|

市場調査レポート

商品コード

1273390

マグネシウム合金市場- 成長、動向、予測(2023年-2028年)Magnesium Alloy Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| マグネシウム合金市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年04月14日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

マグネシウム合金市場は、予測期間中に約4%のCAGRで推移すると予想されています。

COVID-19により、市場はマイナスの影響を受けました。サプライチェーンの混乱、ウイルスの拡散を遅らせるために政府当局が課した措置による作業停止などが、市場に悪影響を及ぼしました。したがって、COVID-19の発生によるこうした影響や不確実性は、マグネシウム合金市場にとって足かせとなっています。しかし、市場は勢いを取り戻し、今後数年で回復すると予想されています。

主なハイライト

- 軽量化を目的としたエンジニアリング部品の生産活動が活発化していることが、市場成長の主な促進要因となっています。

- 逆に、マグネシウム合金の腐食や溶接に関連する問題は、市場成長の妨げになると予想されます。

- 人工の人体インプラントや医療機器におけるマグネシウム合金の成長機会は、市場成長の好機といえるでしょう。

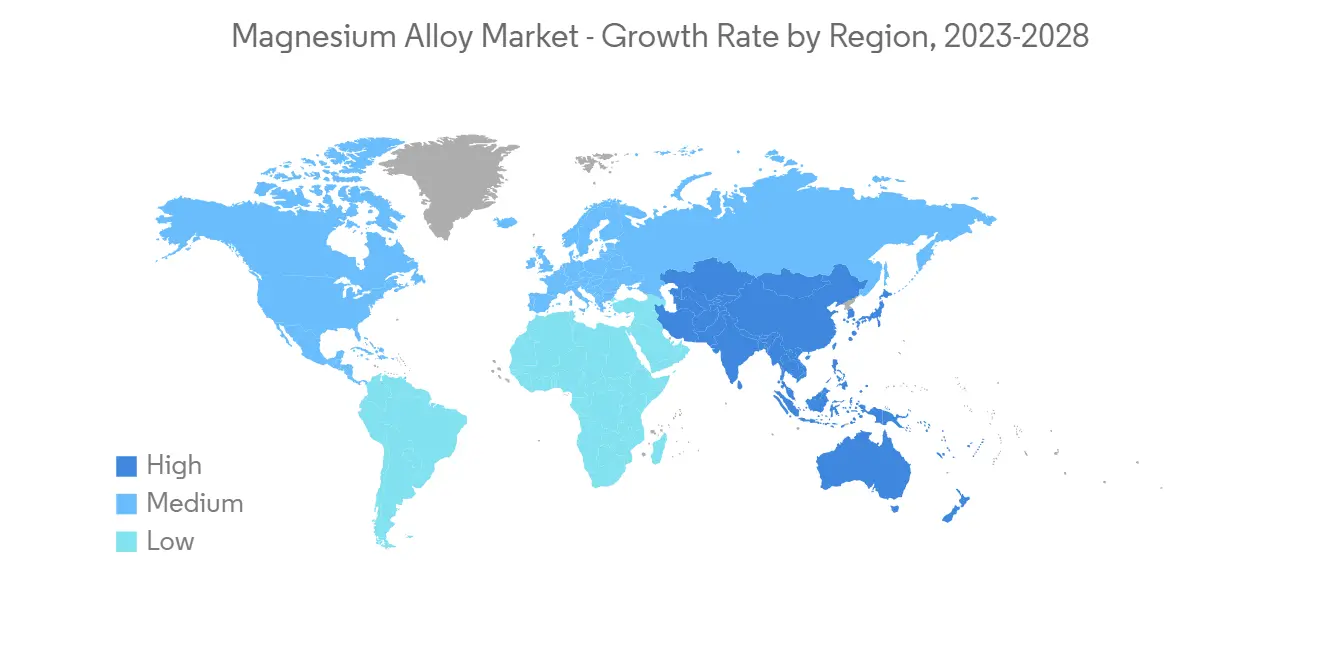

- アジア太平洋が世界を支配し、中国とインドからの消費が最も大きいです。

マグネシウム合金の市場動向

自動車および航空宇宙産業からの需要増加

- マグネシウム合金のアプリケーションは、さまざまな利点をもたらします。エンジンブロックやホイールの製造に採用され、特にスポーツカーの軽量化をサポートします。

- 自動車メーカーは、自動車の燃費と性能を向上させるために、マグネシウム合金を生産に使用しています。マグネシウム合金は高温に強いため、自動車のエンジンブロックに好んで使用されています。

