|

|

市場調査レポート

商品コード

1121183

世界および中国のWEEE(電気電子廃棄物)リサイクル市場予測(2022年~2028年)Global and China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Report Forecast 2022-2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 世界および中国のWEEE(電気電子廃棄物)リサイクル市場予測(2022年~2028年) |

|

出版日: 2022年09月01日

発行: QYResearch

ページ情報: 英文 159 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

毎年、全世界で5,000万トン以上のE-wasteが発生しています。

その一部は埋立地に運ばれ、時間が経つにつれて有害な化学物質が溶出する可能性があります。また、E-wasteは発展途上国にも流れ、非公式のE-waste処理によって深刻な健康問題や公害問題が引き起こされる可能性があります。

2019年の世界のWEEEは5360万トン、回収・リサイクルの記録はわずか930万トン、回収率は17.4%、2021年の世界のWEEEは5740万トン、回収・リサイクルの記録はわずか930万トン、リサイクル率は1117万トン、20.13%、一人当たり7.5kgの廃棄電子製品が発生しています。

米国には、E-waste管理に関する国の法律はありませんが、25の州とコロンビア特別区が何らかの形で法律を制定しています。州法は、その範囲や影響、また消費者が電子製品を埋立地に廃棄することを禁止するかどうかなど、さまざまです。これらの法律を合わせると、米国人口の75-80%をカバーしていることになります。しかし、法律でカバーされている州を含む多くの地域では、範囲が異なるため、便利な回収方法が確立されていないのが現状です。カリフォルニア州とユタ州を除き、法律を導入しているすべての州では、拡大生産者責任(EPR)を採用しています。カナダは、連邦政府機関がこの権限を持っていないため、E-wasteを効果的に管理するための国内法がありません。しかし、カナダで最も人口の少ないヌナブト準州を除き、12の州と準州が業界管理計画を用いて規制を策定しています。平均して、製品の範囲は米国よりもはるかに広いです。カナダの多くの州では、EPRの遵守は、承認されたE-wasteコンプライアンス・プログラムに参加することで達成されます。ラテンアメリカでは、規制の動きは遅く、E-waste法を制定できた国はごくわずかです。ラテンアメリカでは、過去5年から10年の間に、特定のE-waste規制の実施にかなりの進展がありましたが、この進展は一部の国に限られており、その他の国にとっては、前途は非常に長いままとなっています。メキシコ、コスタリカ、コロンビア、ペルーは、この地域の環境に配慮したE-waste管理の主要な担い手となる可能性が高く、2020年までにすでに実施されているシステムの改善に取り組んでいますが、ブラジルとチリだけが正式なE-waste規制の枠組みの実施を開始するための基盤を構築しつつあります。ブラジルは最近、「家庭から見たWEEEリバース・ロジスティクス・システム実施のための部門別合意」を発表し、パブリックコメントを求めています。この協定は、2020年に正式に署名される予定です。2016年に廃棄物管理、拡大生産者責任、リサイクル促進枠組み法が制定されたことを受け、チリは現在、具体的なE-waste規制を策定中で、回収・リサイクル目標を盛り込み、正式な回収システム政策の実施に向けた指針を策定する予定です。コロンビアは、コンピュータ、プリンター、周辺機器からの廃棄物に関する政令第1512号を施行してから7年が経過し、E-wasteの分類をすべてのE-wasteカテゴリーに拡大するための新しい条例を策定し、E-waste統合管理のためにWEEE法第1672号とWEEE国家管理政策に従って確立した教訓と指針を考慮して、システムを調整しているところです。最初のE-waste管理システムの実施から5年を振り返り、ペルーはこの経験を非常に慎重に評価し、ギャップを埋め、国の一般廃棄物管理戦略に合致させることができるようにしています。改正規則は間もなく発表される予定で、小型および大型家電製品、特に冷却装置の回収が義務づけられ、E-wasteの分類範囲が拡大される予定です。

現在の統計によると、中国は世界最大のE-waste生産国であり、2019年には1,010トンのE-wasteが発生することが分かっています。中国が世界のEEE産業で重要な役割を担っているのは、主に2つの理由があります。中国は世界で最も人口の多い国であるため、EEEに対する国内需要が非常に高く、強力なEEE製造業を有していることです。さらに、中国はE-wasteの改修、再利用、リサイクルにおいて重要な役割を担っています。E-waste規制と施設拡張に牽引され、正式なE-wasteリサイクル産業は処理能力と品質で大きく前進し、毎年7000万台以上のE-wasteが解体されています(生態環境部、2019年度)。中国政府によると、実際の回収・リサイクル率は40%だが、この数字は5つのEEE製品のみであり、E-wasteの国際分類(付属書1)に記載されている54のEEE製品ではないことに注意する必要があります。(国際連合大学)。54製品すべてを考慮すると、回収・リサイクル率は15%に低下します。中国の新環境法による規制強化により、インフォーマルセクターは激減しています。固形廃棄物の輸入を禁止する政策により、E-wasteの不法輸入はより急速に消滅しています。しかし、資金のギャップは大きくなっています。税制と補助金は、E-wasteの資金調達政策に独特の課題をもたらしている(Zeng et al.、2017)。中国政府は、2025年までに、新しい電子製品の原材料の20%を再生材料から調達し、E-wasteの50%をリサイクルするという目標を掲げています(世界経済フォーラム2018)。2018年、台湾におけるE-wasteの回収・リサイクル率は、法規制対象製品の64%に達しており(37)、この大きな成果は、EPRの概念をリサイクルシステムに適用することに重点を置いた4in1リサイクルシステムに基づいています。リサイクル基金管理委員会(RFMB)の監督のもと、その仕組みは大きく改善されました。台湾には約20のE-wasteリサイクル施設があり、その生産能力は現在の国内E-waste発生量を上回っているため、台湾のE-wasteリサイクル事業は困難に直面しています。

