|

市場調査レポート

商品コード

1445522

うっ血性心不全(CHF)治療装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Congestive Heart Failure (CHF) Treatment Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| うっ血性心不全(CHF)治療装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

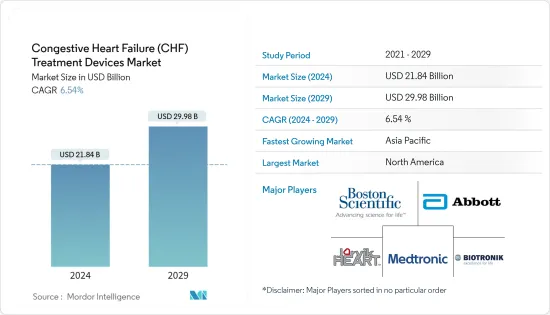

うっ血性心不全治療装置の市場規模は、2024年に218億4,000万米ドルと推定され、2029年までに299億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.54%のCAGRで成長します。

COVID-19のパンデミックによってもたらされた高い感染率とロックダウン規制により、外科手術は影響を受けています。うっ血性心不全市場は影響を受けており、病院や診断センターを訪れる人が減った結果、心血管疾患患者はさらに診断と治療の遅れに直面しています。たとえば、国立医学図書館で発表された2022年3月の調査研究では、2020年2月から2021年1月の間に、成人の心臓手術の件数が52.7%減少し、待機的症例が65.5%減少したことがわかりました。心臓外科手術に対するCOVID-19症の影響。しかし、COVID-19の感染が沈静化し、市場が回復し始めると、業務数は増加しました。COVID-19感染症と心臓病の影響を調べるために、科学者によってさまざまな調査が行われています。米国の科学者グループはCOVID-19症患者を調査し、その論文を2022年4月に国立医学図書館に発表しました。また、この記事では、COVID-19感染症による入院患者は心房性不整脈や心室性不整脈を発症するリスクが高いとも述べています。米国。したがって、国内の入院患者における不整脈のリスクにより、さまざまな心臓処置に使用されるCHF治療装置の需要が増加しました。したがって、COVID-19によるCHFの可能性の増加により、市場の成長が促進されると予想されます。

心血管疾患(CVD)の患者プールの増加とうっ血性心不全(CHF)症例の急増が、CHF治療装置市場の成長を促進する主な要因です。 CVDの急増は心不全に関連するリスクの上昇につながり、その結果、CHFの治療に使用される機器の需要が高まります。座りっぱなしのライフスタイル、ジャンクフードの摂取、精神的ストレスも、CVDの発症に関連する重要な要因です。高齢者人口の増加は、世界中でCVD症例の急増にもつながっています。たとえば、アジア太平洋保健制度と政策に関するアジア太平洋観測所が発行した2021年11月の報告書によると、この地域の出生率の低下により、2050年までにアジア太平洋地域の人口の約4分の1が60歳以上になると予想されています。寿命の延長により心血管疾患の負担がさらに増加すると予想され、効果的で高度な治療手順への需要が高まり、市場の成長が促進されます。この人口統計は、CHFを含む慢性疾患にかかりやすいです。免疫レベルが低いという特徴があるため、予測期間中のこれらの製品の成長に大きな影響を与えるレンダリングの推進力として機能します。その結果、心臓ケアで利用できる最新の治療法により、高齢者の寿命が延びると期待されています。

2022年に発行された世界心臓連盟の報告書では、心臓病や脳卒中を含む心血管疾患が世界的に最も一般的な非感染性疾患であると述べられています。したがって、心血管疾患の有病率の増加が市場の成長を促進する原因となっています。国立医学図書館の2021年6月の記事によると、イタリアにおける心血管疾患有病率の年齢標準化推定値は世界の有病率と同様です。それでも、この国の原油蔓延率は世界の蔓延率のほぼ2倍(12.9%対6.6%)です。心血管疾患の有病率の増加により、ペースメーカーなどのさまざまなうっ血性心不全装置の需要が増加すると予想され、予測期間中に市場の成長が高まると予想されます。