- OICAによると、2021年の世界の自動車生産台数は8,010万台となり、前年の7,760万台から4%増加しました。

- アウディ、メルセデス・ベンツ、フォード、ジャガー、フィアット、起亜自動車株式会社など、多くの大手自動車メーカーが、すでに自動車の鉄やアルミをマグネシウム合金に置き換えています。2022年度、AUDI AGは全世界で1,212,275台の車両を納入し、469億8,000万米ドルの売上を獲得しています。

- マグネシウム合金は最も高い引張強度を示し、他の鍛造合金とは一線を画しています。マグネシウム-亜鉛-ジルコニウム合金は主に専門的なソリューションに使用され、トリウムを含む合金は高温での作業に使用されます。

- 例えば、ZK60合金は、高い強度と動的負荷への耐性が求められる航空機部品に使用されています。Luxfer MEL Technologies社が製造するElektron 43マグネシウム合金は、航空機のシートフレームに使用されるため、連邦航空局(FAA)による大規模な燃焼性テストを受けました。

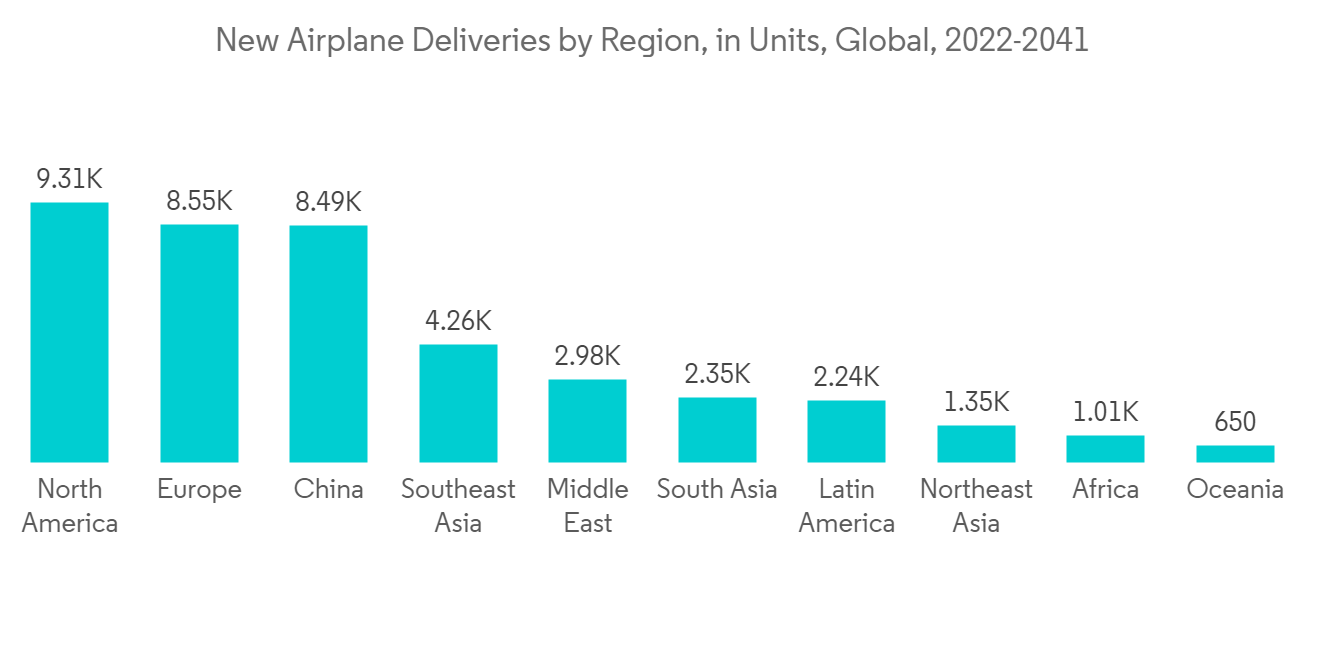

- 航空旅客の増加や貿易業務のための航空輸送による民間航空機の需要拡大が、マグネシウム合金の生産を誘発しました。例えば、北米では、「Boeing Commercial Outlook 2022-2041」によると、2041年までに新型航空機の総納入数は9,310機、市場サービス額は1兆450億米ドルを占めています。

