|

市場調査レポート

商品コード

1687473

リチウムイオン電池リサイクル- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Lithium-ion Battery Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| リチウムイオン電池リサイクル- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

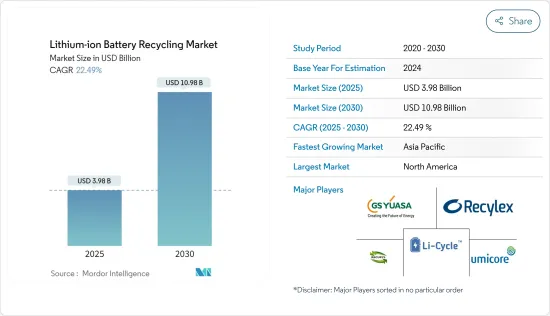

リチウムイオン電池リサイクル市場規模は2025年に39億8,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは22.49%で、2030年には109億8,000万米ドルに達すると予測されます。

さまざまな種類のバッテリーリサイクル技術の中でも、リチウムイオン電池(LIB)リサイクル市場は、予測期間の後半に世界のバッテリーリサイクル市場を独占すると予想されます。さらに、リチウムイオン電池の価格下落や電気自動車の普及によるリチウムイオン電池の使用量の増加と相まって、電池廃棄物処理に関する懸念の高まりや政府の厳しい政策が、予測期間中のリチウムイオン電池リサイクル市場を牽引すると思われます。しかし、リチウムイオン電池を製造するための原材料は低コストで入手できるのに対し、リサイクルには高いコストがかかります。高いコストに加え、強固なサプライチェーンがないこと、バッテリーのリサイクルに関連する歩留まりが低いことが、予測期間中のバッテリーリサイクル市場の成長を抑制する可能性が高いです。

主なハイライト

- 再生可能エネルギー発電を促進する政策レベルの取り組みや電気自動車の大量導入に伴い、エネルギー貯蔵ソリューションが必要とされる電力セクターが著しい成長を遂げています。

- メーカーが開発する技術的に高度な電池の創造につながる電池技術の主要企業の開発は、画期的な電池リサイクル技術を作るために投資し、資源を振り向ける電池リサイクル企業にとって大きな機会を生み出す可能性が高いです。

- アジア太平洋は、製造業、再生可能エネルギー、EV需要の成長により、予測期間中、リチウムイオン電池リサイクル市場をリードすると予想されます。

リチウムイオン電池リサイクル市場動向

電力産業における需要の増加

- リチウムイオン電池の価格は過去10年間で急落しています。2018年、リチウムイオン電池価格は1kWhあたり176米ドルでした。リチウムイオン電池価格は継続的に下落しており、2018年の価格は2017年の価格と比較して17.75%減少しました。リチウムイオン電池はESSなど電力分野に関連する様々なアプリケーションに使用されており、電力分野の市場を牽引する可能性が高いです。

- 大幅なコストダウンの主な理由は以下の2点である:

- 電池材料の改良、非活性材料の量と材料コストの削減、セル設計と生産歩留まりの改善、生産速度の向上を目指した持続的な研究開発によって達成された電池性能の着実な向上。

- リチウムイオン電池製造における規模の経済の達成に貢献した中国を中心とする電力業界のエンドユーザー向け生産量の増加と、メーカー間の競争を激化させた大規模な生産能力増強(価格はさらに低下したが、メーカーの収益性は犠牲になった)。

- こうした動向は、急激かつ持続的なコスト削減をもたらし、リチウムイオンが、グリッド規模、ビハインド・ザ・メーター・ストレージ、住宅用ストレージ、マイクログリッドなど、あらゆるエネルギー・ストレージ、電力産業市場で選択される電池化学として定着するのに役立つと予想されます。

- さらに、リチウムイオン電池の平均価格の下落は続き、2025年までに約100米ドル/kWhに達すると予想されます。この動向により、予測期間中、太陽光、風力、水力などの再生可能エネルギーと組み合わせたエネルギー貯蔵システム(ESS)のような、新しくエキサイティングな市場でのリチウムイオン電池の用途が、住宅用と商業用の両方で増加すると予想されます。

- したがって、価格の下落に伴い、電力業界ではリチウムイオン電池の使用が増加すると予想されます。このような電池の採用をより持続可能で環境に優しいものにするために、これらの電池をリサイクルする必要性も予測期間中に加速すると予想されます。

アジア太平洋が市場を独占する

- リチウムイオン電池は従来、主に携帯電話、ノートパソコン、PCなどの民生用電子機器に使用されてきたが、EVはCO2や窒素酸化物などの温室効果ガスを排出しないため環境負荷が低いなどの理由から、現在ではハイブリッド車や完全な電気自動車(EV)の電源として使用されるよう設計が見直されつつあります。