また、南アフリカ、モロッコ、エジプト、ナミビア、ルワンダなどアフリカの一部の国には、E-wasteのリサイクル施設がありますが、これらの施設は大規模なインフォーマル産業と共存しています。そのため、これらのリサイクル業者の中には、新たな取り組みでパイロットや努力を動員して、処理量の前進・増加に努めているところもあります。一方、ナイジェリア、ケニア、ガーナといった規模の大きな国では、依然としてインフォーマル・リサイクルに大きく依存しています。ナイジェリアで行われた調査によると、2015年と2016年には、毎年約60,000~71,000トンの使用済みEEEがラゴスの2つの主要港を通じてナイジェリアに輸入されました。この調査によると、輸入される廃電子機器の多くは、ドイツ、英国、ベルギー、米国などの先進国から輸入されていることが判明しました。また、基本的な機能テストを行ったところ、平均して少なくとも19%の機器が正常に動作しないことが分かりました。

市場の分析と洞察

本レポートでは、世界と中国のWEEE(電気電子廃棄物)リサイクル市場に焦点を当て、その他の地域の地域レベル、郡レベルのセグメントデータもカバーしています。

世界のWEEE(電気電子廃棄物)リサイクル市場規模は、2022年の39億4079万米ドルから、レビュー期間中にCAGR 8.79%で推移し、2028年には65億3459万米ドルに達すると予測されています。2021年にWEEE(電気電子廃棄物)リサイクル世界市場の35%を占めた小型電気電子機器(小型家電、家電、懐中電灯、小型扇風機など)は、2028年には24億5897万米ドルとなり、COVID-19後の期間にCAGR9.89%で成長すると予測されています。金属製錬が主要セグメントで、2021年には81.74%以上の市場シェアを占め、この予測期間を通して9.03%のCAGRに変化しています。

中国のWEEE(電気電子廃棄物)リサイクル市場規模は、2021年の15億4198万米ドルから2028年には27億3962万米ドルに成長し、予測期間中のCAGRは8.72%と予測されています。

対象範囲と市場規模

WEEE(電気電子廃棄物)リサイクル市場は、地域・国レベル、プレイヤー別、タイプ別、用途別に分類されています。世界のWEEE(電気電子廃棄物)リサイクル市場におけるプレイヤー、利害関係者、その他の参加者は、本レポートを強力なリソースとして利用することで、優位に立つことができるようになることでしょう。セグメント別分析では、2017年から2028年までのタイプ別とアプリケーション別の収益と予測に焦点を当てます。

中国市場については、2017-2028年のWEEE(電気電子廃棄物)リサイクル市場規模を、プレイヤー別、タイプ別、用途別に集計しています。主要企業には、中国で重要な役割を担う世界プレイヤーとローカルプレイヤーを含んでいます。

目次

第1章 調査範囲

- WEEE(電気電子廃棄物)リサイクル製品イントロダクション

- 世界のWEEE(電気電子廃棄物)リサイクルの見通し(2017 VS 2022 VS 2028)

- 世界のWEEE(電気電子廃棄物)リサイクル市場規模(2017-2028)

- 中国のWEEE(電気電子廃棄物)リサイクル市場規模(2017-2028)

- WEEE(電気電子廃棄物)リサイクル市場規模:中国と世界の比較(2017 VS 2022 VS 2028)

- WEEE(電気電子廃棄物)リサイクル市場力学

- 業界の動向

- 市場抑制要因

- 調査目的

- 検討年数

第2章 タイプ:WEEE(電気電子廃棄物)リサイクル

- タイプ別:WEEE(電気電子廃棄物)リサイクル市場セグメント

- 熱交換器(冷蔵庫、冷凍庫、エアコン、除湿機、ヒートポンプなど)

- 一般家庭向けディスプレイ機器(モニター、テレビ、液晶画面、ノートパソコンなど)

- ランプ・グロー放電ランプ(蛍光灯、電球形蛍光灯、放電灯、LEDランプなど)

- 大型電子機器(家電、電熱器、ストーブ、換気扇)

- 小型電気・電子機器(小型家電、家電、懐中電灯、小型扇風機など)

- 小型IT・通信機器(携帯電話、GPSナビゲーションデバイス、電卓など)

- タイプ別:世界の市場規模(2017、2022、2028)

- タイプ別:世界の市場規模(2017-2028)

- タイプ別:中国の市場規模(2017、2022、2028)

- タイプ別:中国の市場規模(2017-2028)

第3章 用途別:WEEE(電気電子廃棄物)リサイクル

- 用途別:WEEE(電気電子廃棄物)リサイクル市場セグメント

- 環境保護

- 金属製錬

- 化学抽出

- エネルギー電力

- 用途別:世界の市場規模(2017、2022、2028)

- 用途別:世界の市場規模(2017-2028)

- 用途別:中国の市場規模(2017、2022、2028)

- 用途別:中国の市場規模(2017-2028)

第4章 企業別:世界のWEEE(電気電子廃棄物)リサイクルの競合情勢

- 企業別:市場規模

- 世界の集中率(CR)

