|

市場調査レポート

商品コード

1435894

航空貨物輸送:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Air Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空貨物輸送:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

航空貨物輸送市場規模は2024年に1,109億1,000万米ドルと推定され、2029年までに1,473億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4%のCAGRで成長します。

陸上および船舶による貨物輸送は依然として優れた選択肢ですが、航空による物品輸送は最も迅速で妨げのない手段であると考えられています。貨物トンキロ(CTK)で測定した世界の航空貨物需要は10月に211億となり、前月比3.5%増加しました。しかし、業界のCTKは2022年の同月と比較して前年比13.6%減少し、2019年のパンデミック前のレベルよりも6.2%低かった。2022年10月の季節調整済み(SA)航空貨物需要は前月比2.3%と若干鈍化しました。 9月に比べて減少。 CTKと同様に、SA CTKは前年比13.1%縮小し、2019年10月と比べて6.1%減少しました。

航空貨物業界は、先進国における高いインフレ率、世界の商品とサービスの流れの低迷、ウクライナで続く戦争、異常な米国高などにより、2022年10月も状況は続いた。これらすべての要因が航空貨物の成長に下押し圧力をかけています。新規輸出受注は歴史的に航空貨物輸送の先行指標であったが、依然として好調ではありません。世界のPMIは依然として重要な50ラインを下回っており、世界平均で引き続き縮小が続いていることを示唆しています。中国と韓国は、2022年10月に2022年9月よりわずかに増加した新規輸出受注を記録したが、依然として50を下回った。他の主要国は下降傾向を維持しました。特にドイツは3月以来50を下回る水準で横ばいとなっており、東欧における戦争の経済への影響が続いていることを示しています。

有効貨物トンキロ(ACTK)で測定した業界全体の航空貨物輸送能力は、9月と比較して2%増加しました。 10月の業界貨物積載率(CLF)はマイナス7.4%となり、9月のマイナス7.0%から低下しました。業界のSA ACTKは、2021年 10月と比較してほぼ同じレベルを維持しました。ラテンアメリカは、SA ACTKの前年比で最も高い20.3%の成長を達成しました。これに北米が前年比3%、中東が同ベースで1.1%で続きます。これに対し、今年 10月にSA ACTKが前年比でマイナス成長となった地域は、アフリカ(-7.5%)、欧州(-5%)、アジア太平洋(-2.1%)でした。

航空貨物輸送市場動向

eコマースの増加が市場を牽引

eコマースは今後5年間で世界的に14%成長すると予測されています。米中関税戦争の影響でここ10年で最悪の年を迎えた航空貨物業界にとって、これは絶好のチャンスとなります。航空貨物ビジネス全体の16%を占める世界のeコマース業界は、2022年の3兆5,000億米ドルの商品規模から、2025年までに7兆米ドルに増加すると予測されています。

一部の世界の通信事業者は、アマゾン、アリババ、京東商事などのオンラインショッピング大手が独占する宅配市場で、さらに大きなシェアを獲得しようと取り組んでいます。ドバイに拠点を置くエミレーツ航空はエミレーツ・デリバーズを立ち上げ、ルフトハンザドイツ航空にはヘイデイが、そしてブリティッシュ・エアウェイズの親会社であるIAGにはゼンダが含まれています。しかし、IATAは、このような減少にもかかわらず、11月の実績は8か月ぶりの最高で、前年比の縮小率は2019年3月以来最も低いものとなったと指摘しました。

航空貨物業界は、eコマースの成長を最大限に活用できる有利な立場にあります。航空貨物はeコマースを処理するために構築されており、企業間消費者の国境を越えたeコマースの約80%が航空によって輸送されます。電子機器の場合、高額なものに比べて体積やトン数が比較的少ないため、航空貨物が好まれる発送方法です。

したがって、オンラインショッピングが世界中で小包配送サービスの需要を高めるため、eコマースは航空貨物業界を活性化すると予想されています。航空貨物は顧客のニーズに応え、迅速、効率、信頼性をもって商品を届けます。急成長する国境を越えたeコマース市場と、大小の電子小売業者による国内発送量の増加が、世界の航空貨物市場の成長を牽引しています。

