|

市場調査レポート

商品コード

1445511

後眼部疾患: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Posterior Segment Eye Disorders - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 後眼部疾患: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

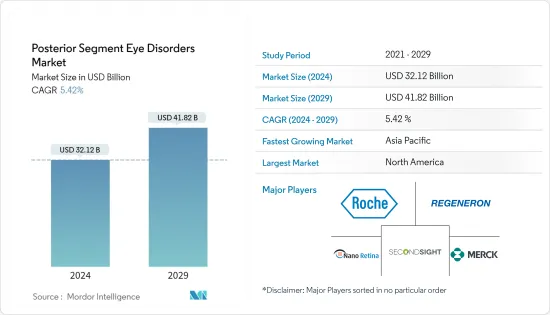

後眼部疾患市場規模は、2024年に321億2,000万米ドルと推定され、2029年までに418億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.42%のCAGRで成長します。

COVID-19感染症のパンデミックにより、COVID-19症以外の病状に対する他の治療法や医薬品の研究開発活動が混乱しました。これは、世界中の医薬品および医療機器の治療手順とサプライチェーン、そして後眼部疾患の市場に影響を与えました。たとえば、オフタルモロガー・バラカー誌が2021年3月に発表した健康に関する記事によると、COVID-19は、非常に急速に病気が進行し、検査機関による追跡調査ができなかった緑内障患者に重篤かつ不可逆的な結果を引き起こしたといいます。場合によっては視野の喪失につながることもありました。したがって、後眼部疾患市場に対するCOVID-19の全体的な影響は、主に後眼部に関連する疾患の診断および治療手順の低下により、悪影響を及ぼしました。しかし、パンデミック関連の制限によって生じた外科手術の未処理を解消するための眼疾患手術が世界中で増加し、パンデミック後期の市場の成長を補った。

後眼部疾患は、世界中で視覚障害の主な原因の1つです。眼疾患、糖尿病、および眼疾患にかかりやすい高齢者人口の増加により、その有病率は徐々に増加しています。これらの疾患の負担の増加に伴い、診断と治療の需要が世界中で増加しており、研究市場の成長を推進しています。

世界緑内障協会(WGA)の2022年の最新情報によると、2020年には約7,960万人が緑内障を抱えており、その数は2040年までに1億1,180万人に達すると予測されています。また、緑内障患者の少なくとも50%が緑内障に気づいていないことも強調しました。一部の新興諸国では、緑内障症例の約90%が検出されていません。したがって、緑内障の急増は最終的に、予測期間中に後眼部疾患市場を押し上げると予測されます。

新製品の発売、研究開発、コラボレーション、合併、買収により、後眼部疾患の市場は予測期間中に成長すると予想されます。たとえば、イリデックスコーポレーションは2022年 6月に、中国で緑内障治療用のCyclo G6プラットフォームを販売および販売するための規制当局の承認を国家医薬品局(NMPA)から取得しました。

眼疾患に対する意識の高まりと上記の要因により、後眼部疾患市場は予測期間中に健全な成長を記録すると予想されます。しかし、各国の厳しい規制政策や、発展途上国や低新興諸国における適切なヘルスケアインフラの欠如などの要因により、この成長は抑制される可能性があります。

後眼部疾患市場動向

医薬品セグメント別の小分子は、予測期間中にかなりの市場シェアを保持すると予想される

病気を治療するための生化学的プロセスを変化させることができる低分子量の化合物は、低分子薬として知られています。眼疾患の負担の増大、新しい治療法の革新のための研究開発の増加、製品の発売などの要因がセグメントの成長を推進しています。

国立医学図書館が2021年11月に発表した研究によると、2020年には世界中で約1億312万人の成人が糖尿病性網膜症を抱えて暮らしており、その数は2045年までに1億6,050万人に増加すると予測されています。したがって、眼疾患の負担は増大しています。治療に対する需要が増加する可能性が高く、このセグメントを牽引することになります。

この市場セグメントは、臨床研究の増加や市場関係者間の協力によっても後押しされています。たとえば、2021年12月にAbbVie Inc.(アラガン)は、老眼治療用として米国FDAからVUITY(塩酸ピロカルピン点眼液)1.25%の承認を取得し、米国の薬局で処方箋で入手できるようになりました。このような発売は、市場セグメントの成長を促進すると予想されます。したがって、小分子セグメントは予測期間中に成長すると予想されます。

