|

|

市場調査レポート

商品コード

1439787

血管塞栓術:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Vascular Embolization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 血管塞栓術:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界の血管塞栓術市場規模は2024年に19億4,000万米ドルと推定され、2029年までに27億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.26%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)の流行は、世界的に施行された社会的距離措置により、新型コロナウイルス以外の適応症に対する病院やヘルスケアサービスが大幅に減少したため、血管塞栓術市場に影響を与えました。しかし、多くの調査研究により、血管塞栓術は細心の注意と予防策を講じて実施すれば、COVID-19感染症のパンデミック下でも安全であることが証明されています。 2020年に発表された「COVID-19症患者で行われた気管支動脈塞栓術:耐性と転帰」と題された調査研究によると、その結果は、気管支動脈塞栓術(BAE)を伴うCOVID-19症患者の重度の喀血(SH)の管理が効果的であることを実証しました。実現可能かつ効率的であり、安全ガイドラインに関しては、インターベンショナル放射線科(IR)スタッフを保護することが最も重要です。したがって、前述の要因により、調査対象の市場はCOVID-19感染症のパンデミック中に影響を受けると予想されます。

血管疾患の有病率の増加、塞栓製品と塞栓術の技術進歩、研究開発活動の増加、低侵襲手術に対する需要の高まりが、世界の血管塞栓術市場の主要な促進要因となっています。世界保健機関の2020年の最新情報によると、虚血性心疾患は世界の年間総死亡者数の16%の原因となっています。さらに、世界保健機関によると、世界中で毎年推定1,790万人が心血管疾患により死亡しています。これは世界の死亡者数の35%に相当します。さらに、これらの心血管疾患による死亡の85%は心臓発作や脳卒中が原因です。さらに、2020年7月にCureus Journal of Medical Scienceに掲載された論文によると、虚血性心疾患(IHD)は世界中で主な死因となっています。虚血性心疾患は世界中で約1億2,600万人(10万人あたり1,655人)が罹患しており、これは世界人口の約1.72%に相当します。虚血性心疾患の世界の有病率は、冠状動脈性心疾患、リウマチ性心疾患、脳血管疾患、その他の心臓疾患を含む心血管疾患のせいで、2030年までに10万人あたり1,845人を超えると予想されています。世界中で主な死因の一つとなっています。

さらに、従来の手術と比較して、低侵襲手術には、手術の痛み、損傷、傷跡、入院期間の短縮、精度の向上、回復時間の短縮などのいくつかの利点があり、低侵襲バルーン血管形成術を選択する患者が増加しています。手術。米国心臓病学会が報告したデータによると、2020年には米国で年間約120万件の血管形成術が行われました。さらに、専門クリニックと比較して、病院はアクセスしやすく、手頃な価格であるため、多くの患者数が集まることが予想されます。

また、主要企業のいくつかは、既存の製品と競合するために新しい製品や技術を開発して発売しており、また、他の企業は市場で動向になっている他の企業を買収して提携しています。たとえば、2020年 2月、Merit Medical Systems Inc.のEmboCubeおよびTorpedoデバイスは、血流を遮断する血管塞栓術の適応としてFDAに承認され、末梢血管系の出血と出血の制御に役立ちました。したがって、前述の要因により、調査対象セグメントは予測期間中に成長すると予想されます。ただし、手順に関連する高額なコスト、厳しい規制、およびこれらの手順に関連する複雑さは、調査対象の市場の成長を妨げると予想されます。

血管塞栓術市場の動向

非コイリングデバイスセグメントは、予測期間中に血管塞栓市場で主要な市場シェアを保持すると予想されます

慢性疾患の負担の増大や対象となる患者層の拡大などの要因が、この部門の成長を促進すると予想されています。世界保健機関の2020年報告書によると、過去20年間で慢性疾患の増加により死亡率が上昇しており、世界中で心臓病が主な死因となっています。 2000年以来、心臓病による死亡者数は約200万人増加し、2019年には約900万人に達しました。米国では現在、心臓病が全死亡者の16%を占めています。これは、血管塞栓に対する潜在的な市場需要を示しています。さまざまな種類の慢性疾患の負担が増大しているため、調査対象の市場は将来的に成長すると予想されます。

