|

市場調査レポート

商品コード

1940682

自動車搭載充電器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Automotive On-board Charger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車搭載充電器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

概要

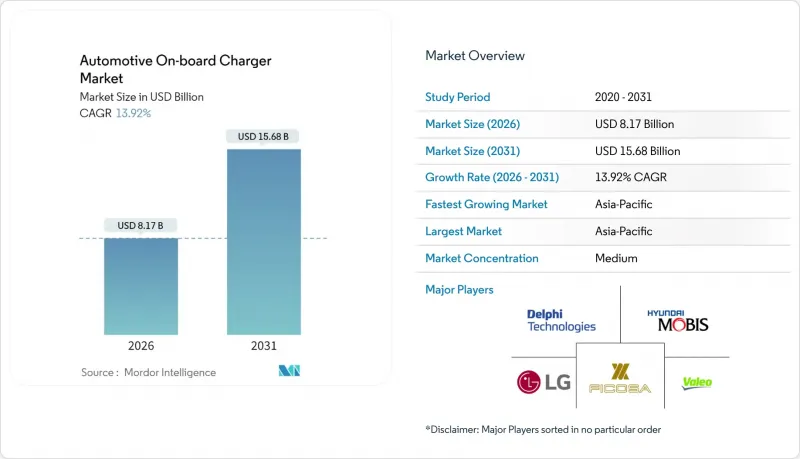

自動車用車載充電器市場は、2025年の71億7,000万米ドルから2026年には81億7,000万米ドルへ成長し、2026年から2031年にかけてCAGR13.92%で推移し、2031年までに156億8,000万米ドルに達すると予測されております。

主要経済圏における電気自動車導入義務化の急増、800V車両プラットフォームへの急速な移行、およびワイドバンドギャップ半導体の価格安定的な低下は、総合的に仕様アップグレードのサイクルを強化し、高出力充電ソリューションに対する全体的な需要を押し上げております。欧州および一部のアジア市場では、自動車メーカーが三相住宅用グリッドを活用し、11~22kWユニットの標準化を進めています。北米のOEMメーカーは、コスト感度と連邦政府のインセンティブを両立させつつ、国内充電器生産とISO 15118準拠を優先しています。ティア1サプライヤーが、従来のバリューチェーンを迂回してトラクション統合型アーキテクチャを追求する半導体専門企業とのシェア争いを展開する中、競争の勢いはさらに強まっています。同時に、政策立案者はアルミニウム筐体に対する安全性とリサイクル性に関する規制を強化しており、これにより設計変更の必要性が増加し、サプライヤーの収益機会が拡大しています。これらの構造的要因が相まって、自動車用車載充電器市場は今後10年間にわたり二桁成長を維持すると見込まれます。

世界の車載充電器市場の動向と洞察

積極的な世界のEV普及目標と購入インセンティブ

各国におけるゼロエミッション規制と購入補助金の導入により、OEM各社が競争力のある総所有コスト(TCO)提案を実現しようと競う中、車載充電器の基本仕様が向上しています。中国の2025年新エネルギー車販売目標、欧州連合(EU)の2030年向け全車両CO2排出量半減要件、カリフォルニア州の先進クリーンカーIIプログラムが相まって、11kWまたは22kWのAC充電機能を標準装備とするモデル投入が加速しています。韓国が2020年代末までにEV普及率の大幅な向上を目指す中、現代モービスは2020年代後半から統合充電制御ユニット(ICCU)の生産拡大を予定しております。この動きは地域的な需要急増を裏付けるものであり、SiCデバイスの価格低下に寄与しております。一方、補助金制度では家庭用充電器購入補助券の提供が増加しています。この施策は、高出力ウォールボックスへの投資における消費者の回収期間を短縮するだけでなく、双方向電力フローや車載充電器向けISO 15118認証といった先進機能への自動車メーカーの投資を正当化する役割も果たしています。