- 世界のWEEEリサイクル企業本社、製品タイプ

- 企業別:中国の市場規模

第5章 地域別:世界のWEEE(電気電子廃棄物)リサイクル市場規模

- 地域別:世界の市場規模(2017 VS 2022 VS 2028)

- 地域別:世界の市場規模(2017-2028)

第6章 地域・国レベルのセグメント

- 北米

- 市場規模の前年比成長(2017-2028)

- 国別市場データ(2017、2022、2028)

- 米国

- カナダ

- アジア太平洋

- 市場規模の前年比成長(2017-2028)

- 地域別市場データ(2017、2022、2028)

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- 東南アジア

- 欧州

- 市場規模の前年比成長(2017-2028)

- 国別市場データ(2017、2022、2028)

- ドイツ

- フランス

- 英国

- ベルギー

- スウェーデン

- ラテンアメリカ

- 市場規模の前年比成長(2017-2028)

- 国別市場データ(2017、2022、2028)

- メキシコ

- ブラジル

- 中東とアフリカ

- 市場規模の前年比成長(2017-2028)

- 国別市場データ(2017、2022、2028)

- トルコ

- サウジアラビア

- アラブ首長国連邦

第7章 主要企業のプロファイル

- China Resources and Environment

- Boliden AB

- Veolia

- GEM

- Umicore

- Stena Metall

- Gree Electric

- Sound Environmental Resour

- Galloo NV

- SIMS Metals

- TCL

- Electronic Recyclers International(ERI)

- Capital Environment Holdings

- Alba AG

- Aurubis

- Coolrec BV

- Environnement Recycling

- Ecoreset

- Hwaxin Environmental

- E-Reciklaza

第8章 調査結果と結論

第9章 付録

LIST OF TABLES

- Table 1. WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size, China VS Global, CAGR (2017 VS 2022 VS 2028)

- Table 2. WEEE (Waste Electrical and Electronic Equipment) Recycling Market Trends

- Table 3. WEEE (Waste Electrical and Electronic Equipment) Recycling Market Restraints

- Table 4. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type: 2017 VS 2022 VS 2028 (US$ Million)

- Table 5. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type: 2017 VS 2022 VS 2028 (US$ Million)

- Table 6. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Application: 2017 VS 2022 VS 2028 (US$ Million)

- Table 7. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Application: 2017 VS 2022 VS 2028 (US$ Million)

- Table 8. Top WEEE (Waste Electrical and Electronic Equipment) Recycling Companies in Global Market, Ranking by Revenue (2021)

- Table 9. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Revenue by Player, (US$ Million), 2017-2022

- Table 10. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Revenue Share by Player, 2017-2022

- Table 11. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Companies Market Concentration Ratio (CR5 and HHI)

- Table 12. Global WEEE (Waste Electrical and Electronic Equipment) Recycling by Company Type (Tier 1, Tier 2, and Tier 3) & (based on the Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling as of 2021)

- Table 13. Top Players of WEEE (Waste Electrical and Electronic Equipment) Recycling in Global Market, Headquarters and Area Served

- Table 14. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Companies Product Type

- Table 15. Established Date of International Companies

- Table 16. Top WEEE (Waste Electrical and Electronic Equipment) Recycling Players in China Market, Ranking by Revenue (2021)

- Table 17. China WEEE (Waste Electrical and Electronic Equipment) Recycling Revenue by Players, (US$ Million), 2020, 2021 & 2022

- Table 18. China WEEE (Waste Electrical and Electronic Equipment) Recycling Revenue Share by Players, 2020, 2021 & 2022

- Table 19. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region (US$ Million): 2017 VS 2022 VS 2028

- Table 20. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region (2017-2022) & (US$ Million)

- Table 21. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Forecast by Region (2023-2028) & (US$ Million)

- Table 22. North America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Country (2017-2028) & (US$ Million)

- Table 23. Asia-Pacific WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region (2017-2028) & (US$ Million)

- Table 24. Europe WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Country (2017-2028) & (US$ Million)

- Table 25. Latin America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Country (2017-2028) & (US$ Million)

- Table 26. Middle East and Africa WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Country (2017-2028) & (US$ Million)

- Table 27. China Resources and Environment Company Details

- Table 28. China Resources and Environment Business Overview

- Table 29. China Resources and Environment WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 30. China Resources and Environment Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 31. Boliden AB Company Details

- Table 32. Boliden AB Business Overview

- Table 33. Boliden AB WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 34. Boliden AB Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 35. Boliden AB Recent Development

- Table 36. Veolia Company Details

- Table 37. Veolia Business Overview

- Table 38. Veolia WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 39. Veolia Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 40. Veolia Recent Development

- Table 41. GEM Company Details

- Table 42. GEM Business Overview

- Table 43. GEM WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 44. GEM Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 45. Umicore Company Details

- Table 46. Umicore Business Overview

- Table 47. Umicore WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 48. Umicore Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 49. Stena Metall Company Details

- Table 50. Stena Metall Business Overview

- Table 51. Stena Metall WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 52. Stena Metall Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 53. Stena Metall Recent Development

- Table 54. Gree Electric Company Details

- Table 55. Gree Electric Business Overview

- Table 56. Gree Electric WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 57. Gree Electric Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 58. Sound Environmental Resour Company Details

- Table 59. Sound Environmental Resour Business Overview

- Table 60. Sound Environmental Resour WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 61. Sound Environmental Resour Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 62. Galloo N.V. Company Details

