|

市場調査レポート

商品コード

1689807

有機顔料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Organic Pigments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 有機顔料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

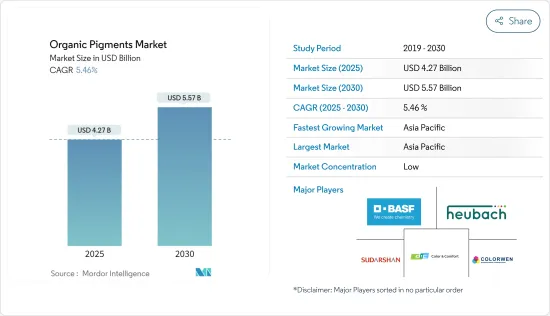

有機顔料市場規模は2025年に42億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.46%で、2030年には55億7,000万米ドルに達すると予測されます。

主要ハイライト

- COVID-19パンデミックは世界の有機市場に打撃を与えました。有機顔料産業は、世界のサプライチェーンの混乱とエンドユーザー部門、特に塗料・コーティング部門からの需要減少の影響を受けました。製造業者は操業停止期間中に生産を停止し、需要の減少につながりました。現在、市場はパンデミックから回復し、かなりの勢いで成長しています。

- 短期的には、塗料・コーティング産業の需要拡大と繊維産業の需要増加が市場を牽引しています。

- 反面、厳しい環境規制による生産コストの上昇や、無機顔料の有機顔料に対する優れた性能が有機顔料市場の成長を妨げています。

- 家具産業は大きな成長の可能性を秘めていると予想されます。有機顔料は、湿気や食べこぼしから木材を保護するのに役立ちます。これらの天然色は、この家具に長持ちする美しさと装飾的な魅力を提供することができます。その拡大の可能性は、市場の総供給率を押し上げると予想されます。

- アジア太平洋は世界の有機顔料市場を独占しており、中国、インド、日本で最も高い消費率を記録しています。

有機顔料市場の動向

塗料とコーティング産業における用途の増加

- 有機顔料は塗料とコーティング産業で広く使用されており、予測期間中に最も急成長する市場になると予想されます。

- 塗料は、建物から橋梁、自動車、電子機器に至るまで、表面を保護するだけでなく美化もします。有機顔料は、微細な顔料化処理によって、鮮やかな色、良好な分散性、高い着色力を記載しています。

- 米国コーティング協会によると、米国における塗料・コーティング産業の製造量は、2022年には約13億6,000万ガロンでした。2023年には13億8,700万ガロンを超えると予想されています。

- 塗料・コーティングは自動車産業において、内装部品と外装部品の両方に、装飾と保護の目的で使用されます。塗布される塗料は、紫外線から外装を保護し、熱、日光、傷、水、アルカリ、酸に対する耐性を提供しなければならないです。

- 国際自動車建設機構(OICA)によると、2022年の世界の自動車生産台数は8,502万台で、前年比6%増となります。2022年には、中国、米国、ドイツが自動車・商用車メーカーのトップ3となります。

- 建設産業では、家具と建築用塗料が最大の塗料消費量を占めています。塗料やコーティング剤は、家具や木材を湿気やその他の流出物から保護します。木材は自然さを伝え、建築の伝統的側面と現代的な側面を融合させています。塗料は家具に装飾的な美しさと耐久性を与えます。

- UN Comtradeによると、2021年の米国への家具の輸入額は約814億米ドル、家具の輸出額は約93億米ドルでした。

- 建設産業における塗料・コーティング需要の増加が、有機顔料市場を牽引すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、インドや中国のような国からの需要の増加により、予測期間中に有機顔料市場を独占すると予想されます。

- 有機顔料の最大の生産者のいくつかはアジア太平洋に位置しています。この市場に進出している企業には、Indian Chemical Industries、Sudarshan Chemical Industries Limited、Koel Colours Pvt Ltd、Hangzhou Han-Color Chemical、Origo Chemicalなどがあります。

- インフラ部門はインド政府の重点セグメントです。持続的な国家成長を確保するため、インドは2019~2023年の間に1兆4,000億米ドルをインフラに投資する計画です。政府は、2018~2030年に鉄道インフラに7,500億米ドルを投資することを提案しています。スマートシティの開発や「house for all」のようなその他の計画は、塗料とコーティングの需要を増加させると予想されます。

