|

市場調査レポート

商品コード

1643095

RFフロントエンドモジュール:市場シェア分析、産業動向、成長予測(2025~2030年)RF Front End Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| RFフロントエンドモジュール:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

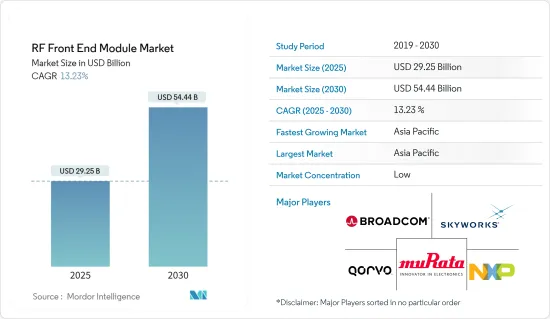

RFフロントエンドモジュール市場規模は、2025年に292億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.23%で、2030年には544億4,000万米ドルに達すると予測されています。

最近の動向では、低コストの超小型衛星の開発が著しく伸びています。これは、低コストの打ち上げベクターと「商用オフザシェルフ・部品」(COTS)が利用可能になったため実現可能になったものです。ほとんどのCOTS部品は、通常、宇宙仕様ではなく、過酷な宇宙環境に耐えて動作させるためには、回路内の再設計と実装に余分な労力を必要とします。RFフロントエンド設計は、COTS部品を使用して完全に実装されたSバンドトランシーバで構成されており、専門家調査において、より優れた、より実現可能な選択肢の1つと考えられています。超小型衛星への実装が進めば、このセグメントの市場は予測期間中に大きく成長すると考えられます。

主要ハイライト

- RFフロントエンドモジュールとは、無線レシーバーのアンテナ入力とミキサー段または送信機のパワーアンプの間にある無線レシーバー回路の回路を指します。

- モバイル通信機器の急激な増加や、データ集約型用途によるデータトラフィックの増大により、RF FEMプロバイダーは携帯端末の高周波数帯などの技術革新をリードしています。さらに、Cisco Visual Networking Indexによると、世界のモバイルデータトラフィックは2017~2022年の間にCAGR 46%で7倍に増加し、2022年には月間77.5エクサバイトに達すると予想されています。

- Qorvoは、Wi-Fi 6用の初のデュアルバンドフロントエンドモジュール(FEM)であるSKY85334-11とSKY85750-11を発表しました。SKY85334-11とSKY85750-11は、HD/4Kビデオの配信に必要な性能とIoTに必要な効率性を兼ね備え、CPE(Customer Premise Equipment)に最適な設計となっています。また、規制、熱、PoE(Power-over-Ethernet)の制限により低消費電流が要求されるアクセスポイント、ルーター、ゲートウェイ向けの直線性、電力損失、効率を特徴とするモジュールにより、用途としてスイッチング、バイパス付きローノイズアンプ(LNA)、パワーアンプ(PA)での統合を見過ごすことはありません。

- さらに、新興国や先進国における防衛予算の絶え間ない増加や、国内外の軍事の武器庫における技術的に進歩した製品に対する需要は、世界市場の成長をさらに促進すると予想されます。軍事用無線周波数と電子戦用途は、自律走行車とドローンの技術進歩に加えて、成長が見込まれています。

- RFパワーアンプ(PA)は、ワイヤレスモバイルインフラのすべての基地局に不可欠な部品です。これらは、最新のインフラ機器のサブアセンブリの中で最も高価な部品の1つです。これらの電力増幅器に使用されるGaN RF半導体は、RF PA設計者とユーザーが直面する経済的技術的現実とともに進化しなければなりません。

- 政府による操業停止や渡航・貿易制限により、エレクトロニクス、自動車、航空宇宙・防衛、通信など多くの産業が操業停止を余儀なくされ、2020年のRFパワー半導体の需要は低下しました。2022年現在、いくつかのRF部品メーカーは、地域の原料サプライヤーと協力することでサプライチェーンを再編成しています。将来的には、COVID-19パンデミックによる生産者の負担が軽減されると予測されます。