さらに、市場関係者は市場での新製品の発売に注力しています。たとえば、2021年 3月、シェイプメモリーメディカルは、IMPEDE-FX塞栓プラグに関して日本の医薬品医療機器総合機構から承認を取得しました。阻害塞栓プラグは、末梢血管系の血流を妨げるか、血流速度を低下させることが示されています。したがって、これらの要因により、非コイリングデバイスセグメントは予測期間中に有利な成長を経験すると予想されます。

北米は調査対象市場で大きなシェアを占めており、予測期間中にも同様のシェアを獲得すると予想される

北米は、がんおよび血管関連疾患の有病率の増加と、この地域での研究開発活動の増加により、世界の血管塞栓術市場で主要な市場シェアを保持すると予想されています。米国がん協会の推計によると、2020年には米国の15歳から39歳までの青少年および若年成人(AYA)の間で約89,500人ががんと診断され、約9,270人ががんで死亡しました。塞栓術は、さまざまな臨床シナリオを持つ患者において最も受け入れられているがん治療法の1つです。これは腫瘍内に虚血を生じさせ、腫瘍壊死を引き起こすために行われます。この効果は、塞栓物質に化学療法剤を添加することによってさらに増強される可能性があります。したがって、がんの負担の増加により、この地域の塞栓術が成長しています。脳動脈瘤は、アメリカ国民に影響を与えているもう一つの主要な疾患です。脳動脈瘤財団による2019年の統計によると、米国では推定650万人が未破裂脳動脈瘤を患っており、年間破裂率は10万人あたり約8~10人です。脳動脈瘤患者の場合、コイル塞栓術は、嚢を閉じて出血のリスクを軽減する物質で動脈瘤を埋めることで動脈瘤を治療する、最も一般的な低侵襲処置の1つです。したがって、国内の疾病負担の増大により、血管塞栓術の需要が高まると予想されます。

さらに、北米地域は他の地域に比べて技術や研究開発活動が進んでおり、市場にプラスの影響を与えることが期待されています。たとえば、2021年 3月、Instylla Inc.は、多血管性腫瘍の治療のための極めて重要なエンブレースハイドロゲル塞栓システム(HES)の世界的ランダム化臨床試験への最初の患者の登録を報告しました。

したがって、前述の要因により、調査対象市場は、予測期間中に北米で大幅な成長を遂げると予想されます。

血管塞栓術業界の概要

血管塞栓市場は競争が激しく、いくつかの主要企業で構成されています。現在市場を独占している企業には、Medtronic PLC、Cook Medical、Stryker Corporation、Boston Scientific Corporation、Abbott Laboratories、Johnson and Johnson(CERENOVUS)、Merit Medical Systems Inc.、Penumbra Inc.、Terumo Corporation、およびShape Memoryなどがあります。 Medical Inc.主要企業は、この市場での拠点を拡大するために、拡張、新製品の発売、買収などのさまざまな戦略を使用してきました。たとえば、ジョンソン・エンド・ジョンソンは2020年10月に、欧州で頑固な血栓を除去し、急性虚血性脳卒中患者の血行再建を可能にするNIMBUSを発売しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 血管疾患の有病率の増加

- 塞栓術の製品と処置における技術の進歩

- 研究開発活動の増加

- 市場抑制要因

- 塞栓術に伴う高額な費用

- 厳しい規制基準

- 塞栓術に伴う合併症

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 塞栓術による

- コイリング装置

- 非コイリング装置

- 用途別

- 末梢血管疾患

- 腫瘍学

- 神経内科

- 泌尿器科

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic PLC

- Cook Medical

- Stryker Corporation

- Boston Scientific Corporation

- Abbott Laboratories

- Johnson and Johnson(CERENOVUS)

- Merit Medical Systems Inc.

- Penumbra Inc

- Terumo Corp

- Shape Memory Medical Inc.

- B. Braun Melsungen AG

- WL Gore &Associates Inc.

