ヘルスケアにおけるビッグデータ市場:業界動向と世界の予測 - コンポーネント別、ハードウェアタイプ別、ソフトウェアタイプ別、サービスタイプ別、展開オプション別、応用分野別、ヘルスケア分野別、エンドユーザー別、経済状況別、地域別、主要参入企業別

Big Data in Healthcare Market: Industry Trends and Global Forecasts - Distribution by Component, Hardware, Software, Service, Deployment Option, Application Area, Healthcare Vertical, End User, Economic Status, Geography and Leading Players- 発行日

- ページ情報

- 英文 331 Pages

- 納期

- 即日から翌営業日

- 商品コード

- 1776873

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 医薬品関連専門 医薬品関連専門を専門とする市場調査会社です。

概要

世界のヘルスケアにおけるビッグデータの市場規模は、2035年までの予測期間中に19.20%のCAGRで拡大し、現在の780億米ドルから2035年までに5,400億米ドルに成長すると予測されています。

市場セグメンテーションでは、市場規模および市場機会を以下のパラメータで区分しています:

コンポーネント

- ハードウェア

- ソフトウェア

- サービス

ハードウェアタイプ

- ストレージ・デバイス

- ネットワーキング・インフラ

- サーバー

ソフトウェアタイプ

- 電子カルテ

- 診療管理ソフトウェア

- 収益サイクル管理ソフトウェア

- ワークフォース管理ソフトウェア

サービスタイプ

- 記述的分析

- 診断アナリティクス

- 予測分析

- 処方的分析

展開オプション

- クラウドベース

- オンプレミス

応用分野

- 臨床データ管理

- 財務管理

- 運用管理

- 集団健康管理

ヘルスケア分野別

- ヘルスケアサービス

- 医療機器

- 医薬品

- その他

エンドユーザー

- クリニック

- 医療保険代理店

- 病院

- その他

経済状況

- 高所得国

- 高中所得国

- 低中所得国

主要地域

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・北アフリカ

- その他の地域

世界のヘルスケアにおけるビッグデータ市場:成長と動向

ヘルスケアにおけるビッグデータとは、継続的に拡大し、従来のツールでは効率的に保存・処理できない膨大な量のデータを指します。特にここ数年、ヘルスケア分野では大量のデータが生成されるため、ビッグデータ/ビッグデータ分析ツールや技術の人気が飛躍的に高まっています。ヘルスケアにおけるビッグデータは、膨大な量の既存データを利用することで、患者にパーソナライズされたケアを提供するという課題をチャンスに変えます。さらにビッグデータは、集団健康管理、電子カルテ(EHR)管理、製薬研究、遠隔医療や遠隔健康など、ヘルスケア業界のさまざまな分野で利用することができます。

ヘルスケア領域におけるビッグデータの普及が進んでいるため、ヘルスケアのビッグデータ市場規模には大きなインパクトがあります。ビッグデータ分析はヘルスケア市場だけでなく、さまざまな分野で組織の成長や、機械学習や人工知能を利用した将来の動向予測に利用されています。さらに、ビッグデータは金融分野にも大きな影響を与えています。ヘルスケア領域におけるビッグデータにはいくつかの利点があり、予測分析と機械学習アルゴリズムをビッグデータと統合することで、病気の早期発見、個別化された治療計画、精密医療が可能になります。

ヘルスケアの世界ビッグデータ市場:主要インサイト

当レポートでは、世界のヘルスケアにおけるビッグデータ市場の現状を掘り下げ、業界内の潜在的な成長機会を特定しています。当レポートの主な調査結果は以下の通りです。

- 405社以上の企業が、ヘルスケアにおけるビッグデータ活用を支援するためのカスタマイズされたソリューションやサービスを提供しており、そのうち約55%がデータ管理や分析のためのデータウェアハウスやデータレイクを提供しています。

- サービスプロバイダーの大半(65%以上)は北米、特に米国に拠点を置いており、米国に拠点を置くサービスプロバイダーの大半(56%)は中堅企業、次いで大手企業(26%)です。

- 市場情勢は非常に断片化されており、異なる地域情勢別を拠点とする新規参入企業と既存企業の両方が存在するのが特徴で、こうした企業の55%近くが中堅企業です。

- さまざまな分析モデルが臨床データ、業務データ、財務データから洞察を導き出しています。参入企業の23%は、予測分析、処方分析、記述分析を含むビッグデータ分析の包括的なソフトウェアスイートを提供しています。

- 競争力を高めるため、各社は既存の能力を積極的にアップグレードし、新たな能力を追加することで、それぞれのポートフォリオや提携ビッグデータ製品を強化しています。

- ヘルスケア市場におけるビッグデータの進化に影響を与える主な促進要因と障壁を分析することで、この領域における現在と将来のビジネスチャンスをより深く理解するための貴重な洞察を得ることができます。

- クラウドベースのソリューションとサービスの採用増加に牽引され、ヘルスケアにおけるビッグデータ市場は、今後12年間でCAGR 19.06%で成長する可能性が高いです。

- 予測される市場機会は、さまざまなタイプのハードウェア、サービス、ソフトウェアなど、ビッグデータのさまざまな構成要素にうまく分散されると予想されます。

- 高所得国は、業務管理を最適化するためにビッグデータ・ソリューションの導入を優先し、ヘルスケア業務の効率性と有効性の強化につなげて市場収益を牽引しています。

- 遠隔医療サービスと個別化医療に対する需要の高まりに伴い、ヘルスケアにおけるビッグデータ市場は、さまざまな地域に拠点を置く参入企業に有利な機会を提供しています。

ヘルスケアにおけるビッグデータの世界市場:主要セグメント

コンポーネント別では、市場はビッグデータハードウェア、ビッグデータソフトウェア、ビッグデータサービスに区分されます。現在、ヘルスケアにおけるビッグデータの世界市場では、ハードウェアセグメントが最大(40%超)のシェアを占めています。また、先進技術の採用が進み、技術革新への投資が続いていることから、ハードウェアセグメントは他のセグメントと比較して速いペースで成長する可能性が高いです。

ハードウェアタイプ別では、市場はストレージデバイス、ネットワークインフラ、サーバーに区分されます。現在、ヘルスケアにおけるビッグデータ市場では、ストレージデバイス分野が最も高い割合(約60%)を占めています。さらに、このセグメントは比較的高いCAGRで成長する可能性が高いです。