- 統計プログラム実施省(MOSPI)によると、インドと中国のインフラと建設活動は急成長しており、家具の消費を増加させています。インドにおける家具製造の収益は、2024年までに40億3,000万米ドルを超えると予想されています。

- Make in India "のような取り組みによる自動車セクタの成長と電気自動車(EV)への投資の増加は、塗料やコーティングにおける有機顔料の範囲を拡大しています。

- 塗料やコーティング以外にも、有機顔料はその不透明性と熱に対する安定性により、プラスチック産業において幅広い用途を提供しています。有機顔料は基材との親和性がないため、染料よりも好まれます。現在、有機顔料は主にポリオレフィンに使用されています。

- アジア太平洋は、世界のプラスチックの半分以上(52%)を製造しています。革新と改良の結果、プラスチックの需要は伸びると予想されます。有機顔料市場は、技術革新とプラスチック使用の増加による需要を予測しています。

- 前述の要因は、政府の支援と相まって、予測期間中の有機顔料市場の需要増加に寄与しています。

有機顔料産業概要

世界の有機顔料市場は部分的にセグメント化されており、大手企業のシェアはわずかです。市場に参入している主要企業には、BASF SE、Sudarshan Chemical Industries Limited、DIC Corp.、Colorwem Int.Corp.、Heubach GmbHなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塗料産業からの需要拡大

- 繊維産業からの需要増加

- その他の促進要因

- 抑制要因

- 厳しい環境規制による生産コストの上昇

- 有機顔料に対する無機顔料の優れた性能

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 顔料タイプ

- アゾ

- フタロシアニン

- キナクリドン

- アントラキノン

- その他の顔料タイプ

- エンドユーザー産業

- 塗料とコーティング

- プラスチックとポリマー

- 印刷と包装

- 繊維

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- Clariant

- COLORWEN INTERNATIONAL CORP.

- DIC CORPORATION

- Hangzhou Han-Color Chemical CO. LTD

- Heubach GmbH

- Indian Chemical Industries

- Koel Colours Pvt Ltd

- Origo Chemical

- Sudarshan Chemical Industries Limited

- Trust Chem Co. Ltd

- VIBFAST PIGMENTS PVT LTD

- Vipul Organics Ltd

- VOXCO India

第7章 市場機会と今後の動向

- 家具産業からの有利な成長機会

- その他の機会

目次

Product Code: 68426

The Organic Pigments Market size is estimated at USD 4.27 billion in 2025, and is expected to reach USD 5.57 billion by 2030, at a CAGR of 5.46% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic harmed the global organic market. The organic pigments industry was impacted by a disrupted global supply chain and reduced demand from end-user sectors, particularly the paints and coatings sector. Manufacturers suspended output during lockdowns, leading to a decrease in demand. Currently, the market has recovered from the pandemic and is growing at a significant rate.

- Over the short term, growing demand in the paints and coatings industry and an increase in the demand from the textile industry are driving the market.

- On the flip side, higher production costs due to stringent environmental regulations and the superior performance of inorganic pigments to organic pigments are hindering the growth of the organic pigments market.

- Nevertheless, the furniture industry is anticipated to have significant growth potential. Organic pigments aid in the protection of wood against moisture and spills. These natural colors can provide long-lasting beauty and decorative appeal to this furniture. Its potential for expansion is expected to boost the market's total supply rate.

- The Asia-Pacific region dominates the global organic pigment market, with the highest consumption rates being registered in China, India, and Japan.

Organic Pigments Market Trends

Increasing Application in the Paints and Coatings Industry

- Organic pigments are extensively used in the paints and coatings industry and are expected to be the fastest-growing market during the forecast period.

- Paints not only protect but also beautifies surfaces from buildings to bridges to automotive to electronics. Organic pigments, through fine pigmentation processing, provide bright color, good dispersion, and high tinting strength.

- According to the American Coatings Association, the manufacture of paint and coatings industry in the United States was around 1.36 billion gallons in 2022. In 2023, the industry's output is expected to exceed 1.387 billion gallons.

