|

市場調査レポート

商品コード

1644369

石油・ガスエンジニアリングサービス:市場シェア分析、産業動向、成長予測(2025年~2030年)Oil & Gas Engineering Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 石油・ガスエンジニアリングサービス:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

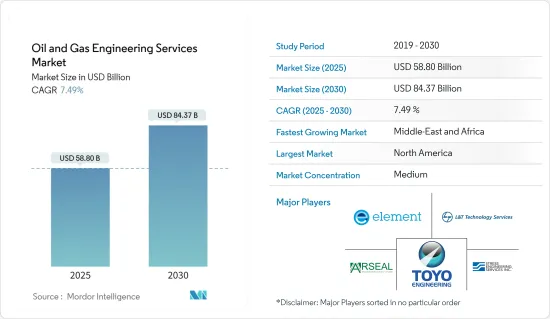

石油・ガスエンジニアリングサービス市場規模は、2025年に588億米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは7.49%で、2030年には843億7,000万米ドルに達すると予測されます。

石油・ガスセクターにおける様々な自動化技術の採用が増加していることが、エンジニアリングサービス市場を飛躍的に高める主要因となっています。

主要ハイライト

- 産業のダイナミックな性質により、生産性と効率性、稼働時間、資産収益率を向上させる必要性が高まっています。同時に、コストを最小限に抑えることが、同産業におけるエンジニアリングサービスの採用を促進すると推定されます。

- さらに石油・ガス産業は、再生可能エネルギーの普及拡大、厳しいカーボンフットプリント規制、電気自動車、さまざまな新しい炭化水素源などの課題に直面しています。したがって、企業はこれらの課題を克服するために、様々な戦略的インダストリー4.0戦略を採用しています。

- 機械学習、分析、その他多くの技術の先進的応用は、石油・ガス会社がビッグデータセットを分析し、意味のある洞察を提供するのに役立ち、支援することが期待されています。したがって、産業内でのエンジニアリングサービスの採用は、予測期間中に増加すると予想されます。

- また、市場拡大への有利な道として、参入企業間の様々な戦略的提携が確認されています。例えば、2023年4月には、エネルギー企業のBlueNord(Noreco Oil Denmark ASまたはNorecoとしても知られる)とエンジニアリングと請負会社のSemco Maritime ASが、石油・ガスセグメントにおける事業機会を共同で特定、探索、調査するための戦略的パートナーシップ契約を締結しました。

- しかし、運用やコンプライアンスに関連する課題の増大、石油・ガス価格の変動、産業内のその他のマクロ経済変動は、予測期間を通じて市場全体の成長を制限する重大な懸念材料となる可能性があります。

石油・ガスエンジニアリングサービス市場の動向

下流セグメントが大幅な成長を示す

- 石油・ガス産業の下流部門は、主に建設段階から販売段階に至るまでに発生する業務を含みます。石油製品の加工、精製、輸送、販売といった下流プロセスが含まれます。安全で信頼性の高い操業と総経費削減に対する需要の高まりが、石油・ガス下流サービスの産業全体の採用を促進すると予想されます。

- 石油・ガス下流サービスは、精製プロセス全体の強化において非常に重要な役割を果たすと同時に、最終製品の市場性や望ましさにも影響を与えます。下流サプライチェーンには、製品によるマーケティング、効果的なデータベース管理、効果的な流通管理といった注目すべき業務が含まれます。

- さらに、石油・ガスの主要な下流サービスには、資産完全性管理、石油検査、工業技術検査、精製・流通、危険場所設備検査、データベースソフトウェアソリューションが含まれます。また、中核となる資産情報管理に対応する企業資産管理(EAM)ソリューションや、プラント資産メンテナンス管理に関わるアプリケーションも含まれます。

- BP International Limitedによると、BPの下流事業セグメントは2022年に約1,886億米ドルの総収入を生み出しています。

北米が市場を独占する見込み

- 北米は石油・ガスエンジニアリングサービス市場を独占すると予想されています。特にカナダや米国などの国々で石油・ガスプロジェクトが増加しているためです。米国エネルギー情報局による2023年1月の短期エネルギー展望によると、米国全体の原油生産量は2023年に平均1,240万バレル/日、2024年には1,280万バレル/日となり、2019年に記録した1,230万バレル/日を上回ると予測されています。