- Table 63. Galloo N.V. Business Overview

- Table 64. Galloo N.V. WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 65. Galloo N.V. Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 66. Galloo N.V. Recent Development

- Table 67. SIMS Metals Company Details

- Table 68. SIMS Metals Business Overview

- Table 69. SIMS Metals WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 70. SIMS Metals Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 71. SIMS Metals Recent Development

- Table 72. TCL Company Details

- Table 73. TCL Business Overview

- Table 74. TCL WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 75. TCL Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 76. Electronic Recyclers International (ERI) Company Details

- Table 77. Electronic Recyclers International (ERI) Business Overview

- Table 78. Electronic Recyclers International (ERI) WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 79. Electronic Recyclers International (ERI) Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 80. Capital Environment Holdings Company Details

- Table 81. Capital Environment Holdings Business Overview

- Table 82. Capital Environment Holdings WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 83. Capital Environment Holdings Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 84. Alba AG Company Details

- Table 85. Alba AG Business Overview

- Table 86. Alba AG WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 87. Alba AG Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 88. Alba AG Recent Development

- Table 89. Aurubis Company Details

- Table 90. Aurubis Business Overview

- Table 91. Aurubis WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 92. Aurubis Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 93. Aurubis Recent Development

- Table 94. Coolrec B.V. Company Details

- Table 95. Coolrec B.V. Business Overview

- Table 96. Coolrec B.V. WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 97. Coolrec B.V. Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 98. Coolrec B.V. Recent Development

- Table 99. Environnement Recycling Company Details

- Table 100. Environnement Recycling Business Overview

- Table 101. Environnement Recycling WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 102. Environnement Recycling Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 103. Ecoreset Company Details

- Table 104. Ecoreset Business Overview

- Table 105. Ecoreset WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 106. Ecoreset Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 107. Ecoreset Recent Development

- Table 108. Hwaxin Environmental Company Details

- Table 109. Hwaxin Environmental Business Overview

- Table 110. Hwaxin Environmental WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 111. Hwaxin Environmental Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 112. E-Reciklaza Company Details

- Table 113. E-Reciklaza Business Overview

- Table 114. E-Reciklaza WEEE (Waste Electrical and Electronic Equipment) Recycling Product

- Table 115. E-Reciklaza Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022) & (US$ Million)

- Table 116. Research Programs/Design for This Report

- Table 117. Key Data Information from Secondary Sources

- Table 118. Key Data Information from Primary Sources

List of Figures

- Figure 1. WEEE (Waste Electrical and Electronic Equipment) Recycling Product Picture

- Figure 2. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size, (US$ Million), 2017 VS 2022 VS 2028

- Figure 3. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size 2017-2028 (US$ Million)

- Figure 4. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size, (US$ Million), 2017 VS 2022 VS 2028

- Figure 5. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size 2017-2028 (US$ Million)

- Figure 6. WEEE (Waste Electrical and Electronic Equipment) Recycling Report Years Considered

- Figure 7. Product Picture of Heat Exchangers (Refrigerator, Freezer, Air Conditioner, Dehumidifier, Heat Pump, etc.)

- Figure 8. Product Picture of Display Devices for Use in Private Households (Monitors, TVs, LCD Screens, Notebook Computers, etc.)

- Figure 9. Product Picture of Lamps/Glow-Discharge Lamps (Fluorescent Lamps, Compact Fluorescent Lamps, Discharge Lamps, LED Lamps, etc.)

- Figure 10. Product Picture of Large Electronic Devices (Household Appliances, Electric Heaters, Stoves, Ventilators)

- Figure 11. Product Picture of Small Electrical and Electronic Devices (Small Household Appliances, Consumer Electronics, Flashlights, Small Fans, etc.)

- Figure 12. Product Picture of Small IT and Telecommunication Devices (Mobile Phones, GPS Navigation Devices, Calculators, etc.)

- Figure 13. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Type in 2022 & 2028

- Figure 14. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type (2017-2028) & (US$ Million)

- Figure 15. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Type (2017-2028)

- Figure 16. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Type in 2022 & 2028

- Figure 17. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type (2017-2028) & (US$ Million)

- Figure 18. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Type (2017-2028)

- Figure 19. Product Picture of Environmental Protection

- Figure 20. Product Picture of Metal Smelting

- Figure 21. Product Picture of Chemical Extraction

- Figure 22. Product Picture of Energy Power

- Figure 23. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Application in 2022 & 2028

- Figure 24. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Application (2017-2028) & (US$ Million)

- Figure 25. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Application (2017-2028)

- Figure 26. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Application in 2022 & 2028

- Figure 27. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Application (2017-2028) & (US$ Million)

- Figure 28. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Application (2017-2028)

- Figure 29. The Top 5 and 10 Largest Companies of WEEE (Waste Electrical and Electronic Equipment) Recycling in the World: Market Share by WEEE (Waste Electrical and Electronic Equipment) Recycling Revenue in 2021

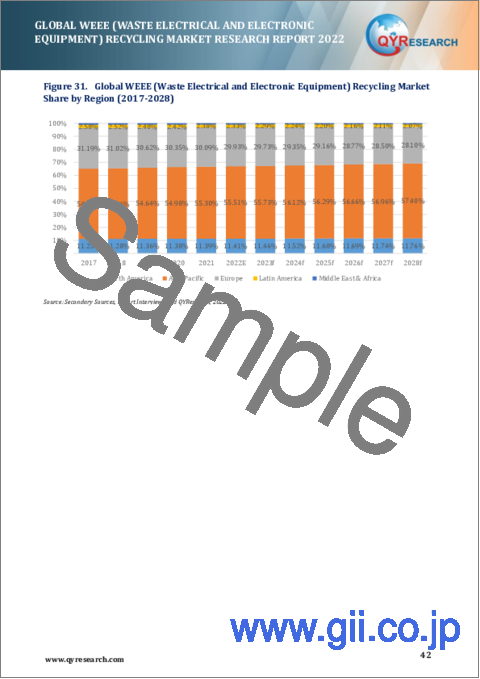

- Figure 30. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Market Share by Region: 2017 VS 2022 VS 2028