第7章 市場機会と将来の動向

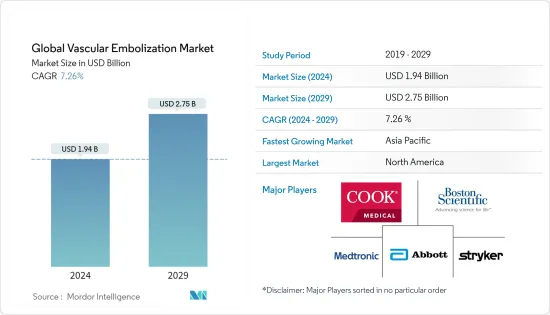

The Global Vascular Embolization Market size is estimated at USD 1.94 billion in 2024, and is expected to reach USD 2.75 billion by 2029, growing at a CAGR of 7.26% during the forecast period (2024-2029).

The outbreak of COVID-19 impacted the vascular embolization market, as hospitals and healthcare services for non-COVID indications were significantly reduced due to social distancing measures enforced globally. However, many research studies have proven that vascular embolization techniques are safe during the COVID-19 pandemic if performed with utmost care and precautions. According to a research study titled "Bronchial Artery Embolization Performed in COVID-19 Patients: Tolerance and Outcomes", published in 2020, the results demonstrated that management of severe hemoptysis (SH) in COVID-19 patients with bronchial artery embolization (BAE) was feasible and efficient, and concerning the safety guidelines, it is of utmost importance to protect the interventional radiology (IR) staff. Thus, owing to the aforementioned factors, the studied market is expected to be impacted during the COVID-19 pandemic.

The increasing prevalence of vascular diseases, technological advancements in embolization products and procedures, increasing research and development activities, and growing demand for minimally invasive procedures are the key driving factors in the global vascular embolization market. According to the 2020 updates of the World Health Organization, ischemic heart disease is responsible for 16% of the world's total deaths annually. Additionally, according to the World Health Organization, an estimated 17.9 million people die due to cardiovascular diseases worldwide, each year. This represents 35% of global deaths. Additionally, 85% of these cardiovascular disease deaths are due to heart attack and stroke. In addition, according to the article published in Cureus Journal of Medical Science in July 2020, ischemic heart disease (IHD) is a leading cause of death worldwide. Ischemic heart disease affects around 126 million individuals (1,655 per 100,000) globally, which is approximately 1.72% of the world's population. The global prevalence of ischemic heart disease is expected to exceed 1,845 per 100,000 by the year 2030.owing to cardiovascular diseases that include coronary heart disease, rheumatic heart disease, cerebrovascular disease, and other heart conditions. It is one of the leading causes of death worldwide.

Moreover, compared to conventional surgeries, the several advantages of minimally invasive surgeries, such as reduced surgical pain, injury, scarring, hospital stay, higher accuracy, and speedy recovery time, are encouraging an increasing number of patients to opt for minimally invasive balloon angioplasty surgeries. As per the data reported by the American College of Cardiology, in 2020, approximately 1.2 million angioplasties were performed in a year in the United States. Moreover, the high accessibility and affordability of hospitals, as compared to the specialty clinics, are expected to attract a large patient population.

Also, a few of the key players are developing and launching novel products and technologies to compete with the existing products, while others are acquiring and partnering with the other companies trending in the market. For instance, in February 2020, EmboCube and Torpedo devices of Merit Medical Systems Inc. were FDA indicated for the embolization of blood vessels to occlude blood flow, thus aiding in the control of bleeding and hemorrhaging in the peripheral vasculature. Thus, owing to the aforementioned factors, the studied segment is expected to grow over the forecast period. However, the high cost associated with the procedures, stringent regulations, and complications associated with these procedures are expected to hinder the growth of the market studied.

Vascular Embolization Market Trends

The Non-coiling Devices Segment is Expected to Hold a Major Market Share in the Vascular Embolization Market over the Forecast Period

Factors such as the growing burden of chronic diseases and the expanding target patient pool are expected to propel the segment's growth. According to the World Health Organization report 2020, the mortality rate has been growing due to the number of chronic diseases increasing over the past 20 years, with heart disease being the leading cause of death worldwide. Since 2000, the number of deaths from heart disease has increased by nearly 2 million, to nearly 9 million in 2019. In the United States, heart disease now accounts for 16% of all deaths. This indicates a potential market demand for vascular embolization. Owing to the increasing burden of various types of chronic disorders, the market studied is expected to grow in the future.

