|

市場調査レポート

商品コード

1644393

サービスフルフィルメント-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Service Fulfillment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サービスフルフィルメント-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

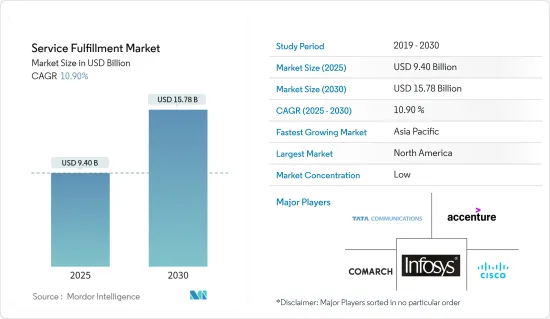

サービスフルフィルメント市場規模は2025年に94億米ドルと推定され、2030年には157億8,000万米ドルに達すると予測され、市場推定・予測期間(2025~2030年)のCAGRは10.9%です。

サービスプロバイダーは、次世代製品やサービスの市場投入期間を短縮しながらサービスを提供する能力を構築しています。IoT、コネクテッドデバイス、5G技術、デジタル化、強化された接続ソリューションの需要増加などの技術があります。

主要ハイライト

- サービスフルフィルメントとは、CSPや組織のさまざまなタスクを合理化し、市場投入までの時間を短縮し、コストを最適化し、自動化を促進するための総合的なツールセットです。ネットワークの最適化は、新しく増大するサービスフルフィルメントのニーズに対応するために不可欠となります。

- ダイナミックなサービスフルフィルメントプロセスやソフトウェアは、コンポーネント・ベースのサービスの作成を可能にし、新製品の発売を簡素化します。受注から現金化までのプロセスを自動化し、サプライチェーン活動、資本支出、営業経費を最適化します。サプライチェーン管理ソリューションは、サプライヤーのエコシステムを合理化しながら、ネットワーク機器の調達を合理化します。

- 急速な接続機器とユーザーの拡大が、世界のサービスフルフィルメント市場を牽引しています。さらに、電気通信運用技術への大規模な支出が、この産業における需要を高めています。さらに、重要な管理ソリューションへの簡単なアクセスが、この産業を前進させています。データサービスによる収入の増加が、世界のサービスフルフィルメント市場の需要を牽引しています。

- さらに、自動化はビジネスの生産性を向上させ、これは常に望ましいことです。課題は、それをコスト効率よく実現することです。クラウドは、サーバーの仮想化や設定など、ITインフラの自動化と利用を効率的に合理化してきました。しかし、ネットワークの自動化は、特に通信サービスプロバイダー(CSP)のネットワークでは、多くのドメイン(クラウド、モバイル、WAN、IT)を横断することが多く、より高いレベルの投資を必要とするため、複雑さが増し、進化が遅れています。

- COVID-19の大流行は、世界中のサービスフルフィルメントに影響を与えました。パンデミック時の主要課題は、労働力関連の問題でした。パンデミック後は、仮想化されたネットワーク機能が顧客サービス創造に使用可能なコンポーネントとして急速に採用され、市場は急成長しました。

サービスフルフィルメント市場の動向

ソフトウェアセグメントが大きな市場シェアを占めると分析

- ネットワーク管理、在庫管理、サービスオーダー管理などのソフトウェアセグメントが、予測期間中、サービスフルフィルメント市場で大きなシェアを占めると分析されています。5G技術、IoT、AI、デジタル化など、いくつかの技術的進歩が展開される中、通信サービスプロバイダ(CSP)は、プラットフォーム、システム、ツール、セグメント化されたデータなどの可視性がほとんどない中で、運用コストを最小限に抑えつつ、高まる顧客の期待を上回り、強化するという絶え間ないプレッシャーに直面しています。

- Ericssonによると、5Gの契約数は2028年までに世界全体で46億2,411万件に増加すると予測されており、北東アジア、東南アジア、インド、ネパール、ブータンが地域別契約数で最大となる見込みです。ユーザー数の増加、5G接続、接続デバイス、モバイルデバイス、アプリケーション、先進的技術や機能の展開に伴い、さまざまなエンドポイントへの接続に不可欠な、強化されたネットワークインフラと強化された接続ソリューションへの依存度が高まっている

- その後、組織やCSPは、AIやMLなどの技術を活用した自律型ネットワークの導入を推進するため、先進的管理ツールを組み込んだ新しいネットワークアーキテクチャへの投資を増やしています。そのため、CSPはソフトウェアソリューションを採用することでサプライチェーン活動を強化するため、サービスフルフィルメントソリューション・プロバイダーにコンタクトを取っています。

- 市場のもう1つの動向は、ネットワークトラフィックとネットワーク処理の増加によるネットワークの継続的な評価とパフォーマンスに対する需要であり、特にローカル・エリア・ネットワークではリアルタイムのストリーミング・ネットワーク分析が必要とされ、顧客はネットワークの健全性を把握し、トラフィック・フローを継続的にモニタリングすることができます。このような開発は、市場におけるネットワーク管理ソフトウェアの需要をさらに促進しています。

