|

市場調査レポート

商品コード

1445521

光触媒: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Photocatalyst - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 光触媒: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

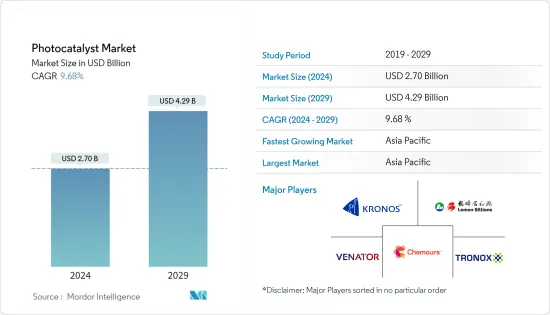

光触媒市場規模は2024年に27億米ドルと推定され、2029年までに42億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.68%のCAGRで成長します。

COVID-19感染症のパンデミックは光触媒市場に悪影響を及ぼしました。現在、市場はパンデミックから回復し、大幅な成長を遂げています。

主なハイライト

- 短期的には、二酸化チタンの高い需要と水処理および空気浄化用途の増加により、光触媒市場の需要が高まる可能性があります。

- しかし、多額の設備投資は市場の成長を妨げると予想されます。

- それにもかかわらず、消毒剤としての研究開発の増加は、魅力的な市場成長を生み出し、予測期間中に大きな可能性をもたらすと予想されます。

- アジア太平洋地域は世界市場を独占すると予想されており、消費の大部分は中国とインドから来ています。

光触媒市場動向

セルフクリーニング用途の需要の増加

- 光触媒によるセルフクリーニングは、おそらく建築建設において最も広く使用されているナノ機能です。世界中の多くの建物がこの機能を利用しています。その主な効果は、表面への汚れの付着の程度を大幅に軽減することです。もう1つの利点は、表面の汚れや不明瞭な汚れの太陽光が少なくなるため、ガラスや半透明の膜の光透過率が向上し、照明エネルギーコストを削減できることです。

- 近年、建物の外面や内部をコーティングする光触媒塗料やコーティングが開発されています。光触媒コーティングは汚れを洗い流すだけでなく、空気中の汚染物質や建物の外面からのスモッグなどの汚染物質や汚れも分解します。さらに、光触媒コーティングは、建物の室内家具から臭気を除去し、VOC、浮遊ウイルス、細菌を分解します。さらに、光触媒コーティングは、建物内部の木の表面を保護するために好まれる主要なオプションの1つです。

- 光触媒材料の応用は大型建築物だけに限定されるものではありません。たとえば、温室やウィンターガーデンにも同様に適しています。道路建設では、透明コーティングを防音壁などに使用することもできます。耐久性のあるコーティングを焼き付けたタイルは、屋内と屋外の両方で使用できます。同様に、ファサードのもう1つの一般的な建築材料であるコンクリートにも、自動洗浄表面を装備することができます。したがって、建設部門は、予測期間中にセルフクリーニング光触媒材料の需要に大きく貢献すると考えられます。

- 世界の建設業界は順調に成長しています。アジア太平洋では、中東やアフリカ地域と同様に、数多くの市場機会が得られるため、建設セクターへの巨額の投資が見られます。

- 中国国家統計局によると、中国の建設生産額は2020年の26兆3,900億元(3兆7,900億米ドル)に対し、2021年には約29兆3,000億元(4兆2,000億米ドル)でピークに達しました。

- 国土交通省(日本)によると、2021年度の日本の総建設投資額は66兆6,000億円(約4億9,810万米ドル)を超え、この支出の半分以上を建築工事が占めています。総建設支出は2022年度には約67兆円(約5億109万米ドル)に達すると予想されています。

- 欧州では、ドイツが建設分野の発展をリードしてきました。アレクサンダー・ベルリンのキャピタル・タワーとエストレル・タワーは、現在この国が開発中の主要な高層ビルの一部です。この国では、インフラ部門への多額の投資と住宅需要の高まりにより、建設部門がさらに成長しています。

- 世界銀行によると、建設業界は2021年に支出額12兆9,000億米ドルに成長し、年間3%の成長が見込まれています。これには、住宅および商業の両方の不動産開発、インフラストラクチャーおよび産業建設が含まれます。建設支出に関するデータには、人件費と材料費、建築工事と土木工事、税金が含まれます。