北米は予測期間中に主要な市場シェアを保持すると予想される

北米は、確立されたヘルスケアインフラ、主要な市場企業の存在、新製品の発売、この地域における後眼疾患の負担の増加により、大幅な市場成長が見込まれています。

合併と買収の増加は、市場成長の主な理由の1つです。たとえば、2021年 11月にアルコンはIvantis Inc.を買収し、外科緑内障用のHydrusマイクロステントを追加することで製品ポートフォリオを拡大しました。 Hydrusマイクロステントはカナダの主要製品の1つです。この買収により、アルコンは市場での存在感を拡大しました。

2021年9月、Zilia Inc.はシードファイナンスを通じて316万米ドルを受け取りました。これにより、後眼部疾患の診断件数が増加し、同社の眼科診断分野への参入が促進されると思われます。この製品は、緑内障、糖尿病網膜症、加齢黄斑変性などの眼疾患の重要なバイオマーカーである眼の酸素飽和度を測定できます。

したがって、このような要因により、北米市場は予測期間中により速い成長を遂げると予想されます。

後眼部疾患業界の概要

後眼部疾患の市場は適度に細分化されています。市場関係者は、市場シェアを拡大するために、新製品の発売、製品イノベーション、地域拡大、コラボレーションに焦点を当てています。市場で活動している主要な市場企業には、F. Hoffmann-La Roche AG、Regeneron Pharmaceuticals Inc.、Rainbow Medical Ltd(Nano Retina)、Second Sight Medical、Merck &Co. Inc.が含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 増加する眼後部疾患の負担

- 後眼部疾患治療のための新たな治療法に向けた研究開発の拡大

- 市場抑制要因

- 厳格な規制政策

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- 薬物

- 低分子

- 生物製剤

- デバイス

- 治療機器

- 診断装置

- 薬物

- 用途別

- 黄斑変性症

- 緑内障

- 糖尿病性網膜症

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Alcon Inc.

- Abbvie Inc.(Allergen PLC)

- Bausch Health Companies Inc.

- F Hoffmann-La Roche

- Merck &Co. Inc.

- Novartis AG

- Santen Pharmaceuticals

- Rainbow Medical Ltd(Nano Retina)

- Regeneron Pharmaceuticals Inc.

- Second Sight Medical Products Inc.

- Aerie Pharmaceuticals

第7章 市場機会と将来の動向

The Posterior Segment Eye Disorders Market size is estimated at USD 32.12 billion in 2024, and is expected to reach USD 41.82 billion by 2029, growing at a CAGR of 5.42% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the research and development activities of other therapies and drugs for medical conditions other than COVID-19. It impacted the treatment procedures and supply chains of pharmaceuticals and medical devices worldwide and the market for posterior segment eye disorders. For instance, according to a health article published in March 2021 by Oftalmologaa Barraquer, COVID-19 caused severe and irreversible consequences for people with glaucoma who suffered a very rapid evolution of the disease and have not been able to carry out follow-ups by the specialist, which, in some cases, resulted in a loss of the visual field. Therefore, the overall impact of COVID-19 on the posterior segment eye disorders market was adverse, primarily due to the decline in the diagnostics and treatment procedures of the diseases associated with the posterior segment of the eye. However, the rise in eye disorder surgeries worldwide to clear the backlogs of surgical procedures caused by the pandemic-related restrictions compensated for the market's growth in the later phase of the pandemic.

Posterior segment eye disorders are one of the major causes of visual impairments worldwide. Their prevalence is increasing gradually due to the increase in the prevalence of eye diseases, diabetes, and geriatric populations that are more vulnerable to eye ailments. With the increase in the burden of these diseases, the demand for diagnostics and treatment is increasing worldwide, driving the growth of the studied market.

According to the World Glaucoma Association (WGA) 2022 update, around 79.6 million people were living with glaucoma in 2020, and the number is projected to reach 111.8 million people by 2040. It also highlighted that at least 50% of glaucoma sufferers are unaware of their condition, and around 90% of glaucoma cases in some developing countries are undetected. Thus, the surge in glaucoma is ultimately projected to boost the posterior segment eye disorders market over the forecast period.