- Figure 31. Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Region (2017-2028)

- Figure 32. North America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate 2017-2028 (US$ Million)

- Figure 33. U.S. WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 34. Canada WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 35. Asia-Pacific WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate 2017-2028 (US$ Million)

- Figure 36. China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 37. Japan WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 38. South Korea WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 39. India WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 40. Australia WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 41. Southeast Asia WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 42. Europe WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate 2017-2028 (US$ Million)

- Figure 43. Germany WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 44. France WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 45. U.K. WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 46. Belgium WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 47. Sweden WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 48. Latin America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate 2017-2028 (US$ Million)

- Figure 49. Mexico WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 50. Brazil WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 51. Middle East and Africa WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate 2017-2028 (US$ Million)

- Figure 52. Turkey WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 53. Saudi Arabia WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 54. UAE WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size Growth Rate (2017-2028) & (US$ Million)

- Figure 55. China Resources and Environment Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 56. Boliden AB Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 57. Veolia Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 58. GEM Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 59. Umicore Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 60. Stena Metall Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 61. Gree Electric Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 62. Sound Environmental Resour Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 63. Galloo N.V. Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 64. SIMS Metals Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 65. TCL Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 66. Electronic Recyclers International (ERI) Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 67. Capital Environment Holdings Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 68. Alba AG Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 69. Aurubis Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 70. Coolrec B.V. Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 71. Environnement Recycling Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 72. Ecoreset Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 73. Hwaxin Environmental Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 74. E-Reciklaza Revenue Growth Rate in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- Figure 75. Bottom-up and Top-down Approaches for This Report

- Figure 76. Data Triangulation

- Figure 77. Key Executives Interviewed 134

More than 50 million tons of e-waste are generated globally every year. Some of it ends up in landfills, where toxic chemicals can leach out over time. E-waste can also flow to developing countries, where informal e-waste disposal can cause serious health and pollution problems.

In 2019, global WEEE was 53.6 million tons, with only 9.3 million tons of recorded collection and recycling, a recovery rate of 17.4%, compared with 57.4 million tons of global WEEE in 2021, with only 9.3 million tons of recorded collection and recycling 11.17 million tons, the recycling rate is 20.13%, and 7.5 kg of waste electronic products are produced per capita.

The United States has no national legislation on e-waste management, but 25 states and the District of Columbia have enacted some form of legislation. State laws vary in scope and impact, as well as in whether to prohibit consumers from disposing of electronic products in landfills. Collectively, these laws cover 75-80% of the U.S. population. However, many areas of the country, including the states covered by law, do not have convenient collection methods due to varying scope. Except for California and Utah, all states that have implemented laws use Extended Producer Responsibility (EPR). Canada does not have national legislation to effectively manage e-waste because federal agencies do not have this authority. However, 12 provinces and territories have developed regulations using industry management plans, with the exception of Nunavut, Canada's least populous territory. On average, the product range is much wider than in the United States; in many Canadian provinces, compliance with the EPR can be achieved by joining an approved e-waste compliance program. Regulation in Latin America has moved slowly, with only a few countries managing to establish e-waste laws. Although Latin America has made considerable progress in implementing specific e-waste regulations over the past 5-10 years, this progress has been limited to a few countries, while for others the road ahead remains very long. With the exception of Mexico, Costa Rica, Colombia and Peru, which are likely to be the leading players in the region's environmentally sound e-waste management and are committed to improving the systems already in place in 2020, only Brazil and Chile are building the foundations from which to begin implementing formal E-waste regulatory framework. Brazil recently published the "Sectoral Agreement for the Implementation of the WEEE Reverse Logistics System from a Household Perspective" for public comment. The agreement is expected to be formally signed in 2020. Following the enactment of the Waste Management, Extended Producer Responsibility and Promotion of Recycling Framework Law in 2016, Chile is currently developing specific e-waste regulations, which will include collection and recycling targets and develop guidance for the implementation of a formal collection system policy. Seven years after implementing Decree No. 1512 on waste from computers, printers and peripherals, Colombia is developing a new ordinance to expand e-waste classification to all e-waste categories and for integrated e-waste management The system is adjusted, taking into account lessons learned and guidelines established in accordance with WEEE Law No. 1672 and the WEEE National Management Policy. Looking back on the five years since the implementation of the first e-waste management system, Peru has been evaluating this experience very carefully so that it can fill the gaps and align with the country's general waste management strategy. The revised regulations are expected to be published soon and will expand the scope of e-waste categories with mandatory collection of small and large household appliances, especially cooling equipment.

