医療機器コネクティビティ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Medical Device Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1850235

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

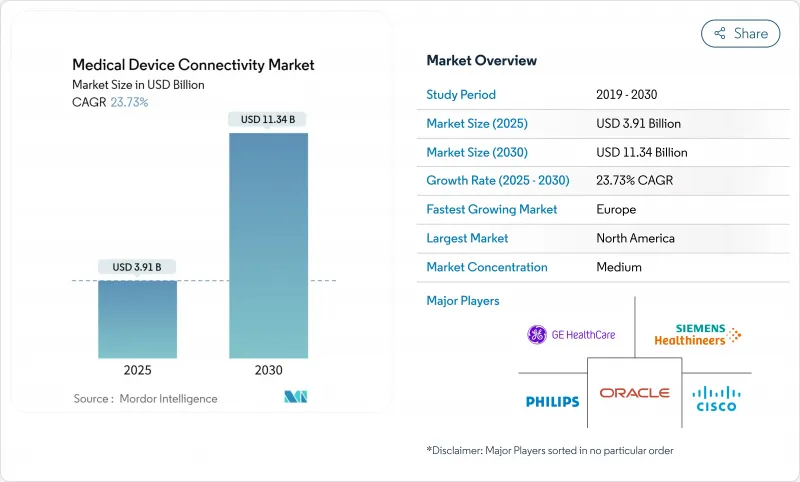

医療機器コネクティビティの世界市場規模は2025年に39億1,000万米ドルに達し、2030年には113億4,000万米ドルに達すると予測され、CAGRは23.73%を記録します。

ヘルスケアの急速なデジタル化、臨床医の作業負荷の増大、バリューベースの診療報酬への移行により、機器とシステムのシームレスなデータ交換に対する需要が高まっています。ヘルスケアプロバイダーは、独自のプロトコルをオープンスタンダードに置き換えることで、情報の遮断によるペナルティを緩和し、文書化にかかる時間を短縮しようとしています。専門医不足の深刻化によりTele-ICUプログラムが拡大する一方、急性期、外来、在宅の各セッティングにまたがる継続的なモニタリングが再入院を減らし、ケア連携を向上させています。規制当局がサイバーセキュリティの監視を強化し、6Gの研究がクリティカルケアアプリケーションのための超高信頼性、低遅延ワイヤレスリンクを約束する中、安全な接続アーキテクチャへの投資が加速しています。

世界の医療機器コネクティビティ市場の動向と洞察

EMR相互運用性の義務化とデジタルヘルス政策

21世紀治療法(21st Century Cures Act)によって義務付けられた標準化APIは、独自プロトコルからFHIRベースの交換への移行を余儀なくしています。コンプライアンス・プログラムを完了した医療システムは、文書化時間を13%短縮し、ケア連携を改善し、接続エンジンの幅広い展開を促しています。機器メーカーは現在、コストのかかる後付けサイクルを回避し、接続性の安全対策をますます重視するFDAの認可プロセスを加速するために、新製品に相互運用性を設計しています。

リアルタイムデータを要求する成果ベースの償還

CMSの代替支払いモデルは、収益を臨床転帰にリンクさせるものであり、病院は、患者の悪化を早期に察知する継続的モニタリングとエッジ分析機能を備えたベッドを導入するよう促しています。コネクテッドRPMプラットフォームを使用している医療システムでは、心不全の再入院が24%減少したと報告されており、財政と質のインセンティブが一致しています。このビジネスケースは、集中治療室、脳卒中病棟、腫瘍輸液センターで最も効果的です。

データ標準のない異種レガシー機器群

病院は輸液ポンプ、人工呼吸器、モニターを8年以上のライフサイクルで運用していることが多く、その多くはパッチ適用可能なオペレーティングシステムを備えていません。インターフェース・エンジンは、ベンダー固有のプロトコルを翻訳する必要があり、プロジェクトのスケジュールを増やし、継続的なメンテナンスを要求します。絶縁ネットワークは脆弱なエンドポイントを保護しますが、配線が重複するため、拡張プロジェクトにコストと複雑さが加わります。

セグメント分析

コネクティビティ・ソリューションは2024年の売上高の63.67%を占め、異種機器データを正規化し、急速に進化する相互運用性ルールを実施するためのバックボーンとして確立しました。これらのプラットフォームは、HL7v2、FHIR、および独自のストリームを、臨床意思決定支援エンジンに供給するEHR対応のペイロードに変換します。Mirth Connectのようなベンダーニュートラルなゲートウェイはオープンソースの柔軟性を提供し、エンタープライズ・スイートはデバイスライブラリ、アラーム管理、分析モジュールをバンドルしています。医療システムは冗長サーバークラスタを導入し、高度急性期病棟のダウンタイムをほぼゼロに保ちます。更新サイクルが加速するにつれ、医療機器コネクティビティ市場では、輸液ポンプ、麻酔器、ワイヤレス遠隔測定パックのためのすぐに使えるアダプタを提供するソリューションがますます好まれるようになっています。

接続サービスは、病院が導入、保守、サイバーセキュリティパッチを外注することにより、年間26.12%の成長が予測されます。マネージドサービス契約は、アップタイムを保証し、プロバイダーを人員不足から守り、コンプライアンス文書が最新であることを保証します。中小規模の施設では、資本支出を予測可能な運用コストに変換するサブスクリプションモデルが選ばれています。サービス会社は、インターフェイスのチューニング、24時間365日の監視、マルチベンダーエステートにわたる変更管理ガバナンスをバンドルしています。この動向は、サービス・サブセグメントを、より広範な市場セグメンテーションの中で重要な収益促進要因として位置づけています。