- 電気自動車やエネルギー貯蔵システム(ESS)のような新しくエキサイティングな市場の出現は、商業用と住宅用の両方のアプリケーションで、LIBの需要を牽引しています。さらに、ESSは風力、太陽光、水力などの自然エネルギーと組み合わされ、送電網の安定性を高めるために技術的にも商業的にも必要であり、その結果、LIB分野を牽引しています。

- 現在、中国は電気自動車の世界販売台数の約40%を占める最大の市場です。中国は国内の大気汚染レベルを下げる努力をしており、電気自動車の販売台数は高い成長率を記録すると予想され、その結果LIBの高い需要につながっています。

- 現在、中国は電気自動車用リチウムイオン電池の最大生産国です。中国のリチウム生産量は、2017年の6,800トンから2018年には8,000トンに増加しています。電池は常に環境問題に関連しているため、中国政府は、業界が必要に応じて設置しなければならないリサイクル施設の方針を提示しています。

- さらに、インド政府は2018年8月、EVの導入とリチウムイオン電池の現地生産を奨励するため、ハイブリッド車と電気自動車の迅速な導入と製造(FAME)インド・スキームの第2フェーズに5,500カロールインドルピーの支出を指示しました。このため、アマゾンやアマラ・ラジャ・バッテリーズなど、インドの自動車部品メーカーや電力・エネルギー・ソリューション・プロバイダー数社が、国内で活況を呈するグリーン車市場を活用するため、リチウムイオン電池の現地生産計画を打ち出しています。

- また、同地域の政府による技術開発のための研究開発投資は、リサイクル工程にかかるコストを削減するのに役立ち、リサイクル企業がリサイクル材料を新たな製品の製造に利用する動機付けとなり、市場の成長に貢献します。したがって、最近の動向は予測期間中にリチウムイオン電池リサイクル市場を促進すると予想されます。

リチウムイオン電池リサイクル産業の概要

リチウムイオン電池リサイクル市場は、複雑な技術のため、この業界で事業展開している企業が少なく、適度に断片化されています。この市場の主要企業には、Glencore、GS Yuasa Corporation、Li-Cycle Technology、Recupyl Sas、Umicore、Metal Conversion Technologiesなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2025年までの市場規模および需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 産業別

- 自動車

- 海洋

- 電力

- その他

- 技術

- 湿式冶金プロセス

- 乾式冶金プロセス

- 物理的/機械的プロセス

- 地域

- 北米

- アジア太平洋

- 欧州

- 南米

- 中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Glencore PLC

- Green Technology Solutions, Inc.

- Li-Cycle Technology

- Recupyl Sas

- Umicore SA

- Metal Conversion Technologies LLC

- Retriev Technologies Inc.

- Raw Materials Company

- TES-AMM Pte Ltd.

- American Manganese

第7章 市場機会と今後の動向

The Lithium-ion Battery Recycling Market size is estimated at USD 3.98 billion in 2025, and is expected to reach USD 10.98 billion by 2030, at a CAGR of 22.49% during the forecast period (2025-2030).

Among different types of battery recycling technology, the lithium-ion battery (LIB) recycling market is expected to dominate the global battery recycling market in the latter part of the forecast period, majorly due to the demand for lithium-ion batteries and its ability such as favorable capacity-to-weight ratio. Moreover, Rising concerns over battery waste disposal and stringent government policies clubbed with the increase in usage of lithium-ion battery due to the declining lithium-ion battery prices and growing adoption of electric vehicles, are likely to drive the lithium-ion battery recycling market during the forecast period. However, the raw materials for the manufacturing of lithium-ion batteries are available at a low cost, whereas a high cost is incurred in recycling. The high cost, along with the lack of a strong supply chain and low yield related to battery recycling, is likely to restrain the growth of the battery recycling market during the forecast period.

Key Highlights

- The power sector witnessing significant growth owing to requirement for energy storage solutions in the wake of policy-level initiatives to promote renewable power generation and massive deployment of electric vehicles.

- Advancements in battery technologies leading to the creation of technologically advanced batteries being developed by manufacturers are likely to create a massive opportunity for the battery recycling companies to invest and redirect their resources to make a breakthrough battery recycling technology.

- Asia-Pacific is expected to lead the lithium-ion battery recycling market, during the forecast period, due to the growth of the manufacturing sector, renewables power and the EV demand.

Lithium-Ion Battery Recycling Market Trends

Increasing Demand In Power Industry

- The price of lithium-ion batteries has fallen steeply over the past 10 years. In 2018, the lithium-ion battery price was USD 176 per kWh. Lithium-ion battery prices are falling continuously, and the price decreased by 17.75% in 2018 compared to the price in 2017. The lithium-ion battery used in various application related to power sector such as ESS and other, which in turn likely to drive the market in power sector.

