|

市場調査レポート

商品コード

1644411

OpenStackサービス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)OpenStack Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| OpenStackサービス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

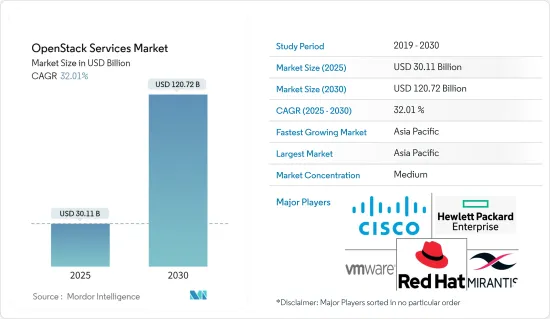

OpenStackサービスの市場規模は、2025年に301億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは32.01%で、2030年には1,207億2,000万米ドルに達すると予測されます。

従量課金モデルの採用が拡大していることや、仮想環境(すべてのワークロードをクラウドベンダーが引き受ける)でのコスト効率の高いITインフラ開拓が、OpenStackサービスの世界の市場成長を促進すると予想される要因です。

主なハイライト

- 世界中の企業がクラウドサービスの導入に傾いています。クラウド大手のオラクルは、クラウド関連サービスの提供により、2025年までに企業のビジネス機能の80%がクラウドに移行すると予測しています。近年、クラウド・サービス・プロバイダーは、プロフェッショナル・サービスやその他のクラウド・サービスにより、莫大な収益と利益を上げています。最も急成長しているクラウド・サービス・プロバイダーのひとつであるマイクロソフトは、2022年にアジュールとその他のクラウド・サービスで前年比31%の成長を記録しました。

- クラウドと産業化サービスの成長と従来のデータセンター・アウトソーシング(DCO)の衰退は、ハイブリッド・クラウド・インフラ・サービスへの大転換を示しています。これにより、クラウドIaaSとホスティングへのシフトが進むと予想されます。専門的なクラウドの導入は、その利点から、これらの市場セグメントで需要の向上が見込まれます。

- IaaS(Infrastructure-as-a-Service)は、クラウドサービスのスペクトルの中で3番目(最下位)のレベルと考えられており、ベンダーはクラウド上のストレージ、サーバー、ネットワーク、その他のコンピューティング・リソースへの従量課金制のアクセスなどのソリューションをクライアントに提供します。IaaSのハードウェアは通常、外部のプロバイダーによって提供され、組織で管理されます。

- Moroever , October 2023-Ironicは、インフラ事業者が「サービス・ステップ」フレームワークを使用して既存のノードを変更するためのローンチを発表しました。サービス・ステップを利用することで、オペレータは、クリーニングやカスタマイズされたデプロイメントのようにステップを活用し、ACTIVE状態でデプロイされたノードを変更するアクションを実行することができます。

- OpenStackはダイナミックでオープンなクラウドコンピューティングソリューションであり、定期的なアップグレードが必要です。新しい機能や特徴は定期的に追加され、古い機能は削除されます。このように非常にダイナミックな機能範囲は、市場の成長にとって課題となる可能性があります。

OpenStackサービス市場の動向

通信分野でのOpenStackサービス利用の増加が市場を牽引

- 通信業界はここ数年、大きな成長を遂げています。通信会社は、競争の激しい市場で顧客を維持するために、革新的なサービスを低コストで提供しなければならないというプレッシャーに常にさらされています。OpenStackを利用することで、通信事業者はプロプライエタリなソリューションに伴う高いコストをかけずに、クラウドインフラストラクチャの導入と管理を行うことができます。

- OpenStackはオープンソースのシステムで、仮想リソースのプールを通じてプライベート・クラウドやパブリック・クラウドを構築・管理できます。コンピュート、ネットワーキング、ストレージ、アイデンティティ、イメージなどのコアとなるクラウド・コンピューティング・サービスは、OpenStackプラットフォームの「プロジェクト」を構成するツールによって処理されます。この機能は、サービス提供と運用効率の向上を目指す通信事業者にとって極めて重要です。

- 通信事業者が選択する基盤として、OpenStackはネットワーク機能仮想化NFVとして選ばれています。OpenStackによるNFVは、幅広い通信事業者やビジネスリーダーに選ばれています。AT&T、Bloomberg LP、China Mobile、Deutsche Telekom、Nippon Telegraph &Telephone Corporation、SK Telecom、Verizonなどがその一例です。

- さらに、5Gなどのワークロードを含むOpenStackは、最大のモバイル通信ネットワークの電源として使用されています。チャイナ・モバイルのモバイル・ネットワークは、300万以上の基地局と8億人の加入者を擁し、5万台以上のサーバーを備えた現在最大のNFVネットワークは、チャイナ・モバイルがOpenStackを使って構築したものです。

