallel Connection (2020-2028) ($MN)

- 74 Asia Pacific Polysilicon Market Outlook, By Series Connection (2020-2028) ($MN)

- 75 Asia Pacific Polysilicon Market Outlook, By Technology (2020-2028) ($MN)

- 76 Asia Pacific Polysilicon Market Outlook, By Upgraded Metallurgical-Grade Silicon Process (2020-2028) ($MN)

- 77 Asia Pacific Polysilicon Market Outlook, By Fluidized Bed Reactor (FBR) Process (2020-2028) ($MN)

- 78 Asia Pacific Polysilicon Market Outlook, By Siemens Process (2020-2028) ($MN)

- 79 Asia Pacific Polysilicon Market Outlook, By Application (2020-2028) ($MN)

- 80 Asia Pacific Polysilicon Market Outlook, By Photovoltaic (2020-2028) ($MN)

- 81 Asia Pacific Polysilicon Market Outlook, By Solar Power Generation (2020-2028) ($MN)

- 82 Asia Pacific Polysilicon Market Outlook, By Monocrystalline Solar Panel (2020-2028) ($MN)

- 83 Asia Pacific Polysilicon Market Outlook, By Multicrystalline Solar Panel (2020-2028) ($MN)

- 84 Asia Pacific Polysilicon Market Outlook, By Civilian Solar Small Equipment (2020-2028) ($MN)

- 85 South America Polysilicon Market Outlook, By Country (2020-2028) ($MN)

- 86 South America Polysilicon Market Outlook, By Grade (2020-2028) ($MN)

- 87 South America Polysilicon Market Outlook, By Electronic Grade (2020-2028) ($MN)

- 88 South America Polysilicon Market Outlook, By Solar Grade (2020-2028) ($MN)

- 89 South America Polysilicon Market Outlook, By Form (2020-2028) ($MN)

- 90 South America Polysilicon Market Outlook, By Granules (2020-2028) ($MN)

- 91 South America Polysilicon Market Outlook, By Chunks (2020-2028) ($MN)

- 92 South America Polysilicon Market Outlook, By Rods (2020-2028) ($MN)

- 93 South America Polysilicon Market Outlook, By Product Type (2020-2028) ($MN)

- 94 South America Polysilicon Market Outlook, By Parallel Connection (2020-2028) ($MN)

- 95 South America Polysilicon Market Outlook, By Series Connection (2020-2028) ($MN)

- 96 South America Polysilicon Market Outlook, By Technology (2020-2028) ($MN)

- 97 South America Polysilicon Market Outlook, By Upgraded Metallurgical-Grade Silicon Process (2020-2028) ($MN)

- 98 South America Polysilicon Market Outlook, By Fluidized Bed Reactor (FBR) Process (2020-2028) ($MN)

- 99 South America Polysilicon Market Outlook, By Siemens Process (2020-2028) ($MN)

- 100 South America Polysilicon Market Outlook, By Application (2020-2028) ($MN)

- 101 South America Polysilicon Market Outlook, By Photovoltaic (2020-2028) ($MN)

- 102 South America Polysilicon Market Outlook, By Solar Power Generation (2020-2028) ($MN)

- 103 South America Polysilicon Market Outlook, By Monocrystalline Solar Panel (2020-2028) ($MN)

- 104 South America Polysilicon Market Outlook, By Multicrystalline Solar Panel (2020-2028) ($MN)

- 105 South America Polysilicon Market Outlook, By Civilian Solar Small Equipment (2020-2028) ($MN)

- 106 Middle East & Africa Polysilicon Market Outlook, By Country (2020-2028) ($MN)

- 107 Middle East & Africa Polysilicon Market Outlook, By Grade (2020-2028) ($MN)

- 108 Middle East & Africa Polysilicon Market Outlook, By Electronic Grade (2020-2028) ($MN)

- 109 Middle East & Africa Polysilicon Market Outlook, By Solar Grade (2020-2028) ($MN)

- 110 Middle East & Africa Polysilicon Market Outlook, By Form (2020-2028) ($MN)

- 111 Middle East & Africa Polysilicon Market Outlook, By Granules (2020-2028) ($MN)

- 112 Middle East & Africa Polysilicon Market Outlook, By Chunks (2020-2028) ($MN)

- 113 Middle East & Africa Polysilicon Market Outlook, By Rods (2020-2028) ($MN)

- 114 Middle East & Africa Polysilicon Market Outlook, By Product Type (2020-2028) ($MN)

- 115 Middle East & Africa Polysilicon Market Outlook, By Parallel Connection (2020-2028) ($MN)