高周波(RF)フロントエンドモジュール市場動向

大きな成長を遂げるRFフィルター

- 無線周波数(RF)フィルターは、さまざまなチャネルでデータを受信・転送する際にホワイトノイズの干渉を除去するために通信産業で広く使用されています。これらのフィルタは、テレビ放送、無線通信、中周波から高周波で動作するラジオなどのセグメントで採用されることが多いです。これは、信頼性が高く、エラーのない、適切な通信を端から端まで提供するために行われます。RFフィルターには、帯域阻止、ハイパス、バンドパス、ローパスの4種類があります。

- RFフィルターは無線受信機で使用され、適切な周波数のみが放送されるようにし、望ましくない周波数帯をフィルタリングします。ワイヤレス技術には欠かせない要素です。これらのフィルターは、メガヘルツやギガヘルツといった、中程度から非常に高い周波数で機能するように作られています。その機能的特徴から、放送ラジオ、無線通信、テレビなどの機器に最も一般的に採用されています。

- モバイルコンピューティングデバイスは、常時移動と接続を必要とするモバイルユーザーや出張者の間で人気が高まっています。消費者は、ソーシャルメディア用途へのアクセス、ネットサーフィン、ニュースの閲覧、電子メールのチェックなど、さまざまな作業にこれらのガジェットを使用しています。インターネット普及率の高まりと、手頃な速度で高速データ通信が可能なことが、モバイルコンピューティングデバイスの需要を牽引しています。

- モバイルコンピューティングデバイスの利用拡大により、ネットワークトラフィックは指数関数的に増加しています。機能が向上したモバイルコンピューティングデバイス(スマートフォン、タブレット、ノートパソコンなど)の普及が、インターネット帯域幅を拡大しています。スマートフォンやタブレット端末では、LTEやWi-Fiなどの先進的無線技術を取り入れることで、新たなRF機能に対するニーズが高まっている

- さらに、RFフィルターは携帯電話環境において不可欠な機能を果たしています。例えば携帯電話は、効果的に機能するために特定のバンド数を必要とします。適切なRFフィルターがなければ、さまざまな帯域を同時に共存させることはできないです。その結果、Wi-Fi、公共安全、全地球航法衛星システム(GNSS)など、特定の帯域が拒絶されることになります。RFフィルターは、すべての帯域を同時に共存させることができるため、非常に重要です。

- 5Gスマートフォンの需要の増加は、RFフィルターの需要をさらに押し上げると考えられます。GSMAによると、カナダのモバイル接続に占める5Gの普及率は、2021年の8%から2025年には49%に達します。

アジア太平洋が大きな成長を遂げる

- アジア太平洋は大きな成長が見込まれます。中国、インド、韓国などの主要新興国の著しい成長とともに、民生用電子機器の進歩や防衛機器への要求の高まりが、RF部品市場の需要をさらに押し上げると考えられます。

- 集積回路(IC)産業の繁栄、アジア太平洋におけるSOIエコシステムの拡大、IoT用途でのSOI使用の増加はRFフロントエンドモジュール(RFFE)の成長機会として作用します。フォーブスによると、IoTデバイスの数は2023年までに35億を突破し、アジアが最も高い市場シェアをリードします。2023年までに、北東アジアは22億台以上のデバイスの市場となります。

- 2G、3G、4G/LTE(Long-term Evolution)でのデータ伝送のために、モバイル機器は専用のフロントエンドモジュール(FEM)を必要とします。FEMはRF-SOIチップを使用し、スイッチ、電力増幅器、アンテナ調整部品、電力管理ユニット、フィルターなどをIoT用途用の単一プラットフォーム上に集積しています。そのため、この地域の市場成長に貢献しています。