ソフトウェアタイプ別では、市場は電子カルテ、診療管理ソフトウェア、収益サイクル管理ソフトウェア、労働力管理ソフトウェアに区分されます。現在、ヘルスケアにおけるビッグデータ市場では、電子カルテ分野が最大シェア(45%超)を占めています。また、労働力管理ソフトウェア分野は比較的高いCAGRで成長する可能性が高いです。

サービスタイプ別に、市場は記述アナリティクス、診断アナリティクス、予測アナリティクス、処方アナリティクスに区分されます。現在、診断アナリティクス分野がヘルスケアにおけるビッグデータ市場で最も高い割合(30%超)を占めています。さらに、処方的アナリティクスセグメントのヘルスケアにおけるビッグデータ市場は、比較的高いCAGRで成長する可能性が高いことは注目に値します。

市場は展開オプション別では、クラウドベース展開とオンプレミス展開に区分されます。スケーラビリティ、柔軟性、費用対効果、導入とメンテナンスの容易さ、データへのアクセスのしやすさなど、クラウドベースの展開が提供するさまざまなメリットにより、現在、クラウドベースのセグメントがヘルスケア分野のビッグデータ市場で最大シェア(約60%)を占めています。この動向は今後も変わらないと思われます。

応用分野別では、市場は臨床データ管理、財務管理、運用管理、集団健康管理に区分されます。現在、ヘルスケアにおけるビッグデータ市場では、運用管理セグメントが最大シェア(30%超)を占めています。さらに、人口健康管理セグメントは、予測期間中、他のセグメントと比較して高いCAGRで成長し、最も高い成長の可能性を示すと予想されます。

ヘルスケア分野別では、ヘルスケアサービス、医療機器、医薬品、その他の分野に区分されます。ヘルスケアサービス分野が市場全体の主要な牽引役となることが予想されるが、医療機器分野のヘルスケアにおけるビッグデータの世界市場が20%以上の比較的高いCAGRで成長する可能性が高いことは注目に値します。

エンドユーザー別では、世界市場は診療所、医療保険機関、病院、その他に区分されます。現在、病院セグメントが最大の市場シェア(40%超)を占めています。しかし、診療所セグメントのヘルスケアにおけるビッグデータ市場は、今後数年間で大幅な成長が見込まれています。

経済状況別では、市場は高所得国、高中所得国、低中所得国に区分されます。現在、高所得国セグメントはヘルスケアにおけるビッグデータ市場で最も高い割合(~85%)を占めています。さらに、高中所得国セグメントのヘルスケアにおけるビッグデータ市場は、比較的高いCAGRで成長する可能性が高いことは注目に値します。

主要地域別に見ると、市場は北米、欧州、アジア、中東・アフリカ、ラテンアメリカ、その他に区分されます。現在、北米(~60%)がヘルスケアにおけるビッグデータ市場を独占し、最大の収益シェアを占めています。しかし、アジア太平洋地域の市場はより高いCAGRで成長すると予想されています。

ヘルスケアにおけるビッグデータ市場の参入企業例

- Accenture

- Akka Technologies

- Altamira.ai

- Amazon Web Services

- Athena Global Technologies

- atom Consultancy Services(ACS)

- Avenga

- Happiest Minds

- InData Labs

- Itransition

- Kellton

- Keyrus

- Lutech

- Microsoft

- Nagarro

- Nous Infosystems

- NTT data

- Oracle

- Orange Mantra

- Oxagile

- Scalefocus

- Softweb Solutions

- Solix Technologies

- Spindox

- Tata Elxsi

- Teradata

- Trianz(formerly CBIG Consulting)

- Trigyn Technologies

- XenonStack

当レポートでは、世界のヘルスケアにおけるビッグデータ市場について調査し、市場の概要とともに、コンポーネント別、ハードウェアタイプ別、ソフトウェアタイプ別、サービスタイプ別、展開オプション別、応用分野別、ヘルスケア分野別、エンドユーザー別、経済状況別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 序文

第2章 調査手法

- 章の概要

- 調査の前提

- プロジェクト調査手法

- 予測調査手法

- 堅牢な品質管理

- 重要な考慮事項

- 主要な市場セグメンテーション

第3章 経済的およびその他のプロジェクト特有の考慮事項

- 章の概要

- 市場力学

第4章 エグゼクティブサマリー

第5章 イントロダクション

- 章の概要

- ビッグデータの概要

- ビッグデータ分析

- ヘルスケアにおけるビッグデータの応用

- 将来の展望

第6章 市場情勢

第7章 重要な洞察

- 章の概要

- ヘルスケアサービスプロバイダーにおけるビッグデータ:重要な洞察

第8章 企業競争力分析

- 章の概要

- 前提と主要なパラメータ

- 調査手法

- ヘルスケアサービスプロバイダーにおけるビッグデータ:企業競争力分析

第9章 企業プロファイル北米のヘルスケアサービスプロバイダーにおけるビッグデータ

- 章の概要

- 北米の主要参入企業の詳細プロファイル

- Amazon Web Services

- Microsoft

- Oracle

- Teradata

- 北米のその他の参入企業のプロファイル

- Itransition

- Nous Infosystems

- Oxagile

- Softweb Solutions

- Solix Technologies

- Trianz(formerly CBIG Consulting)

第10章 企業プロファイル:欧州のヘルスケアサービスプロバイダーにおけるビッグデータ

- 章の概要

- 欧州の主要参入企業の詳細プロファイル

- Accenture

- Keyrus

- 欧州のその他の参入企業のプロファイル

- Akka Technologies

- Altamira.ai

- atom Consultancy Services(ACS)

- Avenga

- Lutech

- Nagarro

- Scalefocus

- Spindox

第11章 企業プロファイル:アジアおよび世界のその他の地域のヘルスケアサービスプロバイダーにおけるビッグデータ

- 章の概要

- アジアおよびその他の諸国の主要参入企業の詳細プロファイル

- Tata Elxsi

- Kellton

- アジアおよびその他の諸国のその他の参入企業のプロファイル

- Athena Global Technologies

- Happiest Minds

- InData Labs

- NTT data

- OrangeMantra

- Trigyn Technologies

- XenonStack

第12章 市場影響分析:促進要因、抑制要因、機会、課題

第13章 ヘルスケア市場における世界ビッグデータ

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場における世界のビッグデータ、歴史的動向(2018年以降)と予測(2035年まで)

