|

市場調査レポート

商品コード

1690700

世界の溶剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Global Solvents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の溶剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

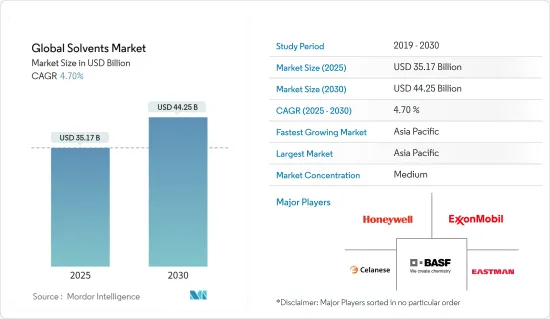

世界の溶剤市場規模は2025年に351億7,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは4.7%で、2030年には442億5,000万米ドルに達すると予測されます。

溶剤市場は、COVID-19パンデミックの影響を受け、塗料やコーティング剤、ポリマー、接着剤などの業界が封じ込め対策や経済的混乱により生産の遅れを余儀なくされるなど、生産と移動に減速が見られました。しかし、2021年には状況が回復し、市場の成長軌道が回復しました。

主なハイライト

- 短期的には、塗料・コーティング分野からの需要の急増と、VOC排出を最小限に抑えるための厳しい規制が、調査対象市場の需要を牽引する主な要因となっています。

- しかし、高い製造コスト、溶剤の性能問題、化学溶剤の有害作用が市場成長の妨げになると予想されます。

- とはいえ、酸素ベースの工業用溶剤の開発とバイオベース製品への需要の増加は、この市場に新たな機会をもたらすと期待されています。

- アジア太平洋が世界市場を独占すると予想され、需要の大半は中国とインドからもたらされます。

溶剤市場の動向

市場を独占する塗料・コーティング剤セグメント

- 溶剤は塗料とコーティング剤の調合に不可欠であり、その性能と用途に大きな影響を与えます。

- 溶剤は、塗料やコーティング剤の樹脂、顔料、その他の成分を溶かすのに役立ち、均一な混合物を作り、塗料やコーティング剤をスムーズかつ均一に塗布できるようにします。

- ケトン系溶剤は、粘度が低く、固形分が多いため、業界で好まれています。エステル系溶剤は、塗料の硬化剤としての役割と、工業用洗浄剤としての役割という2つの役割を果たします。

- バイオベースの溶剤は、塗料やコーティング剤のバインダーや色を溶解し、一貫性を確保します。グリコールエーテルエステルは、装飾塗料やスプレー塗料に配合され、早期乾燥を防ぎます。

- 溶剤は塗料やコーティング剤の粘度を調整し、塗布やレベリングを容易にします。

- WPCIA(Worlds Paint and Coatings Industry Association)によると、世界の塗料・コーティング市場は2023年に1,855億米ドルの評価額を達成し、前年比3.2%増となりました。この上昇の主な要因は、建設、自動車、製造セクターにおける需要の高まりです。

- さらに、WPCIAのデータによると、アジア太平洋は世界最大の塗料・コーティング剤生産国で、2023年の世界生産量の54.7%を占め、次いで欧州(19.6%)、北米(15.6%)、ラテンアメリカ(6.4%)、中東・アフリカ(3.6%)となっています。このように、塗料とコーティング産業の拡大は、調査された市場を促進すると予想されます。

- 米国は、世界最大かつ最も技術的に進んだ経済のひとつです。この圧倒的な地位により、同国は塗料・コーティング市場のホットスポットのひとつとなりました。米国は世界でもトップクラスの塗料・コーティングメーカーであり、1,400社以上の製造会社があります。

- 米国塗料協会によると、米国における塗料・コーティング産業の生産量は、2023年には約13億1,000万ガロンとなりました。さらに、同産業の生産量は2024年には13億4,000万ガロンを超えると推定されています。PPG、Sherwin-Williams Company、Axalta Coating Systems、RPM Inc.、Diamond Paintsは、米国の主要な塗料・コーティング剤メーカーおよびサプライヤーです。

- フランスの塗料・コーティング業界における最近の動向は、溶剤に対する需要の高まりを示唆しています。特筆すべき例は、2023年12月にフランスのトゥールーズに開設されたPPGの1,700万米ドルの航空宇宙アプリケーション・サポート・センター(ASC)です。このセンターは、多様な航空機用のコーティング剤とシーリング剤を含む航空宇宙材料の充填と包装を提供します。

