|

市場調査レポート

商品コード

1405733

金属洗浄剤 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測Metal Cleaning Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 金属洗浄剤 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

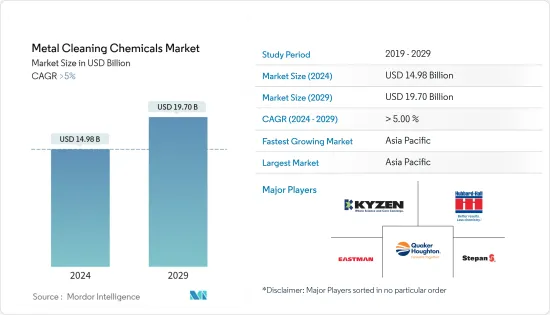

金属洗浄剤市場規模は、2024年に149億8,000万米ドルと推定され、2029年には197億米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは5%以上で成長すると予測されます。

COVID-19パンデミックは、消毒剤、万能クリーナー、表面クリーナー、洗剤、石鹸、その他の衛生製品の需要が増加したため、金属洗浄化学品市場にプラスの影響を与えました。これは、製薬会社や化学会社が衛生・清掃分野での売上を伸ばすのにプラスに働いた。

製造業における工業用洗浄とメンテナンスの需要の増加が、市場成長の原動力となっています。

ほとんどの洗浄用化学薬品は腐食性があり、酸素と混ざると危険です。廃棄物管理と洗浄化学薬品の有害性は、市場成長を妨げる大きな課題です。

さらに、グリーンおよびバイオベースの金属洗浄剤は、その有効性、安全性、持続可能性により需要が伸びています。これらは、世界市場において急速かつ収益性の高い拡大の機会を生み出す可能性が高いです。

アジア太平洋地域は、インド、中国、日本を消費量の主要国として、金属洗浄剤の市場を独占しました。

金属洗浄剤の市場動向

鉄鋼セクターにおける需要の増加

- 鉄鋼業界は、金属表面を清潔に保つ必要があるため、金属洗浄剤の最大のユーザーです。工業用金属洗浄剤は、装置を分解・組立することなく洗浄でき、洗浄後の腐食も防止できるため、この課題に対する貴重なソリューションです。

- この分野は、都市化、技術の進歩、政府の支援、工業用途における鉄鋼の旺盛な需要、製造ニーズの増加、工業用クリーニングとメンテナンスへの注目の高まりにより成長しています。

- 世界鉄鋼協会は、2022年の2.3%減に続き、2023年には1.0%増の完成鋼材使用量になると予測しています。中国経済は2022年の鉄鋼生産に大きな影響を与え、4%減少しました。COVID-19抑制策が長期化し、不動産や建設プロジェクトの需要が減少したため、2023年の中国の鉄鋼生産は安定を保つと予想されます。

- 2022年には、インフラ支出、旺盛な消費者需要、自動車産業の成長に牽引されたインドの鉄鋼完成品生産が増加し、予測期間中に鉄鋼生産に関連する金属洗浄化学品市場を押し上げると予想されます。

- 国家鉄鋼政策によると、インドは2022-23会計年度に1億2,500万トンを超える鉄鋼を生産します。ニューデリーは、この生産量を2030年までに3億トンに増やすことを目指しています。

- 鉄鋼は、金属洗浄剤市場において最も重要な金属種類の一つであり、予測期間中、この市場をさらに牽引すると予想されます。

アジア太平洋が金属洗浄剤市場を独占する

- アジア太平洋市場は、鉄鋼やアルミニウムなどの金属の生産量と消費量が多いため、最も速い速度で成長すると予想されます。これらの金属は、各種部品、自動車フレーム、工業用制御パネルなどの製造に広く使用されており、洗浄には金属洗浄液が必要です。

- この地域の急速な経済成長は、可処分所得の上昇と相まって、国際企業が現地市場に参入し、知名度と収益の可能性を高める機会を生み出しています。

- 世界鉄鋼協会によると、インドの2022-23年度の粗鋼生産量は1億2,532万トン、完成鋼生産量は1億2,129万トンで、粗鋼生産量では世界第2位です。

- OICAによると、世界の自動車産業は2022年に6%成長しました。中国、ドイツ、韓国、カナダ、英国、イタリアを含む世界中の先進国および発展途上国において、2022年の自動車生産台数は増加しました。2022年には8,500万台以上の自動車が生産されました。

- IBEF(インド・ブランド・エクイティ財団)によると、30社が特殊鋼の生産連動奨励金(PLI)スキームの申請を67件承認しました。これらの承認により、4,250兆インドルピー(51億9,000万米ドル)の投資が誘致され、下流の鉄鋼生産能力が2,600万トン増加する見込みです。

- インベスト・インディアは、インドが2026年度までにエレクトロニクス・システム設計・製造(ESDM)分野で1兆米ドルのデジタル経済になると予測しています。インドのエレクトロニクス市場は現在1,550億米ドル規模であり、国内生産が65%を占めています。さらに、100億米ドルのインセンティブ・プログラムであるセミコン・インディア・プログラムが、国内の持続可能な半導体とディスプレイのエコシステムを発展させるために開始されました。