北米が最大の市場規模を記録する見込み

- 北米地域では、ビデオストリーミング、ビデオ通話プラットフォーム、電話会議など、さまざまなプラットフォームにおける接続ソリューションの強化に対する需要が増加しているため、サービスフルフィルメントソリューションとサービスに対する需要が増加しています。

- これは、3G、4G、5Gなどの様々なネットワークにおける加入者の急増と相まって、サービスフルフィルメントを採用する参入企業を後押ししています。また、この地域は5G展開の主要拠点となっており、カナダのサービスプロバイダーは5Gライセンス調達への投資を増やしています。

- 市場ベンダーは、同地域でのサービスフルフィルメント提供を強化するため、提携や買収活動に乗り出しており、これが同地域の市場成長を促進すると分析されています。例えば、2023年5月、技術主導の物流プラットフォームであるFlexportは、Deliverr, Inc.を含むShopify Logisticsの資産を買収しました。Shopify Logisticsの統合により、同社はAIを活用した先進的最適化を強化し、世界サプライチェーンの合理化、コスト削減、消費者の信頼性向上を実現します。

- さらに、2022年12月、JLLとAmerican Eagle Outfitters Inc.の完全子会社であるQuiet Platformsは、Quiet Platformsのサプライチェーンネットワークに加盟する小売業者やブランドにサービスを提供するため、2023年に米国全土で先進的なフルフィルメント施設の追加建設を加速させる協業を発表しました。両社はこの契約により、物流不動産の柔軟な収益歩合賃料モデルを開拓することになります。

サービスフルフィルメント産業概要

サービスフルフィルメント市場は、Comarch SA、Accenture PLC、Cisco Systems, Inc.、Infosys Limited、TATA Communications Ltd.などの参入企業が存在し、セグメント化されています。同市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

2023年12月、Infosysは、インフォシスと構築したオムニチャネル・デジタルフルフィルメントと先進的分析プラットフォームを通じて、Spotlight Retail Groupの消費者成長強化を支援し、InfosysのAIファースト・オファリングであるInfosys Topazを活用することで、Spotlight Retail Groupが消費者に超パーソナライズされたオンラインショッピング体験を可能にしたと発表しました。顧客体験の向上により、12ヶ月間で顧客数は113%、取引件数は93%増加しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- ネットワークの自動化と自動化されたリアルタイムサービスに対する需要の増加

- 仮想化されたネットワーク機能の、顧客サービス創出のための利用可能なコンポーネントへの急速な採用

- 市場抑制要因

- 認識不足

第6章 市場セグメンテーション

- タイプ別

- ソフトウェア

- ネットワーク管理

- 在庫管理

- サービスオーダー管理

- サービス別

- ソフトウェア

- 導入形態別

- オンプレミス

- ホスト型

- 地域別

- 北米

- 欧州

- アジア太平洋

- その他

第7章 競合情勢

- 企業プロファイル

- Comarch SA

- Accenture PLC

- Cisco Systems, Inc.

- Infosys Limited

- TATA Communications Ltd.

- Amdocs Group

- Suntech S.A.

- Telefonaktiebolaget LM Ericsson

- NEC Technologies India Private Limited

- Hewlett Packard Enterprise Development LP

- TIBCO Software Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Service Fulfillment Market size is estimated at USD 9.40 billion in 2025, and is expected to reach USD 15.78 billion by 2030, at a CAGR of 10.9% during the forecast period (2025-2030).

Service providers are building capabilities to provide services while reducing time-to-market for next-generation products and services, owing to the introduction of several technologies across industries. Technologies such as IoT, connected devices, 5G technology, digitization, and increase the demand for enhanced connectivity solutions.

Key Highlights

- Service fulfillment is a combined comprehensive set of tools that assist in streamlining various tasks of CSPs and organizations to reduce time to market, optimize cost, and boost automation. Network optimization becomes essential to meet new and growing service fulfillment needs.

- A dynamic service fulfillment process or software enables the creation of component-based services and simplifies the launch of new products. It automates the order-to-cash process to optimize supply chain activities, capital expenditures, and operating expenses. The supply chain management solutions streamline network equipment procurement while rationalizing the supplier ecosystem.

- Rapid connectivity devices and user expansion drive the global service fulfillment market. Moreover, large-scale expenditures in telecom operating technologies are increasing in demand in this industry. Moreover, simple access to crucial management solutions is propelling this industry forward. Rising income from data services drives demand in the global service fulfillment market.

- Further, automation drives business productivity, which is always desirable. The challenge is achieving it cost-effectively. The cloud has efficiently streamlined the automation and use of IT infrastructures, such as server virtualization and configuration. Still, network automation has been slower to evolve due to higher complexity levels, especially among communication service provider (CSP) networks, which often cross an increased number of domains (cloud, mobile, WAN, and IT) and require higher levels of investment.