- 主要な市場セグメンテーション

第14章 ヘルスケア市場におけるビッグデータ(コンポーネント別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:コンポーネント別

- データの三角測量と検証

第15章 ヘルスケア市場におけるビッグデータ(ハードウェア別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:ハードウェアタイプ別

- データの三角測量と検証

第16章 ヘルスケア市場におけるビッグデータ(ソフトウェアタイプ別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:ソフトウェアタイプ別

- データの三角測量と検証

第17章 ヘルスケア市場におけるビッグデータ(サービス別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:サービスタイプ別

- データの三角測量と検証

第18章 ヘルスケア市場におけるビッグデータ(展開オプション)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:展開オプション別

- データの三角測量と検証

第19章 ヘルスケア市場におけるビッグデータ(応用分野別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:応用分野別

- データの三角測量と検証

第20章 ヘルスケア市場におけるビッグデータ(ヘルスケア分野別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:ヘルスケア分野別

- データの三角測量と検証

第21章 ヘルスケア市場におけるビッグデータ(エンドユーザー別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:エンドユーザー別

- データの三角測量と検証

第22章 ヘルスケア市場におけるビッグデータ(経済状況別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:経済状況別

- データの三角測量と検証

第23章 ヘルスケア市場におけるビッグデータ(地域別)

- 章の概要

- 主要な前提と調査手法

- ヘルスケア市場におけるビッグデータ:地域別分布

- データの三角測量と検証

第24章 ヘルスケア市場におけるビッグデータ、主要企業の収益予測

- 章の概要

- 主要な前提と調査手法

- Microsoft

- Optum

- IBM

- Oracle

- Allscripts

第25章 結論

第26章 エグゼクティブ洞察

第27章 付録I:表形式データ

第28章 付録II:企業および組織の一覧

図表

List of Tables

- Figure 2.1 Research Methodology: Project Methodology

- Figure 2.2 Research Methodology: Forecast Methodology

- Figure 2.3 Research Methodology: Robust Quality Control

- Figure 2.4 Research Methodology: Key Market Segmentation

- Figure 3.1 Lessons Learnt from Past Recessions

- Figure 4.1 Executive Summary: Overall Market Landscape

- Figure 4.2 Executive Summary: Global Market for Big Data in Healthcare by Component, Type of Hardware, Type of Software, Type of Service, and Deployment Option

- Figure 4.3 Executive Summary: Global Market for Big Data in Healthcare by Application Area, Healthcare Vertical, End User, Economic Status, Geography and Leading Players

- Figure 5.1 Types of Big Data Analytics

- Figure 5.2 Applications of Big Data in Healthcare

- Figure 6.1 Big Data in Healthcare Service Providers: Distribution by Year of Establishment

- Figure 6.2 Big Data in Healthcare Service Providers: Distribution by Company Size

- Figure 6.3 Big Data in Healthcare Service Providers: Distribution by Location of Headquarters (Region)

- Figure 6.4 Big Data in Healthcare Service Providers: Distribution by Location of Headquarters (Country)

- Figure 6.5 Big Data in Healthcare Service Providers: Distribution by Type of Business Model

- Figure 6.6 Big Data in Healthcare Service Providers: Distribution by Type of Offering

- Figure 6.7 Big Data in Healthcare Service Providers: Type of Big Data Analytics Offered

- Figure 6.8 Big Data in Healthcare Service Providers: Type of Big Data Storage Solution Offered

- Figure 6.9 Big Data in Healthcare Service Providers: Distribution by Deployment Option

- Figure 6.10 Big Data in Healthcare Service Providers: Distribution by Application Area

- Figure 6.11 Big Data in Healthcare Service Providers: Distribution by End User

- Figure 7.1 Big Data in Healthcare Service Providers: Distribution by Year of Establishment and Company Size

- Figure 7.2 Big Data in Healthcare Service Providers: Distribution by Company Size and Location of Headquarters

- Figure 7.3 Big Data in Healthcare Service Providers: Distribution by Type of Offering and Company Size

- Figure 7.4 Big Data in Healthcare Service Providers: Distribution by Type of Big Data Analytics Offered and Application Area

- Figure 7.5 Big Data in Healthcare Service Providers: Distribution by Company Size, Application Area and End User

- Figure 8.1 Company Competitiveness Analysis: Small Service Providers based in North America

- Figure 8.2 Company Competitiveness Analysis: Mid-sized Service Providers based in North America (I/II)

- Figure 8.3 Company Competitiveness Analysis: Mid-sized Service Providers based in North America (II/II)

- Figure 8.4 Company Competitiveness Analysis: Large Service Providers based in North America (I/II)

- Figure 8.5 Company Competitiveness Analysis: Large Service Providers based in North America (II/II)

- Figure 8.6 Company Competitiveness Analysis: Very Large Service Providers based in North America

- Figure 8.7 Company Competitiveness Analysis: Small Service Providers based in Europe

- Figure 8.8 Company Competitiveness Analysis: Mid-sized Service Providers based in Europe

- Figure 8.9 Company Competitiveness Analysis: Large and Very Large Big Service Providers based in Europe

- Figure 8.10 Company Competitiveness Analysis: Small Service Providers based in Asia and Rest of the World

- Figure 8.11 Company Competitiveness Analysis: Mid-sized Service Providers based in Asia and Rest of the World (I/II)

- Figure 8.12 Company Competitiveness Analysis: Mid-sized Service Providers based in Asia and Rest of the World (II/II)

- Figure 8.13 Company Competitiveness Analysis: Large Big Service Providers based in Asia and Rest of the World

- Figure 8.14 Company Competitiveness Analysis: Very Large Service Providers based in Asia and Rest of the World

- Figure 9.1 Amazon Web Services: Annual Revenues (USD Billion)

- Figure 9.2 Microsoft: Annual Revenues (USD Billion)

- Figure 9.3 Oracle: Annual Revenues (USD Billion)

- Figure 9.4 Teradata: Annual Revenues (USD Billion)

- Figure 10.1 Accenture: Annual Revenues (USD Billion)

- Figure 10.2 Keyrus: Annual Revenues (USD Million)

- Figure 11.1 Tata Elxsi: Annual Revenues (INR Billion)

- Figure 11.2 Kellton: Annual Revenues (INR Billion)