- PwCによると、インドの化学産業は世界で最も急成長している分野のひとつで、2025年には3,040億米ドルに達すると予測されています。

- IBEFによると、インドは世界第6位、アジア第3位の化学品生産国で、インドのGDPに7%貢献しています。政府は、2023-24年度連邦予算において、化学・石油化学省に173.45カロールインドルピー(2,093万米ドル)を割り当てた。

- アジア太平洋地域は、政府や企業による急速な成長と投資を経験しています。アジア太平洋地域は、中国、インド、日本が生産と消費をリードしており、世界の主要な化学市場になろうとしています。

金属洗浄剤産業の概要

金属洗浄剤市場は、その性質上、断片化されています。主な企業(順不同)には、クエーカー・ホートン、ステパン・カンパニー、ハバード・ホール、KYZEN CORPORATION、イーストマン・ケミカル・カンパニーなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 製造業からの需要増加

- 水性ベースの金属洗浄ソリューション市場の成長

- 航空宇宙産業における需要の高まり

- 抑制要因

- 金属洗浄剤の使用に関する安全衛生上の懸念

- 高度な金属洗浄剤の高コスト

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模)

- タイプ

- 酸性

- 塩基性

- 中性

- 形態

- 水性

- 溶剤

- エンドユーザー産業

- 航空宇宙

- 自動車・輸送

- 電気・電子

- 化学・製薬

- 石油・ガス

- その他のエンドユーザー産業(ヘルスケア、飲食品)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Arrow Solutions

- Avudai Surface Treatments Pvt Ltd

- BASF SE

- CLARIANT

- Chautauqua Chemical Company

- Crest Chemicals.

- Delstar Metal Finishing, Inc.

- Dow

- DST-CHEMICALS

- Eastman Chemical Company

- Ecolab

- Elmer Wallace Ltd.

- Hubbard-Hall

- Henkel AG & Co. KGaA

- ICL

- KYZEN CORPORATION

- Lincoln Chemical Corporation

- Luster-On Products, Inc.

- Modern Chemical, Inc.

- PARKER HANNIFIN CORP

- PCC Group

- Quaker Houghton

- Rochester Midland Corp

- Solugen

- Spartan Chemical Company, Inc.

- Stepan Company

- The Chemours Company

- Zavenir Daubert

第7章 市場機会と今後の動向

- バイオベースの洗浄剤の開発

- ヘルスケア産業における需要の高まり

The Metal Cleaning Chemicals Market size is estimated at USD 14.98 billion in 2024, and is expected to reach USD 19.70 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The COVID-19 pandemic had a positive impact on the metal cleaning chemicals market, as demand for disinfectants, all-purpose cleaners, surface cleaners, detergents, soaps, and other hygiene products increased. This positively affected the pharmaceutical and chemical companies to boost their sales in the hygiene and cleaning sector.

The increasing demand for industrial cleaning and maintenance in the manufacturing sector is driving the market growth.

Most cleaning chemicals are corrosive and dangerous to mix with oxygen. Waste management and the harmful effects of cleaning chemicals are major challenges hindering market growth.

Further, green and bio-based metal cleaning chemicals are growing in demand due to their effectiveness, safety, and sustainability. They are likely to create opportunities for rapid and profitable expansion in the global market.

Asia-Pacific region dominated the market for metal cleaning chemicals, with India, China, and Japan representing major countries in terms of consumption.

Metal Cleaning Chemicals Market Trends

Increasing Demand in the Steel Sector

- The steel industry is the largest user of metal cleaning chemicals because it needs to keep its metallic surfaces clean. Industrial metal cleaners are a valuable solution for this challenge because they can clean equipment without having to disassemble and reassemble it, and they also prevent corrosion after cleaning.

- This segment is growing due to urbanization, technological advancements, government support, strong demand for steel in industrial applications, increasing manufacturing needs, and a growing focus on industrial cleaning and maintenance.

- The World Steel Association predicts that finished steel usage will increase by 1.0% in 2023, following a 2.3% decline in 2022. China's economy had a significant impact on steel production in 2022, which fell by 4%. Due to prolonged COVID-19 containment measures, which reduced demand for real estate and construction projects, steel production is expected to remain stable in China in 2023.

- India's increased production of finished steel products in 2022, driven by infrastructure spending, strong consumer demand, and automotive industry growth, is expected to boost the metal cleaning chemicals market associated with steel production during the forecast period.

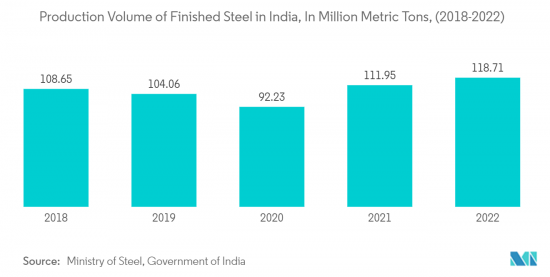

- India produced over 125 million metric tons of steel in the fiscal year 2022-23, according to the National Steel Policy. New Delhi aims to increase this production to 300 million metric tons by 2030.

