|

市場調査レポート

商品コード

1644371

石油・ガス業界のMAC(主要オートメーション請負業者):市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Main Automation Contractor (MAC) In Oil & Gas Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 石油・ガス業界のMAC(主要オートメーション請負業者):市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

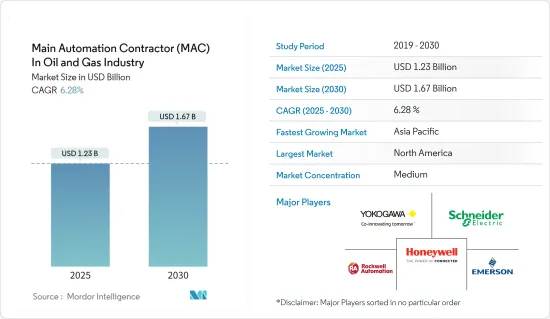

石油・ガス業界のMAC(主要オートメーション請負業者)は、予測期間(2025-2030年)にCAGR 6.28%で、2025年の12億3,000万米ドルから2030年には16億7,000万米ドルに成長すると予測されます。

主なハイライト

- 様々なエンドユーザー産業における石油・ガス需要の増大は、より高いプロセス効率と運用効率への要求とともに、機械化率と自動化ソリューションの導入率を著しく高め、調査市場の成長にプラスの影響を与えています。

- 今日の情報主導の石油生産環境では、自動化の範囲が拡大しており、生産現場の近くでより多くの情報処理を処理することが重要です。適切な生産・操業データは、石油生産システムとビジネス・システムの間をスムーズに流れる必要があります。MACの責任は、すべてのオートメーション関連機器と手順を設計、エンジニアリング、納入し、これらのシステムが安全かつ確実に統合され、必要なサービスによってサポートされるようにすることです。

- 石油・ガス業界では近年、オートメーション・ソリューションの普及が新たな高みに達しており、MACのサービスに対する需要に拍車をかけています。例えば、ダウンストリーム、ミッドストリーム、アップストリームの各企業は、様々な方法で機械学習を業務に組み込んでおり、今後も成長が続く可能性があります。とはいえ、業界は新しい運用方法を採用する必要があります。しかし、最近の動向は、自動化、人工知能(AI)、機械学習(ML)などの技術が業界にもたらす計り知れない可能性を認識しています。

- こうした動向を考慮し、ベンダーは石油・ガス会社とパートナーシップを結び、MACサービスを提供するケースが増えています。例えば、ABBは2022年6月、都市ガス配給会社のThink Gasと提携し、複数の拠点に広がる多数の遠隔端末を含むThink Gasのガスネットワーク全体の運用を自動化しました。ABBは同社全体のオペレーションを監視、統合、制御するシステムを構築し、ワークフローを自動化してオペレーターの安全性向上をサポートしました。

- さらに、大手の石油・ガス会社は、MACの導入がさまざまな業界で長期的に大きな成果を上げていることから、適切な管理、自動化・計装、製造、実行エンジニアの選定、機器の設置、試運転設備、アフターサービスを容易にすることで、プロジェクトの全責任を引き受け、満足のいく結果を出す手段として、MACの活用に力を入れています。

- しかし、主要自動化請負業者(MAC)の導入コストは、調査対象市場の成長にとって依然として大きな課題となっています。さらに、MACと関連ソリューションの標準化が進んでいないことも、調査対象市場の成長を抑制する主な要因の1つとなっています。

- COVID-19の発生当初は、MACのサプライチェーンにおけるパンデミックによる大きな変化と、よりクリーンで信頼性が高く、持続可能なエネルギー源への転換を求める動きの高まりのため、企業は努力の調整を余儀なくされました。しかし、COVID期間中に自動化ソリューションがその優位性を証明したことで、石油・ガス業界で事業を展開する多数のベンダーが高度な自動化ソリューションへの投資を増加させ、予測期間中に調査された市場に機会を創出すると予想されます。

石油・ガス業界のMAC(主要オートメーション請負業者)市場動向

上流部門が大きな成長を遂げる

- 石油・ガス産業の上流部門では、厳しい政府規制を満たす必要があり、運用コストを削減するための綿密な計画を必要とする掘削活動がいくつかあります。多くの場合、この業界では膨大な空間データを扱い、いくつかの意思決定を行う。この分野では、空間データの完全な力を活用するために、いくつかのプロセス自動化ツールや分析エンジンが採用されています。