- Figure 12.1 Big Data in Healthcare Market Drivers

- Figure 12.2 Big Data in Healthcare Market Restraints

- Figure 12.3 Big Data in Healthcare Market Opportunities

- Figure 12.4 Big Data in Healthcare Market Challenges

- Figure 13.1 Global Market for Big Data in Healthcare, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 13.2 Global Market for Big Data in Healthcare, Forecasted Estimates (Till 2035): Conservative Scenario (USD Billion)

- Figure 13.3 Global Market for Big Data in Healthcare, Forecasted Estimates (Till 2035): Optimistic Scenario (USD Billion)

- Figure 14.1 Big Data in Healthcare Market: Distribution by Component (USD Billion)

- Figure 14.2 Big Data in Healthcare Market for Hardware, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 14.3 Big Data in Healthcare Market for Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 14.4 Big Data in Healthcare Market for Services, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.1 Big Data in Healthcare Market: Distribution by Type of Hardware (USD Billion)

- Figure 15.2 Big Data in Healthcare Market for Storage Devices, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.3 Big Data in Healthcare Market for Servers, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.4 Big Data in Healthcare Market for Networking Infrastructure, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.1 Big Data in Healthcare Market: Distribution by Type of Software (USD Billion)

- Figure 16.2 Big Data in Healthcare Market for Electronic Health Records, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.3 Big Data in Healthcare Market for Revenue Cycle Management Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.4 Big Data in Healthcare Market for Practice Management Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.5 Big Data in Healthcare Market for Workforce Management Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.1 Big Data in Healthcare Market: Distribution by Type of Service (USD Billion)

- Figure 17.2 Big Data in Healthcare Market for Diagnostic Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.3 Big Data in Healthcare Market for Descriptive Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.4 Big Data in Healthcare Market for Predictive Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.5 Big Data in Healthcare Market for Prescriptive Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.1 Big Data in Healthcare Market: Distribution by Deployment Option (USD Billion)

- Figure 18.2 Big Data in Healthcare Market for Cloud-based Deployment, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.3 Big Data in Healthcare Market for On-premises Deployment, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.1 Big Data in Healthcare Market: Distribution by Application Area

- Figure 19.2 Big Data in Healthcare Market for Operational Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.3 Big Data in Healthcare Market for Clinical Data Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.4 Big Data in Healthcare Market for Financial Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.5 Big Data in Healthcare Market for Population Health Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.1 Big Data in Healthcare Market: Distribution by Healthcare Vertical

- Figure 20.2 Big Data in Healthcare Market for Healthcare Services, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.3 Big Data in Healthcare Market for Pharmaceuticals, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.4 Big Data in Healthcare Market for Medical Devices, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.5 Big Data in Healthcare Market for Other Verticals, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.1 Big Data in Healthcare Market: Distribution by End User (USD Billion)

- Figure 21.2 Big Data in Healthcare Market for Hospitals, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.3 Big Data in Healthcare Market for Health Insurance Agencies, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.4 Big Data in Healthcare Market for Clinics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.5 Big Data in Healthcare Market for Other End Users, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.1 Big Data in Healthcare Market: Distribution by Economic Status

- Figure 22.2 Big Data in Healthcare Market in High Income Countries, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.3 Big Data in Healthcare Market in the US, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.4 Big Data in Healthcare Market in Canada, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.5 Big Data in Healthcare Market in Germany, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.6 Big Data in Healthcare Market in the UK, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.7 Big Data in Healthcare Market in the UAE, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.8 Big Data in Healthcare Market in South Korea, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.9 Big Data in Healthcare Market in France, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.10 Big Data in Healthcare Market in Australia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.11 Big Data in Healthcare Market in New Zealand, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.12 Big Data in Healthcare Market in Italy, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.13 Big Data in Healthcare Market in Saudi Arabia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.14 Big Data in Healthcare Market in Nordic Countries, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.15 Big Data in Healthcare Market in Upper-Middle Income Countries, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.16 Big Data in Healthcare Market in China, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.17 Big Data in Healthcare Market in Russia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.18 Big Data in Healthcare Market in Brazil, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.19 Big Data in Healthcare Market in Japan, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.20 Big Data in Healthcare Market in South Africa, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.21 Big Data in Healthcare Market in India, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.1 Big Data in Healthcare Market: Distribution by Geography (USD Billion)

- Figure 23.2 Big Data in Healthcare Market in North America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.3 Big Data in Healthcare Market in Europe, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.4 Big Data in Healthcare Market in Asia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.5 Big Data in Healthcare Market in Middle East and North Africa, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.6 Big Data in Healthcare Market in Latin America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.7 Big Data in Healthcare Market in Rest of the World, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 24.1 Microsoft: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

- Figure 24.2 Optum: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

- Figure 24.3 IBM: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

- Figure 24.4 Oracle: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 USD Billion)

- Figure 24.5 Allscripts: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

目次

GLOBAL BIG DATA IN HEALTHCARE MARKET: OVERVIEW

As per Roots Analysis, the big data in healthcare market is estimated to grow from USD 78 billion in the current year to USD 540 billion by 2035, at a CAGR of 19.20% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Component

- Hardware

- Software

- Services

Type of Hardware

- Storage Devices

- Networking Infrastructure

- Servers

Type of Software

- Electronic Health Record

- Practice Management Software

- Revenue Cycle Management Software

- Workforce Management Software

Type of Service

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

Deployment Option

- Cloud-based

- On-premises

Application Area

- Clinical Data Management

- Financial Management

- Operational Management

- Population Health Management

Healthcare Vertical

- Healthcare Services

- Medical Devices

- Pharmaceuticals

- Other Verticals

End User

- Clinics

- Health Insurance Agencies

- Hospitals

- Other End Users

Economic Status

- High Income Countries

- Upper-Middle Income Countries

- Lower-Middle Income Countries

Key Geographical Regions

- North America

- Europe

- Asia

- Latin America

- Middle East and North Africa

- Rest of the World

GLOBAL BIG DATA IN HEALTHCARE MARKET: GROWTH AND TRENDS

Big Data in healthcare refers to the vast amount of data that is continuously expanding and cannot be efficiently stored or processed using traditional tools. Notably, over the past few years, the popularity of big data / big data analytics tools and technologies has increased exponentially in healthcare due to the large volumes of data being generated in this domain. Big data in healthcare turns the challenges into opportunities to provide personalized care to the patients by using huge amounts of existing data. Further, big data can be used across different verticals of healthcare industry, such as in population health management, Electronic Health Record (EHR) management, pharmaceutical research, and telemedicine and telehealth.