- さらに、アジア太平洋では自動車の生産台数が増加しており、L1バンド(1,574.42~1,576.42 MHz)で動作する全地球測位システム(GPS)とSバンド(2,320~2,345 MHz)で動作する衛星デジタルオーディオ・ラジオシステム(SDARS)用の小型デュアルバンドRFフロントエンド・モジュールの需要が高まると予想されます。これが、この地域の市場を押し上げる可能性があります。中国は最大の電気自動車メーカーであり、予測期間中のEV普及率も最高レベルでリードしています。2030年までに、新車販売台数に占めるEVの割合は、すべての道路交通モード(二輪車、自動車、バス、トラック)で57%に達すると推定されます。

- さらに、フロントエンドモジュールは基地局や5Gスマートフォンなど多くのワイヤレス用途に不可欠であるため、国内半導体産業の育成を目的とした中国の大規模設備投資プロジェクトは、第2段階の資金調達を開始しました。同プロジェクトは今後5年間の予定で、予算は2041億5,000万元(289億米ドル)。Huaweiは、RFフロントエンドモジュールに取り組むことで、必要な技術、設計、IPを開発するために注意を払う必要があるセグメントを熟考する機会を作り出し、おそらく中国での全統合モジュールシステムの設計を開始する見込みです。これにより、市場の将来的な成長がさらに促進されます。

高周波(RF)フロントエンドモジュール産業概要

RFフロントエンドモジュール市場は、高い市場競合により細分化されています。技術革新、提携、合併の増加に伴い、市場は予測期間中に高い競争が予想されます。市場の主要企業は、Broadcom Inc.、Skyworks Solutions, Inc.などがあります。

2022年6月、Qualcomm Technologies Inc.は、車載機器やインターネット接続機器の無線性能を強化したWi-Fi 7フロントエンドモジュールの発売を発表しました。RFFEモジュールの採用は、車載とIoT向けのモデム-to-アンテナソリューションで携帯電話端末の製品レンジを拡大するという同社の目標に沿ったものでした。

Murata Manufacturingは2022年2月、5G無線インフラ向けのミリ波RFフロントエンド・ポートフォリオの拡充を発表しました。3つのビームフォーミングICと2つのアップダウンコンバータにより、n257、n258、n260の各帯域でIFからRFまでをフルカバーするICを柔軟に交換できるようになりました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- RF-SOIの普及とスマートデバイスの普及拡大

- Bluetooth IoT用途の採用

- 市場課題

- COVID-19の影響による需要の低迷

- 製造コストが高く、ウエハーサイズが小さい

第6章 市場セグメンテーション

- 部品別

- RFフィルター

- RFスイッチ

- RFパワーアンプ

- その他

- 用途別

- 民生用電子機器

- 自動車

- 軍事用

- 無線通信

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他のアジア太平洋

- その他その他(ラテンアメリカ、中東・アフリカ)

- 北米

第7章 競合情勢

- 企業プロファイル

- Broadcom Inc.

- Skyworks Solutions Inc.

- Murata Manufacturing Co. Ltd

- Qorvo Inc.

- NXP Semiconductors NV

- Texas Instruments Incorporated

- Infineon Technologies AG

- Qualcomm Technologies Inc.

- Teradyne, Inc.(LitePoint Corporation)

- RDA Microelectronics Inc.

第8章 投資分析

第9章 市場の将来

The RF Front End Module Market size is estimated at USD 29.25 billion in 2025, and is expected to reach USD 54.44 billion by 2030, at a CAGR of 13.23% during the forecast period (2025-2030).

In recent years, the development of low-cost nanosatellites has grown considerably. It has been made viable due to the availability of low-cost launch vectors and "commercial off-the-shelf components" (COTS). Most COTS components are usually not space-qualified, and to make them work and withstand the harsh space environment, they need extra effort in in-circuit redesign and implementation. The RF front-end design is considered one of the better and more feasible choices in expert research, which consists of an S-band transceiver that is fully implemented using COTS components. If further implemented in nanosatellites, the market in this sector shall grow significantly during the forecast period.

Key Highlights

- An RF front-end module refers to the circuitry in a radio receiver circuit between a radio receiver's antenna input and the mixer stage or the transmitter's power amplifier.

