|

市場調査レポート

商品コード

1643014

データコンバータ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Data Converter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データコンバータ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

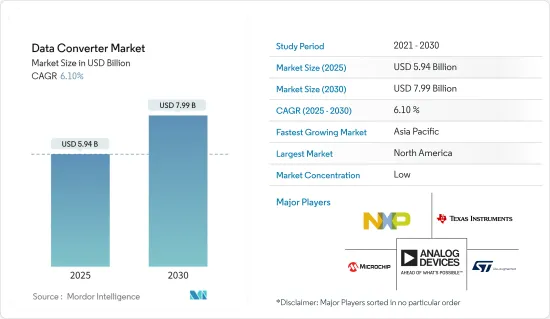

データコンバータ市場規模は2025年に59億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.1%で、2030年には79億9,000万米ドルに達すると予測されます。

高性能電子システムは、アーキテクチャを改善・形成し、新しい用途の展望を開くために、より多くの高性能データコンバータを使用しています。最先端の変調器の最前線にある新たな回路とシステム技術は、その性能を押し進め、新世代のデータコンバータを生み出しています。さらに、現在と将来の動向は、世界経済、技術進化、マーケティングなど、新旧の要因に左右されます。

主要ハイライト

- 技術的に先進的データ収集システムの採用が市場を牽引しています。複数の信号に符号化された情報の割合が高いため、データ収集(DAQ)システムは研究作業から近代的なエンジニアリングプロセスへと進化を余儀なくされています。産業は、モジュール型ハードウェアと柔軟なソフトウェアの組み合わせという動向に向かって進化しており、これらの新しいモジュール型システムは、適切な信号調整とアナログデジタル変換(ADC)を備え、複数のデータ収集要件をサポートするさまざまなセンサとのインタフェースを備えています。

- 特定のDAQタスクを実行するための従来のアプローチは、今日の要件を考慮すると実行不可能です。そのため、市場ではDAQに対するよりソフトウェア定義のアプローチや、高速USB対応DAQの出現に向かう傾向があります。

- さらに、科学と医療用途における高解像度画像への需要の高まりが、市場調査を後押ししています。データコンバータは、必要とされるダイナミックレンジ、分解能、精度、直線性、ノイズという点で、医療用画像がエレクトロニクス設計に課す最も厳しい課題となっています。ADC(アナログデジタル変換)は、より良い鮮明な画像を実現するために少なくとも24ビットの高分解能を持ち、CT(コンピュータ断層撮影)ソリューションでは100μsと短い検出器の読み取り値をデジタル化するために高速サンプリングレートを持つ必要があります。ADCのサンプリング・レートは、より少ないコンバータの使用とシステム全体のサイズと電力の削減を可能にする多重化も可能にしなければなりません。

- アナログ・デバイセズのような企業は、これらの要件に対応し、クラス最高の臨床画像診断装置を実現するための主要なシグナルチェーン機能ブロックの高度に統合されたソリューションを提供しています。ADAS1256(X線用途)、ADAS1135、ADAS1134(CT用途)など、同社の製品は医療用途市場を牽引しています。

- さらに、低消費電力データコンバータの開発が市場成長の課題となっています。消費電力は、今日の集積回路における主要な設計制約の1つです。低周波の生体電気信号の変換には高速性は要求されないが、超低消費電力動作が要求されます。このことは、要求される変換精度と相まって、このようなADCの設計を大きな課題にしています。

- さらに、COVID-19パンデミックの影響により、半導体産業では国際的に需給への影響が大きいです。データコンバータの開発には、IC、抵抗、コンデンサなどが必要です。流通チャネルの断絶がデータ変換器市場の成長を鈍化させています。しかし、多くの中央政府や地方自治体は半導体産業の戦略的重要性を認識しており、事業閉鎖が義務付けられる中、国内企業やサプライヤーの中断のない運営を優先しています。