Owing to the increasing popularity of big data in healthcare domain, there is a huge impact of big data in healthcare market size. Big data analysis is used not only in healthcare market but also used in different sectors for the growth of the organization and to forecast future trends using machine learning and artificial intelligence. Moreover, big data has also had a considerable impact on the financial sector. Big data in the healthcare domain has several advantages and the integration of predictive analytics and machine learning algorithms with big data can enable early detection of diseases, personalized treatment plans, and precision medicine.

GLOBAL BIG DATA IN HEALTHCARE MARKET: KEY INSIGHTS

The report delves into the current state of global big data in healthcare market and identifies potential growth opportunities within industry. Some key findings from the report include:

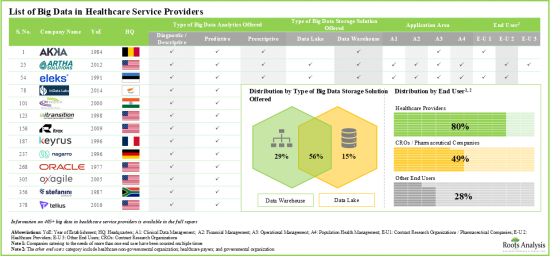

- More than 405 players claim to offer customized solutions and services to support big data in healthcare initiatives, with around 55% offering data warehouses and data lakes for data management and analytics.

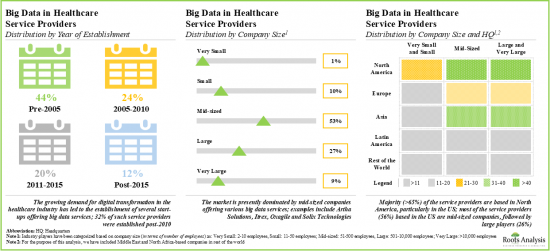

- Majority (>65%) of the service providers are based in North America, particularly in the US; most of the service providers (56%) based in the US are mid-sized companies, followed by large players (26%).

- The market landscape is highly fragmented, featuring the presence of both new entrants and established players based across different geographical regions; close to 55% of such players are mid-sized companies.

- Various analytical models derive insights from clinical, operational and financial data; 23% of the players offer a comprehensive software suite of big data analytics including predictive, prescriptive, and descriptive analytics.

- In pursuit of building a competitive edge, players are actively upgrading their existing capabilities and adding new competencies in order to augment their respective portfolios and affiliated big data offerings.

- By analyzing the key drivers and barriers affecting the evolution of big data in healthcare market, valuable insights can be generated leading to a deeper understanding of the current and future opportunities within this domain.

- Driven by the increasing adoption of cloud-based solutions and services, the big data in healthcare market is likely to grow at a CAGR of 19.06% over the next 12 years.

- The projected market opportunity is anticipated to be well distributed across different components of big data, including various types of hardware, services and software.

- High-income countries are driving market revenues by prioritizing the deployment of big data solutions to optimize operational management, leading to enhanced efficiency and effectiveness in healthcare operations.

- With the rise in demand for telehealth services and personalized medicine, the big data in healthcare market presents lucrative opportunities for players based across various geographies.

GLOBAL BIG DATA IN HEALTHCARE MARKET: KEY SEGMENTS

Hardware Segment Occupies the Largest Share of the Big Data in Healthcare Market

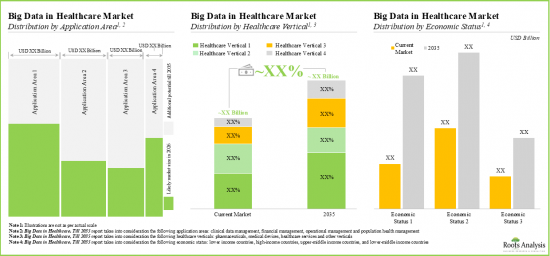

Based on the component, the market is segmented into big data hardware, big data software and big data services. At present, hardware segment holds the maximum (>40%) share of the global big data in healthcare market. Additionally, due to the rising adoption of advanced technologies, and ongoing investments in innovation, the hardware segment is likely to grow at a faster pace compared to the other segments.

By Type of Hardware, Storage Devices Segment is the Fastest Growing Segment of the Global Big Data in Healthcare Market

Based on the type of hardware, the market is segmented into storage devices, networking infrastructure and servers. Currently, storage devices segment captures the highest proportion (~60%) of the big data in healthcare market. Further, this segment is likely to grow at a relatively higher CAGR.

Electronic Health Record Segment Occupy the Largest Share of the Big Data in Healthcare Market

Based on the type of software, the market is segmented into electronic health record, practice management software, revenue cycle management software, and workforce management software. At present, the electronic health record segment holds the maximum share (>45%) of the big data in healthcare market. In addition, workforce management software segment is likely to grow at a relatively higher CAGR.

By Type of Service, the Diagnostic Analytics Segment is the Fastest Growing Segment of the Big Data in Healthcare Market During the Forecast Period

Based on the type of service, the market is segmented into descriptive analytics, diagnostic analytics, predictive analytics, and prescriptive analytics. Currently, the diagnostic analytics segment captures the highest proportion (>30%) of the big data in healthcare market. Further, it is worth highlighting that the big data in healthcare market for prescriptive analytics segment is likely to grow at a relatively higher CAGR.

Cloud-based Segment Account for the Largest Share of the Global Big Data in Healthcare Market

Based on the deployment option, the market is segmented into cloud-based deployment and on-premises deployment. Currently, cloud-based segment holds the maximum share (~60%) of the big data in healthcare market owing to the various benefits offered by cloud-based deployment, such as scalability, flexibility, cost-effectiveness, ease of implementation and maintenance, and data accessibility. This trend is likely to remain the same in the coming years.

By Application Area, Operational Management Segment is Likely to Dominate the Big Data in Healthcare Market

Based on the application area, the market is segmented into clinical data management, financial management, operational management, and population health management. At present, the operational management segment holds the maximum share (>30%) of the big data in healthcare market. Additionally, the population health management segment is expected to show the highest growth potential during the forecast period, growing at a higher CAGR, compared to the other segments.

The Healthcare Services Segment in Healthcare Vertical Occupy the Largest Share of the Big Data in Healthcare Market

Based on the healthcare vertical, the market is segmented into healthcare services, medical devices, pharmaceuticals, and other verticals. While healthcare services segment is expected to be the primary driver of the overall market, it is worth highlighting that the global big data in healthcare market for medical devices segment is likely to grow at a relatively higher CAGR of more than 20%.