さらに、CHF治療装置の技術進歩は市場全体に有利に働いています。たとえば、2022年 8月にアボットが発表したデータでは、HeartMate 3心臓ポンプは患者の寿命を少なくとも5年改善し、重篤な疾患に対処する人々にとって確実な救命代替手段となると述べられています。 MOMENTUM 3実験は、左心室補助装置(LVADまたは心臓ポンプとしても知られる)で重度心不全の治療を受けている患者の長期転帰を評価するためにこれまでに実施されたランダム化臨床調査でした。したがって、このような臨床試験は市場における技術の進歩に関する洞察を提供し、予測期間中の市場の成長を高めます。

ただし、CHF治療装置のコストが高いため、予測期間中の市場の成長が妨げられる可能性があります。

うっ血性心不全(CHF)治療装置の市場動向

植込み型ペースメーカーセグメントは、予測期間中にかなりの市場シェアを保持すると予想されます

植込み型ペースメーカーは、電気インパルスを使用して心臓のリズムを調節する装置です。体内ペースメーカーは、心臓に電極が配置され、電子回路と電源が体内に埋め込まれたものです。さらに、ペースメーカーは心臓のリズムを調整することにより、徐脈の症状を取り除くことができます。これは、多くの場合、エネルギーが増し、息切れが軽減されることを意味します。

植込み型ペースメーカーの成長を促進する主な要因には、心血管患者の増加と、心房細動を正確に検出してその可能性を低減する独自のアルゴリズムなどの技術の進歩が含まれます。心房細動は、しばしばAFibまたはAFと呼ばれ、最も一般的なタイプの心臓不整脈です。不整脈とは、心臓の鼓動が遅すぎる、速すぎる、または不規則になることです。 2022年 10月のCDCのプレスリリースによると、2030年には米国で1,210万人がAFibになると推定されています。同様に、2022年 2月に国立医学図書館に掲載された調査論文では、次のように推定されています。米国では2050年までに世界中で600万人から1,200万人、欧州では2060年までに1,790万人がこの症状に苦しむと予想されています。したがって、心房細動の蔓延により治療用のCHFデバイスの需要が増加し、市場が拡大すると予想されています。

市場リーダーは臨床試験によるテクノロジーの進歩に関与しています。たとえば、ボストンサイエンティフィックコーポレーションは、2021年 12月に、mCRMモジュラー療法システムの安全性、性能、有効性を評価するためのMODULAR ATP臨床試験を開始しました。これには、リードレス治療用に設計されたEMPOWERモジュラーペーシングシステム(MPS)が含まれます。徐脈ペーシングのサポートと抗頻脈ペーシング(ATP)の両方を提供できるペースメーカー。したがって、このような臨床試験は、高度な技術を提供することにより、予測期間中に市場の成長を促進すると予想されます。

したがって、CVDや臨床試験の増加などの上記のすべての要因が、予測期間中のこのセグメントの良好な成長に寄与すると予想されます。

北米は予測期間中にかなりの市場シェアを保持すると予想される

北米地域の市場成長を牽引する要因には、うっ血性心不全(CHF)治療の需要の増加、対象疾患の有病率の増加、ヘルスケアの高騰、治療の利用可能性に関する国民の意識の高まりなどが含まれます。デバイス。さらに、強力な臨床パイプライン、治療薬に対する有利な償還ポリシー、およびこれらの機器の普及促進も、収益の成長を促進すると予想されるその他の要因です。

この地域における心臓病の有病率の増加は、市場成長の重要な要因の1つです。たとえば、米国心臓協会誌の2021年版に記載されているように、2035年までに米国の成人 1億3,000万人以上が何らかの心臓病を患うと推定されています。さらに、カナダ心臓脳卒中財団が2022年 2月に提供した統計によると、現在カナダでは75万人が心不全を抱えており、毎年 10万人が心不全と診断されています。したがって、心臓病の有病率の増加により、そのような病気の治療のためのデバイスの採用が増加すると予想され、予測期間中に市場の成長が増加すると予想されます。