- The exponential increase in mobile communication devices on a unit basis and rising data traffic due to data-intensive applications have led RF FEM providers to lead innovation, such as high-frequency bands in handsets. Additionally, per the Cisco Visual Networking Index, the global mobile data traffic is expected to increase sevenfold between 2017 and 2022, with a CAGR of 46%, reaching 77.5 exabytes per month by 2022.

- Qorvo introduced the first dual-band front-end module (FEM) for Wi-Fi 6, the SKY85334-11 and SKY85750-11. It is designed ideally for customer premise equipment (CPE), combining the performance required to deliver HD/4K video with the efficiency needed for IoT. Also, by featuring linearity, power dissipation, and efficiency for access points, routers, and gateways, where regulatory, thermals, or Power-over-Ethernet (PoE) limitations demand low current consumption, the modules overlook integration at switching, low-noise amplifier (LNA) with bypass and power amplifier (PA) as applications.

- Moreover, the constant increase in defense budgets in developing and developed nations and the demand for technologically-advanced products in the arsenal of national and international armed forces are expected to further fuel the global market's growth. Military radio frequency and electronic warfare applications are expected to grow in addition to the technological advancements in autonomous vehicles and drones.

- RF power amplifiers (PA), thus, form an integral part of all the base stations for wireless mobile infrastructure. They represent one of the most expensive components of sub-assemblies in modern infrastructure equipment. The GaN RF semiconductors used in these power amplifiers must evolve with the economic and technical realities facing the designers and users of these RF PAs.

- Due to government-imposed lockdowns and travel and trade restrictions, many industries, such as electronics, automotive, aerospace & defense, and telecommunications, were forced to shut down their operations, lowering the demand for RF power semiconductors in 2020. As of 2022, several RF component makers have reorganized their supply chains by working with regional raw material suppliers. In the future, this is projected to reduce the burden of the COVID-19 pandemic on producers.

Radio Frequency (RF) Front End Module Market Trends

RF Filters to Witness Significant Growth

- Radiofrequency (RF) filters are widely used in the communication industry to eliminate white noise interference when receiving and transferring data across various channels. These filters are often employed in operating fields, such as television broadcasting, wireless communication, and radios operating from medium to high frequencies. This is done to provide reliable, error-free, and appropriate communication from one end to the other. Band-reject, high-pass, band-pass, and low-pass filters are the four types of RF filters.

- RF filters are used with radio receivers to ensure that only the appropriate frequencies are broadcasted, filtering out undesirable bands of frequencies. They are a crucial component of wireless technology. These filters are built to function at frequencies ranging from medium to extremely high, such as megahertz and gigahertz. Due to their working feature, they are most commonly employed in equipment like broadcast radio, wireless communications, and television.

- Mobile computing devices are becoming more popular among mobile users and business travelers who need constant mobility and connection. Consumers use these gadgets for various tasks, including accessing social media applications, surfing the web, reading news, and checking emails. The growing internet penetration rate and the availability of high data rates at affordable speeds are driving the demand for mobile computing devices.

- Network traffic is increasing exponentially, owing to the growing use of mobile computing devices. The proliferation of mobile computing devices (such as smartphones, tablets, and laptops) with increased capabilities is driving internet bandwidth. The increased need for new RF functionalities in smartphones and tablets has resulted from incorporating advanced wireless technologies, such as LTE and Wi-Fi.

- Furthermore, RF filters play an essential function in the cell phone environment. Mobile phones, for example, require a particular number of bands to function effectively. Without the right RF filter, the various bands cannot coexist simultaneously. This will result in the rejection of certain bands, such as the Wi-Fi, public safety, and global navigation satellite system (GNSS). RF filters are crucial because they allow all bands to coexist simultaneously.

- The increasing demand for 5G smartphones will further boost the demand for RF filters. According to GSMA, the 5G adoption rate as a share of mobile connections in Canada will reach 49% by 2025 from 8% in 2021.