データコンバータ市場動向

通信が大きな市場シェアを占める

- 通信インフラは、4G通信と5G通信の出現により市場成長を刺激しています。無線インフラ、特に4Gと5Gのメーカーは、性能、機能性、サービス品質の高水準を維持しながら、新たに設置する無線インフラのサイズとコストを常に削減しています。データ変換ブロックは、無線インフラ設計において重要な機能です。アナログデジタルコンバータ(ADC)は、入力される中間周波数(IF)信号をデジタル化し、デジタルデータをデジタルダウンコンバータに渡す基本ブロックです。

- 5Gソリューションの広帯域要求は、周波数変換とフィルタリングをアナログ領域からデジタル領域に移行することで満たすことができます。AD9081/AD9082ミックスドシグナルRFコンバータという2つのRFコンバータは、アナログデバイスが発表するこのデジタル化の波の一部です。これらのRFコンバータは、マルチバンド無線機をシングルバンド無線機と同じフットプリントに設置できるように設計されており、現在の4G LTE基地局で利用可能な通話容量と比較して、通話容量を3倍に増やすのに役立ちます。

- さらに、5Gソリューションが小型アンテナの展開をサポートするためには、無線アーキテクチャ・コアを緊密に統合する必要があります。一つの解決策は、マルチギガサンプルのADCとDACをシステムオンチップ(SoC)と組み合わせた従来のアプローチです。このアプローチは、組み込みシステム設計を実行し、要求される動作帯域幅の増加に対応する能力を記載しています。いくつかのデータコンバータは、JESD204Bを使用したインターフェースを実装しています。

- また、ザイリンクスのようなFPGAメーカーは過去10年間にわたり、シリコン製造構造のサイズを縮小することで技術を向上させ、その結果、デバイスのサイズ、重量、消費電力(SWaP)値も縮小してきました。ザイリンクスの最新のシステムオンチップ(SoC)デバイスであるRFSoCは、FPGAファブリックとアームプロセッサ、アナログデジタルコンバータ(ADC)、デジタルアナログコンバータ(DAC)のすべてを同一チップ上に集積したものです。

- この16nm技術は、1デバイスあたり4.2K DSPスライス、4個の1.5GHz A53 Armプロセッサ、2個の600MHz R5 ARMプロセッサ、8個の4GHz、12ビットADC、8個の6.4GHz、14ビットDACを搭載しています。COTS(Commercial-off-the-shelf)メーカーは、5G無線製品を開発するエンジニアにマルチチャネルSDRトランシーバーを提供するために、この画期的な技術を使用することができます。

北米が最大の市場シェアを占める

- 北米は、通信セグメントの成長とFPGA(フィールド・プログラマブル・ゲート・アレイ)の使用により、最も高いシェアを占めています。民生用電子機器では、高解像度の画像を得るためにA2Dコンバータの需要が高まっており、市場を牽引する重要な要素となっています。

- さらに、データコンバータを必要とする自動車のセンサ用途は、さまざまなエンジン状態を識別する温度センサから、自動車運転支援システム(ADAS)を可能にするレーダー/ライダーまで多岐にわたります。その他のデータコンバータ用途には、他の車両や固定ネットワークと通信するためのワイヤレストランシーバが含まれます。米国でEV販売を後押ししてきた車両1台当たり7,500米ドルの税額控除は、インセンティブの上限を増やすことなく廃止される方向です。

- また、関税リスクも外資系企業に北米での買い物を迫っています。Volkswagenは、テネシー州チャタヌーガに8億米ドルを投じて製造施設を建設すると発表しました。さらに、トヨタとマツダは共同でアラバマ州ハンツビルに組立工場を建設します。約16億米ドルを投じるこの工場は、年間30万台の生産能力を持っています。このような事例は、この地域の自動車セグメントにおけるデータコンバータ市場の成長を高めると予想されます。

- さらに、米国ではIT・通信用途がデータコンバータ市場で最大のシェアを占めると推定されます。この成長を牽引しているのは4Gネットワークの開発であり、音声とデータサービスの向上のために優れた変調方式とアンテナ方式が採用され、AMSブロックの需要を高めています。