- このような力学を踏まえると、塗料・コーティング分野では溶剤の需要が高まり、今後数年間の市場成長を牽引すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、接着剤、塗料・コーティング剤、パーソナルケア、医薬品、その他の用途など、多様な用途で消費量が増加していることから、世界の溶剤市場の大部分を占めています。この動向は、同地域を今後数年間の市場リーダーとして位置づけています。

- 塗料やコーティング剤の配合において、溶剤は不可欠です。溶剤は成分を溶解、分散、安定化させ、粘度や流動性を調整して滑らかな仕上がりを実現します。大手メーカーが生産能力を拡大し、塗料・コーティング部門が成長しているため、溶剤の需要は増加する傾向にあります。

- European Coatingsの報告によると、世界の工業化の拠点である中国には、1万社もの塗料メーカーがあります。特に、日本ペイント、アクゾノーベル、PPGインダストリーズなどの大手企業が中国に製造拠点を設けています。

- 中国塗料工業協会の統計によると、2023年の中国の塗料生産量は357億7,200万トンに達し、前年比4.5%増となりました。輸出は19.6%増の26万2,000トンと急増し、国内消費は4.2%増の356億6,300万トンと、このセクターの力強い成長を裏付けています。

- メーカー各社は新工場を設立したり、既存設備の能力を増強したりしています。こうした戦略的な動きが塗料・コーティングの需要を高め、市場の成長を下支えしています。

- 例えば、2024年1月、ベルジェー・ペイント・インディアは、オディシャ州の新しいグリーンフィールド複合工場に1,000カロールインドルピー(~1億2,060万米ドル)以上を投入する計画を発表しました。この大胆な投資は、近い将来、塗料とコーティング剤の需要を喚起し、研究市場に利益をもたらすと思われます。

- 溶剤は接着剤の配合において極めて重要であり、材料の効果的な接着を保証します。接着剤産業における拡張プロジェクトは市場成長を後押しすると予想されます。

- 例えば、2023年6月にHenkel AG &Co.KGaAは、中国山東省の煙台化学工業園に接着剤の新しい製造施設を開設すると発表しました。同社はこの拡張プロジェクトを通じて、中国でインパクトのある接着剤製品を製造し、市場の成長を支えることを目指しています。

- 化粧品分野では、溶剤は成分の溶解や安定化に役立っています。同地域の化粧品産業が盛んになるにつれ、溶剤の需要も高まると予想されます。

- 中国国家統計局の報告によると、化粧品部門は過去10年間で急速に拡大しました。2023年の中国における化粧品小売売上高は約4,141億7,000万人民元(~584億米ドル)に達し、前年から緩やかに増加しました。

- 韓国は世界の美容市場のトップ10にランクされ、その革新性、天然成分の使用、魅力的なパッケージングで称賛されています。食品医薬品安全部(MFDS)のデータによると、韓国の化粧品輸出は2023年に85億米ドルに達し、世界第4位の地位を確保します。

- 医薬品分野では、溶剤は医薬品有効成分(API)や医薬品の製造工程を促進します。同地域の製薬産業は増加傾向にあり、溶剤の需要は拡大するとみられます。

- インドの製薬業界は、手頃な価格で高品質の医薬品を世界的に供給していることで有名であり、急速な科学の進歩を目の当たりにしています。政府の予測によると、同産業の市場規模は現在の500億米ドルから2030年には1,300億米ドル、2047年には4,500億米ドルに急増すると見込まれています。このような成長は、予測期間中、医薬品製造における溶剤の需要を促進すると予想されます。

- このようなダイナミクスを考えると、アジア太平洋の溶剤需要は今後数年で上昇するものと思われます。

溶剤業界の概要

溶剤市場は部分的に統合されています。主な企業は、Eastman Chemical Company、BASF SE、Exxon Mobil Corporation、Honeywell International Inc.、Celanese Corporationなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塗料・コーティング分野からの需要急増

- VOC排出を最小限に抑えるための厳しい規制

- その他の促進要因

- 抑制要因

- 高い製造コストと溶剤の性能問題

- 化学溶剤の有害な影響

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 原料別

- バイオベース溶剤

- 石油化学系溶剤

- タイプ別

- 酸素系溶剤

- 炭化水素系溶剤

- ハロゲン系溶剤

- 用途別

- 接着剤

- 塗料

- パーソナルケア

- 医薬品

- ポリマー製造

- その他の用途(印刷インキ、農薬、金属洗浄)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ADM

- Arkema

- Ashland

- BASF SE

- Bharat Petroleum Corporation Limited

- Celanese Corporation

- Dow

- Eastman Chemical Company

- Exxon Mobil Corporation

- Gandhar Oil Refinery(India)Limited

- GROUPE BERKEM

- Honeywell International Inc.

