|

市場調査レポート

商品コード

1643229

IoTデバイス管理-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)IoT Device Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| IoTデバイス管理-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

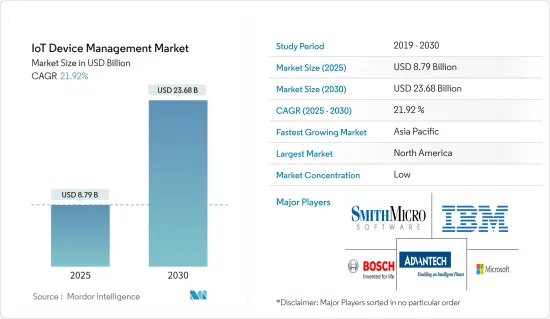

IoTデバイス管理市場規模は2025年に87億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは21.92%で、2030年には236億8,000万米ドルに達すると予測されます。

IoTデバイス管理市場には、接続デバイスのプロビジョニング、管理、モニタリング、トラブル再現と是正措置に必要な診断が含まれます。

同市場は主に、ネットワークセキュリティに対する懸念の高まり、IoTネットワークとシステムの全体的な成長、IoTデバイスの健全性(オン/オフ状態、電力、接続性など)をモニタリングするニーズの高まり、5Gネットワークの展開とマルチアクセス・エッジコンピューティング(MEC)と組み合わせた大規模IoTへの対応といった特定の要因によって牽引されています。さらに、IoTデバイス管理システムはデータの収集と分析も可能にし、これも市場成長を促進する要因のひとつと予想されます。

世界のIoT需要動向は、今後数年間で消費者需要から産業セグメントへとシフトし、さまざまなインダストリー4.0用途によって大量の需要が牽引されると予想されます。製造業、エネルギー、ビジネスモビリティ、医療、サプライチェーンが需要の大きなシェアを占めると予想されます。

スマートフォンやモバイルデバイスの普及が拡大し、インターネットの普及が進んでいるため、IoTデバイス管理の進化は近年大きな成長を遂げています。

しかし、プライバシーの問題、リアルタイムの複雑さ、動的な環境、互換性と接続性の欠如、相互運用性のための統一されたIoT標準の不在などに関する機密情報の露出は、市場にとって重要な課題となっています。世界のサプライチェーンは、大きな混乱にさらされています。

最近のCOVID-19の発生により、電子機器の世界のサプライチェーンと需要が混乱し、そのためにIoTデバイス管理市場のハードウェア導入は深刻な影響を受けると予想されます。中国などの生産停止により、電子機器産業は電子機器の供給不足を観察しています。

IoTデバイス管理市場の動向

小売業がIoTデバイス管理市場で大きなシェアを占める

小売業は、スマートデバイスとIoTの助けを借りて顧客体験を向上させ、コンバージョンを増加させることができ、日々の業務に大きな影響を与えます。小売業でIoTを利用する利点には、エネルギー管理、店内ナビゲーション、盗難防止、消費者エンゲージメントなどがあります。

小売業におけるIoTとスマートデバイスによって、企業は顧客からのフィードバックを収集し、顧客体験を向上させることができます。エネルギー管理、店舗内ナビゲーション、盗難防止、消費者エンゲージメントは、小売業に役立つIoTデバイスのメリットです。

店舗管理者は、これらの洗練された電力管理デバイスを使用することで、冷蔵庫のコントローラとインターフェースを取ったり、センサを使用して優先順位の高い情報を取得したりすることができます。IoTデバイス管理市場の開拓が産業を後押ししています。

組み込みセンサにより、多くのIoTベースのプラットフォームは、温度、ガス漏れ、電気故障、エネルギー使用量、暖房などについて、記録、モニタリング、アラームを鳴らしたり、店内スタッフに通知したりすることができます。店舗のオーナーは、これらのインテリジェントなエネルギー管理ツールを使って冷蔵庫のコントローラとインターフェースすることができ、センサの助けを借りて優先順位の高い情報を取得することもできます。

増加する攻撃とその悪意のある性質は、市場のエンドユーザーがこれらのリスクを軽減するためにこれらのソリューションを採用することを後押ししています。このため、進化する攻撃の性質に起因する需要の増加が生じています。

北米が市場で優位な地位を占める

北米はIoT導入の主要地域の一つです。最先端技術の利用拡大、サイバー攻撃の増加、同地域における接続デバイス数の増加が、同地域におけるIoTデバイス管理市場の成長を促進する主要要因となっています。デジタル化の進展とIoTセキュリティへの支出は、同地域の市場に影響を与えているその他の変数です。

また、同地域では製造業でのIoT利用が拡大しているため、IoTセキュリティソリューションの導入が促進され、市場の拡大に好影響を与えています。

消費者や電力会社は、IoTデバイスの普及と税制優遇措置や住宅保険の割引を組み合わせることで、このような変化する市場で競合を維持するために、自社のサービスをスマート化し、新世代の住宅建設業者や所有者に適したものにするための行動を促しています。