アジア太平洋地域の航空貨物への最大の貢献者

多くのアジア太平洋諸国で課された渡航制限により、COVID-19感染症のパンデミック下で航空部門が低迷したにもかかわらず、航空貨物需要は比較的堅調に推移しました。しかし、サプライチェーンの混乱、不確実性の高まりと失業率の上昇による企業と消費者信頼感の低下は、航空貨物事業に悪影響を及ぼしました。

アジア太平洋航空協会(AAPA)は、航空貨物部門は必須の医療機器や物資の輸送に積極的に取り組んでいると述べています。多くのアジア太平洋諸国は、複数の航空会社に旅客機を航空貨物輸送用に一時的に改造するよう奨励しました。標準的な旅客用ATR72-600は1.7トンの貨物しか運ぶことができないが、貨物機を改造したモデルは最大8トンまで運ぶことができ、地域の需要と運航条件を考慮すると太平洋島嶼国に適しています。

韓国は、2022年のアジア太平洋航空貨物市場シェアで第4位の市場シェアを占めました。韓国には、世界で最も重要な航空貨物運送業者産業の1つが含まれています。旅客輸送の崩壊により利用可能な輸送スペースが減少した際に、旺盛な需要の恩恵を受けました。航空会社は声明で、貨物機の運航率を高め、アイドル状態の旅客機を輸送に活用するという航空会社の戦略が貨物の売上を支えたと発表しました。韓国の2大航空会社である大韓航空とアシアナ航空は、貨物輸送需要の急増を利用して旅客数の減少を補い、2021年の営業収益を大幅に伸ばしました。

COVID-19感染症の診断キットや自動車部品のニーズが高まり、海上貨物の需要が航空輸送に移り、航空貨物の売上が伸びた。したがって、これは韓国の航空貨物市場の大幅な成長につながります。さらに、2022年6月には、大韓航空が引き続き高い貨物需要に向けた態勢を整えているため、エアバスとボーイングがここ数カ月で発表した新型ワイドボディ貨物機への移行を検討しています。また、長期的な強い貨物需要により、エアバスは昨年2021年にA350貨物機を、ボーイングは2022年1月に777X貨物機を就航させました。したがって、貨物サービスの航空機数の増加は、予測期間中にアジア太平洋航空貨物市場を押し上げるでしょう。

航空貨物輸送業界の概要

航空貨物輸送市場は、著名な国際プレーヤーの存在により適度に集中しています。ほとんどのサービスプロバイダーは、梱包、ラベル貼り、文書化、チャーターサービス、貨物輸送などのバンドルソリューションを提供しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析調査手法

- 調査段階

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- バリューチェーン/サプライチェーン分析

- 技術動向

- 投資シナリオ

- 政府の規制と取り組み

- スポットライト-航空貨物輸送コスト/運賃

- eコマース業界に関する洞察

- COVID-19による航空貨物輸送市場への影響

第5章 市場力学

- 促進要因

- 航空貨物輸送能力の需要の増加

- eコマースの台頭

- 抑制要因

- 貨物制限

- 機会

- AIと自動化の統合

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の激しさ

第6章 市場セグメンテーション

- サービス別

- 航空会社

- 郵便

- その他のサービス

- 仕向地別

- 国内

- 国際

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- オランダ

- 英国

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- オーストラリア

- インド

- シンガポール

- マレーシア

- インドネシア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- 南アフリカ

- エジプト

- GCC諸国

- その他中東とアフリカ

- 南米

- ブラジル

- チリ

- その他南米

- 北米

第7章 競合情勢

- 市場集中の概要

- 企業プロファイル

- DHL Supply Chain &Global Forwarding

- Kuehne+Nagel

- DB Schenker Logistics

- DSV Panalpina

- UPS Supply Chain Solutions

- Expeditors International

- Nippon Express

- Bollore Logistics

- Hellmann Worldwide Logistics

- Kintetsu World Express*

第8章 市場機会と将来の動向

第9章 付録

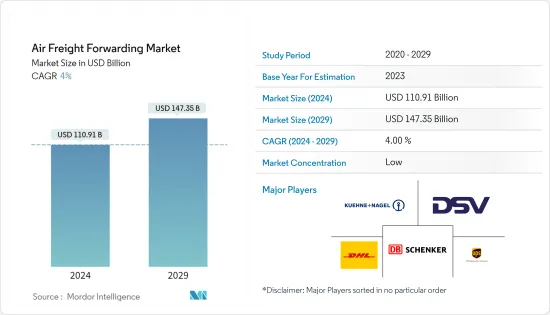

The Air Freight Forwarding Market size is estimated at USD 110.91 billion in 2024, and is expected to reach USD 147.35 billion by 2029, growing at a CAGR of 4% during the forecast period (2024-2029).

