|

市場調査レポート

商品コード

1690101

医薬品中間体:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Pharmaceutical Intermediates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医薬品中間体:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

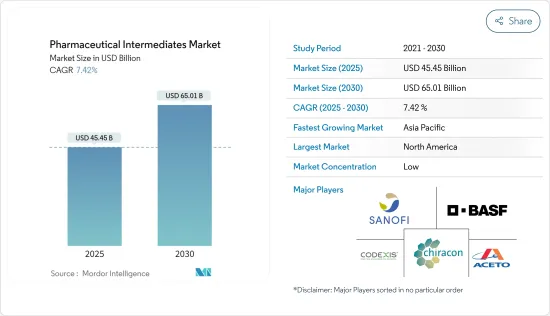

医薬品中間体の市場規模は2025年に454億5,000万米ドルと予測され、予測期間(2025-2030年)のCAGRは7.42%で、2030年には650億1,000万米ドルに達すると予測されます。

COVID-19パンデミックは、調査した市場に大きな影響を与えました。American Chemical Society Pharmacology and Translational Science, 2020に掲載された研究によると、COVID-19に対する新たな潜在的治療薬は、仮想スクリーニングと実験スクリーニングを組み合わせた戦略を用いて発見されました。さらに、ヒドロキシクロロキン(HCQ)を参照薬として、すでに使用されている薬剤の中から選択し、すでに使用されている約4,000種類の薬剤のライブラリーと照らし合わせて構造的類似性を調べた。この研究では、COVID-19治療におけるアジュバントとしてレムデシビルとファビピラビル療法が有望であること、SARS-CoV-2感染の初期段階に対する臨床試験の候補としてズクロペンチキソール、ネビボロール、アモジアキンが有望であることが示唆されました。このように、医薬品中間体市場はコビドパンデミックの間に大きな成長を示し、パンデミック後も医薬品中間体の需要は世界市場で高いことが確認されています。

市場成長を牽引する具体的な要因としては、慢性疾患の蔓延の増加、製薬業界における研究開発イニシアティブと活動の拡大などが挙げられます。これらの医薬品中間体は、がんの検出や様々な慢性疾患の治療に使用されることから、慢性疾患の有病率の増加は、調査対象領域における市場拡大を促進すると予測されます。例えば、2021年4月に発表されたWHOの非伝染性疾患に関する主要事実によると、慢性疾患による年間死亡者数は約4,100万人で、全世界の死亡者数の71%を占めています。こうした疾患による致死率の高さが早期介入への需要を高め、市場の拡大を後押ししています。

市場は、肺がん、慢性閉塞性肺疾患などの呼吸器疾患の有病率の上昇により発展すると予想されます。例えば、WHOは2022年1月の報告書で、慢性閉塞性肺疾患(COPD)は世界的に罹患率と死亡率の3番目に多い原因であると述べています。COPDの世界の有病率の上昇には、低・中所得国(LMIC)が大きく寄与しています。慢性閉塞性肺疾患の有病率の増加により、効果的な治療が必要となり、市場の成長が期待されています。

より優れた薬剤候補同定のために、ハイスループット、バイオインフォマティクス、コンビナトリアルケミストリーなどの先端技術の利用が急増しています。がん、糖尿病、心血管疾患、慢性腎臓病など、さまざまな疾患の治療、予防、治癒を目的とした新薬の発見と開発は、世界の疾患罹患率の大幅な上昇によって加速しています。2022年3月に発表されたCMSのデータによると、米国の医療費は9.7%増加し、2021年には4兆3,000億米ドルに達し、2020年の4.2%増を大幅に上回る。さらに、研究開発への投資拡大も市場拡大の大きな要因となっています。例えば、JSRライフサイエンスは2021年3月、中小・発展途上のバイオテクノロジーに焦点を当てたコーポレート・ベンチャー・ファンドを導入し、ライフサイエンス・サービスの範囲に顧客を引き付けています。したがって、製薬業界における研究開発活動の高まりにより、医薬中間体の使用量も力強い成長が見込まれています。