- Huntsman International LLC

- INEOS

- LyondellBasell Industries Holdings BV

- Sasol Limited

- Shell PLC

- Solvay

第7章 市場機会と今後の動向

- 酸素系工業溶剤の開発

- バイオベース製品の需要増加

- その他の機会

The Global Solvents Market size is estimated at USD 35.17 billion in 2025, and is expected to reach USD 44.25 billion by 2030, at a CAGR of 4.7% during the forecast period (2025-2030).

The solvents market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries such as paints and coatings, polymers, and adhesives, etc., were forced to delay their production due to containment measures and economic disruptions. However, the conditions recovered in 2021, restoring the market's growth trajectory.

Key Highlights

- Over the short term, surging demand from the paints and coatings sector and stringent regulations in place to minimize VOC emissions are the major factors driving the demand for the market studied.

- However, high manufacturing costs, performance issues of solvents, and detrimental effects of chemical solvents are expected to hinder the market's growth.

- Nevertheless, the development of oxygenated-based industrial solvents and increasing demand for bio-based products are expected to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the global market, with the majority of demand coming from China and India.

Solvents Market Trends

Paints and Coatings Segment to Dominate the Market

- Solvents are integral to formulating paints and coatings, significantly influencing their performance and applications.

- Solvents help to dissolve the resin, pigment, and other components of the paint or coating, creating a uniform mixture and ensuring that the paint or coating can be applied smoothly and evenly.

- Ketones are favored in the industry for their low-viscosity properties and high solid content. Ester solvents serve a dual purpose: acting as hardeners in paints and functioning as industrial cleaners.

- Bio-based solvents dissolve binders and colors in paints and coatings and ensure consistency. Glycol ether esters are incorporated into decorative and spray paints to prevent premature drying.

- Solvents adjust the viscosity of paints and coatings, facilitating easier application and leveling, which is especially crucial for spray or brush-on coatings.

- According to the Worlds Paint and Coatings Industry Association (WPCIA), the global paint and coatings market achieved a valuation of USD 185.5 billion in 2023, marking a 3.2% increase from the prior year. This uptick was largely fueled by heightened demand across the construction, automotive, and manufacturing sectors.

- Furthermore, Asia-Pacific is the largest producer of paint and coatings globally, accounting for 54.7% of global production in 2023, followed by Europe (19.6%), North America (15.6%), Latin America (6.4%), and Middle East and Africa (3.6%) as per the data from WPCIA. Thus, expansion in the paints and coatings industry is anticipated to drive the market studied.

- The United States represents one of the largest and most technologically advanced economies globally. This dominant position enabled the country to become one of the hotspots for the paints and coatings market. It is one of the top global paints and coatings producers, with more than 1,400 manufacturing companies.

- According to the American Coatings Association, the paint and coatings industry's production volume in the United States was approximately 1.31 billion gallons in 2023. Moreover, the industry's production is estimated to surpass 1.34 billion gallons in 2024. PPG, Sherwin-Williams Company, Axalta Coating Systems, RPM Inc., and Diamond Paints are a few major paints and coatings manufacturers and suppliers in the United States.

- Recent developments in the French paints and coatings industry hint at a growing demand for solvents. A notable example is PPG's USD 17 million aerospace application support center (ASC), inaugurated in Toulouse, France, in December 2023. This center provides filling and packaging for aerospace materials, encompassing coatings and sealants for diverse aircraft.

- Given these dynamics, the paints and coatings sector is expected to see a rising demand for solvents, driving the market's growth in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific commands a significant portion of the global solvents market, driven by rising consumption across diverse applications, including adhesives, paints and coatings, personal care, pharmaceuticals, and other applications. This trend positions the region as a likely market leader in the coming years.

- In the formulation of paints and coatings, solvents are essential. They dissolve, disperse, and stabilize components, adjusting viscosity and flow to ensure a smooth finish. With major manufacturers expanding production capacities and the paints and coatings sector growing, the demand for solvents is set to rise.