Currently, Hospitals Segment Holds the Largest Share of the Big Data in Healthcare Market

Based on end users, the global market is segmented into clinics, health insurance agencies, hospitals, and other end users. Currently, the hospitals segment holds the largest market share (>40%). However, the big data in healthcare market for clinics segment is expected to witness substantial growth in the coming years.

By Economic Status, the Upper-Middle Income Countries Segment is the Fastest Growing Segment of the Big Data in Healthcare Market During the Forecast Period

Based on the economic status, the market is segmented into high income countries, upper-middle income countries, and lower-middle income countries. Currently, the high-income countries segment captures the highest proportion (~85%) of the big data in healthcare market. Further, it is worth highlighting that the big data in healthcare market for upper-middle income countries segment is likely to grow at a relatively higher CAGR.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia, Middle East and North Africa, Latin America and Rest of the World. Currently, North America (~60%) dominates the big data in healthcare market and accounts for the largest revenue share. However, the market in Asia-Pacific is expected to grow at a higher CAGR.

Example Players in the Big Data in Healthcare Market

- Accenture

- Akka Technologies

- Altamira.ai

- Amazon Web Services

- Athena Global Technologies

- atom Consultancy Services (ACS)

- Avenga

- Happiest Minds

- InData Labs

- Itransition

- Kellton

- Keyrus

- Lutech

- Microsoft

- Nagarro

- Nous Infosystems

- NTT data

- Oracle

- Orange Mantra

- Oxagile

- Scalefocus

- Softweb Solutions

- Solix Technologies

- Spindox

- Tata Elxsi

- Teradata

- Trianz (formerly CBIG Consulting)

- Trigyn Technologies

- XenonStack

PRIMARY RESEARCH OVERVIEW

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews conducted with the following industry stakeholders:

- Chief Executive Officer and Founder, Company A

- Chief Executive Officer and Co-Founder, Company B

- Chief People Officer and Co-Founder, Company C

- Vice President, Company D

- Vice President, Company E

- Business Head, Company F

- Senior IT Inside Sales Lead, Company G

- Senior Manager, Company H

- Delivery Manager, Company I

- Strategy, Research and Analyst Relations Manager, Company J

- Business Development Manager, Company K

- Business Development Associate, Company L

- Business Development Specialist Advisor, Company M

- Business Development Executive, Company N

GLOBAL BIG DATA IN HEALTHCARE MARKET: RESEARCH COVERAGE

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global big data in healthcare market, focusing on key market segments, including [A] component, [B] type of hardware, [C] type of software, [D] type of service, [E] deployment option, [F] application area, [G] healthcare vertical, [H] end user, [I] economic status and [J] key geographical regions.

- Market Landscape: A comprehensive evaluation of big data in healthcare service providers, considering various parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] business model, [E] type of offering, [F] type of big data analytics offered, [G] type of big data storage solution offered, [H] deployment option, [I] application area and [J] end user.

- Company Competitiveness Analysis: A comprehensive competitive analysis of big data in healthcare service providers, examining factors, such as [A] supplier strength and [B] portfolio strength.

- Company Profiles: In-depth profiles of companies engaged in offering big data analytics solutions across various geographies, focusing on [A] company overviews, [B] financial information (if available), [C] big data analytics offerings and capabilities and [D] recent developments and an informed future outlook.

- Market Impact Analysis: A thorough analysis of various factors, such as drivers, restraints, opportunities, and existing challenges that are likely to impact market growth.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2.RESEARCH METHODOLOGY

- 2.1.Chapter Overview

- 2.2.Research Assumptions

- 2.3.Project Methodology

- 2.4.Forecast Methodology

- 2.5.Robust Quality Control

- 2.6.Key Considerations

- 2.6.1.Demographics

- 2.6.2.Economic Factors

- 2.6.3.Government Regulations

- 2.6.4. Supply Chain

- 2.6.5.COVID Impact / Related Factors

- 2.6.6. Market Access

- 2.6.7. Healthcare Policies

- 2.6.8. Industry Consolidation

- 2.7. Key Market Segmentations

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Market Dynamics

- 3.2.1. Time Period

- 3.2.1.1. Historical Trends

- 3.2.1.2. Current and Forecasted Estimates

- 3.2.2. Currency Coverage

- 3.2.2.1. Major Currencies Affecting the Market

- 3.2.2.2. Impact of Currency Fluctuations on the Industry

- 3.2.3. Foreign Exchange Impact

- 3.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 3.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 3.2.4. Recession

- 3.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 3.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 3.2.5. Inflation

- 3.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 3.2.5.2. Potential Impact of Inflation on the Market Evolution

- 3.2.1. Time Period

4. EXECUTIVE SUMMARY

- 4.1. Chapter Overview

5. INTRODUCTION

- 5.1. Chapter Overview

- 5.2. Overview of Big Data

- 5.2.1. Types of Big Data

- 5.2.1.1. Structured Data

- 5.2.1.2. Unstructured Data

- 5.2.1.3. Semi-Structured Data

- 5.2.2. Management and Storage of Big Data

- 5.2.1. Types of Big Data

- 5.3. Big Data Analytics

- 5.3.1. Types of Big Data Analytics

- 5.3.1.1. Descriptive Analytics

- 5.3.1.2. Diagnostic Analytics

- 5.3.1.3. Predictive Analytics

- 5.3.1.4. Prescriptive Analytics

- 5.3.1. Types of Big Data Analytics

- 5.4. Applications of Big Data in Healthcare

- 5.5. Future Perspective

6. OVERALL MARKET LANDSCAPE

- 6.1. Chapter Overview

- 6.2. Big Data in Healthcare Service Providers: Overall Market Landscape

- 6.3. Analysis by Year of Establishment

- 6.4. Analysis by Company Size

- 6.5. Analysis by Location of Headquarters

- 6.6. Analysis by Type of Business Model

- 6.7. Analysis by Type of Offering

- 6.8. Analysis by Type of Big Data Analytics Offered

- 6.9. Analysis by Type of Big Data Storage Solution Offered

- 6.10. Analysis by Deployment Option

- 6.11. Analysis by Application Area

- 6.12. Analysis by End User

7. KEY INSIGHTS

- 7.1. Chapter Overview

- 7.2. Big Data in Healthcare Service Providers: Key Insights

- 7.2.1. Analysis by Year of Establishment and Company Size

- 7.2.2. Analysis by Company Size and Location of Headquarters

- 7.2.3. Analysis by Type of Offering and Company Size

- 7.2.4. Analysis by Type of Big Data Analytics Offered and Application Area

- 7.2.5. Analysis by Company Size, Application Area and End User

8. COMPANY COMPETITIVENSS ANALYSIS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Big Data in Healthcare Service Providers: Company Competitiveness Analysis