- 英国では、かなりの探鉱活動によって、Glendronachのような重要な発見がなされました。Glendronachは、英国大陸棚における在来型天然ガスの埋蔵量としては、この1000年で5番目に大きいと推定されています。Glendronachの成功を受けて、Total Energiesのような企業は、上流の石油・ガス部門からのオートメーション・ソリューションの重要な需要源となる可能性のある近辺でのさらなる探査活動を計画しています。

- さらに、石油・ガス需要の増大は、上流活動を大幅に増加させるため、調査された市場での機会も促進します。例えば、OPECによると、世界の原油需要は2023年に日量1億189万バレルに達すると予測されています。

- 石油・ガス需要の増加は、石油・ガス産業の上流セグメントへの投資も促進しています。例えば、カナダ石油生産者協会(CAPP)によると、石油・天然ガスの上流生産への投資は2023年に400億カナダドル(294億米ドル)に達し、パンデミック前の水準を上回ると予想されています。

- 同様に、2019~2024年の全国大陸棚外石油・ガス租借プログラムでは、米国内務省は大陸棚外鉱区の約90%で洋上試掘を許可する予定です。この分野は、市場に新たな機会をもたらすと期待されています。

中東とアフリカが著しい成長を記録する

- 中東・アフリカは堅調な石油・ガス部門を誇る。近年、この産業は世界の動向を反映し、変化と課題を経験しています。アジア太平洋地域の投資は多様化し、より複雑なオフショアやLNGプロジェクトなど、新たな道が模索されています。

- この地域の石油・ガス生産能力拡張のために、いくつかの投資が行われています。例えば、2023年1月、ウガンダ石油庁は、2025年の最初の石油生産という目標を達成するため、最初の石油掘削プログラムを開始しました。キングフィッシャー油田は、アルバート湖の地下に埋蔵される同国の石油を開発し、タンザニアのインド洋港を経由して原油を国際輸送する広大なパイプラインを建設する100億米ドルの計画の一部です。

- 同様に2022年9月、アラブ首長国連邦は、世界がよりクリーンなエネルギーに移行する前に原油埋蔵量を活用しようと、石油生産能力を引き上げる計画を加速させていると発表しました。アラブ首長国連邦の石油のほとんどを汲み上げるアブダビ国営石油会社(Adnoc)は、2025年までに毎日500万バレルを生産したいと考えています。アラブ首長国連邦はまた、化石燃料価格が高止まりしている間に、石油・天然ガスの販売量を増やすことを目指しています。

- サウジアラビアでは、過去40年間に石油・ガス建設プロジェクトが急激に増加しました。ジュベイルやヤンブといった工業都市では、プラント建設、石油・ガス精製、パイプライン建設、採掘用坑井設置、石油化学製造業、その他ユーティリティなど、主要な石油・ガス開発プロジェクトが建設されています。したがって、中東&アフリカ地域での活動の増加は、予測期間中にMAC(主要オートメーション請負業者)市場の機会を促進すると予想されます。

石油・ガス業界のMAC(主要オートメーション請負業者)産業概要

石油・ガス業界のMAC(主要オートメーション請負業者)市場は、国内外にソリューションを提供する多数のプレイヤーの存在により、中程度の競争力を示しています。同市場は中程度の集中度を示しており、主要な業界リーダーは、製品革新、合併、買収、パートナーシップなどの主要戦略を採用してソリューションを強化し、世界のプレゼンスを拡大しています。この市場における著名なプレーヤーには、Rockwell Automation Inc.、Schneider Electric SE、横河電機株式会社、Honeywell International Inc.などが含まれます。

2023年2月、ValmetとNaizak Global Engineering Systemsは、Valmet DNA Automation Systemsに関する付加価値再販業者(VAR)契約を締結しました。この契約は、サウジアラビアとバーレーンの石油・ガス、電力、上下水道、その他のプロセス産業など、様々な分野でのアプリケーションを網羅しています。両社は、主要な分散型制御システムベンダーと効果的に競合することを目的として、専門のMAC(主要オートメーション請負業者)チームを設立する計画を打ち出しています。

横河電機は2022年10月、オランダのロッテルダム港にあるシェルPLCのオランダ水素Iプラントの建設で、MAC(主要オートメーション請負業者)として重要な契約を獲得しました。このプラントは、洋上風力発電所で発電された電力を利用し、再生可能な水素を製造するものです。2025年の稼働開始が見込まれるオランダ水素Iプラントは、欧州最大の再生可能水素製造施設となります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 伝統的アプローチとMACアプローチ(コスト削減アプローチ)の比較