- The two principal reasons for the drastic cost decline are:

- The steady improvement of battery performance achieved through sustained R&D, aimed at improving battery materials, reducing the amount of non-active materials and the cost of materials, improving cell design and production yield, and increasing production speed.

- Increase in production volume for end user in power industry, particularly in China, which helped in achieving the economies of scale in lithium-ion battery manufacturing, and the large capacity additions, which increased the competition among manufacturers (further declining the prices, but at the expense of the profitability of the manufacturers).

- These trends result in sharp and sustained cost reduction which is expected to help cement lithium-ion as the battery chemistry of choice in all energy storage, power industry markets, including grid-scale, behind-the-meter storage, residential storage, and micro-grids.

- Furthermore, the decline in average lithium-ion battery prices is expected to continue and reach approximately USD 100/kWh by 2025, in turn, making it much more cost-competitive than other battery types. The trend is expected to result in an increased application of lithium-ion batteries in new and exciting markets, such as energy storage systems (ESS), paired with renewables, like solar, wind, or hydro, for both residential and commercial applications, during the forecast period.

- Hence, with declining prices, the use of lithium-ion batteries is expected to rise in power industry. The need for recycling these batteries is also expected to gain pace during the forecast period, in order to make the adoption of such batteries more sustainable and eco-friendlier.

Asia-Pacific to Dominate the Market

- Lithium-ion batteries have traditionally been used mainly in consumer electronic devices, such as mobile phones, notebook, and PCs, but are now increasingly being redesigned for use as the power source of choice in hybrid and the complete electric vehicle (EV) range, owing to factors, such as low environmental impact, as EV does not emit any CO2, nitrogen oxides, or any other greenhouse gases.

- The emergence of the new and exciting markets, such as electric vehicle and energy storage systems (ESS), for both the commercial and residential applications, is driving the demand for LIB. Moreover, ESS, coupled with renewables, such as wind, solar, or hydro, is technically and commercially necessary for increasing grid stability, consequently, driving the LIB segment.

- Currently, China is the largest market for electric vehicles, as the country accounts for around 40% of the global sale. China is making efforts to reduce the air pollution level in the country, and it is expected to register a high growth rate in the electric vehicle sales, consequently, leading to the high demand for LIB.

- Currently, China is the largest manufacturer of lithium-ion battery majorly for electric vehicles. In China, lithium production in the country, increasing from 6,800 metric tons in 2017 to 8,000 metric tons in 2018. As batteries are always related to environmental concerns, the government of china presents a policy for recycling facilities that the industry must set up as required.

- Furthermore, in August 2018, the Government of India directed an outlay of INR 5,500 crore for the second phase of the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) India Scheme, for encouraging the adoption of EVs and local manufacturing of lithium-ion batteries. Thus, several automobile component manufacturers and power and energy solution providers in India, such as Amazon and Amara Raja Batteries, have put forth plans for manufacturing lithium-ion batteries locally, to leverage the booming green vehicles market in the country.

- Additionally, the R&D investment by the government in the region on developing technologies can help decrease the cost incurred for the recycling process, which can motivate the recycling companies to take up recycled material for manufacturing a new product, and thereby, helping the growth of the market. Hence the recent trends are expected to propel the lithium-ion battery recycling marketduring the forecast period.

Lithium-Ion Battery Recycling Industry Overview

The lithium-ion battery recycling market is moderately fragmented due to few companies operating in the industry because of the complex technology. The key players in this market include Glencore, GS Yuasa Corporation, Li-Cycle Technology, Recupyl Sas,Umicore, Metal Conversion Technologies, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD billion, until 2025

- 4.3 Recent Trends and Developments

- 4.4 Government Policies & Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes Products and Services

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Industry

- 5.1.1 Automotive

- 5.1.2 Marine

- 5.1.3 Power

- 5.1.4 Others

- 5.2 Technology

- 5.2.1 Hydrometallurgical Process

- 5.2.2 Pyrometallurgy Process

- 5.2.3 Physical/Mechanical Process

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Asia-Pacific

- 5.3.3 Europe

- 5.3.4 South America

- 5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Glencore PLC

- 6.3.2 Green Technology Solutions, Inc.

- 6.3.3 Li-Cycle Technology

- 6.3.4 Recupyl Sas

- 6.3.5 Umicore SA

- 6.3.6 Metal Conversion Technologies LLC

- 6.3.7 Retriev Technologies Inc.

- 6.3.8 Raw Materials Company

- 6.3.9 TES-AMM Pte Ltd.

- 6.3.10 American Manganese