- 同地域では、石油・ガス産業が提供する機会をつかむ有利な方法として、戦略的提携も数多く見られます。例えば、2023年3月、米国エネルギー省(DOE)は、Project Innerspace、国際石油技術者協会(Society of Petroleum Engineers International)、Geothermal Risingによって形成されたコンソーシアムに、約1億6,500万米ドルの「石油・ガスからの地熱エネルギー実証エンジニアリング」助成金を授与しました。コンソーシアムによって形成される異業種コラボレーションは、石油・ガスの専門家、地熱スタートアップ、その他の利害関係者と関わり、地熱イノベーションの戦略と機会に関するコンセンサスを形成します。

- 昨年10月、インドと米国は、特にクリーンエネルギーへの移行を支援するために必要とされる再生可能エネルギーの広範な統合を促進するために、新たなエネルギータスクフォースの創設を宣言しました。この宣言は、石油・天然ガス省のハーディープシン・プリ大臣と米国のジェニファー・グランホルムエネルギー長官との二国間会談の後に発表されたもので、重要なエネルギーセグメントにおけるインドと米国のパートナーシップをまったく新しいレベルに引き上げるものです。

- また、カナダは世界でも有数の石油・ガス産出国であり、同産業はカナダ経済全体にとって極めて重要な役割を果たしています。カナダ石油・ガス生産者協会によると、石油・天然ガスの上流生産への投資額は2023年に約400億カナダドル(297億3,000万米ドル)に達し、COVID以前の投資額を上回ると予測されています。これは、カナダ経済全体の追加支出が前年より約40億カナダドル(29億7,000万米ドル)、11%増加することを意味します。

- 2022年10月、カナダ・アルバータ州エドモントン近郊のストラスコナ製油所に世界クラスの再生可能ディーゼル・コンプレックスを建設するImperialのために、Fluor Corporationは払い戻し可能なフロントエンド・エンジニアリングと詳細エンジニアリング、設計、調達サービスを受注しました。この新しい複合施設は、カナダで最も重要な再生可能ディーゼル生産施設になると予想され、特に地元産の原料から1日当たり約2万バレルの再生可能ディーゼルを生産することになります。

石油・ガスエンジニアリングサービス産業概要

石油・ガスエンジニアリングサービス市場は、主に複数の世界的企業の存在と新規市場参入企業の出現により、半固体化が予想されます。Toyo Engineering Corporation、Stress Engineering Services Inc.、Element Materials Technologyなどの市場参入企業は、産業におけるエンジニアリングサービスの全体的な採用を強化するため、世界的に様々な石油・ガス会社と様々な戦略的提携やパートナーシップを結ぶことを目標としています。

2023年6月、Clariant Oil Servicesは、石油・ガス産業の脱乳化ニーズにより効率的でサステイナブルソリューションを提供するため、PHASETREAT WETを発表しました。従来の石油生産プロセスに内在する課題(特に、油水分離に関するより厳しい環境要件への対応)を克服するために設計されたこの斬新なソリューションは、ロジスティクスの簡素化、操業コストの最小化、安全リスクの軽減において、オペレーターを支援し、サポートします。

2023年1月、National Oil Corporation of Libya(NOC)のファルハット・ベングダラ最高経営責任者(CEO)とEniのクラウディオ・デスカルツィ最高経営責任者(CEO)は、戦略的プロジェクトである「構造物A&E」の開発に合意しました。これは、特にリビア国内市場への供給と欧州への輸出を確保するために、ガス生産量を最大化することを主要目的としています。「構造物A&E」は、主に2,000年初頭以来、同国初の大規模プロジェクトです。これは、リビア沖合の契約エリアDに位置する2つのガス田、すなわちストラクチャー「E」と「A」の開発からなります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 石油・ガス産業における自動化の採用拡大による設計・エンジニアリングサービスの成長促進

- 石油・ガス産業におけるコストと業務効率向上のための継続的な取り組み

- 拡張現実やBIM 4Dといったインダストリー4.0の実践によるTTMの削減

- 市場抑制要因

- 石油・ガス価格の変動やその他のマクロ経済変動の影響を受けやすい市場

- 運用とコンプライアンス関連の課題

- 産業の利害関係者とビジネスモデルの分析

- エンジニアリングサービス産業のインハウスとアウトソーシングの比較分析

- コスト内訳分析

- 石油・ガスとその他の主要プロセス産業との採用動向の比較分析

- COVID-19がエンジニアリングサービス産業に与える影響

第6章 市場セグメンテーション

- タイプ別

- ダウンストリーム

- 中流

- 上流

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Stress Engineering Services Inc.