また、新無線(NR)を用いた新たな5G標準は、産業用ユースケースとして、Vehicle-to-Everythingや超高信頼性低遅延通信などの機能を対象としています。さらに、PROFINETやModbusなど、IECによって標準化された産業用通信バスにより、市場は信頼性と安全性の高い産業用採用に向かっています。

IoTデバイス管理産業概要

IoTデバイス管理市場は競争が激しいです。産業全体でIoTが広く利用されるようになったことで、この産業が提供する機会の数が急増しています。現在のところ、市場では少数の重要な参入企業によって支配されているが、産業全体にわたるIoT用途の深度が増すにつれて、市場は複数の参入企業の参入を確認すると予想されます。ほとんどの企業は、市場シェアを拡大するために様々なマーケティング戦術を駆使しています。世界のIoTデバイス管理サービスで理想的なポジションを確保するため、市場のベンダーは価格、品質、ブランド、製品やサービスの差別化で競争しています。

2023年1月、Tech MahindraとMicrosoftは、通信事業者向けに世界のクラウドパワーによる5Gコアネットワークの近代化を実現するための戦略的協業を発表しました。5Gコアネットワークの変革は、通信事業者が5Gコアの使用事例を開発し、顧客の増大する技術(AR(拡張現実)、VR(仮想現実)、IoT(モノのインターネット)、エッジコンピューティング)要件を満たすのに役立ちます。これにより、コスト削減と市場投入までの時間短縮を実現し、事業運営の近代化、最適化、安全性を確保し、グリーンネットワークを開発することが可能になります。

2022年6月、AdvantechとActilityは、先進的で堅牢なアドバンテックIPCと組み込みのアクティリティソフトウェアを組み合わせ、ゲートウェイとの互換性を拡大した高信頼性でセキュアなキャリアグレードのサービスを提供することで、エンタープライズIoT LoRaWANネットワークを顧客構内に展開するための「エッジソリューション対応包装」の提供を開始するための協業を発表しました、この統合ソリューションは、急成長する産業用オートメーション市場のニーズを満たすことを目的としており、企業がIoT使用事例を簡素化、迅速かつ効率的な方法で展開できるようにすることで、インダストリー4.0の実現を加速します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- COVID-19の産業への影響評価

- 産業のバリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- スマートコネクテッドデバイスの普及拡大

- 統合デバイス管理へのニーズの高まり

- 市場抑制要因

- 相互運用性のための統一されたIoT標準が存在しないこと

第6章 市場セグメンテーション

- コンポーネント別

- ソリューション

- セキュリティソリューション

- データ管理

- 遠隔モニタリング

- その他のソリューション(リアルタイムストリーミング分析、ネットワーク帯域幅管理)

- サービス

- プロフェッショナルサービス

- マネージドサービス

- ソリューション

- 組織規模別

- 中小企業

- 大企業

- 産業別

- 小売

- 医療

- 運輸・物流

- 製造業

- その他産業別

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Microsoft Corporation

- International Business Management(IBM)Corporation

- Smith Micro Software, Inc.

- Advantech Co., Ltd.

- Bosch Software Innovations GmbH

- Amplia Soluciones S.L.

- Aeris Communication, Inc.

- PTC Incorporation

- Oracle Corporation

- Smith Micro Software, Inc.

- Telit Communications PLC

- Cumulocity GmbH

- Enhanced Telecommunications Inc.

- Zentri Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The IoT Device Management Market size is estimated at USD 8.79 billion in 2025, and is expected to reach USD 23.68 billion by 2030, at a CAGR of 21.92% during the forecast period (2025-2030).

The IoT device management market encompasses connected device provisioning, administration, monitoring, and diagnostics necessary for trouble replication and corrective measures.

The market is primarily driven by certain factors, such as growing concerns over network security, the overall growth of IoT networks and systems, the growing need to monitor the health (on/off condition, power, connectivity, etc.) of IoT devices, and the deployment of 5G networks and its support for massive IoT, coupled with Multi-access Edge Computing (MEC). Besides, IoT device management systems also enable the collection and analysis of data, which is another factor anticipated to fuel market growth.

The global IoT demand trend is expected to shift towards industrial space from consumer demand over the coming years, with sheer volumes of demand driven by various Industry 4.0 applications. A significant share of the demand is expected by manufacturing industries, energy, business mobility, healthcare, and supply chain.

Owing to the expanding adoption of smartphones and mobile devices, coupled with the increasing penetration of the internet, the evolution of IoT device management has witnessed immense growth in recent years.

However, exposure of confidential information concerning privacy concerns, real-time complexity, dynamic environment, and lack of compatibility and connectivity, along with the absence of uniform IoT standards for interoperability, is a crucial challenge for the market. The global supply chain is undergoing a level of disruption.

Due to the recent outbreak of COVID-19, the global supply chain and demand for electronics were disrupted, owing to which the IoT device management market hardware adoption was expected to be severely influenced; due to the production shutdown in countries such as China, the electronics industry was observing a shortage of supply of electronics.

IoT Device Management Market Trends

Retail to Have a Major Share in the IoT Device Management Market

Retailers may enhance the customer experience and increase conversions with the help of smart devices and IoT, significantly impacting day-to-day operations. A few benefits of using IoT in the retail sector include energy management, in-store navigation, theft prevention, and consumer engagement.