- 8.4.1. Big Data in Healthcare Service Providers based in North America

- 8.4.1.1. Small Service Providers based in North America

- 8.4.1.2. Mid-sized Service Providers based in North America

- 8.4.1.3. Large Service Providers based in North America

- 8.4.1.4. Very LargeService Providers based in North America

- 8.4.2. Big Data in Healthcare Service Providers based in Europe

- 8.4.2.1. Small Service Providers based in Europe

- 8.4.2.2. Mid-sized Service Providers based in Europe

- 8.4.2.3. Large and Very Large Service Providers based in Europe

- 8.4.3. Big Data in Healthcare Service Providers based in Asia and Rest of the World

- 8.4.3.1. Small Service Providers based in Asia and Rest of the World

- 8.4.3.2. Mid-sized Service Providers based in Asia and Rest of the World

- 8.4.3.3. Large Service Providers based in Asia and Rest of the World

- 8.4.3.4. Very Large Service Providers based in Asia and Rest of the World

- 8.4.1. Big Data in Healthcare Service Providers based in North America

9. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN NORTH AMERICA

- 9.1. Chapter Overview

- 9.2. Detailed Company Profiles of Leading Players in North America

- 9.2.1. Amazon Web Services

- 9.2.1.1. Company Overview

- 9.2.1.2. Financial Information

- 9.2.1.3. Big Data Offerings and Capabilities

- 9.2.1.4. Recent Developments and Future Outlook

- 9.2.2. Microsoft

- 9.2.2.1. Company Overview

- 9.2.2.2. Financial Information

- 9.2.2.3. Big Data Offerings and Capabilities

- 9.2.2.4. Recent Developments and Future Outlook

- 9.2.3. Oracle

- 9.2.3.1. Company Overview

- 9.2.3.2. Financial Information

- 9.2.3.3. Big Data Offerings and Capabilities

- 9.2.3.4. Recent Developments and Future Outlook

- 9.2.4. Teradata

- 9.2.4.1. Company Overview

- 9.2.4.2. Financial Information

- 9.2.4.3. Big Data Offerings and Capabilities

- 9.2.4.4. Recent Developments and Future Outlook

- 9.2.1. Amazon Web Services

- 9.3. Short Company Profiles of Other Prominent Players in North America

- 9.3.1. Itransition

- 9.3.1.1. Company Overview

- 9.3.1.2. Big Data Offerings and Capabilities

- 9.3.2 Nous Infosystems

- 9.3.2.1. Company Overview

- 9.3.2.2. Big Data Offerings and Capabilities

- 9.3.3 Oxagile

- 9.3.3.1. Company Overview

- 9.3.3.2. Big Data Offerings and Capabilities

- 9.3.4 Softweb Solutions

- 9.3.4.1. Company Overview

- 9.3.4.2. Big Data Offerings and Capabilities

- 9.3.5 Solix Technologies

- 9.3.5.1. Company Overview

- 9.3.5.2. Big Data Offerings and Capabilities

- 9.3.6 Trianz (formerly CBIG Consulting)

- 9.3.6.1. Company Overview

- 9.3.6.2. Big Data Offerings and Capabilities

- 9.3.1. Itransition

10. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN EUROPE

- 10.1. Chapter Overview

- 10.2. Detailed Company Profiles of Leading Players in Europe

- 10.2.1. Accenture

- 10.2.1.1. Company Overview

- 10.2.1.2. Financial Information

- 10.2.1.3. Big Data Offerings and Capabilities

- 10.2.1.4. Recent Developments and Future Outlook

- 10.2.2. Keyrus

- 10.2.2.1. Company Overview

- 10.2.2.2. Financial Information

- 10.2.2.3. Big Data Offerings and Capabilities

- 10.2.2.4. Recent Developments and Future Outlook

- 10.2.1. Accenture

- 10.3. Short Company Profiles of Other Prominent Players in Europe

- 10.3.1. Akka Technologies

- 10.3.1.1. Company Overview

- 10.3.1.2. Big Data Offerings and Capabilities

- 10.3.2 Altamira.ai

- 10.3.2.1. Company Overview

- 10.3.2.2. Big Data Offerings and Capabilities

- 10.3.3 atom Consultancy Services (ACS)

- 10.3.3.1. Company Overview

- 10.3.3.2. Big Data Offerings and Capabilities

- 10.3.4 Avenga

- 10.3.4.1. Company Overview

- 10.3.4.2. Big Data Offerings and Capabilities

- 10.3.5 Lutech

- 10.3.5.1. Company Overview

- 10.3.5.2. Big Data Offerings and Capabilities

- 10.3.6 Nagarro

- 10.3.6.1. Company Overview

- 10.3.6.2. Big Data Offerings and Capabilities

- 10.3.7 Scalefocus

- 10.3.7.1. Company Overview

- 10.3.7.2. Big Data Offerings and Capabilities

- 10.3.8 Spindox

- 10.3.8.1. Company Overview

- 10.3.8.2. Big Data Offerings and Capabilities

- 10.3.1. Akka Technologies

11. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN ASIA AND REST OF THE WORLD

- 11.1. Chapter Overview

- 11.2. Detailed Company Profiles of Leading Players in Asia and Rest of the World

- 11.2.1. Tata Elxsi

- 11.2.1.1. Company Overview

- 11.2.1.2. Big Data Offerings and Capabilities

- 11.2.1.3. Recent Developments and Future Outlook

- 11.2.2. Kellton

- 11.2.2.1. Company Overview

- 11.2.2.2. Financial Information

- 11.2.2.3. Big Data Offerings and Capabilities

- 11.2.2.4. Recent Developments and Future Outlook

- 11.2.1. Tata Elxsi

- 11.3. Short Company Profiles of Other Prominent Players in Asia and Rest of the World