- Toyo Engineering Corporation

- Element Materials Technology

- L&T Technology Services Limited

- Arseal Technologies

- Citec Group Oy Ab

- WSP Global Inc.

- Wood PLC

- Tetra Tech Inc.

- Mannvit Consulting Engineers

- QuEST Global Services Pte. Ltd

- M&H

- Hatch Ltd

- Lloyd's Register Group Services Limited

第8章 投資分析

第9章 市場機会と今後の動向

The Oil & Gas Engineering Services Market size is estimated at USD 58.80 billion in 2025, and is expected to reach USD 84.37 billion by 2030, at a CAGR of 7.49% during the forecast period (2025-2030).

The rise in the adoption of various automation technologies in the Oil and Gas sector is the prime factor enhancing the engineering services market exponentially.

Key Highlights

- Due to the industry's dynamic nature, the need to increase productivity and efficiency, uptime, and return on assets is rising. At the same time, minimizing costs is estimated to drive the adoption of engineering services in the industry.

- Moreover, the oil and gas industry faces challenges like rising penetration of renewable energy, strict carbon footprint regulations, electric vehicles, and various new hydrocarbon sources. Hence, the companies are adopting various strategic Industry 4.0 strategies to overcome these challenges.

- Advanced application of technologies, such as machine learning, analytics, and many others, is expected to help and assist oil and gas companies in analyzing big data sets and provide meaningful insights. Hence, the engineering services adoption within the industry is anticipated to rise during the forecast period.

- Also, the market is witnessing various strategic collaborations amongst the players, acting as a lucrative path toward expansion. For instance, in April 2023, Energy company BlueNord, also known as Noreco Oil Denmark AS or Noreco, and engineering and contracting company Semco Maritime AS entered into a strategic partnership agreement to jointly identify, explore, and investigate opportunities in the oil and gas space.

- However, the growing operational and compliance-related challenges and the fluctuations in the oil and gas prices, as well as other macroeconomic changes within the industry, could be a significant concern limiting the overall market's growth throughout the forecast period.

Oil & Gas Engineering Services Market Trends

Downstream Segment to Exhibit Significant Growth

- The Downstream section of the Oil and Gas Industry involves the operations that primarily occur after the construction phase until the point of sale. Certain downstream operations comprise processing, refining, transportation, and selling petroleum products. The rising demand for safe and reliable operations while reducing the total cost of operations is anticipated to drive the industry's overall adoption of downstream oil and gas services.

- Downstream oil and gas services play a very significant role in enhancing the total refining process while impacting the marketability and desirability of the finished product. The downstream supply chain includes noteworthy operations such as marketing by-products, effective database management, and effective management of distribution.

- Moreover, key downstream oil and gas services comprise asset integrity management, petroleum testing, industrial technical inspection, refining and distribution, hazardous location equipment testing, and database software solutions. It also includes Enterprise Asset Management (EAM) solutions that address core Asset Information Management as well as applications involving Plant Asset Maintenance Management.

- According to BP International Limited, BP's downstream business segment has generated a total revenue of around USD 188.6 billion in 2022.

North America Expected to Dominate the Market

- North America is anticipated to dominate the Oil and Gas Engineering Services Market, especially due to the rising number of oil and gas projects in countries such as Canada and the United States. According to the January 2023 Short-Term Energy Outlook by the US Energy Information Administration, it is forecasted that the overall crude oil creation in the United States would average 12.4 million barrels per day (b/d) in 2023 and 12.8 million b/d in 2024, thereby surpassing the earlier record of 12.3 million b/d set in 2019.

- The region is also seeing a large number of strategic collaborations as a lucrative way to grab the opportunities offered by the oil and gas industry within the region. For instance, in March 2023, the US Department of Energy (DOE) awarded a sum of around USD 165 million "Geothermal Energy from Oil and Gas Demonstrated Engineering" grant to a consortium formed by Project Innerspace, Society of Petroleum Engineers International, and Geothermal Rising. The cross-industry collaboration that is formed by the consortium would engage with oil and gas professionals, geothermal startups, and other stakeholders to create consensus around strategies and opportunities for geothermal innovation.