アジア太平洋地域は大幅な成長が見込まれる

- 中国のハイパースケールクラウドや通信事業者の大半は、アジア太平洋地域全体でOpenStackサービスの採用を主導しています。OSFは、TencentやChina Mobileといった企業によるOpenStackの利用を挙げ、これらの企業はアジア太平洋地域で急成長するOpenStack市場で重要な役割を果たしていると述べた。

- スーパーアプリ「WeChat」を運営し、ハイパースケールクラウドのサプライヤーでもあるテンセントは、さまざまな業界で利用されている業務や公開クラウドサービスの電源としてOpenStackを利用しています。また、チャイナ・モバイルでは、OpenStackがパブリックおよびプライベート・クラウド・サービスと、次世代通信ネットワークを支えるテレコム・クラウドの提供に利用されています。

- この地域のユーザーは、OpenStackとKubernetesを組み合わせて、オープンなインフラストラクチャの大きな問題を解決しようとしています。AirshipやStarlingXのようなプロジェクトをますます活用し、オープンでコンポーザブルなインフラを使用して、この地域で運用されるアプリケーションの需要に応えています。

- 世界のOpenStackデプロイメントのほぼ半分を占めると予想される中国は、OSF(同組織が試験的にホスティングするオープンインフラプロジェクトのユーザーと貢献者で構成される組織)のメンバー数が3番目に多いです。チャイナモバイルは、OpenStackを主要なクラウド展開技術の1つとして、AUTOと呼ばれる自動テストプラットフォームを構築しました。スケーラビリティとパフォーマンスに重点を置き、AUTOはOpenStack SDKと既存のテストツールを広範囲に活用して、クラウド展開を評価・確認しました。

- 99cloud、中国銀聯、FiberHomeなど、複数の中国企業がStarlingXプロジェクトの上流に貢献しています。例えば、中国銀聯の電子商取引・電子決済国家工程研究所は、非接触決済のユースケースのために、StarlingXを搭載した安全なエッジインフラを研究しています。5Gの進化に伴い、マルチアクセスエッジコンピューティング(MEC)、メディアクラウドなどの技術が登場しています。

- 5Gネットワークインフラの急速な成長とともに、人工知能(AI)が強く台頭してきました。開発を完全にサポートするためには、インフラ自体がクラウド・ネイティブなサービスとして進化する必要があります。韓国を拠点とするSKテレコムは、過去数年にわたりクラウドネイティブなインフラ技術を開発しており、OpenStack Foundation(OSF)、特にOSFのAirshipプロジェクトの両方の世界プロジェクトに積極的に参加しています。

OpenStackサービス業界の概要

OpenStackサービス市場は、以下のような重要なプレーヤーが存在するため、半固体化しています。 Cisco Systems, Inc., Red Hat, Inc., Hewlett Packard Enterprise Development LP, Mirantis, Inc., etc. The players in the market are frequently launching innovative solutions, forming partnerships, and mergers to increase their market share and expand their geographical presence.

203年6月、オープンソース・ソリューションの世界の大手プロバイダーの1つであるNokiaとRed Hat, Inc.は、Nokiaのコア・ネットワーク・アプリケーションをRed Hat Openstack PlatformおよびRed Hat OpenShiftと緊密に統合することで合意したと発表しました。この合意の一環として、ノキアとレッドハットは、既存のNokia Container Services(NCS)とNokia CloudBand Infrastructure Software(CBIS)の顧客を共同でサポートし、進化させながら、時間をかけてレッドハットのプラットフォームに移行する道筋を開発します。さらに、ノキアはレッドハットのインフラストラクチャー・プラットフォームを活用することで、ノキアの広範なコアネットワーク・ポートフォリオの迅速な開発とテストを可能にします。

2022年10月、レッドハットはMWCラスベガスのイベントでOpenStack Platform 17を発表しました。これは、サービスプロバイダーが拡張性の高い次世代ネットワークを構築する際に役立つ、オープンなハイブリッドクラウドアーキテクチャに焦点を当てた幅広い改良をカバーするものです。

2022年6月、エリクソンとレッドハットはソリューションを展開するための提携を発表し、vEPC、5Gコア、IMS、OSS、BSSのネットワーク全体に拡張されたオープンプラットフォームでサービスプロバイダに力を与えました。チームは、エリクソンのネットワーク機能ソリューションをRed Hat OpenShiftおよびRed Hat OpenStack Platformと統合しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19による影響評価