- これらの動きは、予測期間中にマグネシウム合金の需要を押し上げると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は、中国の自動車産業が高度に発展し、航空宇宙部品の生産が近年開拓されていることから、世界市場を独占すると予想されます。また、中国、台湾、韓国は、カメラ、携帯電話、ノートパソコン、ポータブルメディアデバイスの製造など、電子機器の生産拠点が充実しています。

- JEITA(一般社団法人電子情報技術産業協会)によると、2022年11月、電子産業の総生産額は70億9,834万米ドルに達しました。2022年12月、日本は83億9,545万米ドル相当のエレクトロニクスを輸出しました。

- インドでは、エレクトロニクス市場は需要の伸びを目の当たりにし、市場規模は急速に拡大しています。インドの電子製品輸出は、2021年同月の109億9,000万米ドルに対し、2022年12月には166億7,000万米ドルを獲得しました。インドと中国における電子機器・家電市場の成長は、アジア太平洋市場のさらなる成長を後押しする可能性があります。

- 米国国際貿易委員会によると、中国は市場をリードしており、膨大な数のマグネシウム合金製造業があることから、多くのマグネシウム合金を欧州や北米に輸出しています。

- China Export Dataによると、マグネシウム合金の輸出国トップ3は中国で8,955出荷、次いでドイツが2,844出荷、3位が韓国で2,724出荷となっています。

- 2023年2月には、重慶万盛経済開発区が1億4,400万米ドルを投じて、高性能Mg合金生産基地とMg-Al合金研究開発センタープロジェクトの建設を開始しました。

- また、中国、インド、その他ASEAN諸国における各種製造業の成長は、今後のマグネシウム合金の需要を支えるものと期待されます。

マグネシウム合金産業の概要

マグネシウム合金市場は部分的に統合されており、少数の主要企業がかなりの部分を支配しています。主な企業には、Magontec Industry Ltd、Advanced Magnesium Alloys Corporation(AMACOR)、US Magnesium LLC、Smiths Advanced Metalsなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 本調査の対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 軽量化ニーズの高まり

- 電子機器向け鋳造品の需要増加

- 抑制要因

- マグネシウム合金の腐食と溶接に関連する問題

- 代替品との競合

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

第5章 市場セグメンテーション(市場規模:数量ベース)

- 種類別

- 鋳造合金

- 鍛造合金

- エンドユーザー産業別

- 航空宇宙

- 自動車

- 医療

- エレクトロニクス

- その他エンドユーザー産業

- 地域別情報

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 中東およびアフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋地域

第6章 競合情勢

- M&A、ジョイントベンチャー、コラボレーション、契約など

- 市場シェア(%)**/ランキング分析

- 主要企業が採用した戦略

- 企業プロファイル

- Advanced Magnesium Alloys Corporation(AMACOR)

- Canada Magnesium

- Dead Sea Magnesium Ltd

- Hydro Magnesium

- Ka Shui International Holdings Ltd

- MAGONTEC GROUP

- m-tec powder

- Nippon Kinzoku

- Rima Group

- Shanghai Regal Magnesium Limited Company

- Smiths Advanced Metals

- US Magnesium LLC

第7章 市場機会および今後の動向

- 人工関節や医療機器におけるマグネシウム合金の普及率上昇

The magnesium alloy market is expected to register a CAGR of approximately 4% during the forecast period.

The market was negatively impacted due to COVID-19. Due to supply chain disruptions, work stoppages because of the measures imposed by governmental authorities to slow the virus spread negatively impacted the market. Hence, such impact and uncertainties due to the COVID-19 outbreak acted as a stumbling block for the magnesium alloy market. However, the market gained momentum and is expected to recover in the coming years.

Key Highlights

- The increasing production activities of engineering components for weight reduction is the major driving factor for the market growth.

- Conversely, issues associated with the corrosion and welding of magnesium alloys are expected to hinder the market growth.

- The rise in popularity of magnesium alloys in artificial human implants and medical devices is an opportunity for the market's growth.

- Asia-Pacific dominated the globe, with the most significant consumption from China and India.

Magnesium Alloy Market Trends

Increasing Demand from the Automotive and Aerospace Manufacturing Industries

- Magnesium alloy applications offer various benefits. They are employed in the engine block and wheel production, which, in turn, supports weight reduction, especially for sports cars.