- The COVID-19 pandemic impacted service fulfillment throughout the globe. The major challenge during the pandemic was workforce-related issues. Post-pandemic, the market was growing rapidly with the rapid adoption of virtualized network functions into usable components for customer service creation.

Service Fulfillment Market Trends

Software Segment is Analyzed to Hold Significant Market Share

- The software segment including network management, inventory management and service order management is analyzed to hold significant market share in th service fulfillment market over the forecast period. The rollout of several technological advancements, such as 5G technology, IoT, AI, Digitization, and many more, Communication Service Providers (CSPs) face constant pressure to enhance and exceed rising customer expectations while minimizing operational costs, with little visibility across platforms, systems, tools, and fragmented data.

- According to Ericsson, 5G subscriptions are forecast to increase globally to 4624.11 million by 2028, North East Asia, South East Asia, India, Nepal, and Bhutan are expected to have the maximum regional subscriptions.With the increasing number of users, 5G connections, connected devices, mobile devices, applications, and the deployment of advanced technologies and capabilities, they are increasing their dependence on enhanced network infrastructure and enhanced connectivity solutions for essential connectivity to a wide range of endpoints.

- Subsequently, organizations and CSPs are increasingly investing in new network architectures that incorporate advanced management tools to drive the adoption of autonomous networks, leveraging technologies like AI and ML. Hence, the CSPs are contacting Service Fulfillment solution providers to enhance their supply chain activities by adopting software solutions.

- Another trend in the market is the demand for continuous evaluation and performance of networks due to increased network traffic and network processing, particularly from the local area networks, which require real-time streaming network analytics and allows customers to keep track of the health of their network and continuously monitor traffic flows. Such developments further fosters the demand for network management software in the market.

North America is Expected to Register the Largest Market

- The North America region is witnessing an increase in the demand for service fulfillment solutions and services due to an increase in the demand for enhanced connectivity solutions across various platforms, such as video streaming, video calling platforms, and teleconferencing, among various others.

- This, coupled with a rapid increase in subscribers on various networks such as 3G, 4G, 5G, etc., propel the players to adopt service fulfillment. Also, the region has become a major hub for the 5G rollout, with Canadian service providers increasingly investing in procuring 5G licenses.

- Market vendors are entering into partnership and acquisition activities to strengthen their service fulfillment offerings in the region, which is analyzed to drive the market growth in the region. For instance, in May 2023, Flexport, the tech-driven logistics platform, acquired the assets of Shopify Logistics, including Deliverr, Inc. Through the integration of Shopify Logistics, the company will strengthen its advanced AI-driven optimization to streamline the global supply chain, reducing costs and improving consumer reliability.

- Furthermore, in December 2022, JLL and Quiet Platforms, an American Eagle Outfitters Inc. completely owned subsidiary, announced a collaboration to speed the building of additional advanced fulfillment facilities across the United States in 2023 to service retailers and brands in the Quiet Platforms supply chain network. The two businesses would pioneer a flexible rent-as-a-percentage-of-revenue model for logistics real estate under the terms of the agreement.

Service Fulfillment Industry Overview

The Service Fulfillment Market is fragmented with the presence of several players like Comarch SA, Accenture PLC, Cisco Systems, Inc., Infosys Limited, and TATA Communications Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In December 2023 - Infosys announced that it has helped enhance Spotlight Retail Group's consumer growth via an omnichannel digital fulfillment and advanced analytics platform built with Infosys and by leveraging Infosys' AI-first offering, Infosys Topaz, Spotlight Retail Group enabled a hyper-personalized online shopping experience for its consumers. The improved customer experience has led to a growth of 113% in customer base over 12 12-month period and 93% in transactions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Network Automation and Increasing Demand for Automated, Real-time Services

- 5.1.2 Rapid Adoption of Virtualized Network Functions into Usable Components for Customer Service Creation

- 5.2 Market Restraints

- 5.2.1 Lack in Awareness

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Software

- 6.1.1.1 Network Management

- 6.1.1.2 Inventory Management

- 6.1.1.3 Service Order Management

- 6.1.2 Services

- 6.1.1 Software

- 6.2 By Deployment Mode

- 6.2.1 On-Premise

- 6.2.2 Hosted

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Comarch SA

- 7.1.2 Accenture PLC

- 7.1.3 Cisco Systems, Inc.

- 7.1.4 Infosys Limited

- 7.1.5 TATA Communications Ltd.

- 7.1.6 Amdocs Group

- 7.1.7 Suntech S.A.

- 7.1.8 Telefonaktiebolaget LM Ericsson

- 7.1.9 NEC Technologies India Private Limited

- 7.1.10 Hewlett Packard Enterprise Development LP

- 7.1.11 TIBCO Software Inc.