- In October last year, India and the US declared the creation of a new energy task force, especially to facilitate the extensive integration of renewable energy, which is mainly required to support the transition to clean energy. The declaration would elevate the India-US partnership's strength in the vital energy sector to a whole new level, which came following a bilateral meeting between the Union Minister of Petroleum and Natural Gas Hardeep Singh Puri and US Energy Secretary Jennifer Granholm.

- Also, Canada is one of the significant oil and gas producers worldwide, as the industry plays a crucial role in the country's overall economy. According to the Canadian Association of Petroleum Producers, it is forecasted that the oil and natural gas investment in upstream production will hit a sum of around CAD 40.0 billion (USD 29.73 billion) in 2023, surpassing the pre-COVID investment levels. That represents around CAD 4.0 billion (USD 2.97 Billion), or 11%, more in the additional spending across Canada's economy than the prior year.

- In October 2022, Fluor Corporation was given a reimbursable front-end engineering and detailed engineering, design, and procurement services contract for Imperial as the company progresses and intends to build a world-class renewable diesel complex at its Strathcona refinery near Edmonton, Alberta, Canada. The new complex is anticipated to be the most significant renewable diesel production facility in Canada and would produce around 20,000 barrels of renewable diesel per day, especially from locally sourced feedstocks.

Oil & Gas Engineering Services Industry Overview

The Oil and Gas Engineering Services Market is anticipated to be semi-consolidated, primarily due to the presence of several worldwide players, along with the emergence of new market participants. The market players, such as Toyo Engineering Corporation, Stress Engineering Services Inc., and Element Materials Technology, are targeting to form various strategic collaborations and partnerships with various oil and gas companies globally to enhance the overall adoption of engineering services within the industry.

In June 2023, Clariant Oil Services introduced PHASETREAT WET to provide more efficient and sustainable solutions for the oil and gas industry's demulsification needs. Designed to overcome challenges inherent in traditional oil production processes - most notably, meeting stricter environmental requirements for oil and water separation - the novel solution would help and assist operators in simplifying logistics, minimizing operational costs, and mitigating safety risks.

In January 2023, the CEO of the National Oil Corporation of Libya (NOC), Farhat Bengdara, and Eni CEO Claudio Descalzi agreed on the development of "Structures A&E," a strategic project. It is mainly aimed at maximizing gas production, especially to supply the Libyan domestic market and to ensure export to Europe. "Structures A&E" is primarily the first major project in the country since early 2000. It comprises the development of two gas fields, namely Structures "E" and "A," located in the contractual area D, offshore Libya.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Automation in the Oil and Gas Industry to Aid Growth of Design and Engineering Services

- 5.1.2 Ongoing Efforts to Enhance Cost and Operational Efficiency in the Oil and Gas Industry

- 5.1.3 Industry 4.0 Practices Such as Extended Reality and BIM 4D to Reduce TTM

- 5.2 Market Restraints

- 5.2.1 The Market is Susceptible to Fluctuations in the Oil and Gas Prices as Well as Other Macroeconomic Changes

- 5.2.2 Operational and Compliance-related Challenges

- 5.3 Industry Stakeholder and Business Model Analysis

- 5.4 Comparative Analysis of In-house and Outsourced Engineering Services Industry

- 5.5 Cost Breakdown Analysis

- 5.6 Comparative Analysis of the Adoption Trends Between Oil and Gas and Other Major Process Industries

- 5.7 Impact of COVID-19 on the Engineering Services Industry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Downstream

- 6.1.2 Midstream

- 6.1.3 Upstream

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Stress Engineering Services Inc.

- 7.1.2 Toyo Engineering Corporation

- 7.1.3 Element Materials Technology

- 7.1.4 L&T Technology Services Limited

- 7.1.5 Arseal Technologies

- 7.1.6 Citec Group Oy Ab

- 7.1.7 WSP Global Inc.

- 7.1.8 Wood PLC

- 7.1.9 Tetra Tech Inc.

- 7.1.10 Mannvit Consulting Engineers

- 7.1.11 QuEST Global Services Pte. Ltd

- 7.1.12 M&H

- 7.1.13 Hatch Ltd

- 7.1.14 Lloyd's Register Group Services Limited