さらに、製品承認などの取り組みにより、市場の成長が促進されると予想されます。たとえば、アボットは2022年 4月に、新しいAveirシングルチャンバーVRペースメーカーシステムによるリードレスペースメーカー技術について食品医薬品局(FDA)の承認を取得しました。このシステムは、現在市販されているリードレスペースメーカーよりも電池寿命が長いのが特徴です。したがって、このような承認は市場に新しい革新的な技術を提供するため、市場の成長を促進すると予想されます。同様に、2021年 6月、米国心臓病学会(ACC)とGEヘルスケアは協力して、ACCの応用医療イノベーションコンソーシアムを支援および参加し、心臓病学における人工知能(AI)とデジタルテクノロジーのロードマップを構築し、健康改善のための新しい戦略を開発しました。結果。

したがって、CVDの普及の増加などの前述の要因と主要な市場企業による取り組みを考慮すると、予測期間中に北米地域の市場の成長が促進されると予想されます。

うっ血性心不全(CHF)治療装置業界の概要

うっ血性心不全(CHF)治療装置市場は、主要な国際企業が互いに競争しており、競合という点では適度に統合されています。企業は、個別化されたケアを提供できる実用性の高い製品の開発により重点を置いています。主要な市場企業には、Jarvik Heart Inc.、Medtronic PLC、Boston Scientific Corporation、Abbott Laboratories、Biotronik SE &Co. KGなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心血管疾患(CVD)の有病率の上昇

- うっ血性心不全(CHF)症例数の急増

- 技術的に進んだ製品の登場

- 市場抑制要因

- デバイスのコストが高い

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品

- 心室補助装置(VAD)

- LVAD

- RVAD

- BiVAD

- カウンターパルセーションデバイス

- 植込み型除細動器

- 経静脈ICD

- 皮下ICD

- ペースメーカー

- 埋め込み可能

- 外部

- 心臓再同期療法

- 心臓再同期療法- 除細動器(CRT-D)

- 心臓再同期療法- ペースメーカー(CRT-P)

- 心室補助装置(VAD)

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Berlin Heart GmbH

- Biotronik SE &Co. KG

- Boston Scientific Corporation

- Jarvik Heart Inc.

- Lepu Medical Technology(Beijing)Co.,Ltd.

- Magenta Medical Ltd

- MEDICO SRL

- Medtronic PLC

- Oscor, Inc.

- OSYPKA MEDICAL

- Shree Pacetronix Ltd

第7章 市場機会と将来の動向

The Congestive Heart Failure Treatment Devices Market size is estimated at USD 21.84 billion in 2024, and is expected to reach USD 29.98 billion by 2029, growing at a CAGR of 6.54% during the forecast period (2024-2029).

Due to the high infection rate and lockdown regulations brought on by the COVID-19 pandemic, surgical procedures have been affected. The congestive heart failure market has been impacted, and patients with cardiovascular disorders have further encountered delays in diagnosis and treatment as a result of fewer individuals visiting hospitals and diagnostic centers. For instance, a March 2022 research study published in the National Library of Medicine found that between February 2020 and January 2021, there was a 52.7% decrease in the volume of adult cardiac surgery and a 65.5% decrease in elective cases, which shows the negative impact of COVID-19 on the cardiac surgical procedures. But as the COVID-19 instances subsided and the market began to recover, the number of operations increased. Various research has been conducted by scientists to find the impact of COVID-19 infection and cardiac diseases. A group of scientists in the United States researched COVID-19 patients and published the article in the National Library of Medicine in April 2022. The article also stated that COVID-19 hospitalized patients possess a high risk of the development of atrial or ventricular arrhythmias in the United States. Thus, such risk of arrhythmias among hospitalized patients in the country increased the demand for CHF treatment devices used for various cardiac procedures. Thus, such increasing chances of CHF due to COVID-19 are expected to increase the market growth.