800V車載システムへの急速な移行が11-22kW車載充電器を実現

800V電気システムへの移行は、銅の質量や熱負荷を比例的に増加させることなく高電力密度を実現することで、コストパフォーマンスの限界を再定義します。現代自動車のE-GMPやGMのUltiumは急速充電シナリオを実現し、22kWのAC充電能力は住宅用エネルギーアービトラージの自然な補完となります。FORVIA HELLAなどのサプライヤーはインフィニオンのCoolSiCモジュールをコンパクト筐体に統合し、最大効率を達成するとともに冷却プレート面積を3分の1削減。これによりボンネット下のスペースを補助電子機器用に確保しています。早期導入企業は充電時間短縮を武器に価格プレミアムを獲得し、インセンティブ適格性を最低充電性能基準と連動させる市場において貴重なコンプライアンスクレジットを確保します。ティア1サプライヤーが800V対応設計を事前認定する中、二次導入企業は設計期間の短縮に直面し、ターンキーリファレンスプラットフォームへの需要が高まっています。この相乗効果により基本グレードの電力定格が向上し、車載充電器市場は従来の3.3~7.4kWの軸を超えた規模拡大を遂げています。

22kW三相車載充電器におけるワイドバンドギャップ基板の持続的な高コスト

ファウンドリの記録的な拡張にもかかわらず、SiCブールの歩留まりは5分の3未満、GaNエピウェハーのリードタイムは30週間を超え、基板コストの高止まりが続いております。自動車グレードの650V SiC MOSFETダイは、平面シリコンIGBTと比較して依然として3~4倍のプレミアム価格が維持されており、高出力三相設計はプレミアムブランド車種や商用車隊に限定されています。放熱板やEMIシールドはシステム材料コストをさらに押し上げ、ワイドバンドギャップ採用による密度向上の効果を一部相殺しています。コスト重視のCセグメントクロスオーバー車において、0.02米ドル/Wの価格差は概ね45米ドルの部品コスト増加に相当し、価格弾力性のある市場では小売マージンを圧迫します。このためOEMメーカーは、コスト曲線が低下するまで欧州以外の地域で22kWオプションコードの導入を延期しており、自動車搭載充電器市場における次世代充電器の普及率に一時的な上限が生じています。

セグメント分析

商用車は2025年から2031年にかけて14.05%という最速のCAGRを記録しましたが、2025年時点では乗用車が車載充電器市場規模の65.82%を占めていました。デポ中心の稼働サイクルでは待機時間の最小化が重視されるため、物流事業者は夜間エネルギー処理能力の最大化と電力会社の需要応答プログラムへの参加を目的に、22kW双方向充電器を指定しています。

乗用車は、より大きな潜在的なナンバープレートベースにより、絶対的な出荷台数を引き続き支えますが、プラットフォームの共通化がオプション価格設定の自由度を制限するため、その単価貢献度は低下します。安全規制、サイバーセキュリティ要件、リサイクル性規則の統合により、フリート専用ソリューション向けの非反復的エンジニアリング費用が増大し、専門サプライヤーにマージンバッファーをもたらします。フリートはまた、充電器利用状況ダッシュボードや予防保全アラートといった付加価値分析を先導し、統合型OBCソリューションの収益化を差別化しています。結果として、車種別の動向は異なる成長軌道を形成しますが、全体として自動車車載充電器市場は二桁の収益成長を維持します。

2025年時点で、バッテリー電気自動車(BEV)は自動車用車載充電器市場シェアの76.18%を占め、2031年までCAGR14.02%で首位を維持する見込みです。純粋な電気式スケートボード構造は、後輪軸上部の空間を解放し、OBC、トラクションインバーター、DC-DCステージが標準冷却ループを共有する集中型パワーエレクトロニクスベイの設置を可能にします。床下燃料タンクの制約により、このパッケージングはPHEVレイアウトでは再現できないコスト削減の協業を実現します。

