|

市場調査レポート

商品コード

1406110

兵器運搬・発射システム:市場シェア分析、産業動向・統計、成長予測、2024年~2029年Weapons Carriage And Release Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 兵器運搬・発射システム:市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

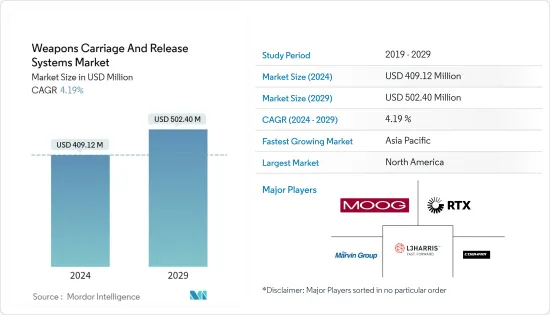

兵器運搬・発射システム市場規模は2024年に4億912万米ドルと推定され、2029年には5億240万米ドルに達し、予測期間(2024-2029年)のCAGRは4.19%で成長すると予測されます。

新しい技術とプラットフォームの出現は、米国、ロシア、中国といった国々の戦争戦略を一変させました。これらの諸国は、敵の拠点に深刻な影響を与え、武力衝突の際に戦術的優位を獲得するのに役立つ、洗練された強力な兵器の開発に力を注いでいます。兵器運搬台車は特定の武器用に再設計されつつありますが、発射システムは、その視覚的優位性と特定の場所への先制攻撃を実行する能力により、現在の戦争シナリオで広く使用されています。

しかし、ペイロード容量、空力特性、射程距離を犠牲にすることなく、高度な機能を製品ポートフォリオに組み込むという、システム・インテグレーターが直面する設計上の課題によって、市場は抑止される可能性があります。設計者はまた、完全に運用可能な兵器運搬・発射システムを開発するために、洗練された統合機能の利用可能性と、複数の武器メーカーのさまざまなタイプの高度な武器システムとの相互互換性を確保する必要があり、そのため、システム全体の設計に複雑な見通しをもたらします。

さらに、兵器運搬・発射システム市場の成長は、国境監視やテロリズムに対する市民の安全保障に関する政府規制の高まりによっても後押しされています。

兵器運搬・発射システム市場の動向

航空機プラットフォームが市場を独占

2023年には、いくつかの航空機の近代化計画が世界的に進行中です。しかし、航空機の導入率が高く、その固有の洗練された飛行特性によって正当化される比較的高い価格設定のため、航空機フリートの拡張と近代化プログラムが、このような実施されたイニシアチブの大半のシェアに寄与しています。兵器運搬・発射システムの需要は、新しい戦闘空中資産の調達率と、その殺傷力を高めるための既存資産の近代化率に正比例します。例えば、インド国防省は、インド空軍(IAF)の在庫枯渇に対処するため、航空機の取得を計画しています。インド空軍は2038年までに、LCAテジャス戦闘機40機、LCAテジャスMark-1A戦闘機180機、テジャスMark-2戦闘機200機を保有する予定です。また、新型ミサイルは複数の航空機プログラムに対応するため、武器のキャリッジや発射システムもそれに合わせて設計する必要があります。このような設計上の特徴は、予測期間中に注目される市場の航空機プラットフォームの成長見通しを促進します。