Current statistics show that China is the largest e-waste producer in the world, generating 1,010 tons of e-waste in 2019. China plays a key role in the global EEE industry for two main reasons: China is the most populous country in the world, so domestic demand for EEE is very high, and it has a strong EEE manufacturing industry. In addition, China plays an important role in the refurbishment, reuse and recycling of e-waste. Driven by e-waste regulation and facility expansion, the formal e-waste recycling industry has made great strides in processing capacity and quality; more than 70 million e-waste units are dismantled each year (Ministry of Ecology and Environment, 2019 year). According to the Chinese government, the actual collection and recycling rate is 40%, but it is important to note that this figure is only for 5 EEE products, not the 54 EEE products listed in the International Classification of Electronic Waste (Annex 1). (United Nations University - Keys). If all 54 products are taken into account, the collection and recycling rate drops to 15%. The informal sector has been in sharp decline due to tighter controls imposed by China's new environmental law. Illegal imports of e-waste are disappearing more rapidly due to the policy of banning the import of solid waste. However, the funding gap is growing. Taxation and subsidies present unique challenges to e-waste funding policies (Zeng et al., 2017). The Chinese government has set a target that, by 2025, 20% of the raw materials for new electronic products will be sourced from recycled materials and 50% of electronic waste will be recycled (World Economic Forum 2018). In 2018, the collection and recycling rate of e-waste in Taiwan Province of China reached 64% of products covered by legislation (37); this significant achievement is based on a 4-in-1 recycling system that focuses on applying the EPR concept to recycling systems. Under the supervision of the Recycling Fund Management Board (RFMB), the mechanism has been greatly improved. There are about 20 e-waste recycling facilities in Taiwan Province of China, and their production capacity is higher than the current domestic e-waste generation, so the e-waste recycling business in Taiwan Province of China is facing challenges.

And few countries in Africa, such as South Africa, Morocco, Egypt, Namibia and Rwanda, have some e-waste recycling facilities, but these facilities coexist with large informal industries. As a result, some of these recycling companies have been working hard to advance and increase their processing volumes, mobilizing new pilots and efforts through new initiatives. On the other hand, sizable countries such as Nigeria, Kenya and Ghana still rely heavily on informal recycling. A study conducted in Nigeria showed that in 2015 and 2016, around 60,000-71,000 tonnes of used EEE were imported into Nigeria through the two main ports of Lagos each year. The survey found that most of the imported waste electronic waste comes from developed countries, such as Germany, the United Kingdom, Belgium, and the United States. In addition, a basic functional test showed that, on average, at least 19% of the devices did not work properly.

Market Analysis and Insights:

This report focuses on global and China WEEE (Waste Electrical and Electronic Equipment) Recycling market, also covers the segmentation data of other regions in regional level and county level.

Due to the COVID-19 pandemic, the global WEEE (Waste Electrical and Electronic Equipment) Recycling market size is estimated to be worth US$ 3,940.79 million in 2022 and is forecast to a readjusted size of US$ 6,534.59 million by 2028 with a CAGR of 8.79% during the review period. Fully considering the economic change by this health crisis, Small Electrical and Electronic Devices (Small Household Appliances, Consumer Electronics, Flashlights, Small Fans, etc.) accounting for 35% of the WEEE (Waste Electrical and Electronic Equipment) Recycling global market in 2021, is projected to value US$ 2,458.97 million by 2028, growing at a revised 9.89% CAGR in the post-COVID-19 period. While Metal Smelting was the leading segment, accounting for over 81.74 percent market share in 2021, and altered to an 9.03 % CAGR throughout this forecast period.

In China the WEEE (Waste Electrical and Electronic Equipment) Recycling market size is expected to grow from US$ 1,541.98 million in 2021 to US$ 2,739.62 million by 2028, at a CAGR of 8.72% during the forecast period.

Scope and Market Size:

WEEE (Waste Electrical and Electronic Equipment) Recycling market is segmented in regional and country level, by players, by Type, and by Application. Players, stakeholders, and other participants in the global WEEE (Waste Electrical and Electronic Equipment) Recycling market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on revenue and forecast by Type and by Application for the period 2017-2028.

For China market, this report focuses on the WEEE (Waste Electrical and Electronic Equipment) Recycling market size by players, by Type, and by Application, for the period 2017-2028. The key players include the global and local players which play important roles in China.

By Company

- China Resources and Environment

- Boliden AB

- Veolia

- GEM

- Umicore

- Stena Metall

- Gree Electric

- Sound Environmental Resour

- Galloo N.V.

- SIMS Metals

- TCL

- Electronic Recyclers International (ERI)

- Capital Environment Holdings

- Alba AG

- Aurubis

- Coolrec B.V.

- Environnement Recycling

- Ecoreset

- Hwaxin Environmental

- E-Reciklaza

Segment by Type

- Heat Exchangers (Refrigerator, Freezer, Air Conditioner, Dehumidifier, Heat Pump, etc.)

- Display Devices for Use in Private Households (Monitors, TVs, LCD Screens, Notebook Computers, etc.)

- Lamps/Glow-Discharge Lamps (Fluorescent Lamps, Compact Fluorescent Lamps, Discharge Lamps, LED Lamps, etc.)

- Large Electronic Devices (Household Appliances, Electric Heaters, Stoves, Ventilators)

- Small Electrical and Electronic Devices (Small Household Appliances, Consumer Electronics, Flashlights, Small Fans, etc.)

- Small IT and Telecommunication Devices (Mobile Phones, GPS Navigation Devices, Calculators, etc.)

Segment by Application

- Environmental Protection

- Metal Smelting

- Chemical Extraction

- Energy Power

By Region

- North America

- U.S.

- Canada

- Asia-Pacific

- China

- Japan

- South Korea

- Southeast Asia

- India

- Australia

- Europe

- Germany

- France

- U.K.