- さらにGSMAによると、米国ではモバイル接続に占める5Gの普及率が今後3年間でそれぞれ33%、40%、46%増加すると予想されています。このことは、データコンバータの5Gにおける用途の成長をさらに促進します。

データコンバータ産業概要

データコンバータ市場は、世界の参入企業が民生用電子機器や自動車などの様々な用途で信号を統合しているためセグメント化されており、競合企業間の激しい競争となっています。主要企業は、Analog Devices Inc.、Microchip Technology Inc.どがあります。

- 2022年5月:Analog Devices Inc.は、次世代の16~24ビット、超高精度SAR ADCの新ポートフォリオを発表し、計装、産業、医療向けのADC設計の複雑なプロセスを簡素化しました。ADIの特許取得済みEasy Drive技術と適応可能なFlexi-SPIシリアル・ペリフェラル・インターフェース(SPI)は、システム設計の問題に対処し、直接互換性のあるコンパニオン製品の範囲を拡大する、新しい高性能SAR ADCシリーズの2つの側面です。

- 2022年 9月:MaxLinear Inc.とRFHICは、量産可能な5Gマクロセル無線用の400MHzパワーアンプ(PA)ソリューションを開発するための協業を発表しました。このソリューションでは、MaxLinear MaxLINのデジタルプレディストーション(DPD)とクレスト・ファクター・リダクション(CFR)技術を使用し、RFHICの最新のID-400WシリーズGaN RFトランジスタの性能を強化します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 市場の定義と範囲

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 技術的に先進的データ収集システムの採用増加

- 科学・医療用途における高解像度画像への需要の高まり

- 市場課題

- 低消費電力データコンバータの開発における課題

- 世界の半導体のサプライチェーン流通におけるCOVID-19パンデミックの影響

第6章 主要技術投資

- クラウド技術

- 人工知能

- サイバーセキュリティ

- デジタルサービス

第7章 市場セグメンテーション

- タイプ別

- アナログデジタルコンバータ

- デジタルアナログコンバータ

- エンドユーザー別

- 自動車

- 通信

- 民生用電子機器

- 産業用

- 医療

- その他

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他のアジア太平洋

- その他

- 北米

第8章 競合情勢

- 企業プロファイル

- Analog Devices Inc.

- Microchip Technology Inc.

- STMicroelectronics NV

- NXP Semiconductors NV

- Texas Instruments Incorporated

- Mouser Electronics Inc.

- DATEL Inc.

- Synopsys Inc.

- Cirrus Logic Inc.

- Maxim Integrated Products Inc.

第9章 投資分析

第10章 市場機会と今後の動向

The Data Converter Market size is estimated at USD 5.94 billion in 2025, and is expected to reach USD 7.99 billion by 2030, at a CAGR of 6.1% during the forecast period (2025-2030).

High-performance electronic systems use more and more high-performance data converters to improve and shape the architecture and open new application perspectives. The emerging circuits and systems techniques at the forefront of state-of-the-art modulators are pushing their performance forward and giving rise to new generations of data converters. Further, the current and future trend depends on old and new factors, including the global economy, technological evolution, and marketing.

Key Highlights

- Increasing adoption of technologically advanced data acquisition systems drives the market. The high rates of encoded information in multiple signals forced data acquisition (DAQ) systems to evolve from research work to modern engineering processes. The industry is evolving toward a trend of having a combination of modular hardware and flexible software, where these newer modular systems have appropriate signal conditioning and analog-to-digital conversion (ADC), with various interfacing sensors that support multiple data acquisition requirements.

- The traditional approach for performing specific DAQ tasks is not feasible, considering today's requirements. Thus, a market tends toward a more software-defined approach to DAQ and the emergence of high-speed USB-enabled DAQs.

