|

市場調査レポート

商品コード

1644288

FaaS(Function As A Service):市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Function As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| FaaS(Function As A Service):市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

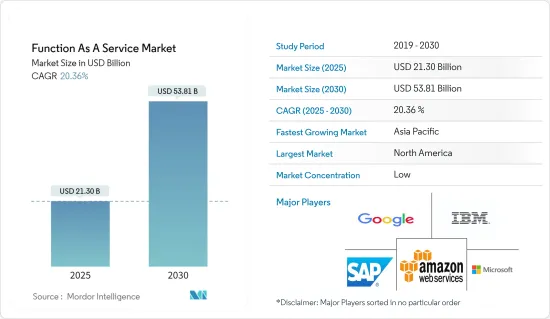

FaaS(Function As A Service)の市場規模は2025年に213億米ドルと推定され、予測期間(2025-2030年)のCAGRは20.36%で、2030年には538億1,000万米ドルに達すると予測されます。

主なハイライト

- FaaS(Function As A Service)はクラウドコンピューティングの一種で、開発者はアプリケーションインフラを管理する必要がなくなるため、より効率的な運用が可能になります。開発者がFaaSプラットフォームを利用する場合、プラットフォームが開発者に代わってアプリケーション・パッケージの構築、実行、管理を行う。

- 開発業務(DevOps)からサーバーレス・コンピューティングへのシフトの進展、俊敏性、拡張性、ホスト型サービスの成熟度が市場開拓の原動力となっています。また、マイクロサービスの最適化や複数プラットフォームの管理に対する企業の傾斜も、市場の成長を後押しするとみられます。

- FaaSの登場により、プログラマブル・クラウドはアプリケーションの展開のために急速に成長しています。オラクルによると、クラウドで共有される機密データは600倍になると推定されています。多くのクラウドプロバイダーが、AWS LambdaやAzure FunctionsなどのFaaSを提供しています。これらのモデルでは、開発者はシンプルなデプロイ、運用の手間の削減、従量課金などのメリットを求めています。

- COVID-19は、さまざまな業種の企業が、COVID-19によって発生したリモートワークの当面のニーズにとどまらず、クラウドコンピューティングの利点と価値を認識し始めたため、企業によるITおよびクラウドリソースへの投資を後押ししました。

- FaaSは、地理的地域ごとに複数のアベイラビリティ・ゾーンにまたがっているため、固有の高可用性を提供し、コストを増加させることなく、いくつもの地域に展開することができます。このようなFaaSにより、市場は予測期間中に成長する可能性が高いです。

FaaS(Function As A Service)市場の動向

ハイブリッドクラウドがセキュリティとプライバシーを重視するエンドユーザーの市場成長を牽引

- ハイブリッドクラウドは、他のクラウドと比較して利用頻度が高いため、市場成長の原動力になると予想されます。ハイブリッドクラウドの導入は、企業が短期的な需要の急増に対応するため、また、より機密性の高いデータやアプリケーションのためにローカル・リソースを解放する必要がある場合に、投資を削減するのに役立ちます。

- コンピューティングや処理に対する需要が変動する中、ハイブリッドクラウドの導入により、企業はオンプレミスのインフラをパブリック・クラウドまで拡張し、サードパーティのデータセンターにデータ全体へのアクセスを与えることなく、オーバーフローを処理することができます。こうした開発により、データの安全性を懸念し、以前はこのソリューションへの移行をためらっていたエンドユーザーの懸念が十分に解消されました。

- クラウドと産業化サービスの成長と従来のデータセンター・アウトソーシング(DCO)の衰退は、ハイブリッドインフラ・サービスへの大転換を示しています。従来のDCO市場が縮小する一方で、コロケーションやホスティングへの支出はインフラ・ユーティリティ・サービスとともに増加しています。このため、クラウド・インフラストラクチャ・アズ・ア・サービス(IaaS)やホスティングへのシフトが進むと予想されます。ハイブリッドクラウドの導入はその利点から、クラウド市場で継続的にシェアを拡大しています。