- MACのベストプラクティス

- 主な使用事例

第5章 市場力学

- 市場促進要因

- プロジェクト管理と統合の複雑さを避けるため、石油・ガス会社によるMACアプローチへの選好の高まり

- 市場の課題

- COVID-19が市場に与える影響と大手石油・ガス会社の支出削減計画

第6章 市場セグメンテーション

- セクター別

- アップストリーム(オフショアとオンショア)

- ミッドストリーム

- ダウンストリーム

- プロジェクト規模別

- 中小規模(500万米ドル~3,000万米ドル)

- 大規模(3,100万米ドル以上)

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Rockwell Automation Inc.

- Schneider Electric SE

- Yokogawa Electric Corporation

- Honeywell International Inc.

- Emerson Electric Co.

- Siemens AG

- ABB Ltd

第8章 投資分析

第9章 市場の将来

The Main Automation Contractor In Oil & Gas Industry is expected to grow from USD 1.23 billion in 2025 to USD 1.67 billion by 2030, at a CAGR of 6.28% during the forecast period (2025-2030).

Key Highlights

- The growing demand for oil and gas across various end-user industries has significantly enhanced the rate of mechanization and the adoption of automation solutions, along with the demand for a higher process and operational efficiency, which positively influences the studied market's growth.

- With the increasing scope of automation in today's information-driven oil production environment, handling more information processing close to the production site is critical. Suitable production and operational data should flow smoothly between oil production and business systems. MAC's responsibility is to design, engineer, and deliver all automation-related equipment and procedures and ensure that these systems are integrated safely and securely and supported by necessary services.

- In the oil and gas industry, the penetration of automation solutions has been touching new heights in recent years, which is fueling the demand for MAC services. For instance, downstream, midstream, and upstream firms have integrated machine learning into their operations in many ways, which may continue to grow. Although, the industry needs to adopt new ways of operating. However, recent trends recognize the immense potential of technologies such as automation, artificial intelligence (AI), and machine learning (ML) can have on the industry.

- Considering such trends, vendors are increasingly entering into partnerships with oil & gas companies to offer MAC services. For instance, in June 2022, ABB partnered with Think Gas, a city gas distribution company, to automate operations across Think Gas' gas network, including many remote terminals spread across multiple locations. ABB created a system to monitor, integrate, and control operations across the company, automating workflows to support operators in improving safety.

- Furthermore, large oil and gas companies are focusing on leveraging MAC as a means of undertaking full project responsibility and delivering satisfactory results by facilitating proper management, automation/instrumentation, manufacture, selection of execution engineers, installation of equipment, commissioning equipment, and after-sales support as MAC implementation has demonstrated significant results in long-term, across various industries.

- However, the cost of implementation of the main automation contractor (MAC) continues to remain among the major challenging factors for the growth of the studied market. Furthermore, the lack of standardization of MAC and related solutions are also among the major restraining factors for the growth of the studied market.

- During the initial outbreak of COVID-19, companies were forced to coordinate their efforts due to the significant changes caused by the pandemic in the MAC supply chain and the growing movement to switch to cleaner, more dependable, and more sustainable energy sources. However, with automation solution proving their supremacy during the COVID period, a significant number of vendors operating in the oil & gas industry are anticipated to increase their investment in advanced automation solutions, creating opportunities in the studied market during the forecast period.

Oil & Gas Main Automation Contractor Market Trends

Upstream Segment to Witness Significant Growth

- The upstream sector of the oil and gas industry involves several drilling activities that must meet stringent government regulations and require intense planning to cut operational costs. Often, the industry deals with vast sets of spatial data to make several decisions. Several process automation tools and analytical engines are employed in the sector to harness the complete power of spatial data.

- Considerable exploration activity in the United Kingdom has led to crucial discoveries such as Glendronach, which is estimated to be the fifth-largest conventional natural gas reserve on the UK Continental Shelf in the millennium. Following Glendronach's success, companies such as Total Energies plan further exploration activities in the vicinity, which may be a significant source of demand for automation solutions from the upstream oil and gas sector.

- Furthermore, the growing demand for oil and gas also drives opportunities in the studied market as it significantly increases upstream activities. For instance, according to OPEC, the global crude oil demand is anticipated to reach 101.89 million barrels per day in 2023.