- セルフクリーニング光触媒コーティングは、自動車のフロントガラス、窓ガラス、高層ビル、顕微鏡、眼鏡、太陽電池パネルのカバー、キッチン家電、多くの電子機器の画面など、多くの用途で使用される光学的に透明なガラス材料のコーティングに使用されます。光学機器。

- 低コスト、軽量、フレキシブルなPC基板上の自動洗浄光触媒コーティングは、多機能の自動洗浄デバイスが有用であるために不可欠です。したがって、自動車、エレクトロニクス、医療、太陽エネルギー生成などの他のエンドユーザー産業も、予測期間における自己洗浄性光触媒材料の需要に大きく貢献すると予想されます。

- 前述のすべての要因は、予測期間中の業界の成長に貢献します。

アジア太平洋地域が市場を独占

- アジア太平洋は、市場シェアと市場収益の点で光触媒市場を独占しています。この地域は、予測期間中引き続きその優位性を維持する予定です。

- 光触媒の超親水性により、自浄作用が得られます。たとえば、二酸化チタンは光触媒保護膜を形成し、超酸化性かつ親水性になることでセルフクリーニングする特性を備えています。光触媒のこの特性は、塗料やコーティングの自己洗浄助剤としての需要の高い用途に応えます。さらに、光触媒として、独自の洗浄および抗菌特性を伝達します。したがって、建設活動の増加に伴い、塗料やコーティングの需要が増加すると予想され、それが光触媒の市場需要を牽引しています。

- 建設、自動車、包装からの需要の増加による塗料およびコーティングの需要の増加は、予測期間中に光触媒市場を牽引すると予想されます。中国は世界の総塗料およびコーティングの約30%を生産しており、塗料やコーティングに誘導される光触媒の自己洗浄特性により、光触媒の消費の主要な供給源となっています。

- PPG Industriesは、6億2,000万元(8,903万米ドル)を投資して、2022年までに南中国の研究開発および生産拠点を建設する予定です。 Asia Cuanonはまた、総投資額6億元(8,616万米ドル)で湖南省長沙に新たな生産拠点を建設する契約にも署名し、これには20万トンの高品質のアーキテクチャ塗料やその他の建設資材が含まれる予定です。

- BASF Coatings(Guangdong)は、アジアで唯一のBASFの自動車補修用塗料の生産拠点です。同社は自動車補修コーティング用の新しい施設を建設中で、2022年上半期に生産を開始します。

- 中国国家統計局によると、中国は世界最大の建設市場に成長しました。 2021年の中国の建設産業の価値は1兆1,174億2,000万米ドルでした。政府は中小規模のコミュニティのインフラ整備に注力する意向であるため、建設産業は年率5%で増加すると予想されています。

- 日本の塗料・コーティング産業は、塗料・コーティング業界の最大の消費者である自動車、化学、家電、電子産業に確立された製造拠点を有しており、アジア太平洋で2番目に大きいです。

- 日本における塗料およびコーティングの生産は、主に建設およびその他の産業部門からの需要の増加によって推進されています。国土交通省によると、2021年度の日本の総建設投資額は66兆6,000億円(4億9,903万米ドル)で、この支出の半分以上を建築工事が占めています。建設投資の総額は、2022年度には約67兆円(5億203万米ドル)に達すると予想されています。

- 国内の需要の増加に伴うこのような塗料生産の拡大は、予測期間中の光触媒の市場需要をさらに促進すると予想されます。

光触媒業界の概要

光触媒市場は本質的に統合されており、上位5社が主要な生産能力を持っています。主要な企業としては、The Chemours Company、Tronox Holdings PLC、Venator Materials PLC、Lomon Billions、KRONOS Worldwide Inc.などが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 急速に高まる二酸化チタンの需要

- 水処理と空気浄化における用途の増加

- 抑制要因

- 多額の設備投資

- その他の抑制要因

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- 二酸化チタン

- 酸化亜鉛

- その他のタイプ

- 用途

- セルフクリーニング

- 空気浄化

- 水処理

- 曇り止め

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他中東およびアフリカ

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場シェア(%)**/ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- Daicel Miraizu Ltd

- Green Millennium

- Hangzhou Harmony Chemical Co. Ltd

- ISHIHARA SANGYO KAISHA Ltd

- KRONOS Worldwide Inc.