- Furthermore, the growing demand for high-resolution images in scientific and medical applications is driving the market studied. Data converters constitute the most demanding challenge medical imaging imposes on the electronics design in terms of required dynamic range, resolution, accuracy, linearity, and noise. The ADC (analog to digital) must have a high resolution of at least 24 bits to achieve better and sharper images and a fast sampling rate to digitize detector readings that can be as short as 100 µs in a CT (computed tomography) solution. The ADC sampling rate must also enable multiplexing, which would allow the use of fewer converters as well as the reduction of the size and power of the entire system.

- A company such as Analog Devices addresses these requirements and offer highly integrated solutions for the key signal chain functional blocks to enable best-in-class clinical imaging equipment. Its products, such as ADAS1256 (X-ray applications), ADAS1135, ADAS1134 (CT applications), and many more, drive the market in medical applications.

- Further, the development of low-power consumption data converters challenges the market's growth. Power consumption is one of the leading design constraints in today's integrated circuits. Conversion of the low-frequency bioelectric signals does not require high speed but requires an ultra-low-power operation. This, combined with the required conversion accuracy, makes designing such ADCs a major challenge.

- Further, due to the impact of the COVID-19 pandemic, there is a high effect internationally on supply-demand in the semiconductor industry. For the development of data converters, there is a need for ICs, resistors, capacitors, etc. The breakage in the distribution channel holds slow growth for the data converter market. However, many central and local governments have recognized the strategic importance of the semiconductor industry and prioritized uninterrupted operations for their domestic companies and suppliers in the midst of mandated business closures.

Data Converter Market Trends

Telecommunication to Account for Significant Market Share

- Telecommunication infrastructure is stimulating market growth owing to the advent of 4G communication and the emerging 5G communication. Manufacturers of wireless infrastructure, especially 4G and 5G, are constantly reducing the size and cost of newly installed wireless infrastructure while holding to high standards of performance, functionality, and quality of service. The data conversion block is a critical function in wireless infrastructure designs. The analog-to-digital converter (ADC) is the fundamental block that digitizes the incoming intermediate frequency (IF) signal and then passes the digital data to the digital downconverter.

- The wide bandwidth demands of the 5G solution can be met by moving frequency translation and filtering from the analog to the digital domain. Two RF converters are part of this digitization wave: the AD9081/AD9082 mixed-signal RF converters, which analog devices introduce. They have been engineered to install multi-band radios in the same footprint as single-band ones, which helps to increase call capacity three-fold, compared to the call capacity available in today's 4G LTE base stations.

- Further, the radio architecture core must be tightly integrated for a 5G solution to support small antenna deployments. One solution is the traditional approach combining multi-Giga sample ADCs and DACs with a System-on-Chip (SoC). This approach provides the ability to perform the embedded system design and to address the increased required operating bandwidths. Several data converters implement interfaces using JESD204B.

- Also, over the past ten years, FPGA manufacturers like Xilinx have been improving technology by reducing the silicon fabrication structure size and, as a result, the device's size, weight, and power (SWaP) values. The latest system-on-chip (SoC) device from Xilinx, the RFSoC, consists of FPGA fabric with arm processors, analog-to-digital converters (ADCs), and digital-to-analog converters (DACs) all on the same chip.

- This 16-nm technology has over 4.2K DSP slices, four 1.5-GHz A53 Arm processors, two 600-MHz R5 ARM processors, eight 4-GHz, 12-bit ADCs, and eight 6.4-GHz, 14-bit DACs per device. COTS (Commercial-off-the-shelf) manufacturers can use this game-changing technology to provide multichannel, SDR transceivers for engineers developing 5G radio products.

North America to Hold the Largest Market Share

- North America holds the highest share due to the growth in the telecom sectors and the use of FPGA (field-programmable gate array). The rising demand for A2D converters in consumer electronics for high-resolution images has become an essential part of driving the market.

- Further, sensor applications in automotive that require data converters range from temperature sensors identifying different engine statuses to radar/LIDAR enabling automotive driver assistance systems (ADAS). Other data converters applications include wireless transceivers for communicating with other vehicles or fixed networks. The USD 7,500 per vehicle tax credit that has boosted EV sales in the United States is drafted to be repealed without any increment in the upper limit of the incentive.