Additionally, market players are focusing on the launch of new products in the market. For instance, in March 2021, Shape Memory Medical received approval from Japan's Pharmaceutical and Medical Devices Agency for IMPEDE-FX Embolization Plug. Impede embolization plugs are indicated to obstruct or reduce the rate of blood flow in the peripheral vasculature. Thus, owing to these factors, the non-coiling devices segment is expected to experience lucrative growth during the forecast period.

North America Holds a Significant Share in the Studied Market and Expected to do Same during the Forecast Period

North America is expected to hold a major market share in the global vascular embolization market due to the increasing prevalence of cancer and vascular-related diseases and increasing research and development activities in this region. According to the American Cancer Society estimates, in 2020, there were approximately 89,500 cancer cases diagnosed and about 9,270 cancer deaths among adolescents and young adults (AYAs) aged between 15 and 39 years in the United States. Embolization is one of the most accepted modalities of cancer treatment in patients with a variety of clinical scenarios. It is done to produce ischemia within the tumor, resulting in tumor necrosis. This effect may be further potentiated by the addition of a chemotherapeutic agent to the embolic material. Hence, the rising burden of cancer is giving growth to the embolization procedures in this region. Brain aneurysm is another major disorder that has affected the American population. As per 2019 Statistics by the Brain Aneurysm Foundation, an estimated 6.5 million people in the United States have an unruptured brain aneurysm, with an annual rate of rupture of approximately 8-10 per 100,000 people. In a patient with a brain aneurysm, coil embolization is one of the most common minimally-invasive procedures to treat an aneurysm by filling it with material that closes the sac and reduces the risk of bleeding. Hence, the increasing burden of diseases in the country is expected to drive the demand for vascular embolization.

Moreover, the North American region is ahead in technology and R&D activities in comparison to other regions, which is expected to positively impact the market. For instance, in March 2021, Instylla Inc. reported the enrollment of the first patients in the pivotal Embrace Hydrogel Embolic System (HES) global randomized clinical trial for the treatment of hypervascular tumors.

Thus, owing to the aforementioned factors, the studied market is expected to witness significant growth in North America over the forecast period.

Vascular Embolization Industry Overview

The vascular embolization market is highly competitive and consists of several major players. Some of the companies that are currently dominating the market are Medtronic PLC, Cook Medical, Stryker Corporation, Boston Scientific Corporation, Abbott Laboratories, Johnson and Johnson (CERENOVUS), Merit Medical Systems Inc., Penumbra Inc., Terumo Corporation, and Shape Memory Medical Inc. The major players have used various strategies such as expansions, new product launches, and acquisitions to increase their footprints in this market. For instance, in October 2020, Johnson and Johnson launched NIMBUS to remove tough clots and enable revascularization for patients with acute ischaemic stroke in Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Vascular Diseases

- 4.2.2 Technological Advancements in Embolization Products and Procedures

- 4.2.3 Increasing Research and Development Activities

- 4.3 Market Restraints

- 4.3.1 High Costs Associated with Embolization Procedures

- 4.3.2 Stringent Regulatory Norms

- 4.3.3 Complications Associated with Embolization Procedures

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Embolization Technique

- 5.1.1 Coiling Devices

- 5.1.2 Non-coiling Devices

- 5.2 By Application

- 5.2.1 Peripheral Vascular Disease

- 5.2.2 Oncology

- 5.2.3 Neurology

- 5.2.4 Urology

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic PLC

- 6.1.2 Cook Medical

- 6.1.3 Stryker Corporation

- 6.1.4 Boston Scientific Corporation

- 6.1.5 Abbott Laboratories

- 6.1.6 Johnson and Johnson (CERENOVUS)

- 6.1.7 Merit Medical Systems Inc.

- 6.1.8 Penumbra Inc

- 6.1.9 Terumo Corp

- 6.1.10 Shape Memory Medical Inc.

- 6.1.11 B. Braun Melsungen AG

- 6.1.12 W. L. Gore & Associates Inc.