- Paints and coatings are used in the automotive industry for both interior and exterior parts for decorative as well as protective purposes. The coatings applied should protect the exteriors from UV radiation and provide resistance against heat, sunlight, scratches, water, alkaline, and acids.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), the world motor vehicle output in 2022 was 85.02 million, a 6% increase over the previous year. In 2022, China, the United States, and Germany were the top three manufacturers of cars and commercial vehicles.

- In the construction industry, furniture and architectural coatings account for the largest consumption of paints. Paints and coatings protect furniture and wood from moisture and other spillages. The wood conveys naturalness, which unites traditional and modern aspects of architecture. Coatings provide decorative beauty and long-lastingness for furniture.

- According to the UN Comtrade, in 2021, the value of furniture imports into the United States was around USD 81.4 billion, while furniture exports were roughly USD 9.3 billion.

- The increase in demand for paints and coatings in the construction industry is expected to drive the organic pigments market.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the organic pigment market during the forecast period due to increased demand from countries like India and China.

- Some of the largest producers of organic pigments are located in the Asia-Pacific region. The companies operating in the market include Indian Chemical Industries, Sudarshan Chemical Industries Limited, Koel Colours Pvt Ltd, Hangzhou Han-Color Chemical Co. Ltd, Origo Chemical, and many others.

- The infrastructure sector is the key focus of the Indian government. To ensure sustained national growth, India plans to invest USD 1.4 trillion in infrastructure between 2019 and 2023. The government has proposed investing USD 750 billion in railway infrastructure from 2018 to 2030. The development of smart cities and other schemes like 'household for all' are expected to increase the demand for paints and coatings.

- The infrastructure and construction activities in India and China have been growing rapidly, which increases the consumption of furniture, according to the Ministry of Statistics and Program Implementation (MOSPI). The revenue from furniture manufacturing in India is expected to be over USD 4.03 billion by 2024.

- The growth in the automotive sector with initiatives like 'Make in India' and the increase in investments in electric vehicles (EVs) is increasing the scope for organic pigments in paints and coatings.

- Apart from paints and coatings, organic pigments offer a wide range of applications in the plastics industry due to their opacity and stability to heat. Organic pigments are preferred over dyes as they have no affinity to the substrate. Currently, organic pigments are mainly used in polyolefins.

- The Asia-Pacific region is responsible for manufacturing more than half (52 percent) of the world's plastic. The demand for plastics is expected to grow as a result of innovations and improvements. The Organic Pigments Market has foreseen demand due to innovations and an increase in the use of plastic.

- The aforementioned factors, coupled with government support, are contributing to the increasing demand for the organic pigments market during the forecast period.

Organic Pigments Industry Overview

The global organic pigments market is partially fragmented, with the major players accounting for a marginal share. A few key companies operating in the market include BASF SE, Sudarshan Chemical Industries Limited, DIC Corp., Colorwem Int. Corp., and Heubach GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Paints and Coatings Industry

- 4.1.2 Increase in Demand from the Textile Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Higher Production Costs Due to Stringent Environmental Regulations

- 4.2.2 Superior Performance of Inorganic Pigments to Organic Pigments

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Pigment Type

- 5.1.1 Azo

- 5.1.2 Phthalocyanine

- 5.1.3 Quinacridone

- 5.1.4 Anthraquinone

- 5.1.5 Other Pigment Types

- 5.2 End-user Industry

- 5.2.1 Paints and Coatings

- 5.2.2 Plastics and Polymer

- 5.2.3 Printing and Packaging

- 5.2.4 Textile

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Clariant

- 6.4.3 COLORWEN INTERNATIONAL CORP.

- 6.4.4 DIC CORPORATION

- 6.4.5 Hangzhou Han-Color Chemical CO. LTD

- 6.4.6 Heubach GmbH

- 6.4.7 Indian Chemical Industries

- 6.4.8 Koel Colours Pvt Ltd

- 6.4.9 Origo Chemical

- 6.4.10 Sudarshan Chemical Industries Limited

- 6.4.11 Trust Chem Co. Ltd

- 6.4.12 VIBFAST PIGMENTS PVT LTD

- 6.4.13 Vipul Organics Ltd

- 6.4.14 VOXCO India

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Lucrative Growth Opportunities from the Furniture Industry

- 7.2 Other Opportunities