|

市場調査レポート

商品コード

1444920

航空機射出座席: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Aircraft Ejection Seat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機射出座席: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 78 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

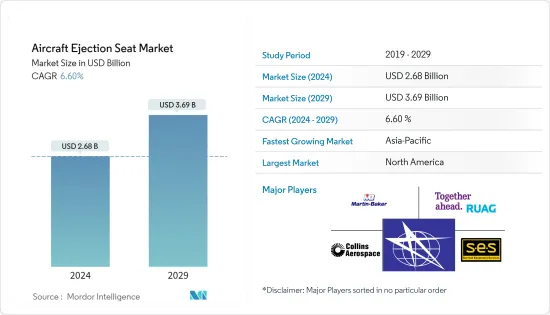

航空機射出座席の市場規模は、2024年に26億8,000万米ドルと推定され、2029年までに36億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.60%のCAGRで成長します。

COVID-19感染症のパンデミックの影響により、サプライチェーンの混乱が企業の成長に影響を及ぼしており、特に固定価格契約の場合、大幅な損失幅に対処しなければならなくなった。世界の軍隊からの需要が持続する限り、業界への長期的な影響はなかったため、2021年には世界中のいくつかの軍用機メーカーの状況が改善されました。

世界規模でパイロット関連の墜落事故が増加しているため、パイロットやその他の乗組員(飛行教官など)の現在の安全基準を強化することに重点を置く必要性が生じています。これにより、射出座席を含むいくつかのコックピット機器の定期的な故障テストが奨励されました。さらに、世界の国防軍が取り組んでいる航空機の近代化と拡張の取り組みも、戦闘機や訓練機に射出座席の設置が義務付けられているため、射出座席の需要も高まっています。

航空機射出座席市場動向

戦闘機セグメントが予測期間中に市場を独占すると予測される

予測期間中、戦闘機分野が市場を支配すると予測されています。地政学的紛争の増加により、各国は敵対勢力に対する戦略的優位性を獲得するため、あるいは防衛能力の点で敵対勢力と肩を並べるために、航空機フリートの近代化とアップグレードを進めている。現在進行中のロシアとウクライナの紛争は、より多くの国が新世代の戦闘機や訓練機を発注し、テンペストやF/A-XXといった第6世代航空機のようなパイプラインプロジェクトの調達や研究開発努力を優先するようになったため、広範なパニックを引き起こした。

予測期間中に北米が市場を独占すると予想される

2022年、航空機射出座席市場では北米が最大のシェアを獲得しました。これは主に米国の強力な艦隊近代化プログラムによるものでした。米国国防総省(DoD)は現在、戦闘機群の更新に取り組んでいます。 F-35統合打撃戦闘機(JSF)計画に基づき、米国国防総省は2,400機以上の新世代F-35航空機を取得する計画を立てています。 F-35Aは、米国で運用されている旧式のF-16およびF-15戦闘機を置き換えると予想されています。 Martin-Bakerは、F-35統合打撃戦闘機プログラムにMk16-US16E射出座席を供給しています。軍はF-35の3つの派生型を大量に調達し続ける一方で、さまざまな部門向けに第5世代戦闘機を補完するためにF-15EXやF/A-18スーパーホーネットのような第4世代戦闘機も調達しています。彼らの軍隊の。同様に、航空機パイロット数の深刻な不足を緩和するために、米国空軍はボーイング・ディフェンスに対し、351機のTX練習機(T-7レッドホーク)を生産する92億米ドル相当の契約を締結し、予測期間中に納入が開始される予定です。この地域の軍隊のこのような調達プログラムは、予測期間中に市場の成長を促進すると予想されます。

航空機射出座席業界の概要

航空機射出座席市場は本質的に高度に統合されており、Martin-Baker Aircraft、Rostec、Collins Aerospace(Raytheon Technologies Corporation)、RAUG Group、Survival Equipment Services Ltd.などの少数の企業が圧倒的なシェアを占めています。市場。主要企業は、広い重量範囲での操作性、重量バランスの向上、安定化、好ましい方向への座席の軌道の高さ、パラシュートの起動の迅速化などの射出座席の機能の改善を可能にする革新的な航空機射出座席技術の研究開発に注力しています。メーカーはまた、パイロットの安全性を高め、それによって生存率を高めるために航空機射出座席の設計において多くの新しい開発を考案しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 航空機タイプ

- 練習機

- 戦闘機

- シートタイプ

- シングルシート

- ツインシート

- 設置

- ラインフィット

- レトロフィット

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Martin-Baker Aircraft Co. Ltd.