- Also, tariff risk is compelling foreign companies to shop in North America. Volkswagen announced spending USD 800 million to build a manufacturing facility in Chattanooga, Tennessee. Further, Toyota and Mazda are joining forces to construct an assembly plant in Huntsville, Alabama. The factory, which costs about USD 1.6 billion, would have a production capacity of 300,000 units per year. These instances are expected to increase the data converter market's growth in the region's automotive segments.

- Further, IT and telecommunications applications were estimated to have the largest share of the data converter market in the United States. The growth is driven by the development of the 4G network, with superior modulation and antenna methods for improved voice and data services, which enhances the demand for the AMS blocks.

- Further, according to GSMA, in the United States, the 5G adoption rate as a share of mobile connections is expected to increase by 33%, 40%, and 46% in the coming three years, respectively. This further enhances the growth of applications in 5G for data converters.

Data Converter Industry Overview

The data converter market is fragmented as the global players integrate signals in various applications like consumer electronics and automotive, which gives an intense rivalry among the competitors. Key players are Analog Devices, Inc., Microchip Technology Inc., etc.

- May 2022: Analog Devices Inc. introduced a new portfolio of next-generation 16- to 24-bit, ultrahigh-precision SAR ADCs to simplify the complicated process of designing ADCs for instrumentation, industrial, and healthcare applications. The patented Easy Drive technology and the adaptable Flexi-SPI serial peripheral interface (SPI) of ADI are two aspects of the new high-performance SAR ADC series that address system design issues and increase the range of directly compatible companion products.

- September 2022: MaxLinear Inc. and RFHIC announced a collaboration to develop a 400MHz Power Amplifier (PA) solution for 5G Macrocell Radios that is production-ready. This solution will use MaxLinear MaxLIN Digital Predistortion (DPD) and Crest Factor Reduction (CFR) technologies to enhance the performance of RFHIC's newest ID-400W series GaN RF Transistors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Technologically Advanced Data Acquisition Systems

- 5.1.2 Growing Demand for High-Resolution Images in Scientific and Medical Applications

- 5.2 Market Challenges

- 5.2.1 Challenges in the Development of Low-power Consumption Data Converters

- 5.3 Impact of the COVID-19 Pandemic in Supply Chain Distribution of Semiconductors Globally

6 KEY TECHNOLOGY INVESTMENTS

- 6.1 Cloud Technology

- 6.2 Artificial Intelligence

- 6.3 Cyber Security

- 6.4 Digital Services

7 MARKET SEGMENTATION

- 7.1 By Type

- 7.1.1 Analog to Digital Converter

- 7.1.2 Digital to Analog Converter

- 7.2 By End User

- 7.2.1 Automotive

- 7.2.2 Telecommunication

- 7.2.3 Consumer Electronics

- 7.2.4 Industrial

- 7.2.5 Medical

- 7.2.6 Other End Users

- 7.3 Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 Germany

- 7.3.2.2 United Kingdom

- 7.3.2.3 France

- 7.3.2.4 Italy

- 7.3.2.5 Rest of Europe

- 7.3.3 Asia-Pacific

- 7.3.3.1 India

- 7.3.3.2 China

- 7.3.3.3 Japan

- 7.3.3.4 Rest of Asia-Pacific

- 7.3.4 Rest of the World

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Analog Devices Inc.

- 8.1.2 Microchip Technology Inc.

- 8.1.3 STMicroelectronics NV

- 8.1.4 NXP Semiconductors NV

- 8.1.5 Texas Instruments Incorporated

- 8.1.6 Mouser Electronics Inc.

- 8.1.7 DATEL Inc.

- 8.1.8 Synopsys Inc.

- 8.1.9 Cirrus Logic Inc.

- 8.1.10 Maxim Integrated Products Inc.