- The growing demand for oil & gas is also driving investments in the upstream segment of the oil and gas industry. For instance, according to the Canadian Association of Petroleum Producers (CAPP), oil and natural gas investment in upstream production is anticipated to reach CAD 40 billion (USD 29.4 billion) in 2023, surpassing the pre-pandemic levels.

- Similarly, under the National Outer Continental Shelf Oil and Gas Leasing Program for 2019-2024, the US Department of the Interior is planning to allow offshore exploratory drilling in about 90% of the Outer Continental Shelf acreage. The sector is expected to open up new opportunities to the market.

Middle-East and Africa to Register Considerable Growth

- Middle-East and Africa boast a robust oil and gas sector. In recent years, the industry has mirrored global trends and experienced changes and challenges. Investment across the Asia pacific region is becoming more diverse, and new avenues are being explored, such as more complex offshore and LNG projects.

- Several investments are being made for the region's oil and gas capacity expansions. For instance, in January 2023, the Petroleum Agency of Uganda launched its first oil drilling program to meet its target of first oil output in 2025. The Kingfisher field is part of a USD 10 billion scheme to develop the country's oil reserves under Lake Albert and build a vast pipeline to ship the crude internationally via an Indian Ocean port in Tanzania.

- Similarly, in September 2022, the United Arab Emirates announced that it is accelerating a plan to raise its oil production capacity as it attempts to leverage its crude reserves before the world transitions to cleaner energy. Abu Dhabi National Oil Co. (Adnoc), which pumps almost all the United Arab Emirates oil, wants to produce 5 million barrels daily by 2025. The United Arab Emirates also aims to sell more oil and natural gas while fossil fuel prices stay high.

- Saudi Arabia witnessed exponential growth in oil and gas construction projects in the last four decades. Major oil and gas development projects have been constructed in industrial cities, such as Jubail and Yanbu, including the construction of plants, oil and gas refineries, construction of pipelines, well oil setups for extraction, petrochemical manufacturing industries, and other utilities. Hence, the growing activities in the Middle East & African region are anticipated to drive opportunities in the main automation contractor (MAC) market during the forecast period.

Oil & Gas Main Automation Contractor Industry Overview

The automation contractor market in the oil and gas industry exhibits moderate competitiveness, owing to the presence of numerous players offering solutions both domestically and internationally. The market demonstrates a moderate level of concentration, with major industry leaders employing key strategies such as product innovation, mergers, acquisitions, and partnerships to enhance their solutions and expand their global presence. Prominent players in this market include Rockwell Automation Inc., Schneider Electric SE, Yokogawa Electric Corporation, and Honeywell International Inc.

In February 2023, Valmet and Naizak Global Engineering Systems inked a Value Added Reseller (VAR) Agreement pertaining to Valmet DNA Automation Systems. This agreement encompasses applications in various sectors, including oil, gas, power, water, wastewater, and other process industries in Saudi Arabia and Bahrain. Both companies have laid out plans to establish a dedicated Main Automation Contractor (MAC) team, with the objective of competing effectively with major distributed control system vendors.

In October 2022, Yokogawa Electric Corporation secured a significant contract as the main automation contractor (MAC) for the construction of Shell PLC's Holland Hydrogen I plant located in the Dutch port of Rotterdam. This plant is set to produce renewable hydrogen, utilizing electricity generated from an offshore wind farm. Upon its anticipated operational launch in 2025, the Holland Hydrogen I plant is poised to become the largest renewable hydrogen production facility in Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Traditional Approach vs. MAC Approach (Cost Savings Approach)

- 4.4 MAC Best Practices

- 4.5 Key Use Cases

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Preference of Oil and Gas Companies for a MAC Approach to Avoid Project Management and Integration Complexities

- 5.2 Market Challenges

- 5.2.1 Impact of COVID-19 on the Market and Planned Spending Cuts from Major Oil and Gas Companies

6 MARKET SEGMENTATION

- 6.1 By Sector

- 6.1.1 Upstream (Offshore and Onshore)

- 6.1.2 Midstream

- 6.1.3 Downstream

- 6.2 By Project Size

- 6.2.1 Small and Medium (USD 5 million to USD 30 million)

- 6.2.2 Large (USD 31 million and Above)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Rockwell Automation Inc.

- 7.1.2 Schneider Electric SE

- 7.1.3 Yokogawa Electric Corporation

- 7.1.4 Honeywell International Inc.

- 7.1.5 Emerson Electric Co.

- 7.1.6 Siemens AG

- 7.1.7 ABB Ltd