- Automotive manufacturers use magnesium alloys in production to increase automobiles' fuel efficiency and performance. Magnesium alloys are resistant to higher temperatures, making them the preferred choice in the engine blocks of automobiles.

- According to the OICA, in 2021, global vehicle production reached 80.1 million units, an increase of 4% from the previous year's production of 77.6 million units.

- Many large automotive manufacturers, like Audi, Mercedes-Benz, Ford, Jaguar, Fiat, and Kia Motors Corporation already replaced steel and aluminum with magnesium alloys in their vehicles. In the fiscal year 2022, AUDI AG delivered 1,212,275 vehicles worldwide and earned a revenue of USD 46.98 billion.

- Magnesium alloy exhibits the highest tensile strength, distinguishing it from other wrought alloys. Magnesium-Zinc-Zirconium alloys are mainly used for specialist solutions, whereas thorium-containing alloys are used for work at elevated temperatures.

- For instance, ZK60 alloy is used for aircraft parts that require high strength and resistance to dynamic loads. Elektron 43 magnesium alloy manufactured by Luxfer MEL Technologies underwent extensive flammability testing by the Federal Aviation Administration (FAA) to be used in the aircraft seat frames.

- The growing demand for commercial aircraft due to increasing air passengers and air transport for trade operations triggered the production of magnesium alloys. For instance, in North America, according to the Boeing Commercial Outlook 2022-2041, the total deliveries of new airplanes accounted for 9,310 units by 2041, with a market service value of USD 1,045 billion.

- These developments are expected to boost the demand for magnesium alloy over the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the global market, owing to China's highly developed automotive sector and the developing production of aerospace components in recent years. China, Taiwan, and South Korea include substantial electronic production bases for manufacturing cameras, cell phones, laptops, and portable media devices.

- According to JEITA (Japan Electronics and Information Technology Industries Association), in November 2022, the total production of the electronics industry reached USD 7,098.34 million. In December 2022, Japan exported electronics worth USD 8,395.45 million.

- In India, the electronics market witnessed a growth in demand, with market size increasing rapidly. India's electronic goods exports fetched USD 16.67 billion in December 2022, compared to USD 10.99 billion in the same month of 2021. The growing electronics and appliances market in India and China may push further Asian-Pacific market growth.

- According to the US International Trade Commission, China leads the market and exports many magnesium alloys to Europe and North America because of the country's vast number of magnesium alloy manufacturing industries.

- According to China Export Data, the top 3 exporters of Magnesium alloy are China with 8,955 shipments, followed by Germany with 2,844, and South Korea at the 3rd spot with 2,724 shipments.

- In February 2023, Chongqing Wansheng Economic Development Zone started the construction of a high-performance Mg-alloy production base and Mg-Al alloy R&D center projects with an investment of USD 144 million.

- Moreover, the growth of various manufacturing industries in China, India, and other ASEAN countries is expected to support the demand for magnesium alloys in the future.

Magnesium Alloy Industry Overview

The magnesium alloy market is partially consolidated, with a few major players dominating a significant portion. Some major companies are Magontec Industry Ltd, Advanced Magnesium Alloys Corporation (AMACOR), US Magnesium LLC, and Smiths Advanced Metals.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Need for Weight Reduction

- 4.1.2 Increasing Demand for Castings in Electronic Applications

- 4.2 Restraints

- 4.2.1 Issues Associated with the Corrosion and Welding of Magnesium Alloys

- 4.2.2 Competition from Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Cast Alloys

- 5.1.2 Wrought Alloys

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Medical

- 5.2.4 Electronics

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) ** /Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Advanced Magnesium Alloys Corporation (AMACOR)

- 6.4.2 Canada Magnesium

- 6.4.3 Dead Sea Magnesium Ltd

- 6.4.4 Hydro Magnesium

- 6.4.5 Ka Shui International Holdings Ltd

- 6.4.6 MAGONTEC GROUP

- 6.4.7 m-tec powder

- 6.4.8 Nippon Kinzoku

- 6.4.9 Rima Group

- 6.4.10 Shanghai Regal Magnesium Limited Company

- 6.4.11 Smiths Advanced Metals

- 6.4.12 US Magnesium LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rise in Popularity of Magnesium Alloys in Artificial Human Implants and Medical Devices