- さらに、ハイパースケールの動きは昨年末には横ばいとなり、近年急増した需要促進要因が停滞し始めました。この動向は、ここ数年よりも速いとはいえ、今後も続くと思われます。

- さらに、ハイブリッドクラウド市場は、他のクラウド・サービスと比較して、ここ数年で全体的に大きく成長しています。ハイブリッドクラウドは、膨大なデータセットを抱える企業に一定のメリットをもたらします。ハイブリッドクラウドを利用することで、企業はコンピューティング・リソースを拡張することができ、より機密性の高いデータやアプリケーションのためにローカル・リソースを解放する必要がある場合に、短期的な需要の急増に対応するために巨額の資本を投資する必要がなくなります。

北米が最も高い市場シェアを占める

- 北米が最も高い市場シェアを占めています。同地域は、5G、自律走行、IoT、ブロックチェーン、ゲーム、人工知能(AI)などの新技術を採用する先進的なイノベーターでありパイオニアです。この動向は、同地域のFaaS(Function As A Service)採用に拍車をかけると思われます。

- より多くの通信サービスプロバイダー(CSP)がハイパースケールクラウドプロバイダーと連携して5Gサービスを提供することを決定するにつれ、ハイブリッドクラウドとマルチクラウドの未来が急速に進展しています。データ消費の大幅な伸びが5G技術をさらに後押しし、市場成長率に寄与しています。

- ハイパースケールクラウドプロバイダー(HCP)との協業を通じて、通信サービスプロバイダー(CSP)はクラウドインフラを拡大し、ハイブリッドおよびマルチクラウド戦略の導入が進んでいます。

- この20年間、IBMとAT&Tはイノベーションで協業し、企業顧客の変革をサポートしてきました。両社は、デジタル・トランスフォーメーションのためのエッジ・コンピューティングと5Gワイヤレス・ネットワーキングの可能性を実証する意向を発表しました。昨年2月、AT&TとIBMは、IBMのハイブリッドクラウドとAI技術をAT&Tの接続と組み合わせることの威力を、ビジネス・クライアントが体感できる仮想環境の提供を開始しました。

- 米国では多くのデータソースが増加し、新たなビジネス洞察の成長が市場拡大に寄与しています。また、FaaSはコンピューティング性能を飛躍的に高め、業績を直接的に強化する成果を向上させることができます。さらに、ビジネスの俊敏性と柔軟性に対する需要の高まりも、同地域の市場需要を高めています。

FaaS(Function As A Service)産業の概要

FaaS(Function As A Service)市場は、参入企業が多いため競争が激しいです。市場の主要企業には、グーグル、AWS、SAP、IBM、マイクロソフトなどが含まれます。市場のプレーヤーは、新製品の発売、事業拡大、契約、合弁事業、パートナーシップ、買収などを利用して市場シェアを拡大しています。市場の主な発展を以下にいくつか紹介します。

2022年6月、世界最大のITインフラ・サービス・プロバイダーであるKyndryl社は、世界中の企業にマネージド・クラウド・ソリューションを提供することで、顧客がクラウドへの移行を加速できるようオラクルと提携しました。この提携の一環として、KyndrylはOracle Cloud Infrastructure(OCI)の主要なデリバリー・パートナーとなり、オラクルの製品やサービスを利用する顧客との協業やサポートにおける深い経験を拡大します。

さらに、2022年5月には、オープンソース・ソリューションの世界的大手プロバイダーであるレッドハット社とアクセンチュアが、約12年にわたる戦略的パートナーシップをさらに拡大し、世界中の企業向けにオープン・ハイブリッドクラウドのイノベーションを推進しています。両社は新たなソリューションの共同開発に共同で投資し、企業がマルチクラウドやハイブリッドクラウドの世界をよりシームレスにナビゲートし、戦略を明確にし、イノベーションのペースを加速して、より早く価値を実現できるよう支援します。