- 116 Middle East & Africa Polysilicon Market Outlook, By Series Connection (2020-2028) ($MN)

- 117 Middle East & Africa Polysilicon Market Outlook, By Technology (2020-2028) ($MN)

- 118 Middle East & Africa Polysilicon Market Outlook, By Upgraded Metallurgical-Grade Silicon Process (2020-2028) ($MN)

- 119 Middle East & Africa Polysilicon Market Outlook, By Fluidized Bed Reactor (FBR) Process (2020-2028) ($MN)

- 120 Middle East & Africa Polysilicon Market Outlook, By Siemens Process (2020-2028) ($MN)

- 121 Middle East & Africa Polysilicon Market Outlook, By Application (2020-2028) ($MN)

- 122 Middle East & Africa Polysilicon Market Outlook, By Photovoltaic (2020-2028) ($MN)

- 123 Middle East & Africa Polysilicon Market Outlook, By Solar Power Generation (2020-2028) ($MN)

- 124 Middle East & Africa Polysilicon Market Outlook, By Monocrystalline Solar Panel (2020-2028) ($MN)

- 125 Middle East & Africa Polysilicon Market Outlook, By Multicrystalline Solar Panel (2020-2028) ($MN)

- 126 Middle East & Africa Polysilicon Market Outlook, By Civilian Solar Small Equipment (2020-2028) ($MN)

According to Stratistics MRC, the Global Polysilicon Market is accounted for $10.22 billion in 2022 and is expected to reach $23.88 billion by 2028 growing at a CAGR of 15.2% during the forecast period. Metallurgical-grade silicon is used to develop polysilicon, also known as polycrystalline silicon. It is a very pure variety of silicon made up of numerous smaller crystals. This substance is an essential component used in the production of solar cells and other electronic devices.

According to International Renewable Energy Agency (IRENA), the total global solar capacity expansion increased by 19% in 2021, recording 133 GW additional installations. Furthermore, as per World Economic Forum, in 2021, for the first time, solar and wind together generated over 10% of the total electricity across the world, with solar power accounting for around 5% of the share.

Market Dynamics:

Driver:

Demand for solar power

An increase in the demand for polysilicon from the solar power industry is the main factor driving the market growth rate. The development and expansion of various end-user verticals in emerging economies, as well as the rising demand for polysilicon for a range of industrial applications, including the production of multi-crystalline solar panels, electronics, civilian small solar equipment, and others, will also directly and favourably affect the market's growth rate.

Restraint:

Insufficient Raw Materials and High Costs

Lack of demand and supply for raw materials as a result of the lockup and price volatility will be a significant barrier to the market's growth. The market's growth rate will be decelerated by the high cost of R&D, stringent government regulations on industrial operations, rising import and export taxes, and severe international trade barriers. The market's capacity for growth will also be restricted by high capital costs.

Opportunity:

Government initiatives

An increase in industrialization, a greater reliance on renewable energy sources, an increase in the number of small and medium-sized businesses, particularly in developing countries, and a growing emphasis on technological advancements and modernization of production methods will all contribute to the industry's growth. The government will also make greater efforts to reduce the cost of solar products.

Threat:

Use of Capital Intensive Manufacturing Process

The development of a manufacturing facility is a costly venture that also needs cutting-edge equipment and a highly qualified workforce. At present, China controls the market, producing about 80% of the world's goods. A silicon chip shortage brought on by pandemic-related supply chain disruptions had an effect on all industries related to semiconductor electronics, including the automotive and consumer electronics sectors, which depend on semiconductor components. Several nations have realised the significance of domestic production and its geopolitical implications for their semiconductor-dependent industries after witnessing supply chain vulnerabilities.

COVID-19 Impact:

In 2020, China dominated the world market and served as the central focus of the COVID-19 outbreak. The regional lockdown restrictions that were imposed during the pandemic disrupted supply chains and had a negative impact on many end-use industries. Additionally, trade restrictions, labour and raw material shortages, a lack of freight containers, and logistical difficulties all contributed to the pandemic's disruption of the global supply chain. Moreover, the capacity for producing semiconductors was significantly impacted by the lack of raw materials, which led to a total lack of silicon chips.

The photovoltaic segment is expected to be the largest during the forecast period

Due to the widespread use of materials in the production of semiconductors and solar photovoltaic panels, the photovoltaics segment is expected to dominate the market during the projection period. However, the main factor driving this segment's growth is the rising global demand for the installation of solar PV systems, which in turn drives up demand.