- Steel is one of the most significant metal types in the metal cleaning chemicals market and is expected to drive this market further during the forecast period.

Asia-Pacific to Dominate the Metal Cleaning Chemicals Market

- The Asia-Pacific market is expected to grow at the fastest rate due to the high production and consumption of metals such as steel and aluminum. These metals are widely used in the manufacturing of various components, vehicle frames, and industrial control panels, among others, and require metal cleaning solutions to be cleaned.

- The rapid economic growth in the region, coupled with rising disposable incomes, is creating opportunities for international companies to enter the local market and increase their visibility and revenue potential.

- India produced 125.32 million metric tons of crude steel and 121.29 million metric tons of finished steel in fiscal year 2022-23, making it the world's second-largest producer of crude steel, according to the World Steel Association.

- The global automotive industry grew by 6% in 2022, according to OICA. In developed and developing countries across the world, including China, Germany, South Korea, Canada, the United Kingdom, and Italy, automotive production increased in 2022. Over 85 million motor vehicles were manufactured in 2022.

- According to IBEF (India Brand Equity Foundation), 30 companies have had 67 applications approved for the Production Linked Incentive (PLI) Scheme for Specialty Steel. These approvals are expected to attract an investment of INR 4,250 trillion (USD 5.19 billion) and increase downstream iron and steel capacity by 26 million tonnes.

- Invest India predicts that India will become a USD 1 trillion digital economy in the Electronics System Design and Manufacturing (ESDM) sector by fiscal year 2026. The Indian electronics market is currently worth USD 155 billion, with domestic production accounting for 65%. Additionally, the Semicon India Program, a USD 10 billion incentive program, was launched to develop a sustainable semiconductor and display ecosystem in the country.

- According to PwC, India's chemical industry is one of the world's fastest-growing sectors, projected to reach a value of USD 304 billion by 2025.

- India is the world's 6th and Asia's 3rd largest producer of chemicals, contributing 7% to India's GDP, according to IBEF. The government allocated INR 173.45 crore (USD 20.93 million) to the Department of Chemicals and Petrochemicals in the Union Budget for 2023-24.

- Asia-Pacific is experiencing rapid growth and investment from governments and businesses in the region. It is poised to become the world's dominant chemical market, with China, India, and Japan leading production and consumption.

Metal Cleaning Chemicals Industry Overview

The metal cleaning chemicals market is fragmented in nature. The major players (not in any particular order) include Quaker Houghton, Stepan Company, Hubbard-Hall, KYZEN CORPORATION, and Eastman Chemical Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Manufacturing Industries

- 4.1.2 Growing Market for Aqueous-Based Metal Cleaning Solutions

- 4.1.3 Rising Demand in the Aerospace Industry

- 4.2 Restraints

- 4.2.1 Health and Safety Concerns Related to the Use of Metal Cleaning Chemicals

- 4.2.2 High Cost of Advanced Metal Cleaning Chemicals

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Type

- 5.1.1 Acidic

- 5.1.2 Basic

- 5.1.3 Neutral

- 5.2 Form

- 5.2.1 Aqueous

- 5.2.2 Solvent

- 5.3 End-user Industry

- 5.3.1 Aerpospace

- 5.3.2 Automotive and Transportation

- 5.3.3 Electrical and Electronics

- 5.3.4 Chemical and Pharmaceutical

- 5.3.5 Oil and Gas

- 5.3.6 Other End-user Industries (Healthcare, and Food and Beverage)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arrow Solutions

- 6.4.2 Avudai Surface Treatments Pvt Ltd

- 6.4.3 BASF SE

- 6.4.4 CLARIANT

- 6.4.5 Chautauqua Chemical Company

- 6.4.6 Crest Chemicals.

- 6.4.7 Delstar Metal Finishing, Inc.

- 6.4.8 Dow

- 6.4.9 DST-CHEMICALS

- 6.4.10 Eastman Chemical Company

- 6.4.11 Ecolab

- 6.4.12 Elmer Wallace Ltd.

- 6.4.13 Hubbard-Hall

- 6.4.14 Henkel AG & Co. KGaA

- 6.4.15 ICL

- 6.4.16 KYZEN CORPORATION

- 6.4.17 Lincoln Chemical Corporation

- 6.4.18 Luster-On Products, Inc.

- 6.4.19 Modern Chemical, Inc.

- 6.4.20 PARKER HANNIFIN CORP

- 6.4.21 PCC Group

- 6.4.22 Quaker Houghton

- 6.4.23 Rochester Midland Corp

- 6.4.24 Solugen

- 6.4.25 Spartan Chemical Company, Inc.

- 6.4.26 Stepan Company

- 6.4.27 The Chemours Company

- 6.4.28 Zavenir Daubert

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Bio-based Cleaning Chemicals

- 7.2 Growing Demand in the Healthcare Industry