さらに2022年8月、エッジクラウドのプロバイダーであるリッジは、全く新しい包括的なクラウドサービスであるハイブリッドクラウドを開始しました。リッジによると、その分散型クラウドアーキテクチャにより、企業はオンプレミスかリッジが運営するマネージド拠点かを問わず、すべての拠点でビジネスクリティカルなアプリを統一することができます。同社によれば、ワークロードは異なる環境間で簡単に移行できます。また、単一のポータルで管理できるため、公開会社と非公開会社のすべての拠点で一貫性のあるクラウド・エクスペリエンスを提供できます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- サーバーレスコンピューティングへのシフトの高まり

- インフラの俊敏性とコスト削減への注目の高まり

- 市場抑制要因

- 一部のアプリケーションとクラウド環境の非互換性

- 業界バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場セグメンテーション

- クラウド展開タイプ別

- パブリック

- プライベート

- ハイブリッド

- 組織規模別

- 中小企業

- 大企業

- エンドユーザー別

- BFSI

- IT・通信

- 小売

- ヘルスケア・ライフサイエンス

- その他のエンドユーザー(メディア・エンターテイメント、政府機関、教育機関)

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- 企業プロファイル

- Amazon Web Services Inc.

- IBM Corporation

- Google Inc.

- Microsoft Corporation

- SAP SE

- Infosys Limited

- Dynatrace LLC

- Tibco Software Inc.

- Oracle Corporation

- Rogue Wave Software Inc

- Fiorano Software and Affiliates

第7章 投資分析

第8章 市場機会と今後の動向

The Function As A Service Market size is estimated at USD 21.30 billion in 2025, and is expected to reach USD 53.81 billion by 2030, at a CAGR of 20.36% during the forecast period (2025-2030).

Key Highlights

- Function as a Service (FaaS) is a type of cloud computing that allows developers to operate more efficiently by eliminating the need to manage application infrastructure. When developers use a FaaS platform, the platform builds, runs, and manages application packages on their behalf.

- The growing shift from development operations (DevOps) to serverless computing, agility, scalability, and the maturity of hosted services drive the market's growth. Also, companies' inclination towards optimizing microservices and managing multiple platforms is expected to boost the market's growth.

- With the emergence of FaaS, the programmable cloud has been rapidly growing for the deployment of applications. According to Oracle, it is estimated that there will be 600 times more sensitive data shared in the cloud. Many cloud providers offer FaaS, such as AWS Lambda, Azure Functions, etc. With these models, developers seek advantages in simple deployments, reduced operation efforts, and pay-as-you-go pricing.

- COVID-19 boosted the investments by companies in IT and cloud resources as companies across various industries started realizing the benefits and value of cloud computing, even beyond the immediate need for remote work generated by COVID-19.

- The FaaS offers inherent high availability because it is spread across multiple availability zones per geographic region and can be deployed across any number of areas without incremental costs. With this FaaS, the market will likely grow over the forecast period.

Function as a Service Market Trends

Hybrid Cloud to Drive the Growth of the Market for Security and Privacy Concerned End Users

- The hybrid cloud market is expected to drive market growth as they are highly used compared to other clouds. Hybrid cloud deployment helps companies reduce their investment for handling short-term spikes in demand and when the business needs to free up local resources for more sensitive data or applications.

- With the rise in fluctuating demand for computing and processing, hybrid cloud deployment allows companies to scale their on-premises infrastructure up to the public cloud to handle any overflow without giving third-party data centers access to the entirety of their data. These developments have adequately addressed the concerns of the end-users, who were concerned about their data security and were earlier hesitant to switch to this solution.

- The growth of cloud and industrialized services and the decline of traditional data center outsourcing (DCO) indicate a massive shift towards hybrid infrastructure services. While the conventional DCO market is shrinking, spending on colocation and hosting is increasing along with infrastructure utility services. This is expected to drive the shift toward cloud infrastructure-as-a-service (IaaS) and hosting. Owing to its benefits, hybrid cloud deployment occupies a continuously increasing share of the cloud market.

- Moreover, hyper-scale activity leveled out at the end of the previous year as demand drivers that spiked in recent years began to plateau, including enterprise clients utilizing hybrid IT solutions to accommodate remote working mandates. This trend will likely continue, albeit faster than in the last few years.