プラグインハイブリッド車は規制対応や地方市場のニッチ需要に応え続けていますが、デュアル燃料の複雑さから、コストと重量管理のためOBC定格は7.4kW前後で頭打ちとなっています。中国や欧州の規制クレジット制度ではPHEVに対するボーナス倍率が段階的に引き下げられており、プレミアム充電機能のビジネスケースは縮小傾向にあります。サプライヤーは、BEVフリート向けにファームウェアのカスタマイズを優先し、動的位相切り替えや高調波低減を実現する一方、PHEV設計は主に派生品として維持しています。2029年までに西欧の新車登録台数の半数をBEVが占める見込みであることから、サプライヤーはBEV専用OBCが総収益の85%以上を占めると予測しており、自動車用車載充電器市場の長期的な成長見通しを確固たるものにしています。

地域別分析

アジア太平洋地域は2025年に自動車用車載充電器市場規模の37.35%を占め首位に立ち、中国のGB38031-2025バッテリー安全基準と記録的なEV導入促進策に支えられ、2031年までCAGR14.07%で他地域を上回る成長を継続します。2023年末までに、中国本土では数百万台の公共・民間充電ユニットが設置されました。この節目は充電密度基準を設定し、共有三相ライザーを備えた高層マンションにおける家庭用充電の実現を可能にしました。アルミニウム筐体のリサイクル割当量に対応するため、中国工業情報化部は材料代替イニシアチブを推進しています。

欧州は第2位の市場として、引き続き力強い成長を見せております。この勢いは主に、AFIR(欧州自動車インフラ規則)によるISO 15118規格の互換性義務化と、欧州横断交通ネットワーク沿線における充電ステーションの必要密度基準によって支えられております。ドイツとフランスでは、電力系統の炭素強度安定化のため、原子力と再生可能エネルギーを系統に統合しています。この統合により、電力会社は中~大容量充電器のV2G(車両から系統への電力供給)機能を活用し、動的料金プランの提供が可能となりました。

北米では、インフレ抑制法に基づく先進製造税額控除の恩恵を受けております。加えて、NEVI資金による回廊開発が地域のインフラ強化に寄与しています。しかしながら、高容量充電器の普及は高級ブランド以外では限定的であり、その主な要因は単相住宅用サービスの制約にあります。これに対応し、OEMメーカーは高出力のデュアル充電器を提供していますが、市場浸透率は依然として控えめです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 積極的な世界の電気自動車導入目標と購入奨励策

- 800V車載アーキテクチャへの急速な移行が11-22kW OBCを実現

- SIC/GANデバイスの価格低下によるOBC電力密度の向上

- EUおよび米国における資金調達スキームにおけるISO 15118の義務化/プラグアンドチャージおよびV2G対応条項

- ティア1/OEMメーカーのトラクション統合型・双方向OBC(3-in-1 E-Axle)への移行

- 新興市場における太陽光発電システム統合業者チャネル:屋根設置型太陽光発電+OBC対応EVパッケージのバンドル販売

- 市場抑制要因

- 22kW三相OBCにおけるワイドバンドギャップ基板の持続的な高コスト

- 直流超急速充電器(350kW以上)の導入加速に伴い、交流充電器の仕様向上にOEMメーカーが消極的

- 高密度都市における住宅用11kW増設の系統連系ボトルネック

- 中国におけるスクラップリサイクル規制の施行が迫る大型OBCアルミハウジングへの課税

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額(米ドル)および数量(台数))

- 車両タイプ別

- 乗用車

- 商用車

- パワートレインタイプ別

- バッテリー式電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- 出力定格別

- 3.3 kW未満

- 3.3~11 kW

- 11kW以上

- 販売チャネル別

- OEM搭載

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ナイジェリア

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- BorgWarner Inc.

- Hyundai Mobis

- LG Electronics

- STMicroelectronics

- Ficosa International S.A.

- Valeo SE

- Delta Energy Systems AG

- Toyota Industries Corp.

- Brusa Elektronik AG

- VisIC Technologies

- Infineon Technologies AG

- Eaton Corp.

- DENSO Corp.

- Panasonic Industry

- TDK Corp.

- Onsemi

- Stercom Power Solutions

- Delta-Q Technologies