With the launch of new products, research and development, collaboration, mergers, and acquisitions, the market for posterior segment eye disorders is expected to grow during the forecast period. For instance, in June 2022, Iridex Corporation received regulatory approval to market and sell its Cyclo G6 platform for the treatment of glaucoma diseases in China from its National Medical Products Administration (NMPA).

Due to the rising awareness about eye disorders and the factors mentioned above, the posterior segment eye disorders market is expected to register healthy growth over the forecast period. However, factors such as stringent regulatory policies of different countries and the lack of proper healthcare infrastructure in developing and under-developing countries are likely to restrain this growth.

Posterior Segment Eye Disorders Market Trends

Small Molecules by Drugs Segment is Expected to Hold a Significant Market Share Over the Forecast Period

Compounds with a low molecular weight that can change the biochemical processes for treating diseases are known as small-molecule drugs. Factors such as the growing burden of eye disorders, increasing R&D for the innovation of new therapeutics, and the launch of products are driving segmental growth.

As per the study published in November 2021 by the National Library of Medicine, around 103.12 million adults were living with diabetic retinopathy globally in 2020, and the number is projected to increase to 160.50 million by 2045. Thus, the growing burden of eye disorders is likely to increase the demand for their treatment, thus driving the segment.

The market segment is also boosted by increasing clinical studies and collaboration among the market players. For instance, in December 2021, AbbVie Inc. (Allergan) received approval for VUITY (pilocarpine HCl ophthalmic solution) 1.25% by the US FDA to treat presbyopia and be available by prescription in pharmacies in the United States. Such launches are expected to drive the growth of the market segment. Thus, the small molecules segment is expected to project growth over the forecast period.

North America is Expected to Hold a Major Market Share Over the Forecast Period

North America is anticipated to have significant market growth owing to its well-established healthcare infrastructure, the presence of key market players, new product launches, and the rising burden of posterior eye disorders in the region.

The growing mergers and acquisitions are one of the key reasons for the market's growth. For instance, in November 2021, Alcon acquired Ivantis Inc. to expand its product portfolio by adding the Hydrus micro stent for surgical glaucoma. Hydrus micro stent is one of the key products in Canada. With this acquisition, Alcon expanded its presence in the market.

In September 2021, Zilia Inc. received USD 3.16 million through seed financing. This would aid the company's entry into ocular diagnostics by increasing the number of posterior segment eye disorders diagnoses. The product can measure oxygen saturation in the eye, an important biomarker for eye diseases such as glaucoma, diabetic retinopathy, and age-related macular degeneration.

Hence, owing to such factors, the North American market is expected to have faster growth over the forecast period.

Posterior Segment Eye Disorders Industry Overview

The market for posterior segment eye disorders is moderately fragmented. Market players are focusing on new product launches, product innovation, regional expansions, and collaborations to increase their market share. The key market players operating in the market include F. Hoffmann-La Roche AG, Regeneron Pharmaceuticals Inc., Rainbow Medical Ltd (Nano Retina), Second Sight Medical, and Merck & Co. Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Burden of Back of the Eye Disorders

- 4.2.2 Growing R&D for New Therapies for the Treatment of Posterior Segment Eye Disorders

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Policies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Drugs

- 5.1.1.1 Small Molecules

- 5.1.1.2 Biologics

- 5.1.2 Devices

- 5.1.2.1 Therapeutic Devices

- 5.1.2.2 Diagnostic Devices

- 5.1.1 Drugs

- 5.2 By Application

- 5.2.1 Macular Degeneration

- 5.2.2 Glaucoma

- 5.2.3 Diabetic Retinopathy

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Alcon Inc.

- 6.1.2 Abbvie Inc. (Allergen PLC)

- 6.1.3 Bausch Health Companies Inc.

- 6.1.4 F Hoffmann-La Roche

- 6.1.5 Merck & Co. Inc.

- 6.1.6 Novartis AG

- 6.1.7 Santen Pharmaceuticals

- 6.1.8 Rainbow Medical Ltd (Nano Retina)

- 6.1.9 Regeneron Pharmaceuticals Inc.

- 6.1.10 Second Sight Medical Products Inc.

- 6.1.11 Aerie Pharmaceuticals