- 11.3.1. Athena Global Technologies

- 11.3.1.1. Company Overview

- 11.3.1.2. Big Data Offerings and Capabilities

- 11.3.2 Happiest Minds

- 11.3.2.1. Company Overview

- 11.3.2.2. Big Data Offerings and Capabilities

- 11.3.3 InData Labs

- 11.3.3.1. Company Overview

- 11.3.3.2. Big Data Offerings and Capabilities

- 11.3.4 NTT data

- 11.3.4.1. Company Overview

- 11.3.4.2. Big Data Offerings and Capabilities

- 11.3.5 OrangeMantra

- 11.3.5.1. Company Overview

- 11.3.5.2. Big Data Offerings and Capabilities

- 11.3.6 Trigyn Technologies

- 11.3.6.1. Company Overview

- 11.3.6.2. Big Data Offerings and Capabilities

- 11.3.7 XenonStack

- 11.3.7.1. Company Overview

- 11.3.7.2. Big Data Offerings and Capabilities

- 11.3.1. Athena Global Technologies

12. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 12.1. Chapter Overview

- 12.2. Market Drivers

- 12.3. Market Restraints

- 12.4. Market Opportunities

- 12.5. Market Challenges

- 12.6. Conclusion

13. GLOBAL BIG DATA IN HEALTHCARE MARKET

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Global Big Data in Healthcare Market, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 13.3.1. Scenario Analysis

- 13.3.1.1. Conservative Scenario

- 13.3.1.2. Optimistic Scenario

- 13.3.1. Scenario Analysis

- 13.4. Key Market Segmentations

14. BIG DATA IN HEALTHCARE MARKET, BY COMPONENT

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Big Data in Healthcare Market: Distribution by Component

- 14.3.1. Big Data Hardware: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.3.2. Big Data Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.3.3. Big Data Services: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.4. Data Triangulation and Validation

15. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF HARDWARE

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Big Data in Healthcare Market: Distribution by Type of Hardware

- 15.3.1. Storage Devices: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.3.2. Servers: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.3.3. Networking Infrastructure: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.4. Data Triangulation and Validation

16. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF SOFTWARE

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Big Data in Healthcare Market: Distribution by Type of Software

- 16.3.1. Electronic Health Record: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.2. Revenue Cycle Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.3. Practice Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.4. Workforce Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.4. Data Triangulation and Validation

17. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF SERVICE

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Big Data in Healthcare Market: Distribution by Type of Services

- 17.3.1. Diagnostic Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.2. Descriptive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.3. Predictive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.4. Prescriptive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.4. Data Triangulation and Validation

18. BIG DATA IN HEALTHCARE MARKET, BY DEPLOYMENT OPTION

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Big Data in Healthcare Market: Distribution by Deployment Option

- 18.3.1. Cloud-based Deployment: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.3.2. On-premises Deployment: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.4. Data Triangulation and Validation

19. BIG DATA IN HEALTHCARE MARKET, BY APPLICATION AREA

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Big Data in Healthcare Market: Distribution by Application Area

- 19.3.1. Operational Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.2. Clinical Data Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.3. Financial Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.4. Population Health Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.4. Data Triangulation and Validation

20. BIG DATA IN HEALTHCARE MARKET, BY HEALTHCARE VERTICAL

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Big Data in Healthcare Market: Distribution by Healthcare Vertical

- 20.3.1. Healthcare Services: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.2. Pharmaceuticals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.3. Medical Devices: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.4. Other Verticals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.4. Data Triangulation and Validation

21. BIG DATA IN HEALTHCARE MARKET, BY END USER

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Big Data in Healthcare Market: Distribution by End User

- 21.3.1. Hospitals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.2. Health Insurance Agencies: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.3. Clinics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.4. Other End Users: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.4. Data Triangulation and Validation

22. BIG DATA IN HEALTHCARE MARKET, BY ECONOMIC STATUS

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Big Data in Healthcare Market: Distribution by Economic Status

- 22.3.1. High Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.1. US: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.2. Canada: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.3. Germany: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.4. UK: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.5. UAE: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.6. South Korea: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.7. France: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.8. Australia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.9. New Zealand: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.10. Italy: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.11. Saudi Arabia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.12. Nordic Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2. Upper-Middle Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.1. China: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.2. Russia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.3. Brazil: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.4. Japan: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.5. South Africa: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.3. Lower-Middle Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.3.1. India: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1. High Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.4. Data Triangulation and Validation

23. BIG DATA IN HEALTHCARE MARKET, BY GEOGRAPHY

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Big Data in Healthcare Market: Distribution by Geography

- 23.3.1. North America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.2. Europe: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.3. Asia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.4. Middle East and North Africa: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.5. Latin America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.6. Rest of the World: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.4. Data Triangulation and Validation

24. BIG DATA IN HEALTHCARE MARKET, REVENUE FORECAST OF LEADING PLAYERS

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Microsoft: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.4. Optum: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.5. IBM: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.6. Oracle: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.7. Allscripts: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

25. CONCLUSION

- 25.1. Chapter Overview

26. EXECUTIVE INSIGHTS

- 26.1. Chapter Overview

- 26.2. Company A

- 26.2.1. Company Snapshot

- 26.2.2. Interview Transcript

- 26.3. Company B

- 26.3.1. Company Snapshot

- 26.3.2. Interview Transcript

- 26.4. Company C

- 26.4.1. Company Snapshot

- 26.4.2. Interview Transcript

- 26.5. Company D

- 26.5.1. Company Snapshot

- 26.5.2. Interview Transcrip

- 26.6. Company E

- 26.6.1. Company Snapshot

- 26.6.2. Interview Transcript

- 26.7. Company F

- 26.7.1. Company Snapshot

- 26.7.2. Interview Transcript

- 26.8. Company G

- 26.8.1. Company Snapshot

- 26.8.2. Interview Transcript

- 26.9. Company H

- 26.9.1. Company Snapshot

- 26.9.2. Interview Transcript

- 26.10. Company I

- 26.10.1. Company Snapshot

- 26.10.2. Interview Transcript

- 26.11. Company J

- 26.11.1. Company Snapshot

- 26.11.2. Interview Transcript

- 26.12. Company K

- 26.12.1. Company Snapshot

- 26.12.2. Interview Transcript

- 26.13. Company L

- 26.13.1. Company Snapshot

- 26.13.2. Interview Transcript

- 26.14. Company M

- 26.14.1. Company Snapshot

- 26.14.2. Interview Transcript

- 26.15. Company N

- 26.15.1. Company Snapshot

- 26.15.2. Interview Transcript

27. APPENDIX I: TABULATED DATA

28. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

- 発行日

- 発行

- Roots Analysis

- ページ情報

- 英文 331 Pages

- 納期

- 即日から翌営業日