- Belgium

- Sweden

- Latin America

- Mexico

- Brazil

- Middle East & Africa

- Turkey

- Saudi Arabia

- UAE

TABLE OF CONTENTS

1 Study Coverage

- 1.1 WEEE (Waste Electrical and Electronic Equipment) Recycling Product Introduction

- 1.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Outlook, 2017 VS 2022 VS 2028

- 1.2.1 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size for the Year 2017-2028

- 1.2.2 China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size for the Year 2017-2028

- 1.3 WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size, China VS Global, 2017 VS 2022 VS 2028

- 1.4 WEEE (Waste Electrical and Electronic Equipment) Recycling Market Dynamics

- 1.4.1 WEEE (Waste Electrical and Electronic Equipment) Recycling Industry Trends

- 1.4.2 WEEE (Waste Electrical and Electronic Equipment) Recycling Market Restraints

- 1.5 Study Objectives

- 1.6 Years Considered

2 WEEE (Waste Electrical and Electronic Equipment) Recycling by Type

- 2.1 WEEE (Waste Electrical and Electronic Equipment) Recycling Market Segment by Type

- 2.1.1 Heat Exchangers (Refrigerator, Freezer, Air Conditioner, Dehumidifier, Heat Pump, etc.)

- 2.1.2 Display Devices for Use in Private Households (Monitors, TVs, LCD Screens, Notebook Computers, etc.)

- 2.1.3 Lamps/Glow-Discharge Lamps (Fluorescent Lamps, Compact Fluorescent Lamps, Discharge Lamps, LED Lamps, etc.)

- 2.1.4 Large Electronic Devices (Household Appliances, Electric Heaters, Stoves, Ventilators)

- 2.1.5 Small Electrical and Electronic Devices (Small Household Appliances, Consumer Electronics, Flashlights, Small Fans, etc.)

- 2.1.6 Small IT and Telecommunication Devices (Mobile Phones, GPS Navigation Devices, Calculators, etc.)

- 2.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type (2017, 2022 & 2028)

- 2.3 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type (2017-2028)

- 2.4 China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type (2017, 2022 & 2028)

- 2.5 China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Type (2017-2028)

3 WEEE (Waste Electrical and Electronic Equipment) Recycling by Application

- 3.1 WEEE (Waste Electrical and Electronic Equipment) Recycling Market Segment by Application

- 3.1.1 Environmental Protection

- 3.1.2 Metal Smelting

- 3.1.3 Chemical Extraction

- 3.1.4 Energy Power

- 3.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size, by Application (2017, 2022 & 2028)

- 3.3 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Application (2017-2028)

- 3.4 China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Application (2017, 2022 & 2028)

- 3.5 China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Application (2017-2028)

4 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Competitor Landscape by Company

- 4.1 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Company

- 4.1.1 Top Global WEEE (Waste Electrical and Electronic Equipment) Recycling Companies Ranked by Revenue (2021)

- 4.1.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Revenue by Player (2017-2022)

- 4.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Concentration Ratio (CR)

- 4.2.1 WEEE (Waste Electrical and Electronic Equipment) Recycling Market Concentration Ratio (CR) (2017-2022)

- 4.2.2 Global Top 5 and Top 10 Largest Companies of WEEE (Waste Electrical and Electronic Equipment) Recycling in 2021

- 4.2.3 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Share by Company Type (Tier 1, Tier 2, and Tier 3)

- 4.3 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Headquarters, Product Type

- 4.3.1 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Headquarters and Area Served

- 4.3.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Companies Product Type

- 4.3.3 Established Date of International Companies

- 4.4 China WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Company

- 4.4.1 Top WEEE (Waste Electrical and Electronic Equipment) Recycling Players in China, Ranked by Revenue (2021)

- 4.4.2 China WEEE (Waste Electrical and Electronic Equipment) Recycling Revenue by Players (2020, 2021 & 2022)

5 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region

- 5.1 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region: 2017 VS 2022 VS 2028

- 5.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region (2017-2028)

- 5.2.1 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region: 2017-2022

- 5.2.2 Global WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size by Region: 2023-2028

6 Segment in Regional Level & Country Level

- 6.1 North America

- 6.1.1 North America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size YoY Growth 2017-2028

- 6.1.2 North America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Facts & Figures by Country (2017, 2022 & 2028)

- 6.1.3 U.S.

- 6.1.4 Canada

- 6.2 Asia-Pacific

- 6.2.1 Asia-Pacific WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size YoY Growth 2017-2028

- 6.2.2 Asia-Pacific WEEE (Waste Electrical and Electronic Equipment) Recycling Market Facts & Figures by Region (2017, 2022 & 2028)

- 6.2.3 China

- 6.2.4 Japan

- 6.2.5 South Korea

- 6.2.6 India

- 6.2.7 Australia

- 6.2.8 Southeast Asia

- 6.3 Europe

- 6.3.1 Europe WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size YoY Growth 2017-2028

- 6.3.2 Europe WEEE (Waste Electrical and Electronic Equipment) Recycling Market Facts & Figures by Country (2017, 2022 & 2028)

- 6.3.3 Germany

- 6.3.4 France

- 6.3.5 U.K.