有線リンクは、2024年の売上高の57.92%を占め、クリティカルケアや手術室におけるシールド・イーサネット・バックボーンがその中心となっています。リアルタイムの波形忠実度と既知の遅延プロファイルにより、高帯域幅の生命維持装置には有線ネットワークが不可欠です。手術室の再配線は臨床スループットを中断させ、厳密な検証を必要とするため、交換サイクルは遅いです。それでも、病院がコアスイッチをパワーオーバーイーサネット対応にアップグレードすることで、コンセントの増設なしに将来の機器クラスが可能になり、医療機器コネクティビティ市場における有線インフラの関連性が高まる。

無線技術は、5Gのアップグレードとミリ秒以下のレイテンシを約束する6Gの調査により、CAGR 25.86%の上昇が見込まれます。アクセスポイント密度は、テレメトリーベルト、ウェアラブルECGパッチ、姿勢や転倒データを送信するスマートベッドをサポートするために一般病棟で増加しています。Wi-Fi 6Eの導入により、レガシー干渉のない新たな周波数帯が確保され、プライベート5Gスライスにより、モバイルCTスキャナーやラピッドレスポンスカート向けに確定的なサービス品質が提供されています。病院では、点滴ポンプが自動的にSSIDを切り替えるため、病棟の境界で手動で再接続する必要がなくなり、患者の移動がスムーズになったと報告しています。これらのイノベーションは、ワイヤレスが医療機器コネクティビティ市場のモビリティ・エンジンであることを裏付けています。

地域分析

北米は、成熟したEHRの普及、厳格な相互運用性の実施、エッジ分析の早期導入により、2024年の売上高の38.58%を占めました。情報遮断に対するCMSの罰則と新たなAPI義務化により、プロバイダーはベッドサイド機器と支払者ポータルをシームレスに接続する標準ベースのゲートウェイの導入を余儀なくされています。学術医療センターは、継続的モニタリングと予測スコアリングを融合させたAI拡張監視を試験的に導入し、高スループット接続ハブの調達を加速させる。デジタルヘルス新興企業へのベンチャー投資は、医療機器コネクティビティ市場の地域的足跡をさらに拡大します。

アジア太平洋地域は2025年から2030年にかけて年間26.73%拡大すると予測されており、これは世界最速です。中国は、プライベート5G、ロボット工学、クラウドPACS統合を特徴とするスマート病院の設計図を拡大し、インドは、生産連動型インセンティブ制度により、当初からオープンスタンダードなインタフェースを組み込んだ国産機器メーカーを育成しています。日本では、暗号化されたVPNを介した県をまたいだ診察に払い戻しを行う政府の刺激策を活用し、遠隔脳卒中ネットワークで地方の診療所をアップグレードします。韓国とオーストラリアは、データ中心のヘルスケア・パイロットを奨励し、ワイヤレス遠隔測定とAIトリアージ・アルゴリズムのための肥沃な土壌を作り出しています。こうした力学により、同地域は医療機器コネクティビティ市場の重要な成長エンジンとして位置付けられています。

欧州のCAGRは21.54%と予測され、相互運用性とサイバーセキュリティを強化する医療機器規制と一般データ保護規制に支えられています。ドイツは、病院未来法に基づき病院のデジタル成熟度のアップグレードを助成し、HL7-FHIRゲートウェイの調達を加速させています。英国はNHS信託にデジタル成熟度評価を義務付け、安全なデバイスオンボーディングのための資金を確保します。北欧諸国は臨床使用のための6G研究テストベッドを開拓し、汎EUイニシアチブは欧州医療データスペースを通じて国境を越えたデータ交換を奨励しています。プライバシーとセキュリティへの強い関心がベンダーの選択を形成し、病院はゼロトラスト設計ときめ細かな同意管理を提供するプラットフォームを好みます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EMR相互運用性の義務とデジタルヘルス政策

- リアルタイムデータを必要とする成果に基づく償還

- 遠隔および在宅での慢性疾患モニタリングの拡大

- IoTサイバーセキュリティフレームワークの融合

- マルチパラメータウェアラブルおよびインプラントデバイスの普及

- 予測的な臨床洞察を可能にするクラウドネイティブ分析

- 市場抑制要因

- データ標準のない異機種混在のレガシーデバイス群

- 初期統合とインターフェースエンジンのコストが高め

- サイバーセキュリティと患者のプライバシーに関する脆弱性が依然として存在

- ワークフローの調整が限定的であるため、医師の抵抗が生じる

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- コンポーネント別

- 接続ソリューション

- インターフェースエンジンと統合プラットフォーム

- 接続ハブとゲートウェイ

- デバイスインターフェースモジュール

- 接続サービス

- 実装と統合

- サポートとメンテナンス

- コンサルティングとトレーニング

- 接続ソリューション

- 技術別

- 有線

- 無線

- ハイブリッド

- 用途別

- 継続的な患者モニタリング

- 遠隔ICUと遠隔脳卒中

- 画像およびPACS接続

- 投薬管理とスマートIVポンプ

- 麻酔と人工呼吸器

- その他の用途

- エンドユーザー別

- 病院とクリニック

- 外来手術および専門センター

- 在宅ヘルスケア環境

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- Competitive Benchmarking

- 市場シェア分析

- 企業プロファイル

- Ascom Holding AG

- Baxter International Inc

- Cisco Systems Inc.

- Digi International Inc.

- Dragerwerk AG & Co. KGaA

- GE HealthCare Technologies Inc.

- Honeywell International Inc.

- ICU Medical

- Koninklijke Philips N.V.

- Lantronix Inc.

- Masimo Corporation

- Medtronic plc

- Mindray Medical International Limited

- NantHealth, Inc.

- Nihon Kohden Corporation

- Oracle Corporation

- S3 Connected Health

- Siemens Healthineers AG

- Spectrum Medical Ltd

- Stryker Corporation

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日