Although land and ship cargo transportation remain outstanding options, goods transport by air is considered the quickest and unhindered mode. Global air cargo demand, measured by cargo tonne-kilometers (CTKs), was 21.1 billion in October, increasing by 3.5% month-on-month (MoM). However, industry CTKs fell by 13.6% YoY compared to the same month in 2022 and were also 6.2% lower than the pre-pandemic levels in 2019. Seasonally adjusted (SA) air cargo demand softened slightly in October 2022, with a 2.3% MoM decline compared with September. Similar to the CTKs, SA CTKs contracted by 13.1% YoY and were 6.1% lower than in October 2019.

The air cargo industry persisted in October 2022, including high inflation rates in advanced economies, weak performance in the global flows of goods and services, the ongoing war in Ukraine, and the unusual strength of the US dollar. All of these factors put downward pressure on air cargo growth. The new export orders, historically a leading indicator for air cargo shipments, were still not buoyant. The global PMI remains below the critical 50 lines, suggesting continued contraction on average globally. China and Korea registered slightly higher new export orders in October 2022 than in September 2022, although they remained below 50. Other significant economies maintained a downward trend. Notably, Germany moved sideways at levels below 50 since March, signaling the continuous impact on the economy of the war in Eastern Europe.

Industry-wide air cargo capacity, measured by available cargo tonne-kilometers (ACTKs), increased by 2% compared with September. It produced an industry cargo load factor (CLF) of -7.4% in October, down from -7.0% in September. Industry SA ACTKs remained at about the same level compared with October 2021. Latin America achieved the highest YoY growth in SA ACTKs, at 20.3%. North America follows this with 3% YoY and the Middle East with 1.1% on the same basis. In comparison, regions that saw negative YoY growth in SA ACTKs this October were Africa (-7.5%), Europe (-5%), and Asia Pacific (-2.1%).

Air Freight Forwarding Market Trends

The increase in E-Commerce is driving the Market

E-commerce is forecast to grow 14% globally over the next five years. It creates an excellent opportunity for the air cargo industry, which witnessed its worst year in a decade due to the US-China tariff war. The global e-commerce industry, which makes up 16% of the total air cargo business, is projected to increase from USD 3.5 trillion in goods in 2022 to USD 7 trillion by 2025.

Some global carriers are working to gain a more significant share of the door-to-door delivery market that online shopping giants such as Amazon, Alibaba, and JD.com dominate. Dubai-based Emirates launched Emirates Delivers, Lufthansa includes Heyday, and British Airways parent IAG includes Zenda. However, IATA pointed out that despite this decline, November's performance was the best in eight months, with the slowest year-on-year rate of contraction recorded since March 2019.

The air cargo industry is well-positioned to capitalize on the growth in e-commerce. Air cargo is built to handle e-commerce, and approximately 80% of business-to-consumer cross-border e-commerce is transported by air. Air cargo is the preferred way of shipment for electronics due to the relatively small volume or tonnage compared to high value.

Thus, e-commerce is expected to fuel the air cargo industry, as online shopping boosts the demand for parcel delivery services across the globe. Air cargo can serve customers' needs and deliver goods with speed, efficiency, and reliability. The fast-growing cross-border e-commerce market and the rising domestic volumes sent by large and small e-retailers are driving growth in the global air cargo market.

APAC Largest Contributor to Air Freight

Irrespective of a downfall in the airline sector during the COVID-19 pandemic due to travel restrictions imposed in many Asian-Pacific countries, air cargo demand held up relatively well. However, supply chain disruptions and weakening business and consumer confidence due to increased uncertainties and rising unemployment adversely affected the air cargo businesses.