IoT and smart devices in retail enable businesses to gather customer feedback and improve the customer experience. Energy management, in-store navigation, theft prevention, and consumer engagement are benefits of IoT devices that help the retail sector.

Store managers can interface with refrigerator controllers and obtain priority information using sensors with these sophisticated power management devices. IoT device management market developments are boosting the industry.

With embedded sensors, many IoT-based platforms may record, monitor, and beep alarms or notify the in-store staff about temperature, gas leakage, electricity breakdowns, energy usage, heating, etc. Store owners may interface with refrigerator controllers using these intelligent energy management tools, and they can also retrieve priority information with the aid of sensors.

The increased attacks and their nature of becoming malevolent have pushed for the market end-users to adopt these solutions to mitigate these risks. This has created an increasing demand owing to the evolving nature of attacks.

North America to Hold a Dominant Position in the Market

One of the key regions in North America for IoT implementation. The growing use of cutting-edge technologies, an increase in cyberattacks, and an increase in the number of connected devices in the area are the main factors propelling the growth of the IoT Device Management market in the region. The rise of digitalization and spending on IoT security are other variables that are having an impact on the market in the area.

Also, the region's expanding IoT use in the manufacturing sector encourages the uptake of IoT security solutions, which favorably impacts the market's expansion.

Consumers and utility companies have been encouraged to take action to make their services smart and suitable for the new generation of home builders and owners to remain competitive in such a changing market by the popularity of IoT devices, combined with tax incentives and discounts on home insurance.

Also, the emerging 5G standards with New Radio (NR) target capabilities such as vehicle-to-everything and ultra-reliable low-latency communications as industrial use cases. And, with industrial communication buses standardized by IEC, such as PROFINET and Modbus, the market is headed towards reliable and securer industrial adoption.

IoT Device Management Industry Overview

The IoT Device Management Market is competitive. The widespread use of IoT across industry verticals has resulted in a boom in the number of opportunities that the industry offers. Though dominated by a few significant players in the market as of now, the market is expected to witness the entry of several players as the depth of IoT applications across industries increases. Most businesses use various marketing tactics to increase their market share. To ensure an ideal place in the global IoT Device management services, the vendors on the market are competing on price, quality, brand, and product and service differentiation.

In January 2023, Tech Mahindra and Microsoft announced a strategic collaboration to enable global cloud-powered 5G core network modernization for telecom operators. The 5G core network transformation will help telecom operators to develop 5G core use cases and meet their customers' growing technological (Augmented Reality (AR), Virtual Reality (VR), IoT (Internet of Things), and edge computing) requirements. It will enable them to modernize, optimize, and secure business operations and develop green networks with reduced costs and a faster time to market.

In June 2022, Advantech Co., Ltd., and Actility announced the collaboration for the Launch an Edge Solution-Ready Package to Deploy Enterprise IoT LoRaWAN Networks, on customer premises, by combining advanced and ruggedized Advantech IPC with embedded Actility software, bringing a highly reliable and secure career-grade service with extended compatibility with gateways, cloud platforms, and devices, this integrated solution aims at meeting the needs of the fast-growing industrial automation market, by allowing businesses to deploy their IoT use cases in a simplified, quicker et more efficient way, thus accelerating the realization of Industry 4.0

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Assessment of Impact of COVID-19 on the Industry

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Smart Connected Devices

- 5.1.2 Accelerating Need for Converged Device Management

- 5.2 Market Restraints

- 5.2.1 Unavailability of Uniform IoT Standards for Interoperability

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Solutions

- 6.1.1.1 Security Solution

- 6.1.1.2 Data Management

- 6.1.1.3 Remote Monitoring

- 6.1.1.4 Other Solutions (Real-Time Streaming Analytics, Network Bandwidth Management)

- 6.1.2 Services

- 6.1.2.1 Professional Services

- 6.1.2.2 Managed Services

- 6.1.1 Solutions

- 6.2 By Organization Size

- 6.2.1 Small and Medium-Sized Enterprises

- 6.2.2 Large Enterprises

- 6.3 By End-user Vertical

- 6.3.1 Retail

- 6.3.2 Healthcare

- 6.3.3 Transportation & Logistics

- 6.3.4 Manufacturing

- 6.3.5 Other End-user Vertical

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Microsoft Corporation

- 7.1.2 International Business Management (IBM) Corporation

- 7.1.3 Smith Micro Software, Inc.

- 7.1.4 Advantech Co., Ltd.

- 7.1.5 Bosch Software Innovations GmbH

- 7.1.6 Amplia Soluciones S.L.

- 7.1.7 Aeris Communication, Inc.

- 7.1.8 PTC Incorporation

- 7.1.9 Oracle Corporation

- 7.1.10 Smith Micro Software, Inc.

- 7.1.11 Telit Communications PLC

- 7.1.12 Cumulocity GmbH

- 7.1.13 Enhanced Telecommunications Inc.

- 7.1.14 Zentri Inc.