- 市場促進要因

- ビジネスの俊敏性と効率性を向上させる組織のニーズの高まり

- オープンソースであるOpenStackはカスタマイズソリューションの柔軟性を提供する

- 通信分野におけるOpenStackサービスの利用の増加

- 市場抑制要因

- 可用性やセキュリティといったIT管理機能を含め、企業がデータセンターに求める堅牢性の欠如

- 技術スナップショット

- OpenStackアプリケーションの管理に利用されるフレームワーク

- OpenStack Foundationが主催し、試験運用されているオープン・インフラストラクチャ・プロジェクト

- 組織横断的なOpenStackの使用事例

第5章 市場セグメンテーション

- 展開モデル別

- オンクラウド

- オンプレミス

- エンドユーザー業界別

- IT

- 通信

- 銀行・金融サービス

- 学術

- 小売/eコマース

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Cisco Systems, Inc.

- Red Hat, Inc.

- Hewlett Packard Enterprise Development LP

- VMware, Inc.

- Mirantis, Inc.

- Canonical Ltd.

- Dell Inc.

- Rackspace US, Inc.

- Huawei Technologies Co., Ltd.

- NetApp, Inc.

第7章 投資分析

第8章 市場の将来

The OpenStack Services Market size is estimated at USD 30.11 billion in 2025, and is expected to reach USD 120.72 billion by 2030, at a CAGR of 32.01% during the forecast period (2025-2030).

The growing adoption of the pay-as-you-go model and the cost-effective IT infrastructure development in a virtual environment (where every workload is taken care of by the cloud vendors) are certain factors expected to drive market growth for OpenStack services globally.

Key Highlights

- Enterprises across the world are inclined towards the adoption of cloud services. Oracle Corporation, the cloud giant, has predicted that owing to the cloud-related service offerings, 80% of the enterprise business functions will move to the cloud by 2025. In recent years, cloud service providers have experienced huge revenues and profit gains due to their professional and other cloud services. Microsoft, one of the fastest-growing cloud service providers, registered a year-on-year growth of 31% in Azure and other cloud services in 2022.

- The growth of cloud and industrialized services and the decline of traditional data center outsourcing (DCO) indicate a massive shift toward hybrid cloud infrastructure services. This is expected to drive the shift toward cloud IaaS and hosting. Owing to its benefits, professional cloud deployment is expected to experience an improved demand for these market segments.

- Infrastructure-as-a-Service (IaaS) is considered the third (lowest) level in the spectrum of cloud services, where a vendor provides clients with solutions such as pay-as-you-go access to storage, servers, networking, and other computing resources in the cloud. IaaS hardware is usually offered and managed by the organization by an external provider.

- Moroever , October 2023 - Ironic has announced the launch of infrastructure operators to modify existing nodes using the "service steps" framework. Servicing allows operators to leverage steps, like you would for cleaning or customized deployments, to perform actions to modify deployed nodes in an ACTIVE state.

- OpenStack is a dynamic and open cloud-computing solution that needs to be upgraded regularly. The new functions & features are added regularly, and other old functions are removed. This high-dynamic range of functions may create challenges for market growth.

OpenStack Services Market Trends

Increasing use of OpenStack Services Across Telecommunication Sector is Driving the Market

- The telecom industry has observed extensive growth during the past few years. Telecommunication companies are encountering constant pressure to deliver innovative services at lower costs to retain their customers in the competitive market. It allows telecom companies to deply and manage their cloud infrastructure without the high costs associated with proprietary solutions.

- OpenStack is an open source system that allows private and public clouds to be built and managed through a pooling of virtual resources. The core clouds computing services, such as compute, networking, storage, identities and images are handled by tools that comprise the OpenStack platform 'projects'. This capability is crucial for telecom operators looking to enhance their service offerings and operational efficiency.

- As a base of choice for operators, OpenStack has been chosen as their Network Function Virtualization NFV. NFV with OpenStack has been chosen by a wide range of telecom operators and business leaders. AT&T, Bloomberg LP., China Mobile, Deutsche Telekom, Nippon Telegraph & Telephone Corporation, SK Telecom and Verizon are among them.

- Moreover, OpenStack, including workloads such as 5G, has been used to power the biggest mobile telecommunications network. The mobile network of China Mobile has over 3 million base stations and 800 million subscribers an With over 50,000 servers, the largest Network of NFV today is built by China Mobile using OpenStack.

Asia-Pacific is Expected to Hold Significant Growth

- The majority of hyperscale cloud and telecom organizations in China are taking charge of adopting OpenStack services across the Asia Pacific region. Citing the use of OpenStack by companies such as Tencent and China Mobile, the OSF said these companies play a critical role in the rapidly growing OpenStack market in Asia-Pacific.