2019年は北米が市場を独占

北米は、2023年に兵器運搬・発射システム市場で最大のシェアを占めると推定されます。米国は、最も先進的な空中戦闘プラットフォームのフリートを保有しており、現在、既存のフリートのアップグレードに注力しています。さらに、兵器運搬・発射システムの大手サプライヤーやインテグレーターの本拠地であることから、同国は世界的にこのような機器の主要な輸出国であり消費国でもあります。2023年から2022年の間に、米国は武器輸出総額のシェアを75億米ドルから145億米ドルへと拡大させました。イスラエル、ロシア、中国といった潜在的な敵対国が、米軍やその同盟国、パートナーの航空資産を脅かす可能性のある、ますます多様で広範かつ近代的な地域攻撃ミサイル・システムを配備しているため、米国を拠点とする防衛請負業者は航空資産の能力を積極的に拡大・近代化し、兵器運搬・発射システムの需要を促進しています。米国はF-22を独自に開発したが、海軍用戦闘機の設計には一定の限界があったため、F-35計画が開始されました。F-22とF-35の能力における物理的な最大の違いは、武器格納庫です。F-35のウェポンベイは、空対地戦闘用の重い爆弾を搭載するため、F-22よりも深く狭いです。2023年6月現在、F-35は950機近く製造されています。同機は最終的に、F-16、F/A-18、A-10、F-117、ハリアーといった多数の米国製ジェット戦闘機に取って代わると予想されています。F-35の機体には、それぞれ2つの武器ステーションを備えた2つの内部武器ベイがあります。この航空機は、非ステルスミッション用に6つの外部武器ステーションを使用することができます。

兵器運搬・発射システム産業概要

兵器運搬・発射システムは、少数の主要企業の存在により統合されています。武器のキャリッジとリリースシステム市場の著名なプレーヤーは、Cobham Limited、RTX Corporation、L3Harris Technologies, Inc.、Moog Inc.、The Marvin Groupです。ベンダーは、統合された武器ペイロードの新しいバリエーションに対応するために、自社の製品にわずかな設計変更を実施しています。同市場では長期的な協力関係が好まれるため、新規参入の脅威は少ないです。例えば、2021年4月、Kratos Defense &Security Solutions, Inc.は、Kratos Unmanned Systems DivisionおよびArea-Iと共同で、XQ-58A Valkyrieの6回目の試験/デモンストレーション飛行と、内部武器格納庫からの最初の発射試験に成功しました。この試験では、小型無人UASシステムを内部武器庫から発射する能力を実証しました。Kratos、Area-I、AFRLはソフトウェアを開発し、SUASキャリッジを設計・製作し、無人UASシステムの発射を成功させました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 航空機

- ヘリコプター

- 無人航空機

- 兵器タイプ

- ミサイル

- 爆弾

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- 南アフリカ

- その他中東・アフリカ

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Cobham Limited

- RTX Corporation

- L3Harris Technologies, Inc.

- Moog Inc.

- The Marvin Group

- Marotta Controls, Inc.

- Alkan

- Systima Technologies, Inc.(Karman Space & Defense)

第7章 市場機会と今後の動向

The Weapons Carriage And Release Systems Market size is estimated at USD 409.12 million in 2024, and is expected to reach USD 502.40 million by 2029, growing at a CAGR of 4.19% during the forecast period (2024-2029).

The emergence of new technologies and platforms has transformed the warfare strategies of nations such as the US, Russia, and China. These countries have diverted their efforts towards the development of sophisticated and powerful weapons that can severely impact enemy strongholds and help attain a tactical advantage in case of an armed standoff. While weapon carriages are being redesigned for specific weaponry, release systems are being used extensively in current warfare scenarios due to their visual superiority and capability of performing pre-emptive strikes on specific locations.

However, the market may be deterred by the design challenges faced by system integrators to incorporate advanced features in their product portfolio without compromising on the payload capacity, aerodynamic profile, and range of a delivery platform. Designers are also required to ensure the availability of sophisticated integrated features and cross-compatibility with the different types of advanced weapon systems from several weapon manufacturers to develop a fully operational weapon carriage and release system, hence rendering a complex outlook to the overall system design.

Furthermore, the growth in the market for weapons transport and release systems is also driven by growing government regulations on border monitoring and the security of citizens against terrorism.

Weapons Carriage and Release System Market Trends

Aircraft Platform to Dominate the Market

Several fleet modernization programs are underway globally in 2023. However, the aircraft fleet expansion and modernization programs contributed to a majority share of such undertaken initiatives due to their high induction rate and relatively higher pricing justified by their inherent sophisticated flight characteristics. The demand for weapon carriage and release systems is directly proportional to the rate of procurement of new combat aerial assets and the modernization of existing ones to increase their lethality. For instance, the Indian Ministry of Defence plans to acquire aircraft to cope with the depleting inventories of the Indian Air Force (IAF). As per the orders, the Indian Air Force will have 40 LCA Tejas fighter jets, 180 LCA Tejas Mark-1A fighter jets, and at least 200 Tejas Mark-2 jets by 2038. Besides, with new missiles being compatible with several aircraft programs, the weapons carriage and release systems are required to be designed accordingly. Such design features drive the growth prospects of the aircraft platform of the market in focus during the forecast period.