しかし、特定の医薬品中間体物質に関する厳しい規制問題が市場成長の妨げになると予想されます。

医薬品中間体市場の動向

心血管治療薬が世界の医薬品中間体市場で大きなシェアを占める

世界のヘルスケアシステムにおける心臓病の負担は増加傾向にあります。医薬品中間体市場の拡大を促す主な要因の一つは、心不全や冠動脈疾患などの慢性心血管系疾患の発生率の増加です。2021年7月にCureus Journal of Medical Scienceに掲載された報告によると、虚血性心疾患(IHD)は世界の主要死因です。同報告書によると、世界で約1億2,600万人(10万人当たり1,655人)、つまり世界人口のおよそ1.72%が虚血性心疾患に罹患しています。2030年までには、世界で人口10万人あたり1,845人以上の虚血性心疾患患者が発生すると予測されています。

さらに、心臓病に関連する危険因子はいくつかの国で増加傾向にあり、これが有病率を押し上げています。例えば、World Population Reviewのデータによると、2022年現在、フランスでは男性の約11.10%、女性の約3.10%がアルコール依存症です。アルコール依存症は心臓病の可能性を高めるため、市場の成長に大きな影響を与えます。同様に、2021年7月に発表された英国心臓財団(British Heart Foundation)による英国ファクトシート(UK Factsheet)では、英国では760万人が心臓・循環障害に罹患していると推定されています。さらに、同じ情報源によると、英国では心臓と循環の病気が年間160,000人以上の死因となっており、これは同国の全死亡者の25%に相当します。このような心血管疾患の高い有病率は、心血管治療薬に対する大きな需要を生み出し、ひいては様々な医薬品中間体に対するニーズの成長を促進すると予想されています。

したがって、前述の要因から、医薬品中間体市場の当該セグメントは予測期間中に安定した成長を遂げると予想されます。

北米が世界の医薬品中間体市場を独占

北米が医薬品中間体市場を独占しているのは、主に米国とカナダに高度な研究開発施設があるためです。加えて、様々な慢性疾患の有病率が上昇していることも、この地域の市場成長に拍車をかけています。

米国におけるヘルスケアに対する政府の支援の拡大は、同国での市場拡大に寄与している要素のひとつです。例えば、米国議会予算局の2021年の調査によると、国立衛生研究所(NIH)は過去数十年の間に7,000億米ドル以上の公的資金を受けています。2020年には食品医薬品局(FDA)から6件の助成金が交付され、新たな臨床試験に資金を提供し、一般的でない疾患の治療用医薬品の創製を進めています。その結果、創薬プロセスで広く使用される医薬品中間体のニーズが高まると思われます。「clinicaltrials.gov」によると、2022年11月現在、米国では443,207件の臨床試験が登録されています。同様に「ClinicalTrial.gov」によると、カナダの製薬会社や研究機関は2022年時点で強力な研究開発パイプラインを有しています。その時点でパイプラインにある様々な評価段階にある新規試験5,659件のうち、1,397件(24%)が食品医薬品局(FDA)または欧州医薬品評価機構(EMA)の承認を受けた第III相臨床試験であり、幅広い治療領域をカバーしています。

感染症が蔓延するにつれ、その診断と治療にますます注目が集まっています。米国疾病予防管理センター(CDC)の推計によると、2020年に米国で発見された結核患者は約7,174人で、人口10万人当たり2.2人の割合となります。このように、結核患者の高い有病率は治療需要を高め、ひいては医薬品中間体市場を牽引します。CDCは2022年2月の記事で、米国では毎年サルモネラ菌が約135万人の感染、26,500人の入院、420人の死亡の原因となっていると報告しています。国のヘルスケアシステムは、毎年報告される多数の感染症によって負担を強いられています。その結果、これらの疾患に対する治療需要の異常な高まりにより、調査対象市場は成長を遂げる可能性があります。このように、上記の要因は市場の成長を高めると予想されます。

医薬品中間体産業の概要

世界の医薬品中間体市場は競争が激しく、少数の大手企業で構成されています。Aceto Corporation、BASF SE、Chiracon GmbH、Yin-sheng Bio-tech、Dishman Group、Green Vision Life Sciences、Codexis, Inc.、Sanofi SAIS、Vertellus Holdings LLC.などの企業がこの市場で大きなシェアを占めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の増加

- 製薬業界における研究開発への取り組みと活動の拡大

- 市場抑制要因

- 特定の医薬品中間物質に関する厳しい規制問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- 化学中間体

- 原薬中間体

- その他

- 用途別

- 鎮痛剤

- 抗感染症薬

- 循環器薬

- 経口糖尿病薬

- 抗菌薬

- その他

- エンドユーザー別

- バイオテクノロジーおよび製薬会社

- 研究機関

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- A.R. Life Science

- Aceto Corporation

- BASF SE

- Chiracon GmbH

- Codexis, Inc.