The electronics grade segment is expected to have the highest CAGR during the forecast period

Due to the electronics sector's rapid growth and a rise in solar energy usage, the electronics segment is expected to have the highest CAGR during the forecast period. Manufacturers are considering other renewable energy options, like solar energy, in a variety of business sectors due to growing concerns about the depletion of conventional energy sources and the sustainability of the environment. Moreover, solar panels are used as alternative sources of electricity alongside various electrical appliances in power grids and commercial and residential buildings.

Region with largest share:

Because of rising consumption in nations like China, South Korea, and India, the Asia-Pacific region is expected to dominate the global market for polysilicon during the estimation period. The nation's 122,000-ton annual production capacity for polysilicon was emerging, according to the Chinese ministry. Additionally, the majority of the largest solar power facilities in the world as of June 2021 were identified in China and India. Moreover, with a total output capacity of 2,245 megawatts, the Bhadla solar farm is located in India's Jodhpur district, Rajasthan.

Region with highest CAGR:

Due to a variety of factors, including an increase in power outages, an immediate need for dependable power supply, rising demand from a range of end-use industries, and an increase in research and development activities, the Asia-Pacific region is anticipated to have the highest CAGR in the polysilicon market during the forecast period. Furthermore, rising consumption and demand from nations like China and India, investment policies by the government to support industrial growth, and high economic growth are driving market growth in this region.

Key players in the market

Some of the key players in Polysilicon market include SunEdison Inc, Hemlock Semiconductor Operations And Hemlock Semiconductor, REC Silicon ASA, Tokuyama Corporation, Mitsubishi Polycrystalline Silicon America Corporation, Qatar Solar Technologies, Wacker Chemie AG, Osaka Titanium Technologies Co. Ltd, OCI Solar Power LLC, Daqo New Energy Corp. and GCL-Poly Energy Holdings Limited.

Key Developments:

In August 2022, REC Silicon ASA and Mississippi Silicon collaborated to develop a solar supply chain in the United States. They plan to develop this solar supply chain from raw silicon to polysilicon and finally to fully assembled modules.

In April 2022, OCI Company Ltd signed a binding memorandum of understanding (MoU) with the South Korean-based solar manufacturer Hanwha Solutions, which is a unit of Hanwha, for the supply of polysilicon. The order was valued at about USD 1.2 billion. This has helped the company in increasing its profit margins.

Grades Covered:

- Electronic Grade

- Solar Grade

Forms Covered:

- Granules

- Chunks

- Rods

Product Types Covered:

- Parallel Connection

- Series Connection

Technologies Covered:

- Upgraded Metallurgical-Grade Silicon Process

- Fluidized Bed Reactor (FBR) Process

- Siemens Process

Applications Covered:

- Photovoltaic

- Solar Power Generation

- Monocrystalline Solar Panel

- Multicrystalline Solar Panel

- Civilian Solar Small Equipment

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2020, 2021, 2022, 2025, and 2028

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Technology Analysis

- 3.8 Application Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Polysilicon Market, By Grade

- 5.1 Introduction

- 5.2 Electronic Grade

- 5.3 Solar Grade

6 Global Polysilicon Market, By Form

- 6.1 Introduction

- 6.2 Granules

- 6.3 Chunks

- 6.4 Rods

7 Global Polysilicon Market, By Product Type

- 7.1 Introduction

- 7.2 Parallel Connection

- 7.3 Series Connection

8 Global Polysilicon Market, By Technology

- 8.1 Introduction

- 8.2 Upgraded Metallurgical-Grade Silicon Process

- 8.3 Fluidized Bed Reactor (FBR) Process

- 8.4 Siemens Process

9 Global Polysilicon Market, By Application

- 9.1 Introduction

- 9.2 Photovoltaic

- 9.3 Solar Power Generation

- 9.4 Monocrystalline Solar Panel

- 9.5 Multicrystalline Solar Panel

- 9.6 Civilian Solar Small Equipment

10 Global Polysilicon Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 SunEdison Inc

- 12.2 Hemlock Semiconductor Operations And Hemlock Semiconductor

- 12.3 REC Silicon ASA

- 12.4 Tokuyama Corporation

- 12.5 Mitsubishi Polycrystalline Silicon America Corporation

- 12.6 Qatar Solar Technologies

- 12.7 Wacker Chemie AG

- 12.8 Osaka Titanium Technologies Co. Ltd

- 12.9 OCI Solar Power LLC

- 12.10 Daqo New Energy Corp.

- 12.11 GCL-Poly Energy Holdings Limited