The Association of Asia-Pacific Airlines (AAPA) states that the air cargo sector is active in transporting essential medical equipment and supplies. Many Asian-Pacific countries encouraged several airlines to modify their passenger aircraft for air freight transport temporarily. While a standard passenger ATR72-600 can only carry 1.7 metric tons of cargo, its freighter-modified model can carry up to 8 metric tons, making it suitable for Pacific Island countries, given the region's demand and operating conditions.

South Korea accounted for the fourth-largest market share in the Asia-Pacific air cargo market share in 2022. South Korea includes one of the world's most significant air cargo carrier industries. It benefitted from strong demand when the collapse of passenger traffic reduced available transport space. Cargo sales were underpinned by the airline's strategy to increase the cargo plane operation rate and utilize idle passenger planes for transport, the airline said in a statement. Korean Air and Asiana Airlines, South Korea's two largest airlines, increased their operational earnings significantly in 2021, harnessing surging demand for cargo transport to help offset low passenger traffic.

The need for COVID-19 diagnostic kits and auto parts increased, and the sea cargo demand transferred to air transport, driving air cargo sales. Therefore, this leads to significant air cargo market growth in South Korea. Further, in June 2022, as Korean Air continues to position itself for high cargo demand, it is considering a move for the new wide-body freighters released by Airbus and Boeing in recent months. Long-term strong cargo demand also prompted Airbus to launch its A350 freighter last year in 2021 and Boeing its 777X freighter in January 2022. Thus, increasing the number of aircraft in cargo service will boost the Asia-Pacific air cargo market during the forecast period.

Air Freight Forwarding Industry Overview

The Air Freight Forwarding Market is moderately concentrated with the presence of prominent international players. Most service providers offer bundled solutions, such as packaging, labeling, documentation, charter services, and freight transportation. Some of the existing major players in the market include - DHL Supply Chain & Global Forwarding, Kuehne + Nagel, DB Schenker Logistics, DSV Panalpina, UPS Supply Chain Solutions, Expeditors International, Nippon Express, Bollore Logistics, Hellmann Worldwide Logistics, and Kintetsu World Express.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Technological Trends

- 4.4 Investment Scenarios

- 4.5 Government Regulations and Initiatives

- 4.6 Spotlight - Air Freight Transportation Costs/Freight Rates

- 4.7 Insights on the E-commerce Industry

- 4.8 Impact of Covid-19 on Air Freight Forwarding Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Increase in the demand for the Air Cargo Capacity

- 5.1.2 The Rise of E-commerce

- 5.2 Restraints

- 5.2.1 Cargo Restrictions

- 5.3 Opportunities

- 5.3.1 AI and Automation Integration

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Airlines

- 6.1.2 Mail

- 6.1.3 Other services

- 6.2 By Destination

- 6.2.1 Domestic

- 6.2.2 International

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Mexico

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 France

- 6.3.2.3 Netherlands

- 6.3.2.4 United Kingdom

- 6.3.2.5 Italy

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Australia

- 6.3.3.4 India

- 6.3.3.5 Singapore

- 6.3.3.6 Malaysia

- 6.3.3.7 Indonesia

- 6.3.3.8 South Korea

- 6.3.3.9 Rest of Asia-Pacific

- 6.3.4 Middle East & Africa

- 6.3.4.1 South Africa

- 6.3.4.2 Egypt

- 6.3.4.3 GCC Countries

- 6.3.4.4 Rest of Middle East & Africa

- 6.3.5 South America

- 6.3.5.1 Brazil

- 6.3.5.2 Chile

- 6.3.5.3 Rest of South America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 DHL Supply Chain & Global Forwarding

- 7.2.2 Kuehne + Nagel

- 7.2.3 DB Schenker Logistics

- 7.2.4 DSV Panalpina

- 7.2.5 UPS Supply Chain Solutions

- 7.2.6 Expeditors International

- 7.2.7 Nippon Express

- 7.2.8 Bollore Logistics

- 7.2.9 Hellmann Worldwide Logistics

- 7.2.10 Kintetsu World Express*