- Lomon Billions

- Nanoptek Corp.

- SHOWA DENKO KK

- TAYCA

- The Chemours Company

- TitanPE Technologies Inc.

- Tronox Holdings PLC

- Venator Materials PLC

第7章 市場機会と将来の動向

- 消毒剤として研究開発が進む

The Photocatalyst Market size is estimated at USD 2.70 billion in 2024, and is expected to reach USD 4.29 billion by 2029, growing at a CAGR of 9.68% during the forecast period (2024-2029).

The COVID-19 pandemic had a negative impact on the market for photocatalysts. Currently, the market has recovered from the pandemic and growing at a significant rate.

Key Highlights

- Over the short term, high demand for titanium dioxide and increasing water treatment and air purification applications are likely to drive the demand for the photocatalyst market.

- However, high capital investments are expected to hinder the growth of the market.

- Nevertheless, increasing research and development as a disinfectant is expected to generate attractive market growth and give substantial potential in the forecast period.

- The Asia-Pacific region is expected to dominate the global market, with the majority of the consumption coming from China and India.

Photocatalyst Market Trends

Increasing Demand from Self Cleaning Application

- Photocatalytic self-cleaning is probably the most widely used nano-function in building construction. Numerous buildings around the world make use of this function. Its primary effect is that it greatly reduces the extent of dirt adhesion on surfaces. Another advantage is that light transmission for glazing and translucent membranes is improved since surface dirt and obscure grime sunshine are less, which can reduce lighting energy costs.

- Photocatalytic paints and coatings have been developed in recent years to coat the outer surface and interiors of the building. Photocatalytic coatings not only wash off dirt but also break down contaminants and stains: airborne pollutants, and smog from the exterior surfaces of the building. Furthermore, photocatalyst coatings remove odors and break down VOC, airborne viruses, and bacteria from the interior furniture of the building. Moreover, photocatalyst coating is one of the major options preferred to protect wooden surfaces in the interior of the building.

- The application of photocatalytic material is not limited exclusively to large buildings. It can be equally appropriate, for example, for conservatories and winter gardens. In road building, the transparent coating can also be used, for example, for noise barriers. Tiles with baked-on durable coatings are available for use both indoors and outdoors. Likewise, concrete, another common building material for facades, can also be equipped with a self-cleaning surface. Hence the construction sector will contribute majorly to the demand for self-cleaning photocatalytic materials in the forecast period.

- The global construction industry is growing at a healthy rate. Asia-Pacific, along with the Middle East and African regions, is witnessing huge investments in the construction sector due to numerous market opportunities available in these markets.

- According to the National Bureau of Statistics of China, China's construction output value peaked in 2021 at roughly CNY 29.3 trillion (USD 4.2 trillion), compared to CNY 26.39 trillion (USD 3.79 trillion) in 2020.

- According to The Ministry of Land, Infrastructure, Transport, and Tourism (Japan), total construction investment in Japan was over JPY 66.6 trillion (~USD 498.10 million) in the fiscal year 2021, with building construction accounting for more than half of this expenditure. Total construction spending is expected to reach almost JPY 67 trillion (~USD 501.09 million) in the fiscal year 2022.

- In Europe, Germany has taken the lead in developments in the construction sector. Alexander Berlin's Capital Tower and Estrel Tower are some of the major high-rise buildings the country is developing at present. The construction sector is further rising in the country owing to significant investments in its infrastructural sector and further due to the rising demand for residential units.

- According to World Bank, the construction industry grew to a spending value of USD 12.9 trillion in 2021 and is expected to grow by three percent per annum. This comprises real estate developments, both residential and commercial, as well as infrastructural and industrial constructions. Data on construction spending cover labor and material costs, architectural and engineering work, and taxes.

- The self-cleaning photocatalytic coating is used to coat optically transparent glass materials, which are used in many applications, including automobile windshields, window glass, skyscrapers, microscopes, eyeglasses, solar cell panel covers, kitchen appliances, screens of many electronic devices, and optical instruments.