- Furthermore, the hybrid cloud market has experienced significant overall growth in the past few years compared to other cloud services. It offers certain benefits to organizations with a vast data set. Using a hybrid cloud allows companies to scale computing resources and helps eliminate the need to invest massive capital in handling short-term spikes in demand when the business needs to free up local resources for more sensitive data or applications.

North America to Hold Highest Market Share

- North America holds the highest market share. The region is among the lead innovators and pioneers in adopting new technologies such as 5G, autonomous driving, IoT, blockchain, gaming, and artificial intelligence (AI), among others. This trend will likely fuel the region's adoption of function as a service.

- As more communication service providers (CSPs) decide to deliver their 5G services in collaboration with hyper-scale cloud providers, a hybrid and multi-cloud future is quickly developing. The significant growth in data consumption is further boosting the 5G technology, thereby contributing to the market growth rate.

- Through collaborations with hyper-scale cloud providers (HCPs), communication service providers (CSPs) are growing their cloud infrastructures and are increasingly implementing a hybrid and multi-cloud strategy.

- Over the last two decades, IBM and AT&T have collaborated on innovations and supported enterprise clients' transformation. The two organizations announced intentions to demonstrate the possibilities of edge computing and 5G wireless networking for digital transformation. In February last year, AT&T and IBM launched virtual environments that allow business clients to physically experience the power of combining IBM hybrid cloud and AI technologies with AT&T connection.

- The growth of new business insights contributes to expanding the market in the United States as many data sources increase. FaaS can also dramatically boost computing performance and improve results that directly strengthen business performance. Furthermore, the rise in demand for business agility and flexibility is also increasing the market demand in the region.

Function as a Service Industry Overview

The function as a service Market is highly competitive due to the many players in the market. Key players in the market include Google, AWS, SAP, IBM, and Microsoft, among others. Players in the market use new product launches, expansions, agreements, joint ventures, partnerships, acquisitions, etc., to increase their market share. Some of the key developments in the market are mentioned below.

In June 2022, Kyndryl, the world's largest IT infrastructure services provider, partnered with Oracle to help customers accelerate their journey to the cloud by delivering managed cloud solutions to enterprises worldwide. As part of the alliance, Kyndryl will become a key delivery partner for Oracle Cloud Infrastructure (OCI), expanding upon its deep experience of working with and supporting customers using Oracle products and services.

Moreover, in May 2022, Red Hat Inc., the world's leading provider of open source solutions, and Accenture expanded their nearly 12-year strategic partnership further to power open hybrid cloud innovation for enterprises worldwide. The companies are jointly investing in the co-development of new solutions to help organizations more seamlessly navigate a multi- and hybrid cloud world, define their strategy, and accelerate their pace of innovation to get to value faster.

Further, in August 2022, Ridge, a provider of edge clouds, launched a hybrid cloud, a brand-new all-inclusive cloud service. According to Ridge, its distributed cloud architecture allows businesses to unify business-critical apps across all their locations, whether on-premises or managed locations run by Ridge. According to the company, workloads can be transferred easily between different environments. Businesses can also manage them through a single portal, providing companies with a cohesive cloud experience across all public and private locations..

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing shift towards serverless computing

- 4.2.2 Increasing focus towards agility of infrastructure and cost reduction

- 4.3 Market Restraints

- 4.3.1 Incompatibility of some applications with cloud environment

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment on the Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Type of Cloud Deployment

- 5.1.1 Public

- 5.1.2 Private

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By End-User

- 5.3.1 BFSI

- 5.3.2 IT and Telecommunication

- 5.3.3 Retail

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Other End-Users (Media and Entertainment, Government, Educational Institutions))

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amazon Web Services Inc.

- 6.1.2 IBM Corporation

- 6.1.3 Google Inc.

- 6.1.4 Microsoft Corporation

- 6.1.5 SAP SE

- 6.1.6 Infosys Limited

- 6.1.7 Dynatrace LLC

- 6.1.8 Tibco Software Inc.

- 6.1.9 Oracle Corporation

- 6.1.10 Rogue Wave Software Inc

- 6.1.11 Fiorano Software and Affiliates