- Tencent, the company behind the WeChat super app and hyperscale cloud supplier, has been using OpenStack to power its operations and public cloud services that are being used by different industries. Also, at China Mobile, OpenStack is being used to deliver public and private cloud services and its telecom cloud to power its next-generation telco network.

- Users throughout the region are combining OpenStack and Kubernetes to solve big open infrastructure problems. They're increasingly leveraging projects like Airship and StarlingX, using open, composable infrastructure to meet the demands of applications operating in the region.

- China, which is expected to account for almost half of the world's OpenStack deployments, has the third-highest number of members in the OSF, an organization comprising users and contributors to the open infrastructure projects piloted and hosted by the organization. China Mobile has created an automated testing platform dubbed AUTO with OpenStack as one of its primary cloud deployment technologies. With an emphasis on scalability and performance, AUTO extensively utilized the OpenStack SDK and pre-existing testing tools to evaluate and confirm the cloud deployment.

- Multiple Chinese companies contribute upstream to the StarlingX project, including 99cloud, China UnionPay, and FiberHome. For instance, the Electronic Commerce and Electronic Payment National Engineering Laboratory of China UnionPay has researched a secured edge infrastructure powered by StarlingX for a contactless payment use case; with the evolution of 5G, technologies such as Multi-Access Edge Computing (MEC), Media Cloud.

- Artificial Intelligence (AI) has strongly emerged along with rapid growth in 5G network infrastructure. The infrastructure itself must evolve as a cloud-native service to fully support the development. Korea-based SK Telecom has been developing cloud-native infrastructure technology for the past few years and actively participates in global projects both in OpenStack Foundation (OSF), especially the Airship project in OSF.

OpenStack Services Industry Overview

The OpenStack Services Market is semi-consolidated due to the presence of significant players such as Cisco Systems, Inc., Red Hat, Inc., Hewlett Packard Enterprise Development LP, Mirantis, Inc., etc. The players in the market are frequently launching innovative solutions, forming partnerships, and mergers to increase their market share and expand their geographical presence.

In June 203, Nokia and Red Hat, Inc., one of the leading global providers of open-source solutions, announced that they had agreed to tightly integrate Nokia's core network applications with Red Hat Openstack Platform and Red Hat OpenShift. As part of the agreement, Nokia and Red Hat would jointly support and evolve existing Nokia Container Services (NCS) and Nokia CloudBand Infrastructure Software (CBIS) customers while developing a path to migrate to Red Hat's platforms over time. Additionally, Nokia would leverage Red Hat's infrastructure platforms to enable faster development and testing of Nokia's extensive core network portfolio.

In October 2022, RedHat announced the launch of OpenStack Platform 17 at the MWC Las Vegas event, covering a wide range of improvements with a focus on open hybrid cloud architectures that are meant to aid service providers as they construct expansive next-generation networks.

In June 2022, Ericsson and Red Hat announced the partnership to deploy solutions, empowering service providers with an open platform that extended across a network for vEPC, 5G Core, IMS, OSS, and BSS. The team integrated Ericsson's network function solutions with Red Hat OpenShift and Red Hat OpenStack Platform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment on the Impact due to COVID-19

- 4.4 Market Drivers

- 4.4.1 Increasing Need for Organizations to Improve Their Business Agility and Efficiency

- 4.4.2 OpenStack Being Open Source Provides the Flexibility for Customized Solution

- 4.4.3 Increasing use of OpenStack Services in Telecommunication Sector

- 4.5 Market Restraints

- 4.5.1 Lack of Robustness that Enterprises Desire for Their Data Centers, Including IT Management Features, Such as Availability and Security

- 4.6 Technology Snapshot

- 4.6.1 Frameworks Utilized to Manage OpenStack Applications

- 4.6.2 Open Infrastructure Projects Hosted and Piloted by OpenStack Foundation

- 4.6.3 Use Cases of OpenStack Across Organizations

5 MARKET SEGMENTATION

- 5.1 By Deployment Model

- 5.1.1 On-Cloud

- 5.1.2 On-Premise

- 5.2 By End-user Industry

- 5.2.1 Information Technology

- 5.2.2 Telecommunication

- 5.2.3 Banking and Financial Services

- 5.2.4 Academic

- 5.2.5 Retail/E-Commerce

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems, Inc.

- 6.1.2 Red Hat, Inc.

- 6.1.3 Hewlett Packard Enterprise Development LP

- 6.1.4 VMware, Inc.

- 6.1.5 Mirantis, Inc.

- 6.1.6 Canonical Ltd.

- 6.1.7 Dell Inc.

- 6.1.8 Rackspace US, Inc.

- 6.1.9 Huawei Technologies Co., Ltd.

- 6.1.10 NetApp, Inc.