- 6.3.6 Belgium

- 6.3.7 Sweden

- 6.4 Latin America

- 6.4.1 Latin America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size YoY Growth 2017-2028

- 6.4.2 Latin America WEEE (Waste Electrical and Electronic Equipment) Recycling Market Facts & Figures by Country (2017, 2022 & 2028)

- 6.4.3 Mexico

- 6.4.4 Brazil

- 6.5 Middle East and Africa

- 6.5.1 Middle East and Africa WEEE (Waste Electrical and Electronic Equipment) Recycling Market Size YoY Growth 2017-2028

- 6.5.2 Middle East and Africa WEEE (Waste Electrical and Electronic Equipment) Recycling Market Facts & Figures by Country (2017, 2022 & 2028)

- 6.5.3 Turkey

- 6.5.4 Saudi Arabia

- 6.5.5 UAE

7 Key Players Profiles

- 7.1 China Resources and Environment

- 7.1.1 China Resources and Environment Company Details

- 7.1.2 China Resources and Environment Business Overview

- 7.1.3 China Resources and Environment WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.1.4 China Resources and Environment Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.2 Boliden AB

- 7.2.1 Boliden AB Company Details

- 7.2.2 Boliden AB Business Overview

- 7.2.3 Boliden AB WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.2.4 Boliden AB Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.2.5 Boliden AB Recent Development

- 7.3 Veolia

- 7.3.1 Veolia Company Details

- 7.3.2 Veolia Business Overview

- 7.3.3 Veolia WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.3.4 Veolia Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.3.5 Veolia Recent Development

- 7.4 GEM

- 7.4.1 GEM Company Details

- 7.4.2 GEM Business Overview

- 7.4.3 GEM WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.4.4 GEM Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.5 Umicore

- 7.5.1 Umicore Company Details

- 7.5.2 Umicore Business Overview

- 7.5.3 Umicore WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.5.4 Umicore Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.6 Stena Metall

- 7.6.1 Stena Metall Company Details

- 7.6.2 Stena Metall Business Overview

- 7.6.3 Stena Metall WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.6.4 Stena Metall Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.6.5 Stena Metall Recent Development

- 7.7 Gree Electric

- 7.7.1 Gree Electric Company Details

- 7.7.2 Gree Electric Business Overview

- 7.7.3 Gree Electric WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.7.4 Gree Electric Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.8 Sound Environmental Resour

- 7.8.1 Sound Environmental Resour Company Details

- 7.8.2 Sound Environmental Resour Business Overview

- 7.8.3 Sound Environmental Resour WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.8.4 Sound Environmental Resour Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.9 Galloo N.V.

- 7.9.1 Galloo N.V. Company Details

- 7.9.2 Galloo N.V. Business Overview

- 7.9.3 Galloo N.V. WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.9.4 Galloo N.V. Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.9.5 Galloo N.V. Recent Development

- 7.10 SIMS Metals

- 7.10.1 SIMS Metals Company Details

- 7.10.2 SIMS Metals Business Overview

- 7.10.3 SIMS Metals WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.10.4 SIMS Metals Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.10.5 SIMS Metals Recent Development

- 7.11 TCL

- 7.11.1 TCL Company Details

- 7.11.2 TCL Business Overview

- 7.11.3 TCL WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.11.4 TCL Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.12 Electronic Recyclers International (ERI)

- 7.12.1 Electronic Recyclers International (ERI) Company Details

- 7.12.2 Electronic Recyclers International (ERI) Business Overview

- 7.12.3 Electronic Recyclers International (ERI) WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.12.4 Electronic Recyclers International (ERI) Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.13 Capital Environment Holdings

- 7.13.1 Capital Environment Holdings Company Details

- 7.13.2 Capital Environment Holdings Business Overview

- 7.13.3 Capital Environment Holdings WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.13.4 Capital Environment Holdings Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.14 Alba AG

- 7.14.1 Alba AG Company Details

- 7.14.2 Alba AG Business Overview

- 7.14.3 Alba AG WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.14.4 Alba AG Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.14.5 Alba AG Recent Development

- 7.15 Aurubis

- 7.15.1 Aurubis Company Details

- 7.15.2 Aurubis Business Overview

- 7.15.3 Aurubis WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.15.4 Aurubis Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.15.5 Aurubis Recent Development

- 7.16 Coolrec B.V.

- 7.16.1 Coolrec B.V. Company Details

- 7.16.2 Coolrec B.V. Business Overview

- 7.16.3 Coolrec B.V. WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.16.4 Coolrec B.V. Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.16.5 Coolrec B.V. Recent Development

- 7.17 Environnement Recycling

- 7.17.1 Environnement Recycling Company Details

- 7.17.2 Environnement Recycling Business Overview

- 7.17.3 Environnement Recycling WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.17.4 Environnement Recycling Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.18 Ecoreset

- 7.18.1 Ecoreset Company Details

- 7.18.2 Ecoreset Business Overview

- 7.18.3 Ecoreset WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.18.4 Ecoreset Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.18.5 Ecoreset Recent Development

- 7.19 Hwaxin Environmental

- 7.19.1 Hwaxin Environmental Company Details

- 7.19.2 Hwaxin Environmental Business Overview

- 7.19.3 Hwaxin Environmental WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.19.4 Hwaxin Environmental Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

- 7.20 E-Reciklaza

- 7.20.1 E-Reciklaza Company Details

- 7.20.2 E-Reciklaza Business Overview

- 7.20.3 E-Reciklaza WEEE (Waste Electrical and Electronic Equipment) Recycling Introduction

- 7.20.4 E-Reciklaza Revenue in WEEE (Waste Electrical and Electronic Equipment) Recycling Business (2017-2022)

8 Research Findings and Conclusion

9 Appendix

- 9.1 Research Methodology

- 9.1.1 Methodology/Research Approach

- 9.1.2 Data Source

- 9.2 Disclaimer

- 9.3 Author Details