An increasing patient pool of cardiovascular diseases (CVDs) and a surge in congestive heart failure (CHF) cases are prime factors augmenting the growth of the CHF treatment devices market. The surge in CVDs leads to a rising in risk related to heart failure, thereby driving the demand for devices used in the treatment of CHF. Sedentary lifestyles, junk food consumption, and mental stress are other key factors associated with the development of CVDs. The increasing geriatric population is also leading to an upsurge in the cases of CVDs, worldwide. For instance, as per the November 2021 report published by the Asian Pacific Observatory on Health Systems and Policies, by 2050, about one-fourth population of the Asia-Pacific region will be 60 years or older due to the decreasing fertility rate in the region and increasing longevity which is further expected to increase the burden of the cardiovascular diseases and thus, driving the demand for the effective and advanced treatment procedures thus increasing market growth. This demographic is prone to chronic diseases, including CHF. It is characterized by low immunity levels, thereby serving as a high-impact rendering driver for the growth of these products over the forecast period. As a result, the latest treatments available in cardiac care are expected to increase the lifespan of the elderly population.

The World Heart Federation report published in 2022 stated that cardiovascular disease, which includes heart disease and stroke, is the most common non-communicable disease globally. Thus, the increasing prevalence of cardiovascular diseases is responsible for boosting the growth of the market. According to a June 2021 article by the National Library of Medicine, age-standardized estimates of cardiovascular disease prevalence in Italy are similar to the global prevalence. Still, the country's crude prevalence is almost two times higher than the global prevalence (12.9% vs. 6.6%). The increasing prevalence of cardiovascular diseases is expected to increase the demand for various congestive heart failure devices, such as pacemakers which are expected to increase the market growth over the forecast period.

Additionally, technological advancements in CHF treatment devices are working in favor of the overall market. For instance, in August 2022, released data from Abbott stated that the HeartMate 3 heart pump improves patients' lives by at least five years and represents a definite life-saving alternative for those dealing with severe disease. The MOMENTUM 3 experiment was the randomized clinical research ever conducted to evaluate long-term outcomes in patients being treated for severe heart failure with a left ventricular assist device (also known as an LVAD or heart pump). Thus, such clinical trials provide insight into the technological advancement in the market, which increases the market growth over the forecast period.

However, the high cost of CHF treatment devices may hamper the growth of the market over the forecast period.

Congestive Heart Failure (CHF) Treatment Devices Market Trends

The Implantable Pacemakers Segment is Expected to Hold a Significant Market Share Over the Forecast Period

The implantable pacemaker is a device that uses electrical impulses to regulate the heart rhythm. An internal pacemaker is one in which the electrodes are placed in the heart, and electronic circuitry and the power supply are implanted within the body. Moreover, by regulating the heart's rhythm, a pacemaker can often eliminate the symptoms of bradycardia, which means individuals often have more energy and less shortness of breath.

The major factors driving the growth of implantable pacemakers include rising cardiovascular patients and technological advancements, such as exclusive algorithms to accurately detect and reduce the likelihood of atrial fibrillation. Atrial fibrillation, often called AFib or AF, is the most common type of heart arrhythmia. An arrhythmia is when the heart beats too slowly, too fast, or in an irregular way. According to a press release by CDC in October 2022, it is estimated that 12.1 million people in the United States will have AFib in 2030. Similarly, in February 2022, a research article published in the National Library of Medicine stated that It had been estimated that 6-12 million people worldwide will suffer this condition in the US by 2050 and 17.9 million people in Europe by 2060. Thus, the increasing prevalence of AFib is expected to increase the demand for CHF devices for treatment, which is expected to increase market growth over the forecast period.

The market leaders are involved in the advancement of technology with clinical trials. For instance, in December 2021, Boston Scientific Corporation initiated the MODULAR ATP clinical trial to evaluate the safety, performance, and effectiveness of the mCRM Modular Therapy System, which includes the EMPOWER Modular Pacing System (MPS), which is designed to be the leadless pacemaker capable of delivering both bradycardia pacing support and anti-tachycardia pacing (ATP). Thus, such clinical trials are expected to increase market growth over the forecast period by providing advanced technology.