- Dishman Group

- Green Vision Life Sciences

- Lianhetech

- Midas Pharma GmbH

- Sanofi SAIS

- Vertellus Holdings LLC

- Yin-sheng Bio-tech Co., Ltd.

第7章 市場機会と今後の動向

The Pharmaceutical Intermediates Market size is estimated at USD 45.45 billion in 2025, and is expected to reach USD 65.01 billion by 2030, at a CAGR of 7.42% during the forecast period (2025-2030).

COVID-19 pandemic had a significant impact on the market studied. According to a study that was published in the American Chemical Society Pharmacology and Translational Science, 2020, new potential therapeutics for COVID-19 were discovered using a combined virtual and experimental screening strategy. Furthermore, they choose among the medications that were already in use and were examined to check for structural similarity against a library of almost 4,000 medications that were already in use, with hydroxychloroquine (HCQ) serving as a reference medication. The study suggested remdesivir and favipiravir therapies as prospective adjuvants in COVID-19 treatment and zuclopenthixol, nebivolol, and amodiaquine as potential candidates for clinical trials against the early phase of the SARS-CoV-2 infection. Thus, the pharmaceutical intermediates market witnessed significant growth during the covid pandemic and it is observed that even after the pandemic, the demand for pharmaceutical intermediates is high in the global market.

Specific factors that are driving the market growth include the increasing prevalence of chronic diseases and growing R&D initiatives and activities in the pharmaceutical industry. Given that these pharma intermediates are used in the treatment of cancer detection and a variety of chronic diseases, the rise in the prevalence of chronic diseases is projected to propel market expansion in the area under study. For instance, chronic diseases account for around 41 million annual fatalities, or 71% of all fatalities worldwide, according to the WHO's key facts on non-communicable diseases published in April 2021. The high fatality rate from these diseases increases the demand for early intervention, which in turn propels the market's expansion.

The market is expected to develop due to the rising prevalence of respiratory ailments such as lung cancer, chronic obstructive pulmonary diseases, and others. For instance, the WHO stated in its January 2022 report that Chronic Obstructive Pulmonary Disease (COPD) is the 3rd most common cause of morbidity and mortality globally. Low- and middle-income nations (LMIC) countries contribute largely to the global rise in prevalence of COPD. The necessity for effective treatment of the disease is brought on by the increasing prevalence of chronic obstructive pulmonary disease which is expected to increase the market growth.

There has been an upsurge in the usage of advanced technologies, such as high throughput, bioinformatics, and combinatorial chemistry for better drug candidate identification. The discovery and development of novel drugs to treat, prevent, or cure several diseases, including cancer, diabetes, cardiovascular disorders, and chronic kidney disease, has been accelerated by the significant rise in disease incidence rates around the world. The United States health care spending climbed 9.7% to reach USD 4.3 trillion in 2021, a substantially greater rate than the 4.2% increase recorded in 2020, according to the CMS data published in March 2022. Additionally, increased investments in R&D are a significant driver of market expansion. For instance, JSR life sciences introduced a corporate venture fund in March 2021 with a focus on small and developing biotech, attracting clients to its range of life sciences services. Hence, owing to the rising R&D activities in the pharmaceutical industry, the usage of pharmaceutical intermediates is expected to observe strong growth as well.

However, stringent regulatory issues regarding certain pharmaceutical intermediate substances are expected to hinder market growth.

Pharmaceutical Intermediates Market Trends

Cardiovascular Drugs Hold Significant Share in the Global Pharmaceutical Intermediates Market

The burden of heart disease on the global healthcare system is on the rise. One of the main elements driving the market expansion of pharmaceutical intermediates is the increase in the incidence of chronic cardiovascular disorders such as heart failure and coronary artery diseases. Ischemic heart disease (IHD) is a primary cause of death worldwide, according to a report published in the Cureus Journal of Medical Science in July 2021. The same report stated that around 126 million people worldwide (1,655 per 100,000), or roughly 1.72% of the world's population are affected by ischemic heart disease. By 2030, it is anticipated that there would be more than 1,845 cases of ischemic heart disease per 100,000 people worldwide.