Asia-Pacific to Witness Major Growth

- The Asia-Pacific is expected to witness significant growth. The advancement in consumer electronics and growing defense equipment requirements with the considerable growth of major emerging economies, such as China, India, and South Korea, will further boost the demand for the RF component market.

- The flourishing Integrated Circuit (IC) industry, expanding the SOI ecosystem in the Asia-Pacific, and increasing the use of SOI in IoT applications act as growth opportunities for the RF Front End Module (RFFE). According to Forbes, the number of IoT devices will surpass 3.5 billion by 2023, with Asia leading the highest market share. By 2023, Northeast Asia will be a market for more than 2.2 billion devices.

- For data transmission over 2G, 3G, and 4G/ Long-term Evolution (LTE), mobile devices require dedicated front-end modules (FEMs). FEMs use RF-SOI chips, which integrate switches, power amplifiers, antenna tuning components, power management units, and filters on a single platform for IoT applications. Hence, this caters to the market growth in the region.

- Further, increasing the production of vehicles in the Asia-Pacific is expected to drive the demand for compact dual-band RF front-end modules for global positioning system (GPS) operating in the L1-band (1574.42-1576.42 MHz) and satellite digital audio radio system (SDARS) operating in the S-band (2320-2345 MHz. This, in turn, may boost the market in the region. China is the largest maker of electric vehicles and leads with the highest level of EV uptake over the projection period. By 2030, the share of EVs in new vehicle sales is estimated to reach 57% across all road transport modes (i.e., two-wheelers, cars, buses, and trucks).

- Furthermore, as front-end modules are essential to many wireless applications, such as base stations and 5G smartphones, China's massive capital investment project designed to nurture the domestic semiconductor industry has rolled out its second funding phase. The project is scheduled for the next five years with a budget of YUAN 204.15 billion (USD 28.9 billion). By addressing RF front-end modules, Huawei creates an opportunity to ponder areas that need attention for developing the necessary technologies, designs, and IPs, possibly expected to begin designing a whole integrated module system in China. This further penetrates future growth for the market.

Radio Frequency (RF) Front End Module Industry Overview

The RF front-end module market is fragmented due to high market rivalry. With increasing innovation, partnerships, and mergers, the market is expected to have high competition in the forecasted period. Key players in the market are Broadcom Inc., Skyworks Solutions, Inc., etc.

In June 2022, Qualcomm Technologies Inc. announced the launch of Wi-Fi 7 front-end modules that offered enhanced wireless performance in automotive and internet-connected devices. The introduction of the RFFE modules aligned with the company's objective to extend its handset range with modem-to-antenna solutions for automotive and IoT.

In February 2022, Murata Manufacturing announced the expansion of its millimeter-wave RF front-end portfolio for 5G wireless infrastructure applications. The three beam-forming ICs and two up-down converters offered flexibility to interchange ICs for full IF-to-RF coverage across the n257, n258, and n260 bands.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Popularity of RF-SOI and the Increasing Adoption of Smart Devices

- 5.1.2 Adoption of Bluetooth IoT Applications

- 5.2 Market Challenges

- 5.2.1 Low Demand due to the Impact of COVID-19

- 5.2.2 Expensive to Fabricate and Smaller Wafer Sizes

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 RF Filters

- 6.1.2 RF Switches

- 6.1.3 RF Power Amplifiers

- 6.1.4 Other Components

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Military

- 6.2.4 Wireless Communication

- 6.2.5 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Rest of the World (Latin America, Middle East and Africa)

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Broadcom Inc.

- 7.1.2 Skyworks Solutions Inc.

- 7.1.3 Murata Manufacturing Co. Ltd

- 7.1.4 Qorvo Inc.

- 7.1.5 NXP Semiconductors NV

- 7.1.6 Texas Instruments Incorporated

- 7.1.7 Infineon Technologies AG

- 7.1.8 Qualcomm Technologies Inc.

- 7.1.9 Teradyne, Inc. (LitePoint Corporation)

- 7.1.10 RDA Microelectronics Inc.