Thus, all the above factors, such as increasing CVDs and clinical trials, are expected to contribute to the good growth of this segment over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

Some of the factors driving the market growth in the North American region include increasing demand for congestive heart failure (CHF) treatment, the increasing prevalence of target disorders, high expenditure on healthcare, and an increase in awareness among the population regarding the availability of treatment devices. Moreover, a strong clinical pipeline, favorable reimbursement policies for therapeutic products, and higher adoption of these devices are the other factors anticipated to promote revenue growth.

The increasing prevalence of heart diseases in the region is one of the key factors in market growth. For instance, as stated by the American Heart Association 2021 journal, it is estimated that by the year 2035, more than 130 million adults in the United States will have some type of heart disease. Additionally, the statistics provided by the Heart and Stroke Foundation of Canada in February 2022 state that there are 750,000 people currently living with heart failure, and 100,000 people are diagnosed with this condition each year in Canada. Thus, the increasing prevalence of heart diseases is expected to increase the adoption of devices for the treatment of such diseases, which is expected to increase market growth over the forecast period.

Furthermore, initiatives such as product approvals are expected to increase market growth. For instance, in April 2022, Abbott received the Food and Drug Administration (FDA) approval for leadless pacemaker technology with its new Aveir single-chamber VR pacemaker system, which features increased battery longevity over current commercially available leadless pacemakers. Thus, such approvals are expected to increase market growth as it provides new innovative technology in the market. Similarly, in June 2021, the American College of Cardiology (ACC) and GE Healthcare collaborated to support and participate in ACC's Applied Health Innovation Consortium to build a roadmap for artificial intelligence (AI) and digital technology in cardiology and develop new strategies for improved health outcomes.

Thus, considering the aforementioned factors, such as the increasing prevalence of CVDs, and initiatives by key market players are expected to fuel the market growth in the North American region over the forecast period.

Congestive Heart Failure (CHF) Treatment Devices Industry Overview

The congestive heart failure (CHF) treatment devices market is moderately consolidated, in terms of competition, with major international companies competing with each other. Companies are more focused on developing high-utility products which can deliver personalized care. Some of the major market players include Jarvik Heart Inc., Medtronic PLC, Boston Scientific Corporation, Abbott Laboratories, and Biotronik SE & Co. KG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Cardiovascular Diseases (CVD)

- 4.2.2 Surge in Number of Congestive Heart Failure (CHF) Cases

- 4.2.3 Advent of Technologically Advanced Products

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices

- 4.4 Porter Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Product

- 5.1.1 Ventricular Assist Devices (VADs)

- 5.1.1.1 LVAD

- 5.1.1.2 RVAD

- 5.1.1.3 BiVAD

- 5.1.2 Counter Pulsation Devices

- 5.1.3 Implantable Cardioverter Defibrillators

- 5.1.3.1 Transvenous ICD

- 5.1.3.2 Subcutaneous ICD

- 5.1.4 Pacemakers

- 5.1.4.1 Implantable

- 5.1.4.2 External

- 5.1.5 Cardiac Resynchronization Therapy

- 5.1.5.1 Cardiac Resynchronization Therapy-Defibrillators (CRT-D)

- 5.1.5.2 Cardiac Resynchronization Therapy-Pacemakers (CRT-P)

- 5.1.1 Ventricular Assist Devices (VADs)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Berlin Heart GmbH

- 6.1.3 Biotronik SE & Co. KG

- 6.1.4 Boston Scientific Corporation

- 6.1.5 Jarvik Heart Inc.

- 6.1.6 Lepu Medical Technology(Beijing)Co.,Ltd.

- 6.1.7 Magenta Medical Ltd

- 6.1.8 MEDICO S.R.L.

- 6.1.9 Medtronic PLC

- 6.1.10 Oscor, Inc.

- 6.1.11 OSYPKA MEDICAL

- 6.1.12 Shree Pacetronix Ltd