- China, a global hub for industrialization, boasts a staggering 10,000 coatings manufacturers, as reported by European Coatings. Notably, major players like Nippon Paint, AkzoNobel, and PPG Industries have established manufacturing bases in the country.

- Figures from the China Coatings Industry Association revealed that in 2023, China's coatings production hit 35,772 million tons, a 4.5% increase from the previous year. Exports surged by 19.6% to 262,000 tons, while domestic consumption rose by 4.2% to 35,663 million tons, underlining the sector's robust growth.

- Manufacturers are either setting up new plants or ramping up the capacities of their existing facilities. These strategic moves bolster the demand for paints and coatings and underpin the market growth.

- For instance, in January 2024, Berger Paints India announced plans to inject over INR 1,000 crore (~ USD 120.6 million) into a new greenfield composite plant in Odisha, focusing on decorative and industrial paints. This bold investment is poised to catalyze the demand for paints and coatings in the near future, thus benefiting the market studied.

- Solvents are pivotal in adhesive formulations, ensuring effective bonding of materials. The expansion projects in the adhesives industry are expected to boost market growth.

- For instance, in June 2023, Henkel AG & Co. KGaA announced that it would be opening a new manufacturing facility for adhesives in Yantai Chemical Industry Park in Shandong Province, China. The company aims to manufacture high-impact adhesive products in China through this expansion project, thereby supporting the market's growth.

- In the cosmetics sector, solvents are instrumental in dissolving and stabilizing ingredients. As the cosmetic industry in the region flourishes, the demand for solvents is expected to rise.

- The National Bureau of Statistics of China reported that the cosmetics sector has expanded rapidly over the past decade. In 2023, retail cosmetics sales in China reached approximately CNY 414.17 billion (~USD 58.4 billion), marking a modest uptick from the prior year.

- South Korea ranks among the top ten global beauty markets and is celebrated for its innovation, use of natural ingredients, and attractive packaging. According to the Ministry of Food and Drug Safety (MFDS) data, South Korea's cosmetics exports hit USD 8.5 billion in 2023, securing the fourth position globally.

- In the pharmaceutical sector, solvents facilitate processes in manufacturing active pharmaceutical ingredients (APIs) and drug products. With the region's pharmaceutical industry on the rise, the demand for solvents is set to grow.

- The Indian pharmaceutical industry, renowned for supplying affordable, high-quality medicines globally, is witnessing rapid scientific advancements. Government projections estimate the industry's value will soar from USD 50 billion today to USD 130 billion by 2030 and an ambitious USD 450 billion by 2047. Such growth is anticipated to drive the demand for solvents in pharmaceutical drug production during the forecast period.

- Given these dynamics, the demand for solvents in Asia-Pacific is poised for an upswing in the coming years.

Solvents Industry Overview

The solvents market is partially consolidated in nature. The major players include Eastman Chemical Company, BASF SE, Exxon Mobil Corporation, Honeywell International Inc., and Celanese Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Surging Demand from the Paints & Coatings Sector

- 4.1.2 Stringent Regulations in Place to Minimize VOC Emissions

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Manufacturing Costs and Performance Issues of Solvents

- 4.2.2 Detrimental Effects of Chemical Solvents

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Source

- 5.1.1 Bio-based Solvents

- 5.1.2 Petrochemical-based Solvents

- 5.2 By Type

- 5.2.1 Oxygenated Solvents

- 5.2.2 Hydrocarbon Solvents

- 5.2.3 Halogenated Solvents

- 5.3 By Application

- 5.3.1 Adhesives

- 5.3.2 Paints and Coatings

- 5.3.3 Personal Care

- 5.3.4 Pharmaceuticals

- 5.3.5 Polymer Production

- 5.3.6 Other Applications (Printing Inks, Agricultural Chemicals, and Metal Cleaning)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Bharat Petroleum Corporation Limited

- 6.4.6 Celanese Corporation

- 6.4.7 Dow

- 6.4.8 Eastman Chemical Company

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 Gandhar Oil Refinery (India) Limited

- 6.4.11 GROUPE BERKEM

- 6.4.12 Honeywell International Inc.

- 6.4.13 Huntsman International LLC

- 6.4.14 INEOS

- 6.4.15 LyondellBasell Industries Holdings BV

- 6.4.16 Sasol Limited

- 6.4.17 Shell PLC

- 6.4.18 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Oxygenated Based Industrial Solvents

- 7.2 Increasing Demand for Bio-based Products

- 7.3 Other Opportunities