Furthermore, risk factors associated with heart disease are on the rise across several countries which is boosting the prevalence. For instance, as of the year 2022, around 11.10% of men and 3.10% of women in France are alcoholics, as per the data from World Population Review. As alcoholism increases the chances of heart disease, it has a significant impact on market growth. Similarly, the UK Factsheet by the British Heart Foundation, released in July 2021, estimated that 7.6 million people in the United Kingdom were affected by heart and circulation disorders. Additionally, according to the same source, heart and circulation illnesses are responsible for more than 1,60,000 deaths annually in the United Kingdom, or 25% of all fatalities in the country. This high prevalence of cardiovascular diseases is generating a huge demand for cardiovascular drugs, which, in turn, is expected to propel the growth in the need for various pharmaceutical intermediates.

Hence, owing to the aforementioned factors, the concerned segment of the pharmaceutical intermediates market is expected to observe steady growth over the forecast period.

North America Dominates the Global Pharmaceutical Intermediates Market

North America dominates the Pharmaceutical Intermediates products market primarily due to the advanced research and development facilities mainly across the United States and Canada. In addition, the rising prevalence of various chronic conditions is also fueling market growth across the region.

Growing government support for healthcare in the United States is one element contributing to the market's expansion in that country. For instance, the National Institutes of Health (NIH) received more than USD 700 billion in public funding over the past few decades, according to a 2021 study from the Congressional Budget Office. Six grants were given out by the Food and Drug Administration (FDA) in 2020 to fund new clinical trials and advance the creation of pharmaceuticals for the treatment of uncommon diseases. The need for pharmaceutical intermediates, which are widely used in the drug discovery process, will increase as a result. According to "clinicaltrials.gov," there were 443,207 registered clinical studies in the United States as of November 2022. Similarly, according to ClinicalTrial.gov, Canadian pharmaceutical companies and research institutions have strong R&D pipelines as of the year 2022. Of the 5,659 new studies in the pipeline at that time that were in various stages of evaluation, 1,397 (24%) were in Phase III clinical trials that had received the Food and Drug Administration (FDA) or European Medicines Evaluation Agency (EMA) approval, covering a wide range of therapeutic areas.

As infectious diseases become more widespread, attention is being paid more and more to their diagnosis and treatment. The Centers for Disease Control and Prevention (CDC) estimated that in 2020, there were approximately 7,174 tuberculosis cases discovered in the United States, translating to a rate of 2.2 per 100,000 people. Thus, a high prevalence of tuberculosis patients drives up the demand for therapy, which in turn drives the market for pharmaceutical intermediates. The CDC reported in a February 2022 article that each year in the United States, Salmonella bacteria causes around 1.35 million infections, 26,500 hospitalizations, and 420 fatalities. The nation's healthcare system is burdened by the large number of infectious infections that are reported each year. As a result, the market under study may experience growth due to the extraordinary rise in demand for treatments for these diseases. Thus, the abovementioned factors are expected to increase market growth.

Pharmaceutical Intermediates Industry Overview

The global pharmaceutical intermediates market is competitive and consists of a few major players. Companies like Aceto Corporation, BASF SE, Chiracon GmbH, Yin-sheng Bio-tech Co., Ltd., Dishman Group, Green Vision Life Sciences, Codexis, Inc., Sanofi SAIS, Vertellus Holdings LLC., among others, hold the substantial market share in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases

- 4.2.2 Growing R&D Initiatives and Activities in the Pharmaceutical Industry

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Issues Regarding Certain Pharmaceutical Intermediate Substances

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Chemical Intermediate

- 5.1.2 Bulk Drug Intermediate

- 5.1.3 Others

- 5.2 By Application

- 5.2.1 Analgesics

- 5.2.2 Anti-Infective Drugs

- 5.2.3 Cardiovascular Drugs

- 5.2.4 Oral Antidiabetic Drugs

- 5.2.5 Antimicrobial Drugs

- 5.2.6 Others

- 5.3 By End-User

- 5.3.1 Biotech and Pharma Companies

- 5.3.2 Research Institutions

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 A.R. Life Science

- 6.1.2 Aceto Corporation

- 6.1.3 BASF SE

- 6.1.4 Chiracon GmbH

- 6.1.5 Codexis, Inc.

- 6.1.6 Dishman Group

- 6.1.7 Green Vision Life Sciences

- 6.1.8 Lianhetech

- 6.1.9 Midas Pharma GmbH

- 6.1.10 Sanofi SAIS

- 6.1.11 Vertellus Holdings LLC

- 6.1.12 Yin-sheng Bio-tech Co., Ltd.