North America Dominates the Market in 2019

North America is estimated to account for the largest share of the weapons carriage and release systems market in 2023. The US has one of the most advanced fleets of aerial combat platforms at its disposal and is currently focusing on upgrading its existing fleets. Moreover, the country is a key exporter and consumer of such equipment globally, as it is home to some of the leading suppliers and integrators of weapons carriage and release systems. Between 2023 and 2022, the US enhanced its share of total arms exports from USD 7.5 billion to USD 14.5 billion. With potential adversaries such as Israel, Russia, and China fielding an increasingly diverse, expansive, and modern range of regional offensive missile systems that can threaten the aerial assets of the US forces, its allies, and partners, the US-based defence contractors are actively expanding and modernizing the capabilities of their aerial assets, thereby driving the demand for weapons carriage and release systems. The US indigenously developed the F-22, but due to certain limitations with designing a naval variant, the F-35 program was initiated. The biggest physical difference in the capabilities between the F-22 and the F-35 is their weapon bays. The weapon bay on the F-35 is deeper and narrower than that of the F-22 to carry heavier bombs meant for air-to-ground combat. As of June 2023, nearly 950 F-35s have been manufactured. The aircraft is expected to eventually replace a large number of US jet fighters such as F-16, F/A-18, A-10, F-117, and the Harrier. The F-35 aircraft has two internal weapons bays with two weapons stations each. The aircraft can use six external weapons stations for non-stealthy missions.

Weapons Carriage and Release System Industry Overview

The weapons carriage and release systems are consolidated due to the presence of a few major players. The prominent players in the carriage of the weapons and release systems market are Cobham Limited, RTX Corporation, L3Harris Technologies, Inc., Moog Inc., and The Marvin Group. Vendors are implementing marginal design changes to their offerings to accommodate newer variants of integrated weapons payload. Long-term collaborations are preferred in the market; hence, the threat of entry of a new market player is minimal. For instance, in April 2021, Kratos Defense & Security Solutions, Inc., in partnership with Kratos Unmanned Systems Division and Area-I, successfully tested the XQ-58A Valkyrie's sixth test/demonstration flight and the first release from its internal weapons bay. The test demonstrated the ability to launch a small, unmanned UAS system from the internal weapons bay. Kratos, Area-I, and AFRL developed software and designed and fabricated the SUAS carriage to enable the successful release of the unmanned UAS system.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Aircraft

- 5.1.2 Helicopters

- 5.1.3 Unmanned Aerial Vehicles

- 5.2 Weapon Type

- 5.2.1 Missiles

- 5.2.2 Bombs

- 5.3 Geography

- 5.4 North America

- 5.4.1 United States

- 5.4.2 Canada

- 5.5 Europe

- 5.5.1 United Kingdom

- 5.5.2 France

- 5.5.3 Germany

- 5.5.4 Russia

- 5.5.5 Rest of Europe

- 5.6 Asia-Pacific

- 5.6.1 China

- 5.6.2 India

- 5.6.3 Japan

- 5.6.4 South Korea

- 5.6.5 Rest of Asia-Pacific

- 5.7 Latin America

- 5.7.1 Brazil

- 5.7.2 Mexico

- 5.7.3 Rest of Latin America

- 5.8 Middle East and Africa

- 5.8.1 United Arab Emirates

- 5.8.2 Saudi Arabia

- 5.8.3 Turkey

- 5.8.4 South Africa

- 5.8.5 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Cobham Limited

- 6.2.2 RTX Corporation

- 6.2.3 L3Harris Technologies, Inc.

- 6.2.4 Moog Inc.

- 6.2.5 The Marvin Group

- 6.2.6 Marotta Controls, Inc.

- 6.2.7 Alkan

- 6.2.8 Systima Technologies, Inc. (Karman Space & Defense)