- Collins Aerospace(Raytheon Technologies Corporation)

- Rostec

- RUAG Group

- Survival Equipment Services Ltd.

- East/West Industries, Inc.

- The Boeing Company

- RLC Group

- EDM Limited

- Ingersoll Engineers

第7章 市場機会と将来の動向

The Aircraft Ejection Seat Market size is estimated at USD 2.68 billion in 2024, and is expected to reach USD 3.69 billion by 2029, growing at a CAGR of 6.60% during the forecast period (2024-2029).

Due to the impact of the COVID-19 pandemic, the disruption in the supply chain has affected the growth of the companies, as they have had to deal with a significant margin of loss, especially in the case of fixed-price contracts. Since there was no long-term impact on the industry as long as the demand was persistent from the global armed forces, the situation improved for several military aircraft manufacturers worldwide in 2021.

There has been an increase in the number of pilot-related crashes on a global scale, which has sparked the need to focus on augmenting the current safety standards of the pilot and other crew members (such as flight instructors). This has encouraged periodic malfunction tests on several cockpit equipment items, including the ejection seat. Furthermore, the fleet modernization and expansion initiatives undertaken by the global defense forces also drive the demand for ejection seats, as these are mandatory to be installed onboard the combat and training aircraft.

Aircraft Ejection Seat Market Trends

Combat Aircraft Segment is Projected to Dominate the Market During the Forecast Period

The combat aircraft segment is projected to dominate the market during the forecast period. The increasing geopolitical conflicts have driven nations to modernize and upgrade their aircraft fleets to gain a strategic advantage over the adversary forces or be on par with them in terms of defense capabilities. The ongoing Russia-Ukraine conflict has triggered widespread panic as more nations have placed orders for new-generation combat and training aircraft and have even prioritized procurement and R&D efforts for pipeline projects such as those of sixth-generation aircraft such as the Tempest and the F/A-XX.

North America is Expected to Dominate the Market During the Forecast Period

In 2022, North America had the largest share of the market for aircraft ejection seats. This was mostly due to the United States' strong fleet modernization programs. The US Department of Defense (DoD) is working on updating its fleet of fighter planes right now. Under the F-35 Joint Strike Fighter (JSF) Program, the US Department of Defense plans to acquire more than 2,400 new generations of F-35 aircraft. The F-35A is expected to replace the older F-16 and F-15 fighter aircraft that are in service with the US. Martin-Baker supplies the Mk16-US16E ejection seats for the F-35 Joint Strike Fighter program. As the armed forces continue to procure the three variants of F-35s in large numbers, they are also procuring fourth-generation fighters like the F-15EX and F/A-18 Super Hornets to complement the fifth-generation fighter aircraft for various branches of their military. Likewise, in order to mitigate the critical shortage in aircraft pilot numbers, the US Air Force awarded Boeing Defense a contract worth USD 9.2 billion to produce 351 T-X trainer jets (T-7 Red Hawk), with deliveries expected to start during the forecast period. Such procurement programs of the armed forces in the region are anticipated to boost the growth of the market during the forecast period.

Aircraft Ejection Seat Industry Overview

The aircraft ejection seat market is highly consolidated in nature, with only a few players, such as Martin-Baker Aircraft Co. Ltd., Rostec, Collins Aerospace (Raytheon Technologies Corporation), RAUG Group, and Survival Equipment Services Ltd., holding a dominant share of the market. The key players are focused on the R&D of innovative aircraft ejection seat technologies to enable improvements in ejection seat features like operability for a large weight range, better weight balance, stabilization, the trajectory height of the seat in a favorable direction, quickening the parachute activation time after the escape, etc. Manufacturers are also coming up with many new developments in the designs of aircraft ejection seats to boost the safety of pilots, thereby augmenting their survival rates.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Training Aircraft

- 5.1.2 Combat Aircraft

- 5.2 Seat Type

- 5.2.1 Single Seat

- 5.2.2 Twin Seat

- 5.3 Fit

- 5.3.1 Linefit

- 5.3.2 Retrofit

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Egypt

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Martin-Baker Aircraft Co. Ltd.

- 6.1.2 Collins Aerospace (Raytheon Technologies Corporation)

- 6.1.3 Rostec

- 6.1.4 RUAG Group

- 6.1.5 Survival Equipment Services Ltd.

- 6.1.6 East/West Industries, Inc.

- 6.1.7 The Boeing Company

- 6.1.8 RLC Group

- 6.1.9 EDM Limited

- 6.1.10 Ingersoll Engineers