- The self-cleaning photocatalytic coating on low-cost, lightweight, and flexible PC substrates is crucial for multifunctional self-cleaning devices to be useful. Therefore, other end-user industries, such as automobile, electronics, medical, and solar energy generation, will also contribute significantly to the demand for self-cleaning photocatalytic material in the forecast period.

- All the aforementioned factors will contribute towards industry growth during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominates the photocatalyst market in terms of market share and market revenue. The region is set to continue its dominance over the forecast period.

- The super-hydrophilic nature of photocatalysts imparts the self-cleaning nature. For instance, titanium dioxide provides a photocatalytic protective film, which possesses the property of self-cleaning by becoming super-oxidative and hydrophilic. This property of photocatalyst caters to its high-demand application as self-cleaning aid in paints and coatings. Moreover, as a photocatalyst, it transmits unique cleaning and anti-microbial properties. Hence, with the increasing construction activity, the demand for paint and coatings is expected to increase, which is driving the market demand for photocatalysts.

- The growing demand for paint and coatings due to the growing demand from construction, automotive, and packaging is expected to drive the market for photocatalysts during the forecast period. China produces around 30% of the total global paints and coatings, which is acting as a major source in the consumption of photocatalysts, owing to their self-cleaning properties when induced in paints and coatings.

- PPG Industries plans to construct its South Chinese R&D and production base by 2022, with an investment of CNY 620 million (USD 89.03 million). Asia Cuanon also signed an agreement to construct a new production base in Changsha, Hunan province, with a total investment of CNY 600 million (USD 86.16 million), which will include 200 thousand metric tons of high-quality architecture coatings and other construction materials.

- BASF Coatings (Guangdong) Co. Ltd has the only automotive refinish coatings production site for BASF in Asia. The company is constructing a new facility for automotive refinish coatings that have started production in the first half of 2022.

- According to the National Bureau of Statistics of China, China has grown to become the world's largest construction market. The value of China's construction industry was USD 1,117.42 billion in 2021. Since the government intends to focus on upgrading infrastructure in small and medium-sized communities, the construction industry is expected to increase at a five percent yearly rate.

- The paints and coatings industry in Japan was the second largest in Asia-Pacific, as it has well-established manufacturing bases in the automotive, chemicals, appliance, and electronic industries, which are the largest consumers of the paints and coatings industry.

- The production of paints and coatings in Japan is mainly driven by the growing demand from the construction and other industrial sectors. According to The Ministry of Land, Infrastructure, Transport, and Tourism (MLIT Japan), total construction investment in Japan was YPY 66.6 trillion (USD 499.03 million) in the fiscal year 2021, with building construction accounting for more than half of this expenditure. Total construction investment is expected to reach almost YPY 67 trillion (USD 502.03 million) in the fiscal year 2022.

- All such expansions in paint production with the growing demand in the country are further expected to drive the market demand for photocatalysts during the forecast period.

Photocatalyst Industry Overview

The photocatalyst market is consolidated in nature, with the top five players having major production capacities. Some of the key players are The Chemours Company, Tronox Holdings PLC, Venator Materials PLC, Lomon Billions, KRONOS Worldwide Inc., and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Growing Demand for Titanium dioxide

- 4.1.2 Increasing Applications in Water Treatment and Air Purification

- 4.2 Restraints

- 4.2.1 High Capital Investment

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Titanium dioxide

- 5.1.2 Zinc Oxide

- 5.1.3 Other Types

- 5.2 Application

- 5.2.1 Self-Cleaning

- 5.2.2 Air Purification

- 5.2.3 Water Treatment

- 5.2.4 Anti-Fogging

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Daicel Miraizu Ltd

- 6.4.2 Green Millennium

- 6.4.3 Hangzhou Harmony Chemical Co. Ltd

- 6.4.4 ISHIHARA SANGYO KAISHA Ltd

- 6.4.5 KRONOS Worldwide Inc.

- 6.4.6 Lomon Billions

- 6.4.7 Nanoptek Corp.

- 6.4.8 SHOWA DENKO KK

- 6.4.9 TAYCA

- 6.4.10 The Chemours Company

- 6.4.11 TitanPE Technologies Inc.

- 6.4.12 Tronox Holdings PLC

- 6.4.13 Venator Materials PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Research and Development as a Disinfectant